The plaintiffs assert “insufficient and arbitrary environmental analyses, in violation of the National Environmental Policy Act (NEPA) and the Administrative Procedure Act (APA).” The court filing is attached.

All of this will have to be resolved in the next 3 weeks, as the congressionally mandated sale, scheduled for 27 September, (presumably) cannot be postponed.

Unsurprisingly, Orsted management assumes no responsibility for the company’s poor performance, blaming supply chain problems, high interest rates and “a lack of new tax credits.” Outsiders might suggest that there were other factors such as irrational exuberance in the acquisition of wind leases at inflated prices, and unrealistic expectations regarding a complementary power source that is dependent on government mandates and subsidies.

“The situation in U.S. offshore wind is severe,” Chief Executive Mads Nipper told reporters on a conference call.

The expanded Rice’s whale area is based on a single 2022 study that concluded that Rice’s whales were “the most plausible explanation” for moan calls observed in the northwest GoM shelf break area. No Brice’s whales were sighted in the expanded area during this study. Is this sufficient basis for restrictions that threaten operations that are critical to our economy?

Stipulations are part of the lease contract and can be difficult to modify, even when the lessor and lessee are in agreement.

Why not rely on voluntary measures until further studies have been completed? The offshore industry has a good record of cooperation with the government to protect sensitive biological resources. The Flower Garden Banks is a good example of such cooperation.

In addition to the lease stipulation, the entire expanded Brice’s whale area has been excluded from the lease sale. Senator Manchin strongly criticized that decision:

Let me be clear, the exclusion of more than 6 million productive acres from the upcoming offshore oil and gas lease sale in the Gulf of Mexico based on a settlement reached in the name of protecting Rice’s whale while conveniently only targeting oil and gas is yet another example of this Administration’s intentional undermining of the strong energy security provisions in the Inflation Reduction Act.

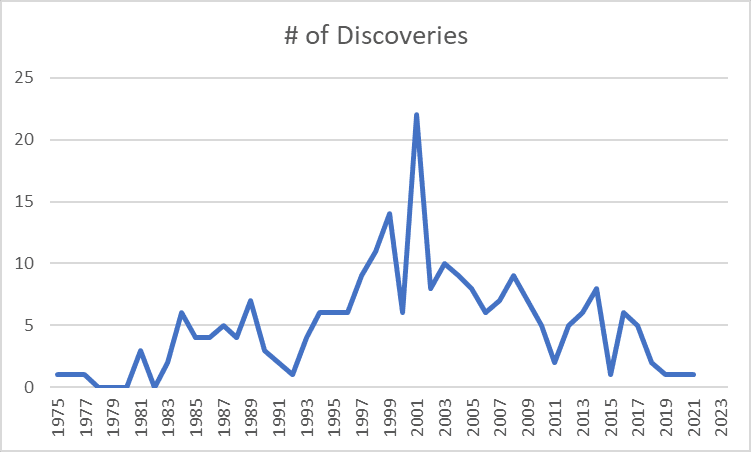

Per our previous post, “Ominous signs for the future of Gulf of Mexico production,” Lars Herbst has plotted (below) deepwater GoM field discoveries dating back to the early days of deepwater drilling operations.

These are official USGS, MMS, and BOEM data (depending on the era) for field discoveries in >1000′ of water. Note that the last discovery was in March 2021.

This is a discouraging graphic given that the deepwater GoM is currently the only option for significant new US offshore production.

Attached is a settlement agreement between NOAA and 4 NGOs that could have major implications for deepwater oil and gas operations in the Gulf of Mexico.

As background, the Rice’s Whale (formerly Bryde’s whale) area has been expanded (see map above) such that it fences off deepwater leases by creating a barrier to vessel transportation. The expansion is based on a single study that concluded that Rice’s whales were “the most plausible explanation” for moan calls observed in the northwest GOM shelf break area. No Brice’s whales were sighted in the expanded area during this study. The authors do point to a 2017 sighting offshore Corpus Christi, which is apparently the only actual sighting of a Brice’s whale along the NW GoM shelf break.

