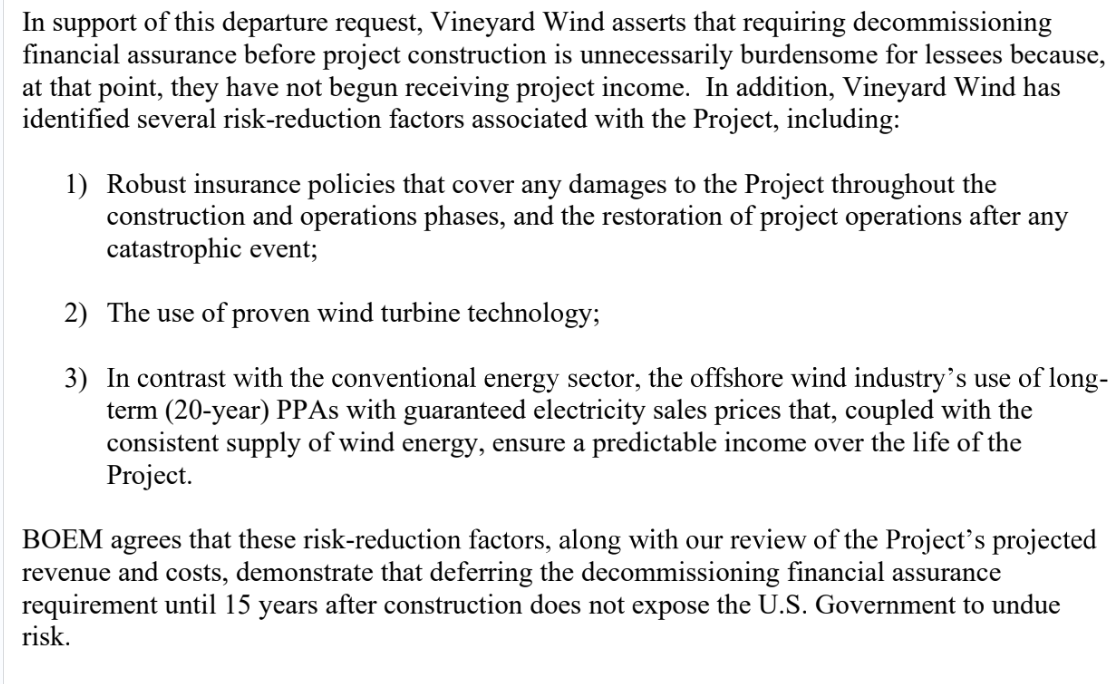

Comments on the 3 risk reduction factors cited in the letter:

Factor 1: Those “robust insurance policies” may soon be tested given the costs associated with the turbine blade incident and potential law suits. (The notice pasted below informs that Nantucket officials will meet on Tuesday to consider litigation. A question for attorneys is the extent to which Nantucket is compromised by their good “Good Neighbor Agreement” with Vineyard Wind. That agreement essentially calls on Nantucket to promote the Vineyard Wind projects in return for payments that seem modest relative to the economic benefits from tourism and fishing.)

Factor 2: To the extent that GE Vernova Haliade-X 13 megawatt turbines are proven technology (and that is very much in doubt), the use of proven technology doesn’t prevent premature abandonment associated with unexpected incidents.

Factor 3: Reliable power generation and predictable long-term income remain to be demonstrated.

Nantucket Current photo: Vineyard Wind turbine AW38 with a damaged blade that has caused thousands of pieces of debris to wash ashore on Nantucket since Tuesday.

“This morning, a significant part of the remaining GE Vernova blade detached from the turbine. Maritime crews were onsite overnight preparing to respond to this development, though current weather conditions create a difficult working environment.”

“We are staying apprised of GE Vernova’s efforts to manage the situation, including the removal and recovery of the remaining blade attached to the turbine.”

Staying apprised? As operator, Vineyard Wind is fully responsible. This is their situation to manage.

BSEE has ordered Vineyard Wind to suspend power production and wind turbine generator construction.

Kudos to BSEE for their decisive and timely action. They need to better understand what happened before allowing operations and construction to continue.

