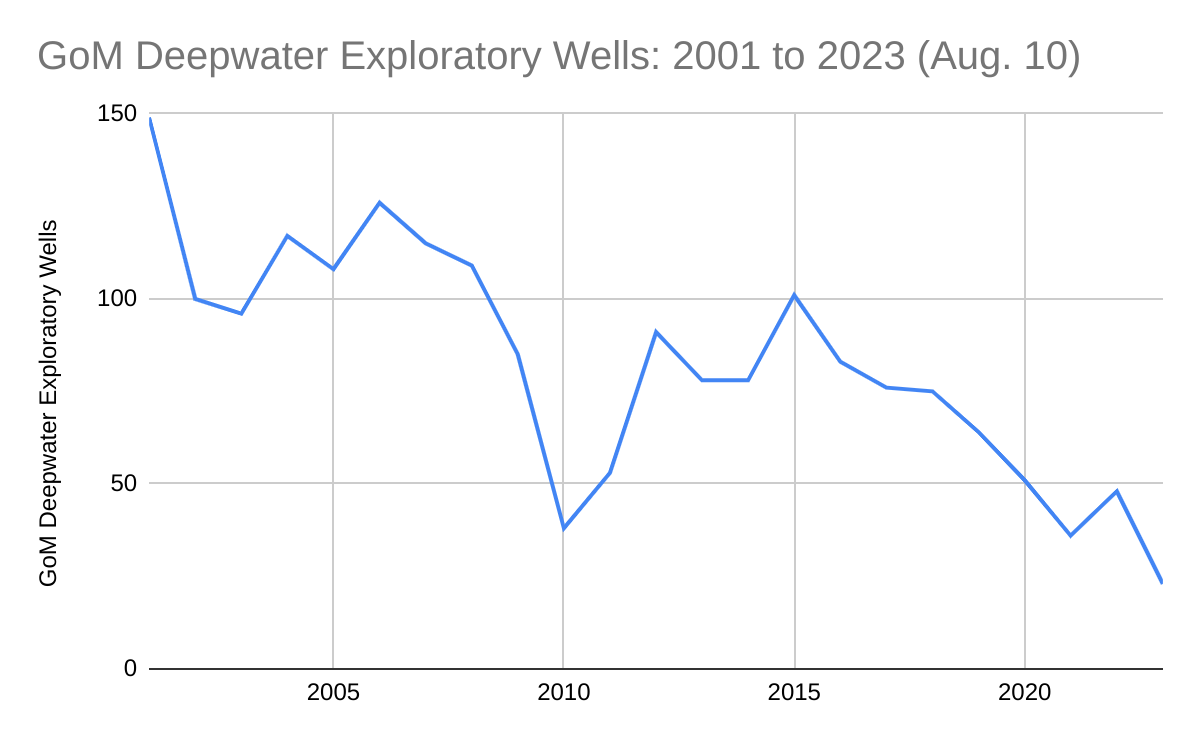

Record low exploratory drilling: 2023 will be the third consecutive year with fewer than 50 deepwater exploratory well starts. The only other year this century with <50 deepwater exploratory well starts was 2010 when there was a post-Macondo drilling moratorium.

