Since well before the Putin crisis, this independent blog has been expressing concerns about sustaining US offshore oil and gas production without new leases and increased exploration (more here). Now that concerns about domestic production and energy security are heightened (understatement of the year!), let’s review where the leasing program stands:

- 466 days have elapsed since the last oil and gas lease sale (Nov. 19, 2020), with no future sales in sight.

- There had been 182 sales in the previous 66 years of the US offshore oil and gas program, an average of 2.76 per year. Never before (since 1953) has a year transpired without a lease sale.

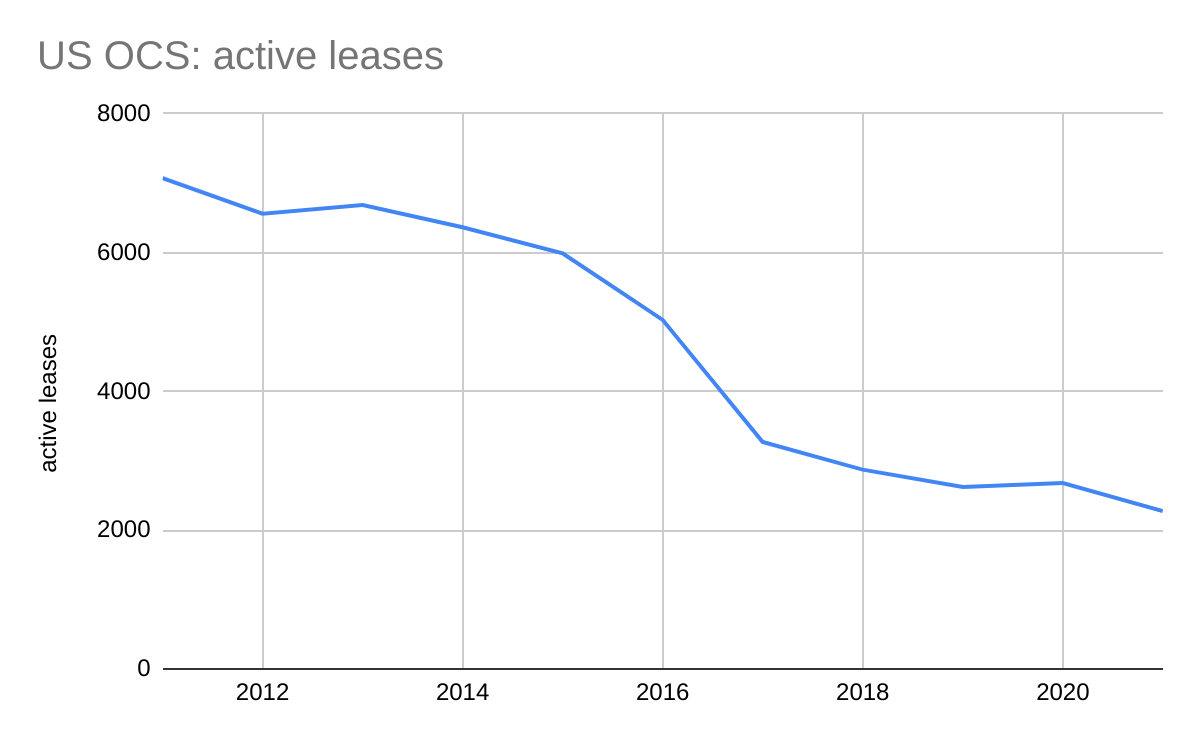

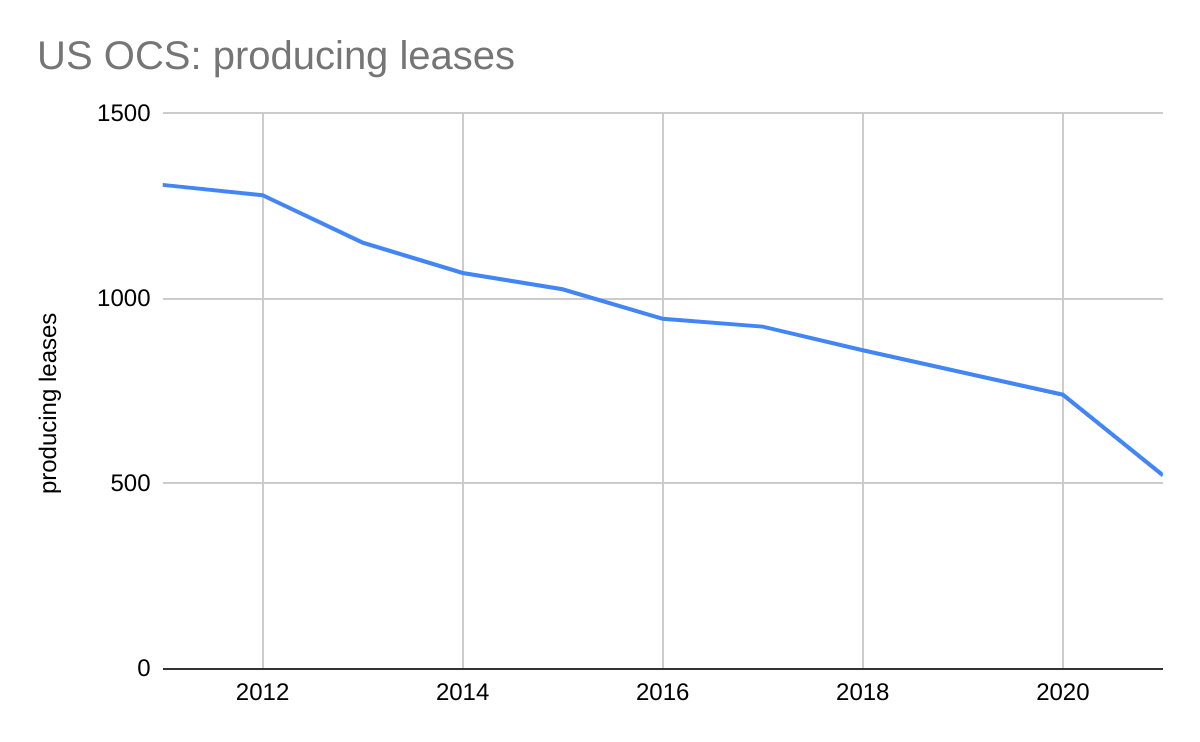