Imagine the pressure on the regulator if the project was providing a significant portion of the region’s electricity.

BSEE’s comment that there has been “no harm to any marine resources or mammals from the incident” is premature given the extensive marine debris and the associated risks to mammals.

What about the CVA?

The regulations at 30 CFR § 285.707-712 assign important responsibilities to Certified Verification Agents (CVAs), independent third parties with established technical expertise. These responsibilities include detailed reviews of the design, fabrication, and installation plans.

Oddly, the CVA’s “Statement of Qualifications” and “Scope of Work and Verification Plan” have been redacted in their entirety from Vineyard Wind’s Construction and Operations Plan (COP) (see Appendix I-C and I-D).

Who was the CVA and why was that important information redacted?

Were any of the CVA requirements waived per 258.705?

Will BOEM, the lessor and Federal wind program manager, be making a statement? Will they be reassessing their COP review procedures?

BOEM should temper their over-the-top promotion of offshore wind. The complete shutdown of the first utility scale offshore wind farm heightens public concerns about the intermittency of this power source, and the need for reliable backup sources.

BOEM’s land rush approach to offshore wind leasing will add up to 1086 turbine towers and 28 offshore substations (OSSs) in the Atlantic just from active projects with approved Records of Decision (RODs). (See the table below.) Another 17 active Atlantic commercial projects have yet to reach the ROD stage. Those projects should increase the total number of structures to >3000. Five more Atlantic wind lease sales are scheduled.

project

turbine towers

offshore substations

Coastal VA Offshore Wind

202

3

Revolution Wind

100

2

Sunrise Wind

94

1

Atlantic Shores South

200

up to 10

Ocean Wind 1

98

up to 3

Vineyard Wind 1

100

2

Empire Wind 1 & 2

147

2

New England Wind (phases 1&2)

150

5

Per the Construction and Operations Plan (COP) for Vineyard Wind, the topsides for a conventional electrical service platform (ESP) (also known as an offshore substation or OSS) are 45 x 70 x 38 m, which is larger in surface area than a typical 6-pile oil and gas platform (~30 x 30 m), and is comparable in size to a large jackup drilling rig.

The Atlantic Shores plan calls for 10 small, 5 medium, or 4 large OSSs. (Uncertainty regarding the number and types of structures seems rather common in wind COPs.) The large OSSs have topsides that are 90 m by 50 m and rise to 63 m above MLLW. These are large offshore structures whether for wind or oil and gas.

Per BOEM, the “Rule to Streamline and Modernize Offshore Renewable Energy Development” is intended to “make offshore renewable energy development more efficient, [and] save billions of dollars. Unfortunately, the savings associated with relaxed financial assurance requirements translates to increased risk for power customers and taxpayers.

BOEM signaled their intentions on offshore wind (OSW) decommissioning three years ago when they granted a precedent setting financial assurance waiver to Vineyard Wind. Despite compelling concerns raised by commenters, the “streamlining” regulations codified this decision.

No one knows what the financial future will be for wind projects and the responsible companies. Financial assurance should therefore be established when the structures are installed, not years into the future as allowed by the revised regulations. What leverage will BOEM have then?

Nordsee One substation, Germany. Rystad Energy projects 137 new power substations offshore continental Europe this decade, requiring $20 billion in total investment.

Carbon sequestration (i.e. subsurface disposal) is a controversial and divisive topic, and important questions regarding the costs and benefits remain. Nonetheless, the Infrastructure Bill of 2021 authorized the disposal of CO2 on the OCS, and stipulated that the Secretary of the Interior promulgate regulations for that purpose. However, that major task cannot be completed without a better understanding of the potential environmental impacts.

BOEM has announced a study (see attached pages from their new Environmental Studies Plan) to consider the potential for CO2 leakage and related environmental concerns. A few excerpts from BOEM’s summary follow:

Problem: Potential CO2 leakage from carbon sequestration (CS) project activities could occur via a number of pathways. Few studies model and/or measure CO2 leakage, transport, dispersion, attenuation, and environmental impacts in the offshore environment, and those that do exist are preliminary.

