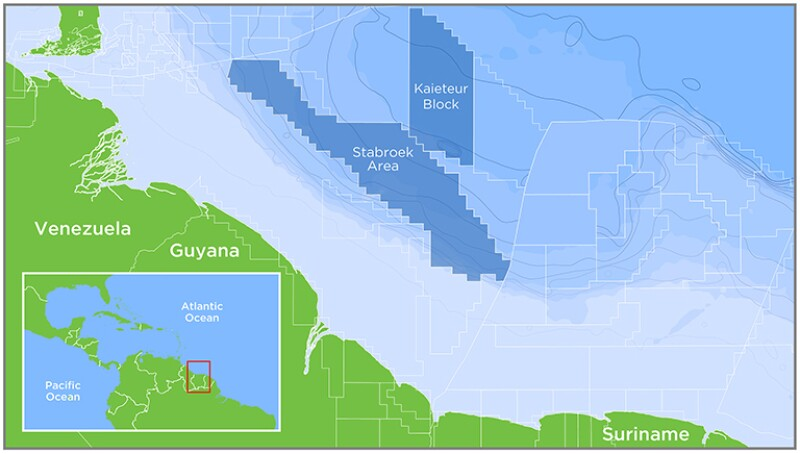

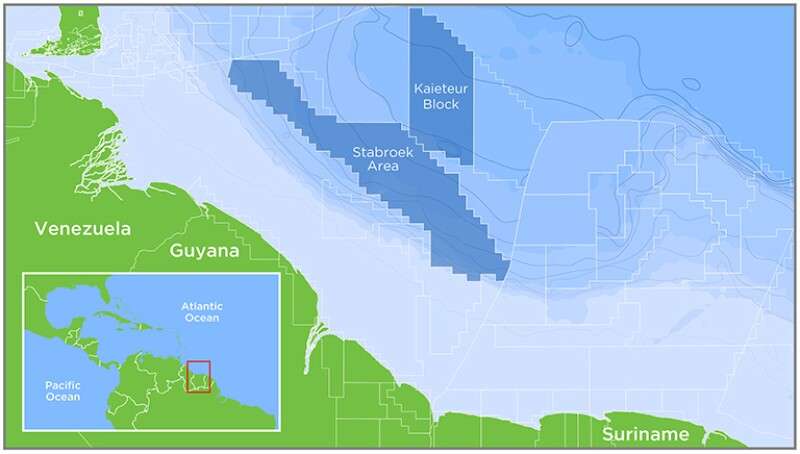

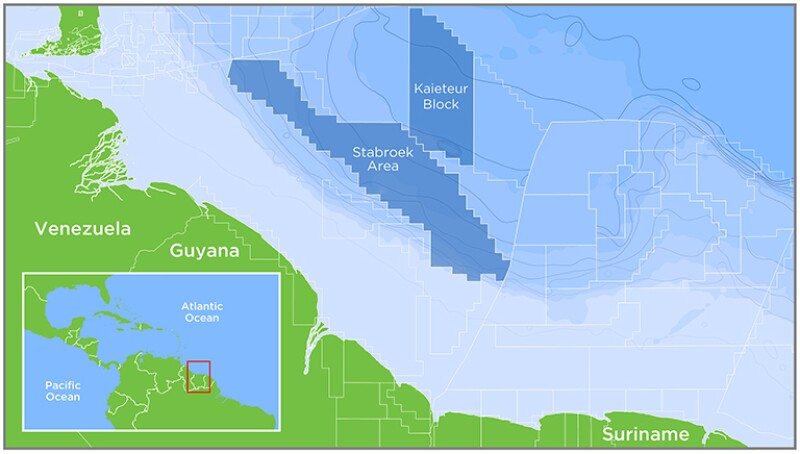

As posted in January, most analysts predicted that Chevron and Hess would prevail. Now that the arbitration panel has ruled, Chevron’s acquisition of Hess can be completed.