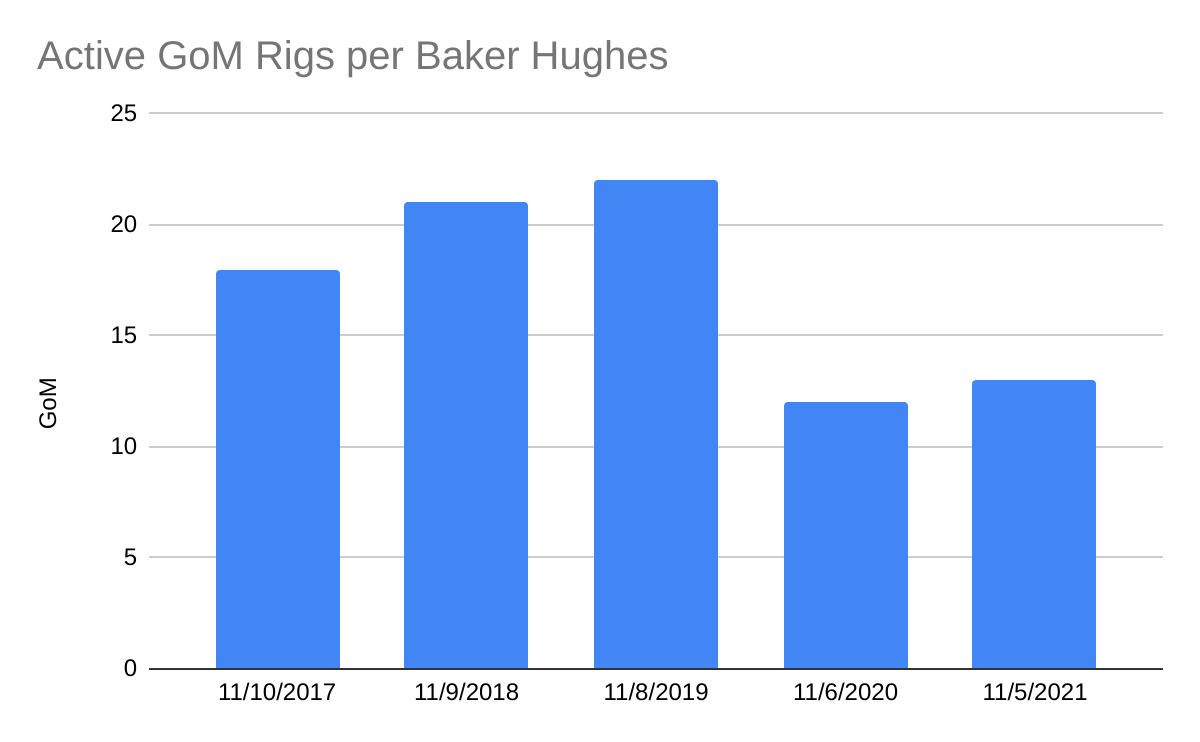

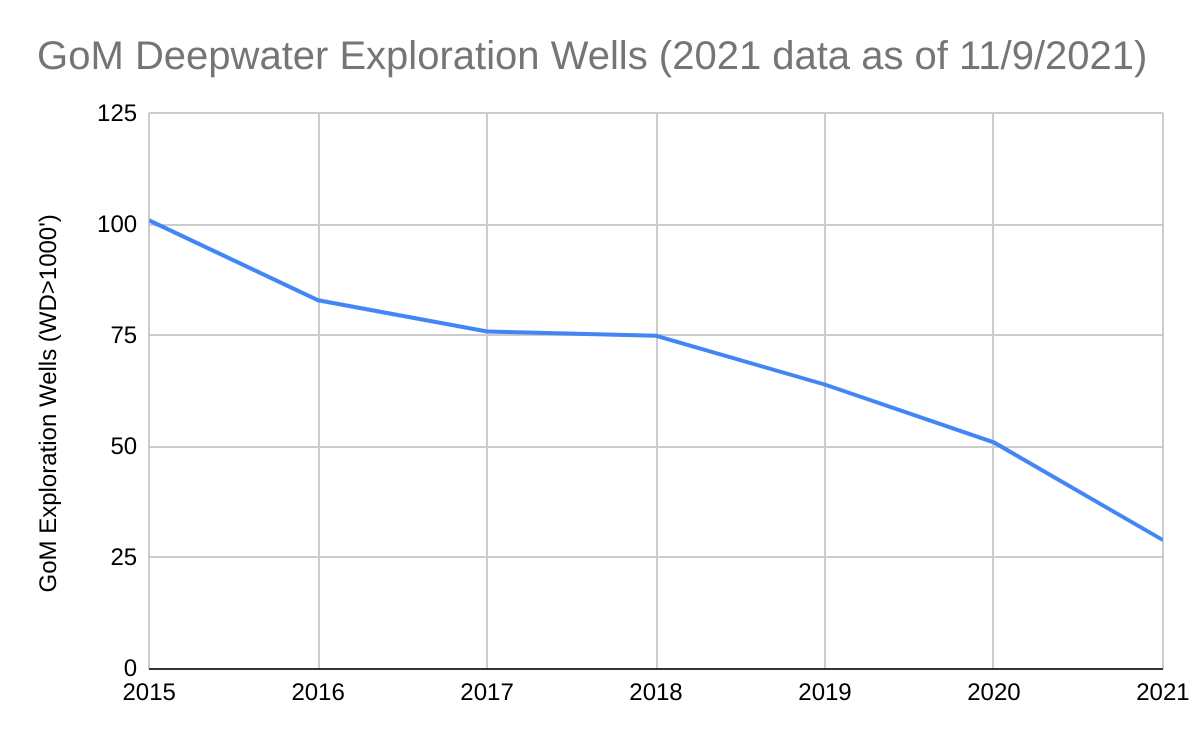

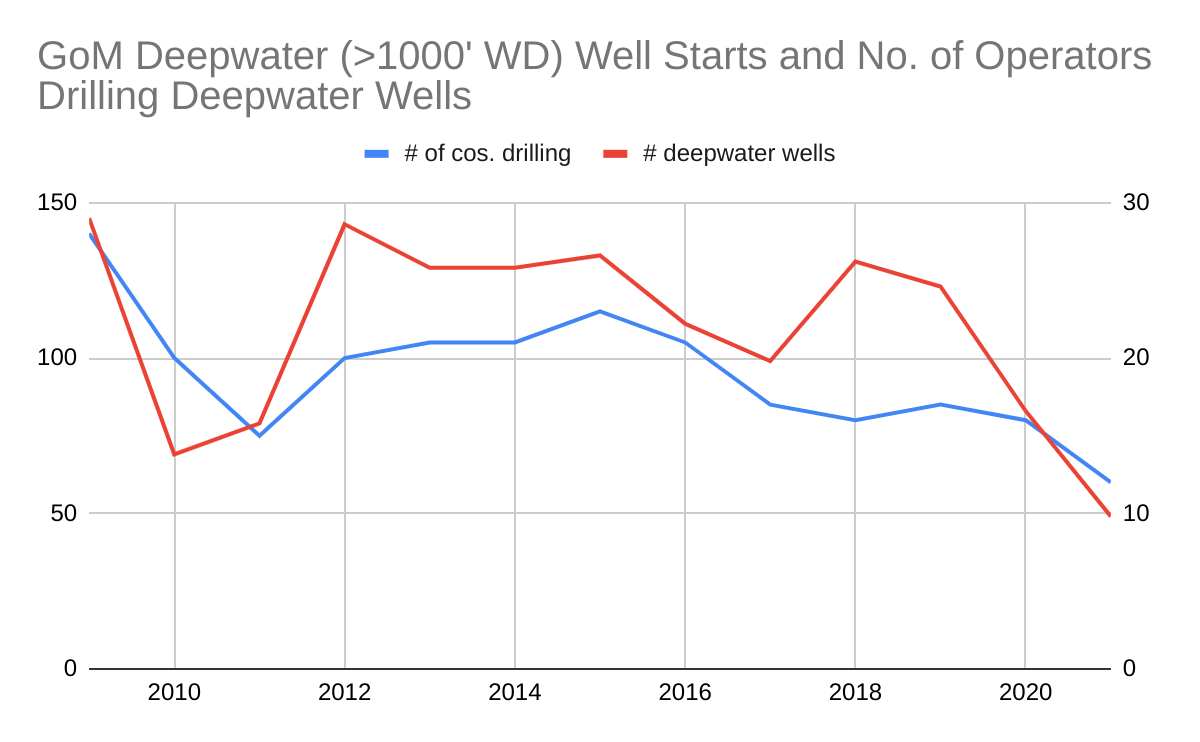

- Currently, there are only 2016 active US OCS leases and 506 producing leases, the fewest in at least 40 years (recent history charted below).