Intervention: BOEM needs more information about the dynamics, fate, transport, and potential environmental impacts of CO2 leakage under various scenarios, including worst-case, on the OCS to inform the new nationwide CS Program and to protect the environment from CO2 leakage.

Comparison: The study will model CO2 leakage under various scenarios, including worst-case scenarios, using the GOM OCS Region as a case-study and can be applied to all OCS regions. Outcome The leakage and worst-case scenario modeling will aid BOEM’s ongoing rulemaking efforts, program development and implementation, and future operational needs including NEPA analyses, lease planning, lease stipulations, consultations, plan and permit approvals, mitigation measures, risk assessment and monitoring requirements, etc. Study results will also provide direction for future studies to include field and/or laboratory analyses.

The performance period for this important study extends through 2027, so it’s hard to envision final CS regulations prior to that date. You can’t issue regulations without first assessing the potential harm that could result from their promulgation (as required by NEPA).

BOEM’s summary mentions “the anticipation of a CS lease sale in the GOM after final regulations are published.” Hopefully, this also means that BOEM will not permit improperly acquired oil and gas leases (Sales 257, 259, and 261) to be converted to CS leases.

The limited media coverage of the lawsuit originated from a single Reuters article. Apparently Reuters learned about the suit and reached out to the litigants. Their article quoted Louisiana Attorney General Liz Murrill as follows:

“This is a really egregious direct assault on intermediate level producers of oil and gas, and that affects a lot of business in our state,” Murrill told Reuters in an interview.

That quote is all we have from the AGs. Why the absence of announcements:

Interest in working with industry and the Federal govt to seek policy solutions that best address OCS decommissioning issues? (This would be encouraging.)

State of Louisiana, Louisiana Oil & Gas Association, State of Mississippi, State of Texas, Gulf Energy Alliance, Independent Petroleum Association of America and U S Oil & Gas Association

Defendant:

Deb Haaland, U S Dept of Interior, Bureau of Ocean Energy Management, Elizabeth Klein, Steve Feldgus and James Kendall

Case Number:

2:2024cv00820

Filed:

June 17, 2024

Court:

US District Court for the Western District of Louisiana

Presiding Judge:

James D Cain

Referring Judge:

Thomas P LeBlanc

Nature of Suit:

Other Statutes: Administrative Procedures Act/Review or Appeal of Agency Decision

Cause of Action:

28 U.S.C. § 2201 Constitutionality of State Statute(s)

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 (94) and 259 (69).

The 199 oil and gas leases that were wrongfully acquired for carbon disposal purposes remain idle with the government collecting rental payments at the rate of $10/acre/yr ($7 for Sale 257 leases). Collectively, this amounts to approximately $10 million/yr.

Presumably, the lessees cannot claim CCS tax credits for their bonus and rental payments.

The primary term for these leases is only 5 years, and the clock is ticking. The 94 oil and gas leases acquired by Exxon at Sale 257 for carbon disposal purposes are approaching the end of their second year. They would be almost a year older if litigation hadn’t delayed the issuance of Sale 257 leases (break for Exxon?).

No exploration plans have been filed for any of these leases. Presumably Exxon and Repsol do not intend to drill any wells unless the leases are converted to authorize carbon disposal.

The “Infrastructure Bill,” signed 2 days before Sale 257, required the Secretary of the Interior to promulgate regulations not later than one year after the date of enactment (11/15/2021). That deadline has long passed.

The delay in the regulations is understandable given the complex lease management, operational, and environmental issues.

Like the practices and operations they are intended to enable, the regulations are certain to be divisive. Neither the offshore industry nor the environmental community are of one mind on these issues, particularly with regard to the acquisition of oil and gas leases for carbon disposal purposes.

Energy Intelligence suggests that final carbon disposal regulations will be promulgated this year. This is highly unlikely, given that a proposed rule must first be published for public comment.

Publication of a proposed rule prior to the election is unlikely – too controversial.

Presumably, the regulations will establish a competitive process for the conversion of any oil and gas leases.