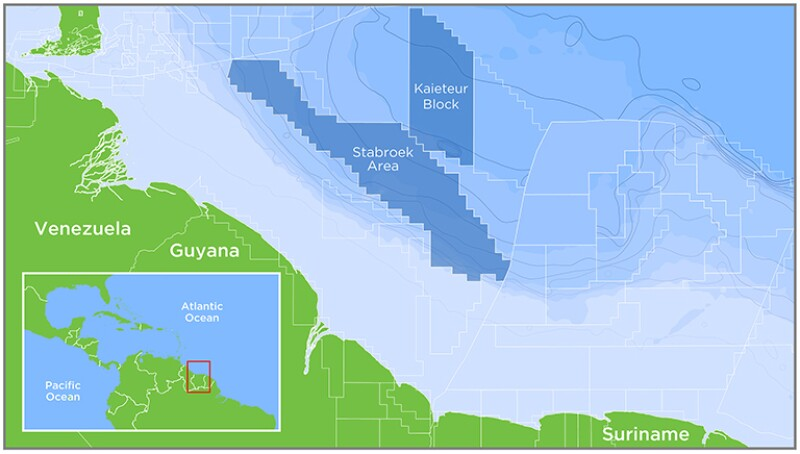

The position of Exxon and its partner, Chinese govt owned CNOOC, never made much sense given that Chevron was not buying the Stabroek share, they were buying the company that holds that share.

Not much attention has been paid to the importance of Chevron’s acquisition of Hess’s Gulf of America assets. The combined company will be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell). Hess acquired 20 GoA leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

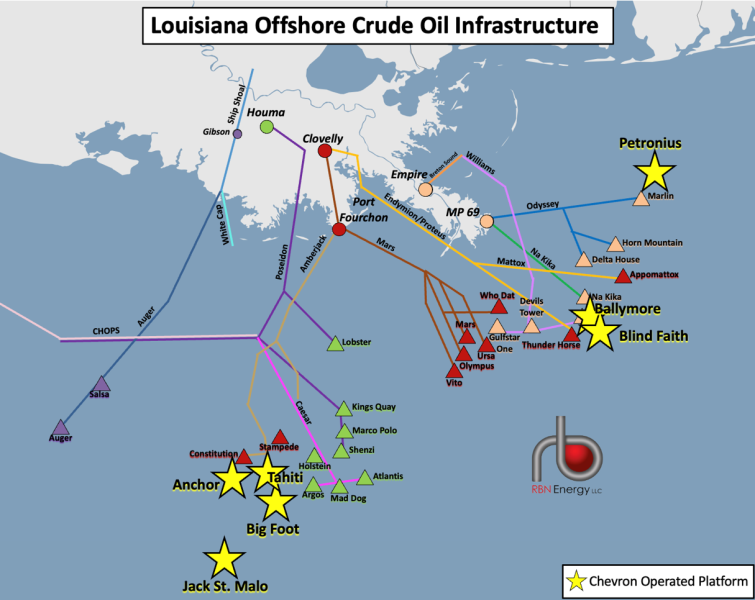

Reuters and others report that zinc from a new Chevron well has contaminated oil production destined for an Exxon refinery via Shell’s Mars Pipeline System. Because contaminated crude may cause maintenance issues and reduces the quality of refined products, Exxon will not accept crude from the Mars system until the zinc issue has been resolved.

The Mars system delivers about 575,000 bopd raising concerns about supplies to Gulf Coast refineries. But fear not, DOE authorized the delivery of up to 1 million barrels of oil from the Strategic Petroleum Reserve to the Exxon’s Baton Rouge refinery.

(Ironically, yesterday’s post pointed to the importance of the SPR and questioned the decision to drastically reduce crude oil purchases. This zinc incident is likely to be minor, and Exxon will repay the SPR in kind. However, more serious regional, domestic, and international events could call for much greater SPR withdrawals.)

The above map shows Chevron platforms that connect with the Mars system at Port Fourchon.

Speculation/commentary:

The well/platform responsible for the zinc contamination has not been identified. Given that production is ramping up at Chevron’s Anchor facility, a new well on that platform may be the source of the zinc. Other Chevron platforms that connect to the Mars system are indicated in the diagram above.