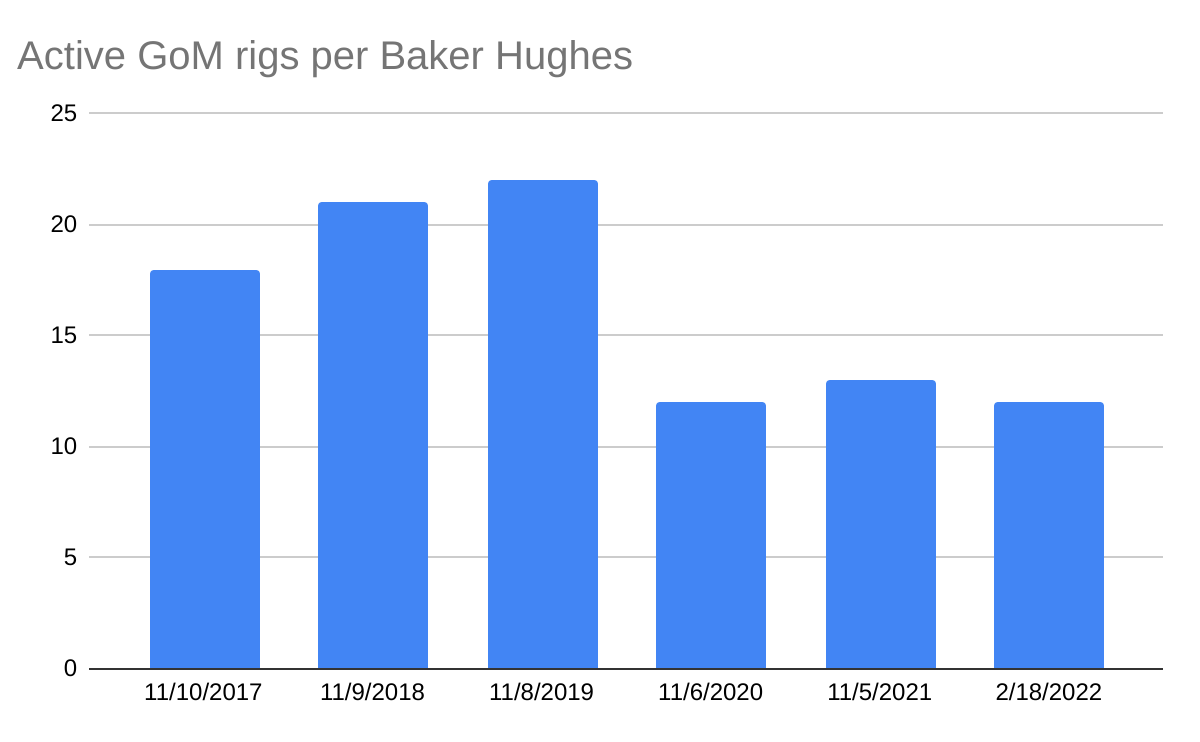

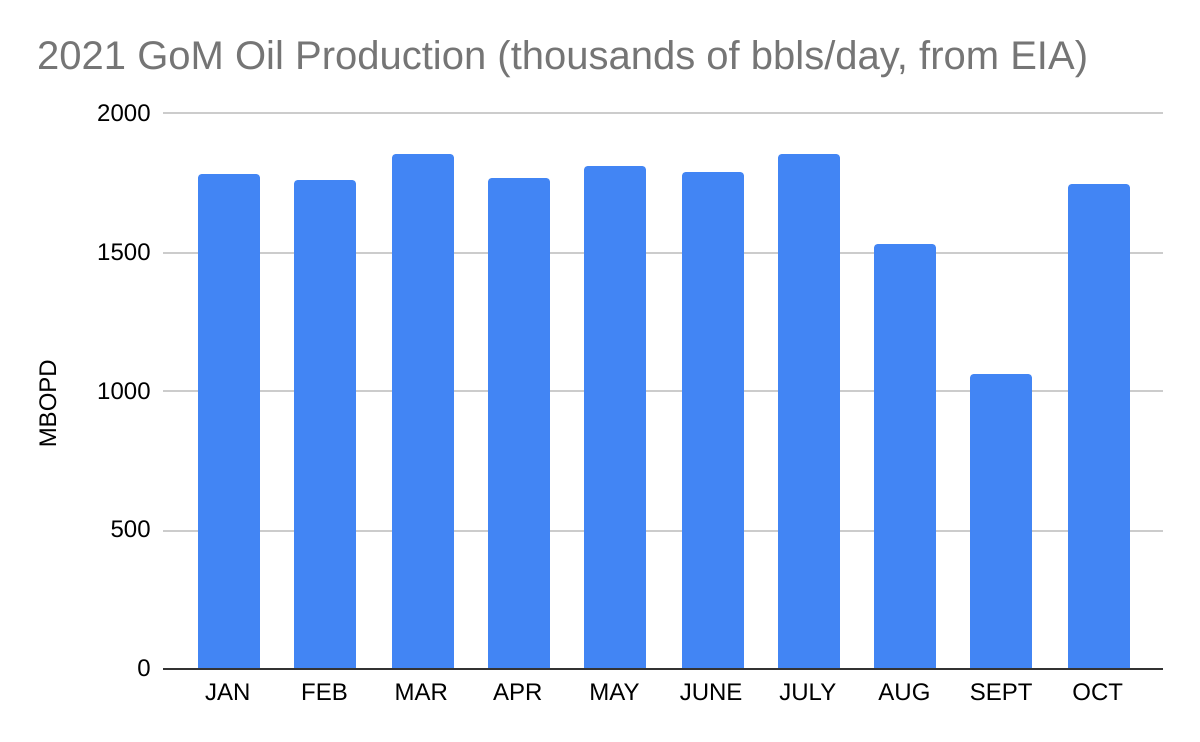

- Despite favorable geology beneath the deepwater Gulf of Mexico and advanced exploration and well completion technology, US offshore oil production (1.713 million bopd per the latest EIA data – Dec. 2021) is down 16% from the August 2019 peak of 2.044 million BOPD. Gulf oil production is thus the lowest since 2018 (except during hurricane shutdowns).

- New projects and higher ultimate recoveries from producing reservoirs could increase total offshore production by 10-20% over the next few years, but sharp declines will follow without new leases and increased exploration.