A leaked Dept. of the Interior (DOI) document will likely have little in common with the Draft Proposed Program (DPP, step 2 above). The DPP decisions will be made by the President, not by DOI staffers or managers.

According to media reports, the leaked document includes lease sales offshore New England, the Carolina’s and California. Unless the President revokes his own 2020 withdrawals, the Carolina’s are off-limits until 2032. Ditto for the Eastern Gulf within 125 miles from Florida. (See the map below.)

Including North Atlantic and offshore California in the DPP would unleash a firestorm of opposition. In the case of the North Atlantic, the acreage may not be sufficiently prospective to justify the fight.

To the extent that marine sanctuary determinations do not preclude California offshore leasing, the litigation and legislative battles probably would. In the unlikely event that a sale could be held, who would bid? Who wants to be the next Sable?

The Beaufort Sea is the most likely frontier area to be included in the DPP given plans to open ANWR, operational history, resource potential, and State support.

Assuming the South Atlantic withdrawal could be partially lifted, a small, targeted lease sale would be of great interest to petroleum geologists and could have significant economic and national security implications. The late Paul Post, the foremost expert on the petroleum geology of the US Atlantic, saw great potential in the paleo deep- and ultra-deepwater areas. He advocated exploration concepts proven successful in analogous West African and South American settings where massive discoveries have been made. Samuel Epstein, another prominent petroleum geologist, also believes the deepwater Atlantic has great resource potential.

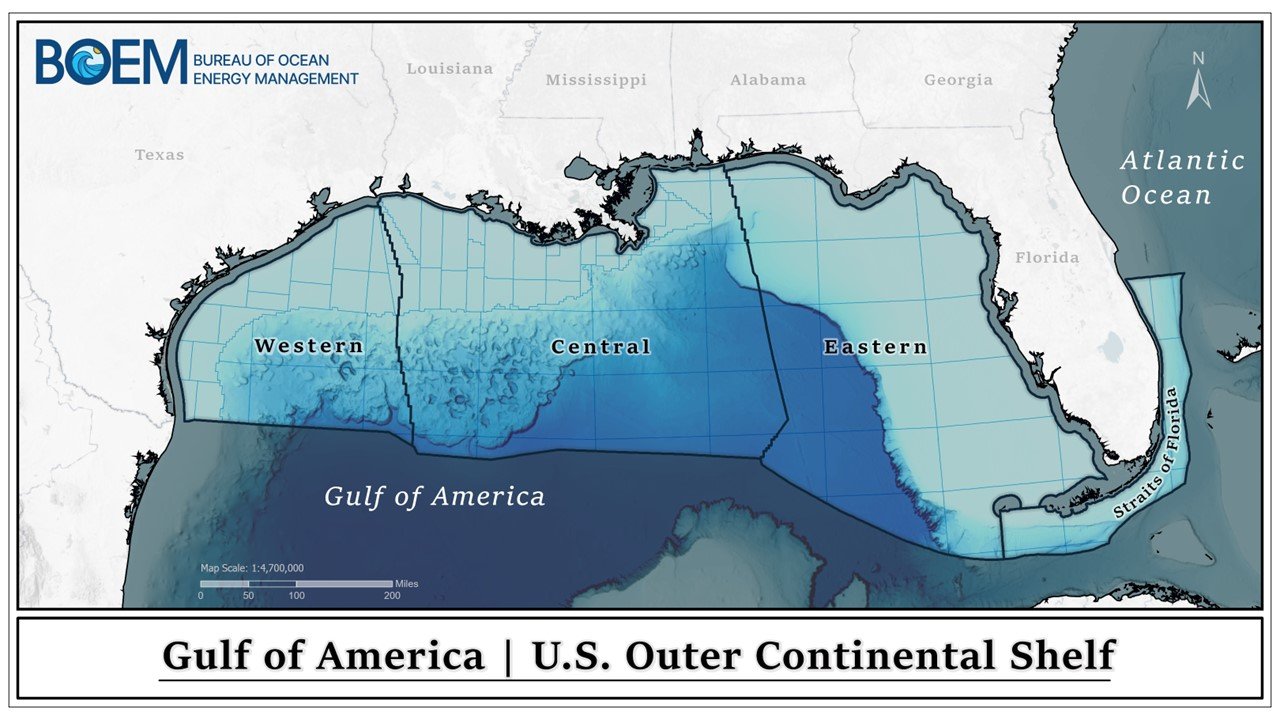

Finally, the extent of the Florida buffer needs to be considered given the high resource potential of the Eastern Gulf. Be it 75, 100, or 125 miles, leasing beyond that buffer should be a priority.