Given that zinc in crude oil is rare, a well completion fluid containing zinc bromide may be the culprit.

Note the integration of offshore production streams, and the involvement of 3 industry super-majors. These companies are highly competitive, as evidenced by the Chevron-Exxon Stabroek dispute, but are also cooperative in producing, transporting, and refining oil and gas. However, they and other majors are restricted (rather illogically) from bidding jointly for leases.

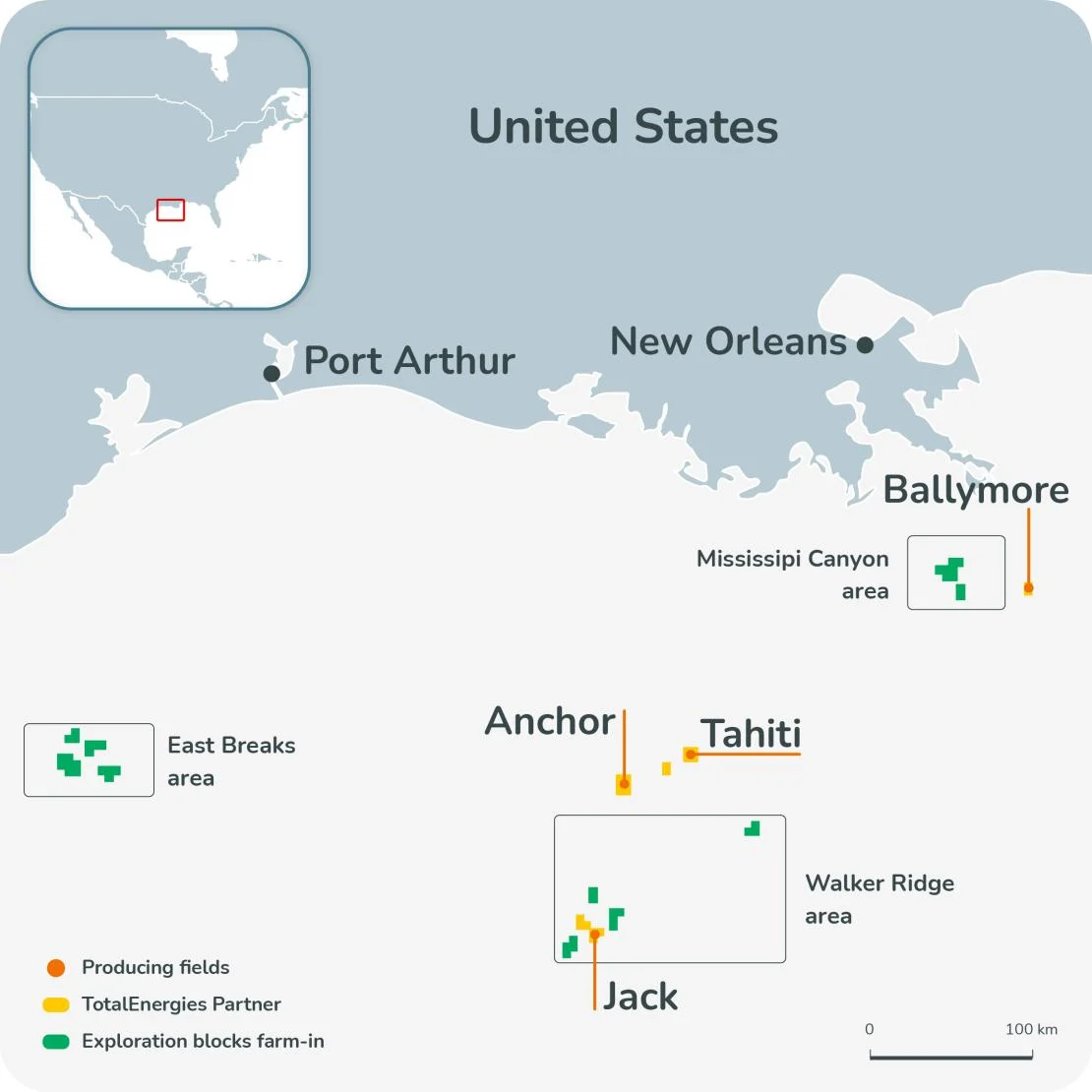

This week Total announced the acquisition of a 25% working interest in 40 Chevron leases in the Gulf of America. Total already owned interest in Chevron’s producing Ballymore (40%), Anchor (37.14%), Jack (25%), and Tahiti (17%) fields. Ironically, Federal regulations prohibited Total from jointly bidding with Chevron for any of those leases at the time of the sales. How does that make sense?