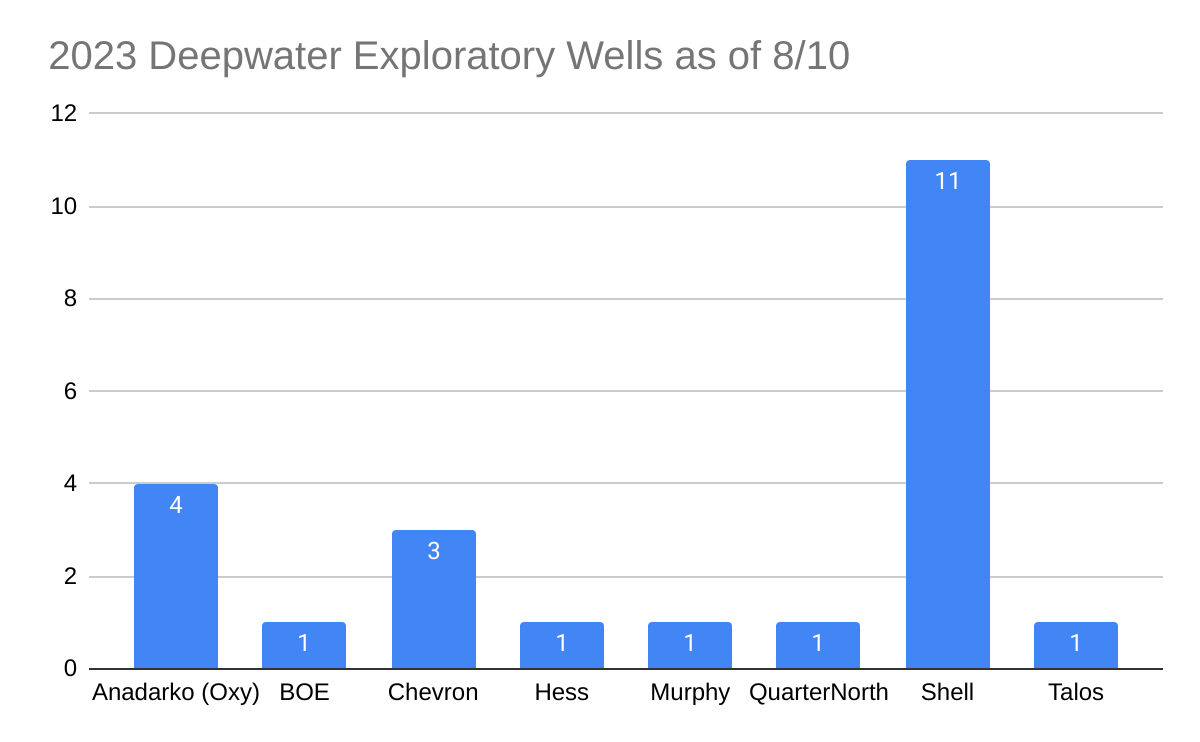

Low participation: Only 8 companies have started deepwater exploratory wells in 2023 YTD. Anadarko, Chevron, and Shell drilled 78% of the wells, with Shell alone accounting for 48%. Compare these numbers with 2001, when 24 companies drilled 149 deepwater exploratory wells.

