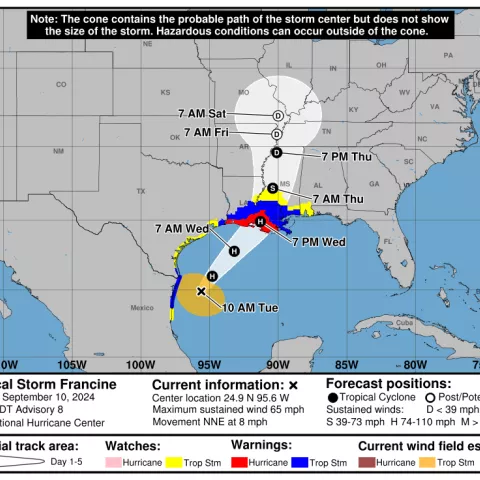

| Total Shut-in (Percentage of GOM Production) | ||

| Oil, BOPD Shut-in | 412,070 BOPD | 23.55% |

| Gas, MMCFD Shut-in | 494 MMCFD | 25.56% |

| Evacuations and rig movements | total | % of GOM |

| Platforms Evacuated | 130 | 35% |

| Rigs Evacuated (non DP) | 2 | 40% |

| DP Rigs Moved-off | 3 | 15% |

Posted in Gulf of Mexico, hurricanes, Offshore Energy - General, tagged evacuations, Gulf of Mexico, Hurricane Francine, production shut-in, rig movement on September 10, 2024| Leave a Comment »

| Total Shut-in (Percentage of GOM Production) | ||

| Oil, BOPD Shut-in | 412,070 BOPD | 23.55% |

| Gas, MMCFD Shut-in | 494 MMCFD | 25.56% |

| Evacuations and rig movements | total | % of GOM |

| Platforms Evacuated | 130 | 35% |

| Rigs Evacuated (non DP) | 2 | 40% |

| DP Rigs Moved-off | 3 | 15% |

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, tagged BOEM forecast, Gulf of Mexico, leasing policy, Permian Basin, production on Federal lands on September 4, 2024| 5 Comments »

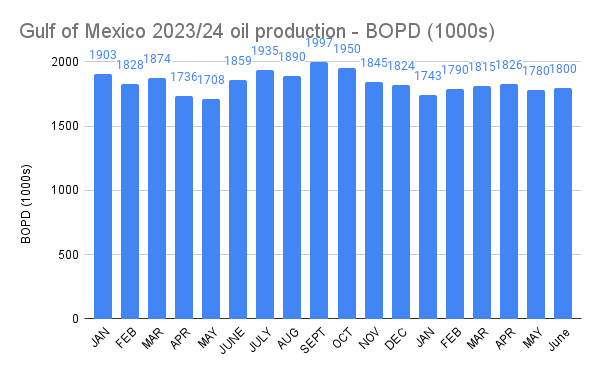

EIA has posted the June 2024 US production data. Gulf of Mexico production was remarkably flat from February through June, with a maximum deviation of only 2.0% (FEB vs. APR) and a deviation of only 0.5% from the beginning of this 5 month period to the end. Looking at the historical EIA data, this is about as stable of a 5 month period as I could find. Presumably, production from the new deepwater facilities is offsetting declines elsewhere as anticipated.

Unfortunately, the production growth forecasted by BOEM is not being realized. BOEM’s 2024 production forecast of 2.013 million bopd will likely be more than 200,000 bopd too high. Their forecast of >2 million bopd through 2027 is increasingly doubtful. These production forecasts contributed to (or were an excuse for) unprecedented leasing policies intended to prevent production from rising too high for too long.

Per ONRR data, the Gulf of Mexico continued to be the top oil producer for Federal lands in 2023. An additional 72.7 million bbls were produced on Native American lands. New Mexico, which has experienced significant Permian basin production growth, ranked second. The Texas Permian was the dominant US oil producer, but that production is almost exclusively on private lands (a big factor in the Permian success story).

| Location (Federal lands) | 2023 production (bbls) |

| Gulf of Mexico | 680,548,975 |

| New Mexico | 409,987,014 |

| Wyoming | 47,232,043 |

| North Dakota | 43,225,104 |

| Other | 33,635,796 |

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, Offshore Wind, Regulation, tagged biological opinion, Gulf of Mexico, Inflation Reduction Act, Judge Deborah Boardman, lease sale 262, Nantucket Magazine, NOAA, Rice's whale, wind leasing on September 3, 2024| Leave a Comment »

In response to a lawsuit filed by the Sierra Club et al, a Federal judge in Maryland vacated a 2020 biological opinion by the National Marine Fisheries Service (part of NOAA) that addressed risks to endangered species, most notably Rice’s whale, from oil and gas operations in the Gulf of Mexico. The decision by Federal Judge Deborah Boardman, who was appointed to her position in 2021, is attached.

