For 40 years, challenges associated with bankruptcies (or the threat thereof), a divided offshore industry, political pressure, hurricane damage, and unresolved legal issues have hindered initiatives to better protect the public from decommissioning liabilities. Nonetheless, regulators and industry were able to prevent taxpayers from incurring any decommissioning costs. Unfortunately that is no longer the case.

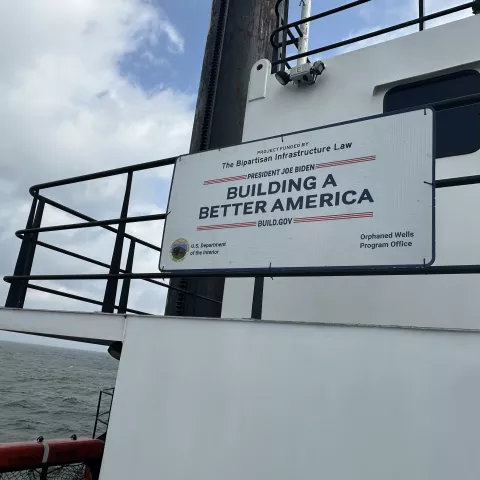

For the first time in history, the govt has funded decommissioning on the OCS (and bragged about it – photo below).

BOEM’s proposed revisions to the decommissioning regulations (attached) would facilitate the transfer of aging structures to companies with limited assets, and in some cases, poor or undemonstrated safety records.

The proposal would reduce or eliminate the supplemental financial assurance requirement if a predecessor lessee has a strong credit rating. For that strategy to work, related decommissioning issues must be addressed. and clarifications and boundaries provided to ensure taxpayers are protected from decommissioning liabilities.

Predecessor liability, which is important because it helps prevent companies from assigning leases for the purpose of avoiding decommissioning obligations, was not established in the regulations until much of the OCS infrastructure was already installed. In a final rule that was effective on 8/20/1997, my office (thanks to the perseverance of Gerry Rhodes, John Mirabella, and Dennis Daugherty) codified the joint and several liability principle in 30 CFR 250.110 as follows:

(b) Lessees must plug and abandon all well bores, remove all platforms or other facilities, and clear the ocean of all obstructions to other users. This obligation:

(1) Accrues to the lessee when the well is drilled, the platform or other facility is installed, or the obstruction is created; and

(2) Is the joint and several responsibility of all lessees and owners of operating rights under the lease at the time the obligation accrues, and of each future lessee or owner of operating rights, until

the obligation is satisfied under the requirements of this part.

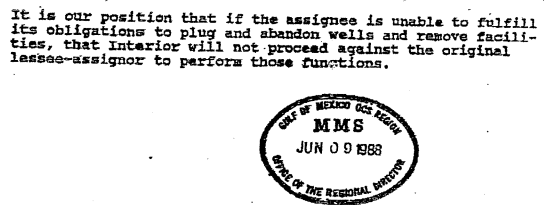

Prior to the that rule, the official policy of the Dept. of the Interior, as expressed in a 1988 letter from the Director of the Minerals Management Service (see excerpt pasted below), was that lease assignors would NOT be held accountable should their successors fail to fulfill their decommissioning responsibilities.

A major unanswered question regarding decommissioning obligations is thus the extent to which predecessor liability applies to leases assigned prior to the 1997 regulation. According to BOEM data, 771 remaining platforms were installed at least 10 years before the rule change, and 504 were installed at least 20 years prior. For assets transferred prior to the rule change, do the predecessors retain liability? BOEM should explain its position on this issue.

Other predecessor liability questions that need to be answered:

- Now that the reverse chronological guidance has been scrapped, what will be the process for determining which predecessors will be held responsible?

- If the govt doesn’t ensure that the new lessees fulfill their performance obligations (e.g. funding escrow accounts, well plugging, insurance, etc.), are predecessors still liable?

- What if the structures were poorly maintained by the new lessees, complicating decommissioning and increasing the costs

- Should a predecessor several transfers removed from operating the facilities still be held responsible?

Two examples of what can happen (and has happened):

Example 1: Big AAA Oil assigns a lease to Proud Production, a reputable independent. After years of operations, Proud can no longer profitably produce from the lease. Proud assigns the lease to CCC Oil & Gas, a small and highly efficient operator. After the lease is no longer profitable, even for a company with a low cost structure, CCC assigns the lease to Elmer’s E&P, a sketchy, barely solvent operating company with a poor compliance record. Elmer rather predictably neglects maintenance and declares bankruptcy after a decline in oil prices. Should Big AAA Oil, which had no say in the last 2 transfers in the assignment chain, be financially responsible for decommissioning the facilities?

Example 2: Big AAA Oil assigns a lease to DDD Development Company. Per the terms of the assignment, DDD establishes an Abandonment Escrow Account, as provided for in 30 CFR 556.904. BOEM allows DDD to withdraw funds from the account for purposes not authorized in the regulations. Should Big AAA Oil be liable for decommissioning costs after DDD is no longer solvent? (See “The troubling case of Platforms Hogan and Houchin.”)

For predecessor liability to be fairly and effectively implemented, and survive legal challenges, BOEM should:

- Before approving lease assignments, verify that the assignors and assignees have contractually specified, to BOEM’s satisfaction, how the decommissioning of assigned assets will be funded.

- Not approve subsequent lease assignments until the predecessor that is being held financially responsible has approved a funding agreement with the new lessees.

Another important concern is that BOEM’s proposal does not correct two prior changes that further expose the public to decommissioning liabilities:

- the use of oil and gas reserve estimates to reduce or eliminate supplement assurance requirements

- the failure to consider safety compliance in determining supplemental assurance amounts.