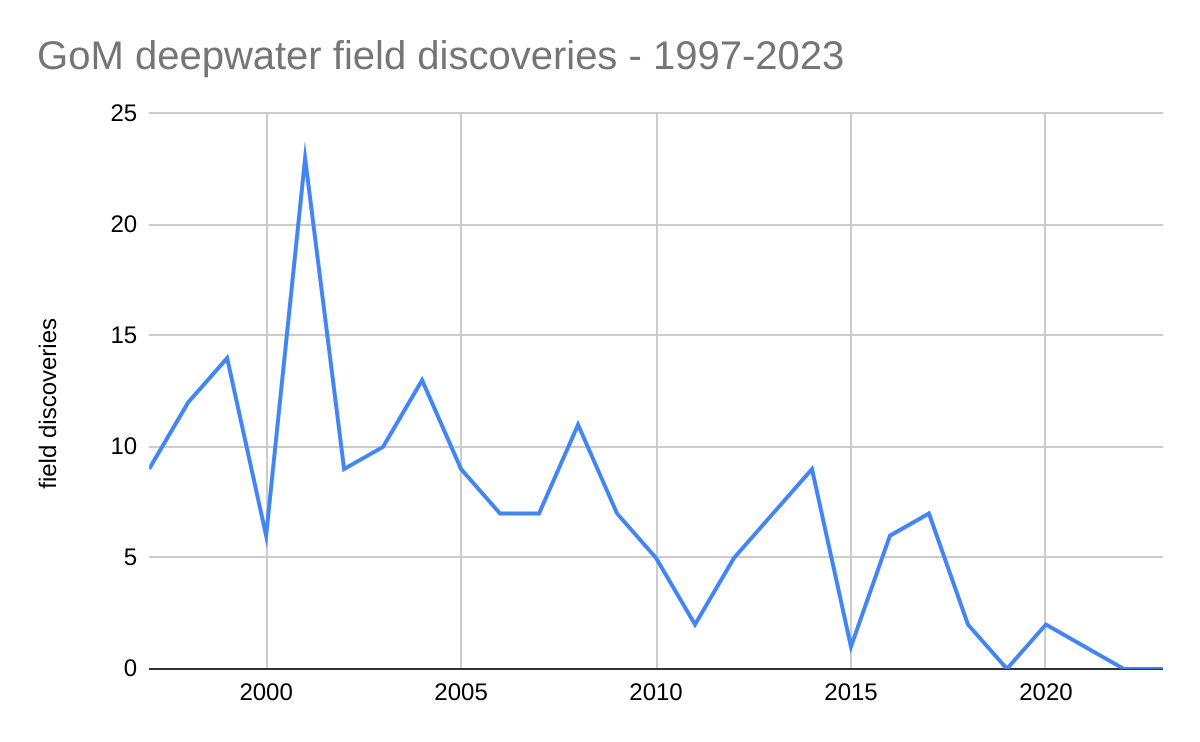

Absence of new field discoveries: Per BOEM’s database, no deepwater fields have been discovered since March 2021 and there were only 3 discoveries in the past 5 years (see chart below)

Leasing and regulatory uncertainty: When will the 5 year leasing plan be finalized and how much will leasing be restricted? What will be the effect of the expanded Rice’s whale area on deepwater operations? To what extent is this expansion justified? What other legal and regulatory threats are on the horizon?

Unrealistic expectations regarding the “energy transition:” In a stunning introductory statement, the Proposed 5 Year Leasing Plan expressed concerns that new leases would produce too much oil and gas for too long. OPEC+ must love the way the US sanctions its own energy production, most notably the oil and gas resources of the OCS. More than 96% of the OCS is off-limits to oil and gas leasing, and the 5 year plan proposed to constrain leasing in the only areas that remain. The favored offshore wind program was intended to be a complement to, not a replacement for, the oil and gas program. Wind energy is limited by intermittency, space preemption, navigation, and wildlife protection concerns.

Some companies have visions of the GoM as a carbon dumping hub: The largest US oil company, which hasn’t drilled a well in the GoM in nearly 4 years and operates just one production platform, seeks praise and profit by sequestering CO2 beneath the Gulf while maximizing oil production elsewhere. How will this sustain economically and strategically important GoM oil and gas production?

The paper is short on facts and long on dogma and political rhetoric, but is not entirely without merit. The author acknowledges, albeit in a backhanded manner, the massive social benefits that fossil fuels have provided (quote below). Would our economy have been strong enough to support academic pursuits such as hers were it not for fossil fuels and “petro-masculine” ingenuity and labor?

“Fossil fuels built the modern world. There remains an appreciation for fossil fuels – or, at least, for the high energy consumption they provided – as a catalyst of mass liberal democracy. This is evident in ecomodernist calls for a good Anthropocene that would decouple the benefits of fossil fuels from the fuels themselves. After all, while industrialisation wreaks planetary destruction, its spread was coterminous with humanist victories like the abolition of slavery, increased literacy rates, gender equality and poverty reduction. Dipesh Chakrabarty notes that this cannot be a coincidence, and that ‘the mansion of modern freedoms stands on an ever-expanding base of fossil-fuel use. Most of our freedoms so far have been energy-intensive.“

“The 19th century is known as the “century of coal,” but, as the technology scholar Vaclav Smil has noted, not until the beginning of the 20th century did coal actually overtake wood as the world’s No. 1 energy source. Moreover, past energy transitions have also been “energy additions”—one source atop another. Oil, discovered in 1859, did not surpass coal as the world’s primary energy source until the 1960s, yet today the world uses almost three times as much coal as it did in the ’60s.“

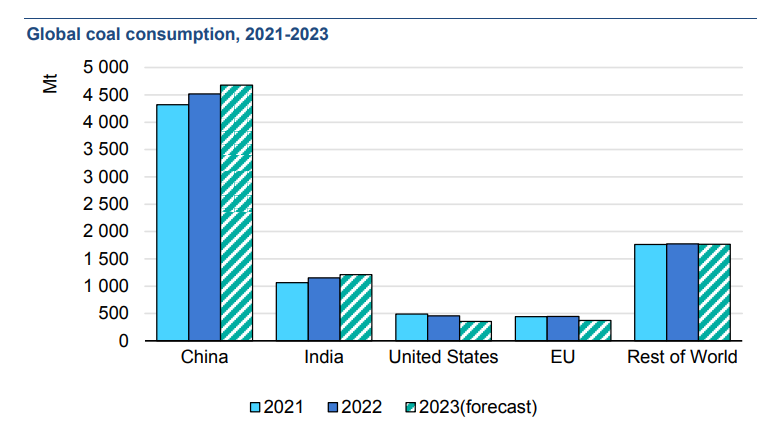

Coal is not going away. Per IEA, coal consumption in 2022 set a new record (8.3 billion tonnes) and will stay at or near that level in 2023 and 2024. See the chart below for 2021, 2022, and 2023 (est.) consumption in million tonnes. India and China are joined by the “Rest of the World” (outside the US and EU) in the billion tonne club.