The settlement agreement commits BOEM, presumably with their concurrence, to exclude the expanded area from future leasing, to issue a Notice to Lessees and Operators (exhibit 1 below) and to attach stipulations to new leases (exhibit 2). Because BOEM’s authority to impose major new requirements without proposing a regulation for public review and comment is questionable, the Notice (NTL) describes the restrictions as “recommended measures.” However, the liability risks associated with the failure to comply with this “guidance” would be unacceptable to most companies. Adding to the muddle, the language in the lease stipulation differs by making it perfectly clear that compliance is required.

The most troubling restriction from an operational standpoint:

“To the maximum extent practicable, lessees and operators should avoid transit through the Expanded Rice’s Whale Area after dusk and before dawn, and during other times of low visibility to further reduce the risk of vessel strike of Rice’s whales.“

Comments:

Deepwater facilities are typically far from shore, and a requirement to transit only between dusk and dawn, particularly in the winter, is unrealistic and onerous. This is further complicated by the speed limit provision.

Those who have worked offshore know that periods of low visibility are unpredictable and can extend for days. The low visibility transit restriction is thus highly punitive and increases operational risks on the vessels and at the facilities they serve.

The vague “to the maximum extent practicable” caveat provides little comfort for planners, managers, and crews, and is a de facto acknowledgement that the requirement is unreasonable.

These restrictions, coupled with the required Automatic Identification System data, open the door to endless challenges, especially given the keen interest of the litigious organizations that are parties in the settlement agreement.

Deepwater GoM operations are few in number and highly dispersed, which is a more important mitigating factor than those included in the agreement. More on this tomorrow.

In addition to the deepwater operations that will be much more difficult to supply, there are currently 81 production platforms within the expanded Rice’s whale area (100 to 400 m water depth).These include important facilities like Amberjack, Cognac, Cerveza, and Lobster. What are the implications for these platforms? Will they be required to have full-time whale observers? Can they only be supplied during daylight hours with good visibility? Why not consider using these platforms as bases for more definitive studies?

Further to the previous point, there are 103 existing leases in the 100-400 m depth zone that is now excluded from leasing? 90 of these leases are still in their primary term, and 21 were issued in the past 2 years. How will the contractual rights of these leaseholders be protected? (In fact, the value of all 1550 active leases in >100 m water depth is affected by this agreement.)

Have BSEE and Coast Guard been consulted on the practicality and safety implications of these requirements?

Deepwater operations have been ongoing in the GoM for 50 years, and there is no apparent evidence of impacts to this species. Why can’t the consultation process and any necessary followup studies be completed before decisions are made regarding operating restrictions?

Finally, BOEM’s third footnote in the NTL (pasted below), doesn’t demonstrate great confidence in the need for the onerous requirements that are being imposed.

“This is not meant to be construed as a blanket determination as to whether BOEM, at present, has determined that there is a “reason to believe” that incidental take may occur, within the meaning of the ESA, the consultation regulations, or BOEM’s regulations. Those decisions will be made on a case-by-case basis in accordance with BOEM regulations referenced below.” Comment: Huh??? How are these blanket restrictions case-by-case, and how are they being imposed without public review?

In 1979 Gulf of Mexico oil production had declined to 263 million barrels and many believed that further declines were inevitable. 40 years later, a record 693 million barrels were produced.

Onshore, lateral drilling and hydraulic fracturing capabilities are continuing. As a result, Exxon and others are predicting projecting higher recovery factors in the Permian Basin. Per Exxon CEO Darren Woods: “We are beginning to see the signs of some very promising new technologies that will significantly improve recovery.”