Total did not submit a single bid in any of the past 4 Gulf of America lease sales. Perhaps they prefer to acquire interest in blocks previously leased to companies like Chevron. That is a reasonable acquisition strategy. However, farm-in acquisitions yield no bonus dollars to the Federal government. Wouldn’t it have been in the government’s best interest if some of those acquisition dollars were spent at lease sales where the bonus bids go to the US Treasury?It’s long past time to remove the joint bidding restrictions!

Two of Israel’s three offshore gas fields are shut-in as a precaution. As a result, exports to Egypt and Jordan has been curtailed. The Tamar field continues to supply Israel’s gas needs.

Summary table:

field (operator)

2024 production (billion cubic meters) (% of Israel’s total)

Exxon senior vice president Neil Chapman said he was confident that a three-member arbitration panel would rule in Exxon’s favor and determine it had a right-of-first-refusal to purchase Hess’ stake in a Guyana oil joint venture operated by Exxon.

Hess: “We remain confident that the arbitration will confirm the Stabroek right of first refusal does not apply to the merger.”

Their filing is attached. I found the following points to be particularly compelling:

p.3: “Despite no evidence that an Oil and Gas Program vessel has ever struck a Rice’s whale, the 2025 BiOp projects that Oil and Gas Program vessels will lethally strike numerous Rice’s whales over the term of the 2025 BiOp. On that basis alone, the Service found that the Oil and Gas Program will jeopardize the continued existence of the Rice’s whale, and developed a multi-step reasonable and prudent alternative which it asserts will reduce projected vessel strikes to zero.“

p. 4: “The Rice’s whale is a rarely found animal that the Service first identified as a new species (separate from the non-endangered Bryde’s whale) in 2021. 86 Fed. Reg. 47,022 (Aug. 23, 2021). There is no evidence that an Oil and Gas Program vessel has ever struck a Rice’s whale (or a Bryde’s whale) despite continued operation in the Gulf over many decades.”

p. 5: “The 2025 BiOp disregards the Bureaus’ logical, fact-based conclusion. Instead, the Service’s 2025 BiOp engages in speculation and guess-work to surmise that Oil and Gas Program vessels could be striking and killing Rice’s whales on a regular basis. The Service ignores the best available data (i.e., showing no recorded observations of an oil and gas vessel striking a Rice’s whale) and instead presumes that forceable and lethal collisions between oil and gas service vessels and 60,000-pound whales are regularly occurring but somehow going unnoticed by the vessels and their crews and that the carcasses silently disappear into the water, never to be seen again.“

On May 26 in London a three-judge International Chamber of Commerce panel will finally begin considering the Exxon claim that the Stabroek joint operating agreement grants them the right-of-first-refusal in Chevron’s acquisition of Hess’s 30% share of the massive field (>11 billion boe) offshore Guyana.

Exxon’s rather unlikely ally in this case is state-owned China National Offshore Oil Corp. How did CNOOC get a stake in Stabroek and why is their position on the Hess acquisition hypocritical?

CNOOC became a 25% Stabroek partner by acquiring Canadian Nexen in 2013. Their Nexen acquisition, which included Canadian, US, and international assets, was only reluctantly approved by the Canadian and U.S. governments, and probably would not be approved today.

CNOOC’s Stabroek acquisition is thus very similar to Chevron’s. In both cases, the entire company, not just the Stabroek asset, was acquired.

The Stabroek acquisition has proven to be most fortuitous for CNOOC, not only because of the oil and gas resources, but also through the deepwater development expertise that has been gained. Now CNOOC is trying to further leverage their Stabroek position by joining Exxon in challenging the Chevron acquisition.