Message: Coal is cost effective and reliable, and will continue to be a major source of energy.

WASHINGTON, Aug 1 (Reuters) – The Biden administration has pulled an offer to buy 6 million barrels of oil for the Strategic Petroleum Reserve, an Energy Department spokesperson said on Tuesday, as oil prices are expected to keep rising after a output cut from Saudi Arabia.

So much for adding a few drops to the SPR bucket. When your reserve is down 380 million barrels in a seller’s market, you don’t have a lot of purchasing leverage. Don’t expect much of an SPR refill anytime soon. It’s easy to deplete strategic assets; much more difficult to replace them.

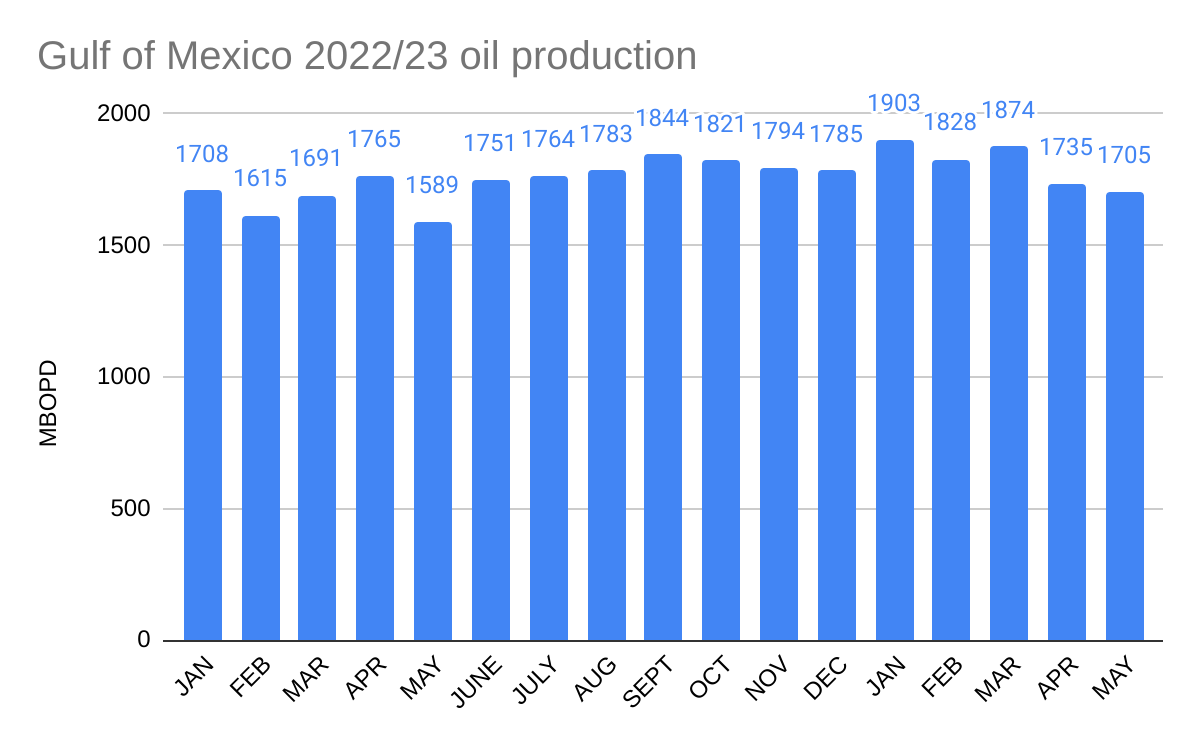

Gulf of Mexico 2023 oil production has dipped over the past 2 months, and is down 10% since January.

2023 production is reasonably well aligned with the EIA forecast which shows new production being offset by declines in existing fields.