Opportunity + Ingenuity ➡ Energy Independence + Prosperity

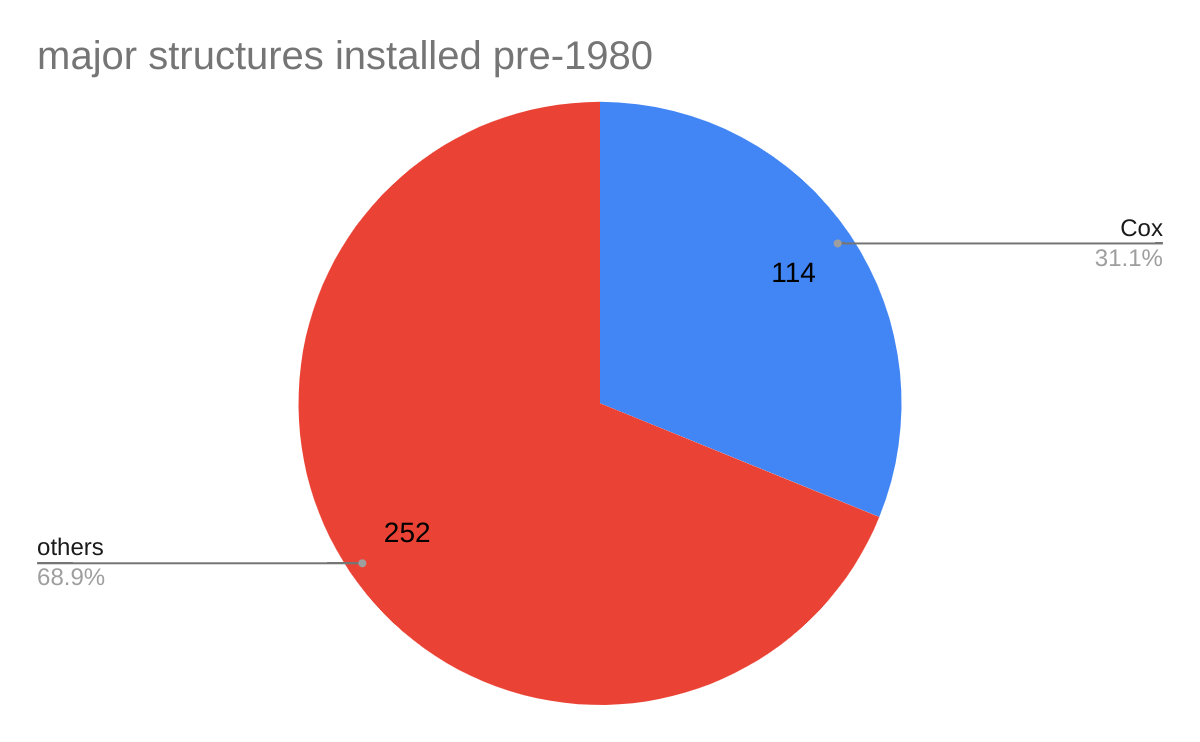

As illustrated in the charts below, Cox has the distinction of being the Gulf of Mexico (world?) leader in aging offshore platforms. Per BOEM data, Cox (includes affiliates Energy XXI GOM and EPL) operates more than 1/4 of all GoM platforms. 44% of these platforms were installed prior to 1980, 114 of which are major structures (defined in notes below). 27 of these major structures were installed prior to 1960!

Notes: (1) A major structure contains at least 6 well completions or more than 2 pieces of production equipment. (2) The platform numbers in an earlier post are incomplete in that they include only structures with helidecks.

A Metairie-based oil company that’s one of the largest independent operators still working in the state’s shallow coastal waters has filed for bankruptcy protection, leaving dozens of south Louisiana service and supply companies facing potential bankruptcies of their own.

Bankruptcy court documents show Cox’s estimated liabilities are close to $500 million – more than $200 million of which is owed to small businesses in the Houma-Thibodeaux and Acadiana areas.

Court documents indicate that Cox followed a path that led to financial trouble for other companies in recent years: using debt to acquire large fields of aging wells in shallow Gulf waters.

This blog is primarily concerned with the potential impacts of the bankruptcy on safety performance, the plugging of wells, and the decommissioning of old facilities. Per BOEM’s data base, Cox currently operates 276 Gulf of Mexico platforms, all in shallow shelf waters. The company is reported (Nola.com) to owe $8 million in bond premiums needed to support well plugging operations.

Cox has not been an active driller of late with only 2 well starts since 1/1/2022 (BSEE borehole file).

Cox has been a major generator of INCs (incidents of noncompliance) with 437 INCs YTD. Cox has been responsible for 47% of all GoM INCs in 2023. Cox’s INC to inspection ratio was 2.46 vs. a combined ratio of 0.50 (490/972) for all other GoM operators.

Cox is currently ranked 11th and 18th respectively in GoM gas and oil production with 7.2 billion cu ft and 1.8 million barrels produced YTD.