Judge Boardman’s ruling is effective on Dec. 20, 2024. After that date, no new GoM leases may be issued and no new operating plans may be approved pending a new biological opinion. Existing GoM operations could also be affected. In other words, the ruling could have unprecedented effects on the OCS oil and gas program. (If you wonder how a Maryland judge can issue a ruling that could have major consequences for Louisiana and Texas, it is presumably because NOAA’s headquarters office is in Silver Spring, MD.)

The biological opinion process will likely be lengthy given the political considerations in an election year and the prospects for related litigation.

The judge’s ruling could also affect wind leasing in a manner that was perhaps unforeseen. Offshore wind leasing, which the plaintiffs strongly support despite the risks to the critically endangered North Atlantic Right Whale, could be delayed. Per a provision in the “Inflation Reduction Act,” no offshore wind leases may be issued after 12/20/2024, the one year anniversary of the last oil and gas lease sale (no. 261). Ironically, this is the same date as the effective date of the judge’s ruling.

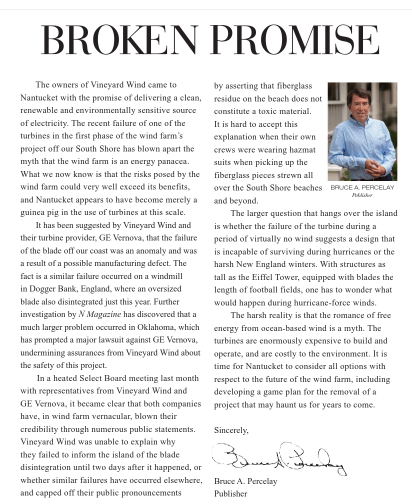

The judge’s decision will likely further delay the next oil and gas lease sale (no. 262) well into 2025 or later, and extend the pause in issuing wind leases that begins on 12/20/2024. Perhaps with that in mind, BOEM has been forging ahead with wind auctions despite the troubling Vineyard Wind blade failure, economic challenges for the wind industry, and growing opposition from coastal residents. An editorial by the publisher of Nantucket Magazine expresses concerns that should not be overlooked in the rush to auction wind leases.

(More on a new biological opinion related to the Right Whale in a future post.)

Posted in accidents, Offshore Energy - General, Regulation, tagged fatality, Gulf of Mexico, hydraulic workover unit, MP 64, Sanare Energy Partners on August 8, 2024| 1 Comment »

2 sentence summary: The well’s degraded 20″ structural casing could not support the hydraulic workover unit (HWU), which included an oversized BOP stack. The HWU began to sway and fell into the water with the victim attached by his fall protection to the top of the unit.

The full report is attached. The report is quite good, but something is seriously amiss when it takes 28 months to finalize a panel report. I suspect that the work of the panel and the regional reviewers was completed in a fraction of that time. Where are the bottlenecks?