Last year, BOEM forecast that production would average 2.0 million bopd in 2023. That forecast was justification for curtailing BOEM’s Proposed 5 Year Leasing Program. For the first time in the history of the OCS program, the primary concern of the program managers was that production might be too high for too long! This stunning quote from the 5 year leasing plan explains why so few lease sales were proposed:

“BOEM’s short-term (20-year) production forecast for existing leases shows steady growth from 2022 through 2024 and declining thereafter (see Section 5.2.1). The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“

Attached is a settlement agreement between NOAA and 4 NGOs that could have major implications for deepwater oil and gas operations in the Gulf of Mexico.

As background, the Rice’s Whale (formerly Bryde’s whale) area has been expanded (see map above) such that it fences off deepwater leases by creating a barrier to vessel transportation. The expansion is based on a single study that concluded that Rice’s whales were “the most plausible explanation” for moan calls observed in the northwest GOM shelf break area. No Brice’s whales were sighted in the expanded area during this study. The authors do point to a 2017 sighting offshore Corpus Christi, which is apparently the only actual sighting of a Brice’s whale along the NW GoM shelf break.

The settlement agreement commits BOEM, presumably with their concurrence, to exclude the expanded area from future leasing, to issue a Notice to Lessees and Operators (exhibit 1 below) and to attach stipulations to new leases (exhibit 2). Because BOEM’s authority to impose major new requirements without proposing a regulation for public review and comment is questionable, the Notice (NTL) describes the restrictions as “recommended measures.” However, the liability risks associated with the failure to comply with this “guidance” would be unacceptable to most companies. Adding to the muddle, the language in the lease stipulation differs by making it perfectly clear that compliance is required.

The most troubling restriction from an operational standpoint:

“To the maximum extent practicable, lessees and operators should avoid transit through the Expanded Rice’s Whale Area after dusk and before dawn, and during other times of low visibility to further reduce the risk of vessel strike of Rice’s whales.“

Comments:

Deepwater facilities are typically far from shore, and a requirement to transit only between dusk and dawn, particularly in the winter, is unrealistic and onerous. This is further complicated by the speed limit provision.

Those who have worked offshore know that periods of low visibility are unpredictable and can extend for days. The low visibility transit restriction is thus highly punitive and increases operational risks on the vessels and at the facilities they serve.

The vague “to the maximum extent practicable” caveat provides little comfort for planners, managers, and crews, and is a de facto acknowledgement that the requirement is unreasonable.

These restrictions, coupled with the required Automatic Identification System data, open the door to endless challenges, especially given the keen interest of the litigious organizations that are parties in the settlement agreement.

Deepwater GoM operations are few in number and highly dispersed, which is a more important mitigating factor than those included in the agreement. More on this tomorrow.

In addition to the deepwater operations that will be much more difficult to supply, there are currently 81 production platforms within the expanded Rice’s whale area (100 to 400 m water depth).These include important facilities like Amberjack, Cognac, Cerveza, and Lobster. What are the implications for these platforms? Will they be required to have full-time whale observers? Can they only be supplied during daylight hours with good visibility? Why not consider using these platforms as bases for more definitive studies?

Further to the previous point, there are 103 existing leases in the 100-400 m depth zone that is now excluded from leasing? 90 of these leases are still in their primary term, and 21 were issued in the past 2 years. How will the contractual rights of these leaseholders be protected? (In fact, the value of all 1550 active leases in >100 m water depth is affected by this agreement.)

Have BSEE and Coast Guard been consulted on the practicality and safety implications of these requirements?

Deepwater operations have been ongoing in the GoM for 50 years, and there is no apparent evidence of impacts to this species. Why can’t the consultation process and any necessary followup studies be completed before decisions are made regarding operating restrictions?

Finally, BOEM’s third footnote in the NTL (pasted below), doesn’t demonstrate great confidence in the need for the onerous requirements that are being imposed.

“This is not meant to be construed as a blanket determination as to whether BOEM, at present, has determined that there is a “reason to believe” that incidental take may occur, within the meaning of the ESA, the consultation regulations, or BOEM’s regulations. Those decisions will be made on a case-by-case basis in accordance with BOEM regulations referenced below.” Comment: Huh??? How are these blanket restrictions case-by-case, and how are they being imposed without public review?