The leases that were wrongfully acquired at Sales 257, 259, and 261 should not be extended for any period of time, even if their expiration date approaches before a competitive process is established.

Diamond Ocean Blackhawk is drilling MC 40 well for Anadarko

Following up on last year’s deepwater diligence post, 4 recent deepwater exploratory wells (table below) were spudded within 4.5 years of the effective date of their leases.

Particularly noteworthy is Anadarko’s well on newly acquired Mississippi Canyon Block 40, which was spudded only 18 months after the lease was acquired. Everything has to be in place for such an outcome: corporate priority, data gathering and analysis, well plan, permitting, and rig contract/availability.

The well was apparently a high priority not just for Anadarko, but also for Chevron and Murphy. MC 40 was acquired by Chevron (bidding alone) at Sale 257 for $4,409,990, the third highest bid at the sale. Murphy had submitted a losing bid of $3 million, but was assigned a 33% share of the lease by Chevron on 12/15/2023. One month earlier, Anadarko had been assigned a 33% interest and became lease operator.

Interestingly, BOEM’s Mean Range of Value (MROV) estimate for the block was only $576,000, so the three companies are seeing something that BOEM doesn’t. We’ll see how this plays out.

According to rig tracker data the Ocean Blackhawk is still on location at MC 40. Per BSEE permitting data, the well was approved to be bypassed in mid-May.

Decommissioning financial assurance issues are complex!

This blog has raised significant concerns about BOEM’s decommissioning financial assurance rule, and will continue to comment on decommissioning policy. That said, decommissioning issues are complex and have challenged industry and government in the US and internationally for decades. Add well plugging practices, corrosion, storm risks, reefing vs. total removal, alternative uses for old platforms, and pipeline and seafloor equipment abandonment to the myriad of financial issues and you get a sense of the breadth and complexity of decommissioning issues.

Decommissioning is unique in that the issues divide sectors of the offshore industry that are typically aligned (majors vs. smaller producers). The environmental community is also divided with the reefing and fishing advocates opposing those who insist on complete removal.

Given these divisions, and decommissioning’s operational, environmental, and political complexities, highly partisan assertions are common. A recent article about the financial assurance rule includes a number of such assertions, and provides a framework for discussing some of the more prominent issues. Excerpts from the article and my comments follow.

“This costly rule became final on April 15, 2024, but in the 10 months since its initial proposal, BOEM did nothing to alleviate concerns for smaller companies that comprise of 76 percent of oil and gas operators in the Gulf.“

Comments:

While I concur that shelf operations and the independent companies that conduct them are important, 94% of OCS oil production and 80% of the gas (2023 data) were from deepwater facilities (>1000′ WD) which are largely the domain of the majors (although the participation of independents in the deepwater sector is increasing).

In 2023, four majors – Shell, bp, Oxy (Anadarko) and Chevron – accounted for 2/3 of the Gulf’s total oil production.

1467 of the remaining 1527 GoM platforms are in <1000 feet of water and are almost exclusively operated by small producers. So 96% of the platforms are producing only 6% of the oil and 20% of the gas.

This dichotomy presents a major challenge for BOEM which must protect the public from decommissioning liabilities without unfairly penalizing small producers.

Having worked for respected political appointees from both parties, my experience has been that the smaller producers (somewhat surprisingly) have more political influence than the majors. For this reason, along with the general lack of attention to financial assurance issues in the early years of the offshore program, the standard bond requirement was ridiculously low for much of the program’s history, and supplemental financial assurance assessments were typically inadequate (and still are which is why the new rule was promulgated).

Attention to decommissioning issues grew exponentially in the early 1990s. Prior to that time, platform removal, like well plugging, was classified as “abandonment,” a term that was considered too harsh when bankruptcy issues and the Brent Spar controversy in the North Sea attracted worldwide attention.

“Records obtained via the Freedom of Information Act show private meetings between Interior officials and representatives of the major oil companies as they cooperated on this rule.“

Comments:

The linked FOIA records are not at all problematic. They pertain to meetings prior to the publication of the draft rule, which are appropriate and desirable.