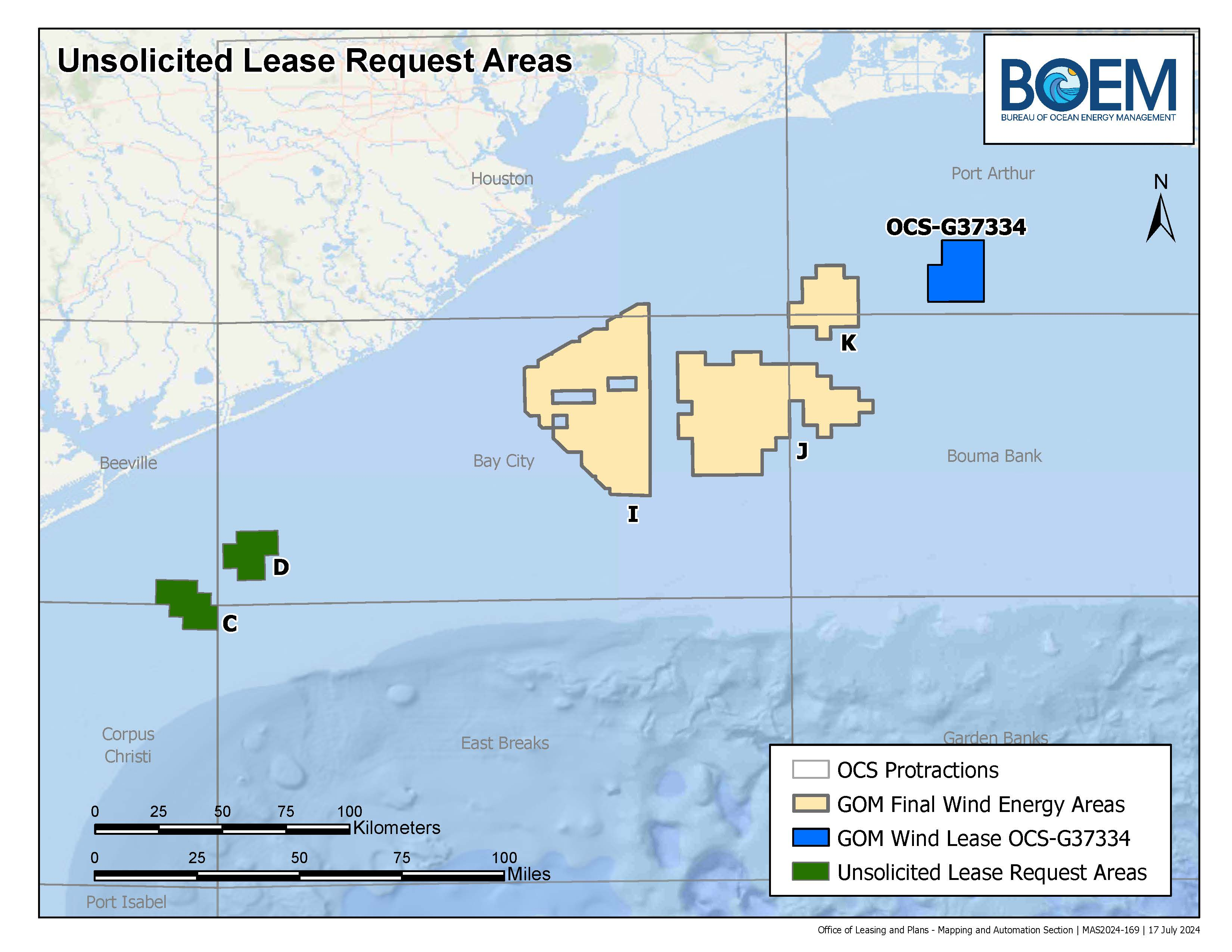

Posted in energy policy, Gulf of Mexico, Offshore Wind, tagged 2023 wind sale, 5 year leasing plan, BOEM, Gulf of Mexico, Hercate, OCS oil and gas leasing, OCSLA, Offshore Wind, unsolicited lease request on July 29, 2024| Leave a Comment »

GoM wind leasing update:

BOEM’s aggressive wind leasing policy stands in stark contrast to their current oil and gas policy. Not a single oil and gas sale will be held in 2024. Were it not for a provision in the “Inflation Reduction Act,” the last 3 GoM sales (257, 259, and 261) would probably not have occurred.

The new 5 year oil and gas leasing plan confirms that the Dept. of the Interior (DOI) has no intention of fulfilling their statutory oil and gas leasing mandate. In announcing the new 5 year plan, DOI boasted that the plan includes the fewest sales (3) of any plan in the history of the program. DOI strongly implied that the only reason those 3 sales were included was to sustain the wind program.,

When we drafted the OCSLA amendments that authorize offshore wind leasing, we envisioned complementary and synergistic programs, not a dogmatic pro-wind bias. As experts like Daniel Yergin have repeatedly warned, the notion that wind energy can eliminate the need for oil and gas is pure folly.

Posted in Gulf of Mexico, Offshore Energy - General, tagged Alta Mar, Beacon Offshore, CSL Exploration, first production, Gulf of Mexico, Heldelberg platform, independents' day, Kosmos Energy, Red Willow, Westlawn, Winterfell field on July 3, 2024| Leave a Comment »

Beacon Offshore Energy (BOE, but not this blog 😉) and its partners, all independent producers, have initiated production at the Winterfell project in the Green Canyon area of the Gulf of Mexico. The 3 initial wells are expected to produce 20,000 bbls of oil equivalent (again BOE 😉) per day. The Winterfell partners are:

Posted in CCS, climate, energy policy, Gulf of Mexico, Offshore Energy - General, Regulation, tagged BOEM, carbon disposal, CCS regulations, CS leasing, environmental studies, Gulf of Mexico, leakage study on June 27, 2024| Leave a Comment »

Carbon sequestration (i.e. subsurface disposal) is a controversial and divisive topic, and important questions regarding the costs and benefits remain. Nonetheless, the Infrastructure Bill of 2021 authorized the disposal of CO2 on the OCS, and stipulated that the Secretary of the Interior promulgate regulations for that purpose. However, that major task cannot be completed without a better understanding of the potential environmental impacts.