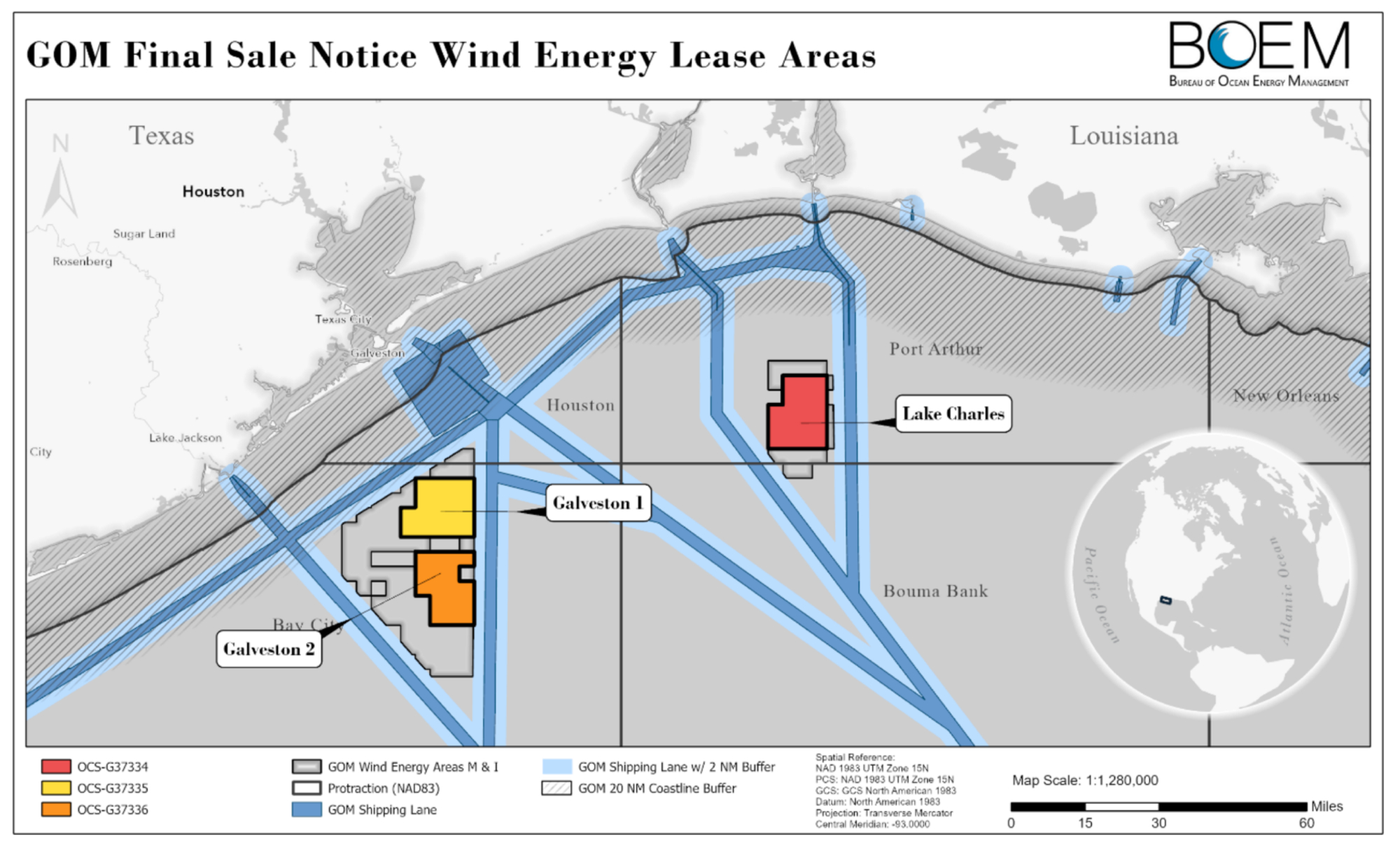

BOEM’s Final Sale Notice for the upcoming Gulf of Mexico wind auction identifies 3 lease areas (see map below). Wind operations in these areas should not significantly conflict with other GoM activities, including oil and gas operations.

Those who followed Exxon’s recent lease acquisitions may be amused by the map below from BOEM’s siting analysis document. The 94 Exxon leases acquired at Oil and Gas Lease Sale 257 (yellow blocks) are misidentified as “Carbon Capture Lease Blocks.” As has been discussed at length on this blog (most recently here), Sales 257 and 259 were oil and gas lease sales. Although Exxon’s intentions are now well known, they may not conduct carbon sequestration operations on these leases unless they are competitively reissued or converted. (Is BOEM’s siting document implying that conversion of the Exxon leases is a fait accompli?) The regulations for such conversions, and for CCS operational activities, have yet to be promulgated. A draft of these regulations is expected later this year, and the comments should be spirited and diverse.