Some of these meetings were in response to BOEM’s request for input regarding their review of the OCS oil and gas program. Such meetings are particularly helpful when a new administration is trying to assess the direction of the program.

Indeed 42 of the 71 pages in the FOIA were official industry comments in response to the BOEM request.

Per the Regulations.gov docket on the financial assurance rule, BOEM also met with stakeholders after the proposed rule was published. Those meetings are allowed as long as the regulator simply receives input and does not signal decisions regarding the content of the final rule.

The docket shows that BOEM had 8 listening sessions with advocates for independent producers. These included 2 sessions with the Gulf Energy Alliance and 6 sessions with individual independent producers.

BOEM also had 2 listening sessions with Oceana, a prominent environmental organization, and multiple sessions with tribal organizations.

The only sessions with representatives from major producers were a single session with API and a single session with Shell, the Gulf’s largest producer.

These meetings (after the proposed rule was published) are noted in the docket as required.

I am concerned that many listening session documents (from all sides of the decommissioning financial assurance issue) were removed from the docket at the direction of OIRA/OMB, purportedly because they included privileged information. This is rather troubling given the number of deletions and the complete absence of information about those meetings. What types of privileged information were these organizations providing and why is there no information whatsoever on these meetings? At a minimum, a list of attendees and general summary for each meeting should have been posted, as was our practice in the past.

“Big Oil must think it won’t miss the small competitors the rule will drive from the market.“

Comments:

There is important synergy between the major producers and independents, and no reason for driving smaller companies from the market.

The independents are critical to sustaining the shelf infrastructure and the associated service companies, which helps to facilitate deepwater development. Majors also benefit from partnering with independents on lease acquisitions, development projects, and lease assignments.

Financial assurance for decommissioning of transferred assets is the one area of significant conflict, particularly when there have been multiple ownership changes since the facilities were initially transferred.

“Historically, joint and several liability protected these small businesses from the financial demands of surety bonds.”

Comments:

Surety bonds, or other forms of financial assurance, have always been required. As previously noted, the amounts were often inadequate.

Joint and several liability was not established in the regulations until May 22,1997. Whether companies are liable for facilities transferred prior to that date has yet to be considered in court.

1130 of the 1527 remaining GoM platforms were installed prior to May 22,1997. Many of these platforms were no doubt transferred prior to that date, which means the liability of the initial owner is uncertain.

Predecessor liability does not apply to new wells and platforms constructed by the current lessees.

Joint and several liability was never intended to relieve current lessees from their financial assurance responsibility, which is why assignors were required to provide such assurance. BOEM is correct in strengthening their enforcement of this requirement.

“The new rule is largely silent on joint and several liability, causing some uncertainty.”

Comment: The joint and several liability provision remains in place at 30 CFR 250.1701(a) BOEM has added language to part 556.704, to clarify, correctly in my opinion, that they may withhold approval of any transfer or assignment of any lease interest if the financial assurance requirements have not been satisfied.

Companies may not be able to acquire the needed financial assurances because the market likely will not even exist.

Comment: The history of small producer failures is no doubt a concern to financial institutions. BOEM offers multiple financial assurance options, some of which have been questioned on this blog. If a company can’t qualify, it’s not the responsibility of the public to assume their decommissioning risks.

What makes matters worse is that all this cost covers a risk that is effectively a rounding error historically and in the context of the royalties flowing from the offshore oil and gas industry. According to BOEM, taxpayers have borne decommissioning liability totaling $58 million – from a single company that lacked predecessor owners of the platform to call on to cover unfunded cleanup costs.

Those who seek to minimize the Federal government’s risk exposure should consider the findings in the 2024 GAO report. Per that report, “BOEM held about $3.5 billion in supplemental bonds to cover between $40 billion and $70 billion in total estimated decommissioning costs as of June 2023.”

When will we find out who will be paying the hundreds of millions needed to decommission long-idled Platforms Hogan and Houchin in the Santa Barbara Channel?

Decommissioning financial assurance is a responsibility of lessees, not the taxpayer.

As summarized below and explained in the attachment, the more realistic independent estimates were 2-3 times higher than the operators’ “high end” estimates.