BOEM has announced a study (see attached pages from their new Environmental Studies Plan) to consider the potential for CO2 leakage and related environmental concerns. A few excerpts from BOEM’s summary follow:

Problem: Potential CO2 leakage from carbon sequestration (CS) project activities could occur via a number of pathways. Few studies model and/or measure CO2 leakage, transport, dispersion, attenuation, and environmental impacts in the offshore environment, and those that do exist are preliminary.

Intervention: BOEM needs more information about the dynamics, fate, transport, and potential environmental impacts of CO2 leakage under various scenarios, including worst-case, on the OCS to inform the new nationwide CS Program and to protect the environment from CO2 leakage.

Comparison: The study will model CO2 leakage under various scenarios, including worst-case scenarios, using the GOM OCS Region as a case-study and can be applied to all OCS regions. Outcome The leakage and worst-case scenario modeling will aid BOEM’s ongoing rulemaking efforts, program development and implementation, and future operational needs including NEPA analyses, lease planning, lease stipulations, consultations, plan and permit approvals, mitigation measures, risk assessment and monitoring requirements, etc. Study results will also provide direction for future studies to include field and/or laboratory analyses.

The performance period for this important study extends through 2027, so it’s hard to envision final CS regulations prior to that date. You can’t issue regulations without first assessing the potential harm that could result from their promulgation (as required by NEPA).

BOEM’s summary mentions “the anticipation of a CS lease sale in the GOM after final regulations are published.” Hopefully, this also means that BOEM will not permit improperly acquired oil and gas leases (Sales 257, 259, and 261) to be converted to CS leases.

Posted in energy policy, Gulf of Mexico, Offshore Energy - General, tagged 5 year leasing plan, Gulf of Mexico, oil sales, SPR depletion, Strategic Petroleum Reserve on June 26, 2024| Leave a Comment »

“We will do everything we can to make sure that the market is supplied well enough to ensure as low price as possible for American consumers,” Hochstein told the newspaper. “I think that we have enough in the SPR if it’s necessary.” ~Amos Hochstein, Special Presidential Coordinator for Global Infrastructure and Energy Security.

Maybe they should remove “Energy Security” from his impressive title since that seems to be a low priority.

Apparently it’s fine (and environmentally friendly) to deplete strategic oil reserves to reduce prices prior to an election, but not to hold regular oil and gas lease sales in the adjacent Gulf of Mexico. 2024 will be the first year without an OCS lease sale since 1958, and the Administration bragged about the new 5 year leasing plan having the fewest proposed sales in history!

5 Year Leasing Plan Announcement:

“Consistent with the requirements of the Inflation Reduction Act (IRA) concerning offshore conventional and renewable energy leasing, the Department of the Interior today published the final 2024–2029 National Outer Continental Shelf Oil and Gas Leasing Program (Program) with the fewest oil and gas lease sales in history.

These three lease sales are the minimum number that will enable the Interior Department’s offshore wind energy program to continue issuing leases in a way that will ensure continued progress towards the Administration’s goal of 30 gigawatts of offshore wind by 2030.”

Posted in California, decommissioning, energy policy, Gulf of Mexico, Offshore Energy - General, Regulation, tagged BOEM, Cox bankruptcy, decommissioning, financial assurance, Gulf of Mexico, Hogan and Houchin, Pacific, TX LA MS suit on June 19, 2024| Leave a Comment »

What’s their solution?

Since the States don’t seem to think there is much risk, perhaps they would like to guarantee decommissioning expenses. Have they looked into the Cox bankruptcy? How about Platforms Hogan and Houchin and the complex decommissioning challenges in the Pacific. Are they comfortable with taxpayer funding for offshore decommissioning?

BOE recently defended the new BOEM rule. If anything, the rule is too lax in that compliance and safety records are not considered in determining financial assurance requirements and lessees may use reserve estimates to reduce supplemental assurance amounts.

Posted in Offshore Energy - General, Gulf of Mexico, energy policy, climate, CCS, tagged BOEM, carbon disposal, CCS, Exxon, Gulf of Mexico, infrastructure bill, Ocean Dumping, Repsol on June 18, 2024| Leave a Comment »

Closing comment: “Sequestration” is a euphemism that is being incorrectly applied to soften the reality of disposing carbon beneath the Gulf of Mexico. Sequestration implies storage for later use and that is clearly not the intent. Because carbon disposal is arguably dumping, a special exemption from the Marine Protection, Research, and Sanctuaries (Ocean Dumping) Act of 1972 had to be added to the Infrastructure Bill.