ENERGYWIRE has reported that the Department of the Interior will publish the legislatively mandated carbon sequestration rule later this year. Given that even close followers of the OCS program were completely unaware of the enabling legislative provisions prior to their enactment, the proposed DOI rule will provide the first opportunity to formally comment.

Within the oil and gas industry and the environmental community, there are considerable differences of opinion about carbon sequestration in general, and more specifically, offshore sequestration. All interested parties are encouraged to submit comments on these important regulations.

Some background information on the sequestration legislation and subsequent actions:

amend the OCS Lands act to authorize “the injection of a carbon dioxide stream to sub-seabed geologic formations for the purpose of long-term carbon sequestration.”

exempt CO2 injection from the restrictions on ocean dumping by stipulating that such injection “shall not be considered to be material (as defined in section 3 of the Marine Protection, Research, and Sanctuaries Act of 1972.” Without this exemption, CO2 streams would clearly be “material,” as defined in 33 U.S.C. 1402, and would be subject to the stringent requirements of that act.

direct that “not later than 1 year after the date of enactment of this Act, the Secretary of the Interior shall promulgate regulations to carry out the amendments made by this section.” (This deadline has been missed, which is rather common for such directives.)

3/29/23: Exxon bid at Sale 259 on 69 nearshore tracts with little oil and gas potential. Once again, this was strictly an oil and gas lease sale and Exxon’s CCS intentions were clear. Nonetheless, the leases were awarded.

Exxon and other companies intend to commercialize carbon sequestration, and Exxon projects an astounding $4 trillion CCS market by 2050. Such a market will of course be dependent on mandates and subsidies, and the costs will ultimately be borne by taxpayers and consumers.

Is it not a bit unsavory and hypocritical for hydrocarbon producers to capitalize on the capture and disposal of emissions associated with the consumption of their products? Perhaps companies that believe oil and gas production is harmful to society should exit the industry, rather than engage in enterprises that sustain it.

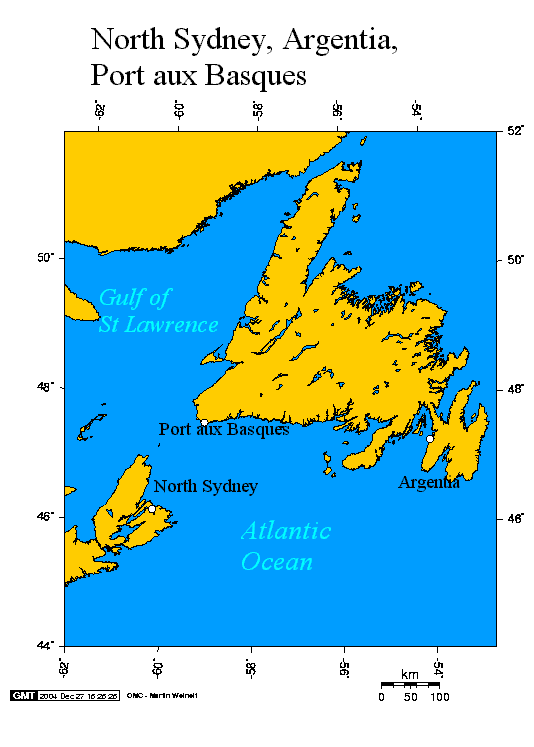

The Jones Act, protectionism at its finest, was enacted 113 years ago, and stipulates that vessels which transport merchandise or people between two US points must be US built, flagged, owned, and crewed. Congress tightened the screws further by ordaining that offshore energy facilities, including wind farms, are US points. That precludes the transportation of wind turbine components from US ports to offshore wind farms.

The Jones Act has thus provided an opportunity for the Port of Argentia, a former US Navy base in southeast Newfoundland, and the port is set to become a key node in the offshore wind supply chain. Monopiles constructed in Europe will be stored in Argentia, until they are delivered to US wind farms in the North Atlantic. Kudos to the folks at the Port of Argentia for taking advantage of this opportunity.

Dutch company Boskalis will be transporting the monopiles, which are expected to land in the Port of Argentia in a few weeks. (Boskalis)