It would be great if the arbitration proceedings were streamed, but that will not be the case. It also appears unlikely that media will be allowed to attend or that transcripts will be made available.

As previously noted, I would have liked the Guyanese government to be more assertive in this dispute. Stabroek is Guyana’s offshore gem, their most important economic asset. This lengthy dispute has to affect partner teamwork and communication. From safety, environmental, and production standpoints, do you want feuding partners managing such an important national asset?

The 2024 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 3 facility inspections (0.33 INCs/facility inspection)

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2024, there were on average 3.4 inspections for every facility inspection.

District investigation reports are more timely and provide additional insights into safety performance. Impressively, Hess had no incidents warranting a District investigation, and was the only ranked operator with this distinction. I will comment more on the District reports in a future post

Chevron’s 2024 compliance record was among the best in the history of the US OCS oil and gas program. Was it the absolute best? Were it not for the FSI INC at a Unocal (Chevron) facility, one could unequivocally assert that it was. Further evaluation of that INC would be helpful. However, details on specific INCs are not publicly available, so the significance of that violation cannot be evaluated.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Chevron

1

0

1

2

117

0.02

311

0.006

BP

2

3

0

5

93

0.05

251

0.02

Anadarko

8

9

1

18

143

0.13

344

0.05

Hess

2

3

0

5

26

0.19

67

0.07

Walter

6

4

1

11

50

0.22

161

0.07

Shell

23

17

5

45

199

0.23

495

0.09

Cantium

24

8

0

32

123

0.26

537

0.06

Murphy

8

9

1

18

70

0.26

191

0.09

Arena

29

28

3

60

189

0.32

803

0.07

Gulf-wide

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2024, there were on average 3.4 inspections for every facility inspection

Not meeting the production facilities requirement to be ranked among the top performers, but nonetheless noteworthy, was the compliance record of BOE Exploration & Production (no relation to the BOE blog 😀). See their impressive inspection results below:

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

BOE

1

1

0

2

21

0.1

48

0.04

Transparency on inspections and incidents is important for a program that is dependent on public confidence. For independent observers to better evaluate industry-wide and company-specific safety performance, publication of the following information should be considered:

quarterly updates of the incident tables, as was once common practice

posting of violation summaries for inspections resulting in the issuance of one or more INCs

Remember that Chevron was once Standard Oil ofCalifornia. The attached WSJ article discusses the ugly divorce after all these years.

Chevron tired of California’s attempts to dictate corporate strategy. Per Chevron CEO Mike Wirth:

“Putting bureaucrats in charge of centrally planning key segments of the economy hasn’t worked in other socialist states,” Wirth said in a Nov. 1 call with investors. “I doubt it will be any different in California.”

California wanted Chevron to commit to the State’s energy agenda:

“Chevron has a future in clean energy in California. They can join us in our steady, long-term transition to a state powered by clean energy,” said Daniel Villaseñor, a spokesman for the governor’s office.

California wanted the interests of shareholders to be subordinate to the State’s carbon goals:

Newsom said Wirth had invested far more in shareholder payouts than in developing low-carbon energy.

Other State actions that contributed to the divorce:

accused Chevron and other companies of price gouging

accused Chevron, as a fossil fuel producer, of indirectly causing tragic fires

Chevron is not buying the Stabroek share; they are buying the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership.

As an offshore operator, Exxon has been highly responsible from a safety standpoint. However, the company is not reluctant to stretch the envelope when it comes to contract rights. The most recent example was their acquisition of 163 GoM oil and gas leases for carbon disposal purposes, contrary to the terms of the sale notice and lease contracts.

Interestingly, Exxon’s partner in this dispute is state-owned China National Offshore Oil Corporation. CNOOC acquired their 25% Stabroek share when they purchased Nexen, a Canadian company (sound familiar?). Both the Canadian and US governments had reservations about this acquisition and nearly nixed the deal. Would either government bless that acquisition today?

An International Chamber of Commerce arbitration panel will hear the Stabroek case in May 2025, and the final decision is expected by September 2025.