Notably, BOEM’s jurisdiction on the OCS has recently changed. A new planning area offshore Alaska—the High Arctic—is being established as the 27th OCS planning area. Additionally, boundaries of other existing planning areas are being updated to align with BOEM’s revised jurisdiction. Details on these changes will be included in a forthcoming Federal Register notice and posted to BOEM’s website.

“The Bureau of Ocean Energy Management’s analysis reveals an additional 1.30 billion barrels of oil equivalent since 2021, bringing the total reserve estimate to 7.04 billion barrels of oil equivalent. This includes 5.77 billion barrels of oil and 7.15 trillion cubic feet of natural gas—a 22.6% increase in remaining recoverable reserves.”

Year

Number of fields

Original Reserves

Historical Cumulative Production

Reserves

Oil Bbbl

Gas Tcf

BOE Bbbl

Oil Bbbl

Gas Tcf

BOE Bbbl

Oil Bbbl

Gas Tcf

BOE Bbbl

1975

255

6.61

59.9

17.3

3.82

27.2

8.66

2.79

32.7

8.61

1980

435

8.04

88.9

23.9

4.99

48.7

13.66

3.05

40.2

10.20

1985

575

10.63

116.7

31.4

6.58

71.1

19.23

4.05

45.6

12.16

1990

782

10.64

129.9

33.8

8.11

93.8

24.80

2.53

36.1

8.95

1995

899

12.01

144.9

37.8

9.68

117.4

30.57

2.33

27.5

7.22

2000

1,050

14.93

167.3

44.7

11.93

142.7

37.32

3.00

24.6

7.38

2005

1,196

19.80

181.8

52.2

14.61

163.9

43.77

5.19

17.9

8.38

2010

1,282

21.50

191.1

55.5

17.11

179.3

49.01

4.39

11.8

6.49

2015

1,312

23.06

193.8

57.6

19.58

186.5

52.78

3.48

7.3

4.78

2016

1,315

23.73

194.6

58.4

20.16

187.5

53.58

3.57

6.8

4.79

2017

1,319

24.65

195.2

59.7

20.78

188.9

54.21

3.87

6.3

5.00

2018

1,319

24.86

195.5

59.7

21.42

189.8

55.21

3.44

5.7

4.45

2019

1,325

26.77

197.0

61.8

22.12

190.9

56.09

4.65

6.1

5.74

2023

1,336

30.43

201.2

66.2

24.66

194.0

59.19

5.77

7.2

7.04

Oil and gas reserves and cumulative production at end of year, 1975-2023, Gulf of America, Outer Continental Shelf and Slope. “Oil” includes crude oil and condensate; “gas” includes associated and non-associated gas. Reserves estimated as of December 31 each year.

This increase in reserves will not please those responsible for the current 5 Year Oil and Gas Leasing Plan. They told us that we don’t need more OCS lease sales and that our biggest concern is producing too much oil and gas for too long!

The long-term nature of OCS oil and gas development, such that production on a lease may not begin for a decade or more after lease issuance and can continue for decades, makes consideration of net-zero pathways relevant to the Secretary’s determinations on how the National OCS Program best meets the Nation’s energy needs.“

“Crude reserves are being found and developed at a much slower pace than they’ve been in the past. Specifically, she said the world has only newly identified less than half the amount of crude it’s consumed over the course of the past 10 years. Given the current trends, this means demand will exceed supply before the end of 2025.“

A bit off-topic, but Jeff Walker, a former colleague and the MMS Regional Supervisor in Alaska, had the best quip about reserve numbers. In explaining an operator’s revised reserve numbers for a producing unit which had leases with different royalty rates, Jeff noted that “oil always migrates to the lower royalty leases.”😉

Of particular interest are mandated reviews of the:

RIsk Management and Financial Assurance Rule: Those who want to gut this rule should come to the table with proposals that better protect the taxpayer from decommissioning liabilities. Pretending that decommissioning financial risks don’t exist or that they are someone else’s (or the govt’s) problem is unacceptable.

5 Year leasing program – This review is urgently needed. See this and this!

BOP/Well Control Rule – This keystone safety rule has undergone multiple reviews in recent years. Because of the rule’s importance, further review for continuous improvement purposes may nonetheless be warranted. Here are the blog comments on the current version of the rule.

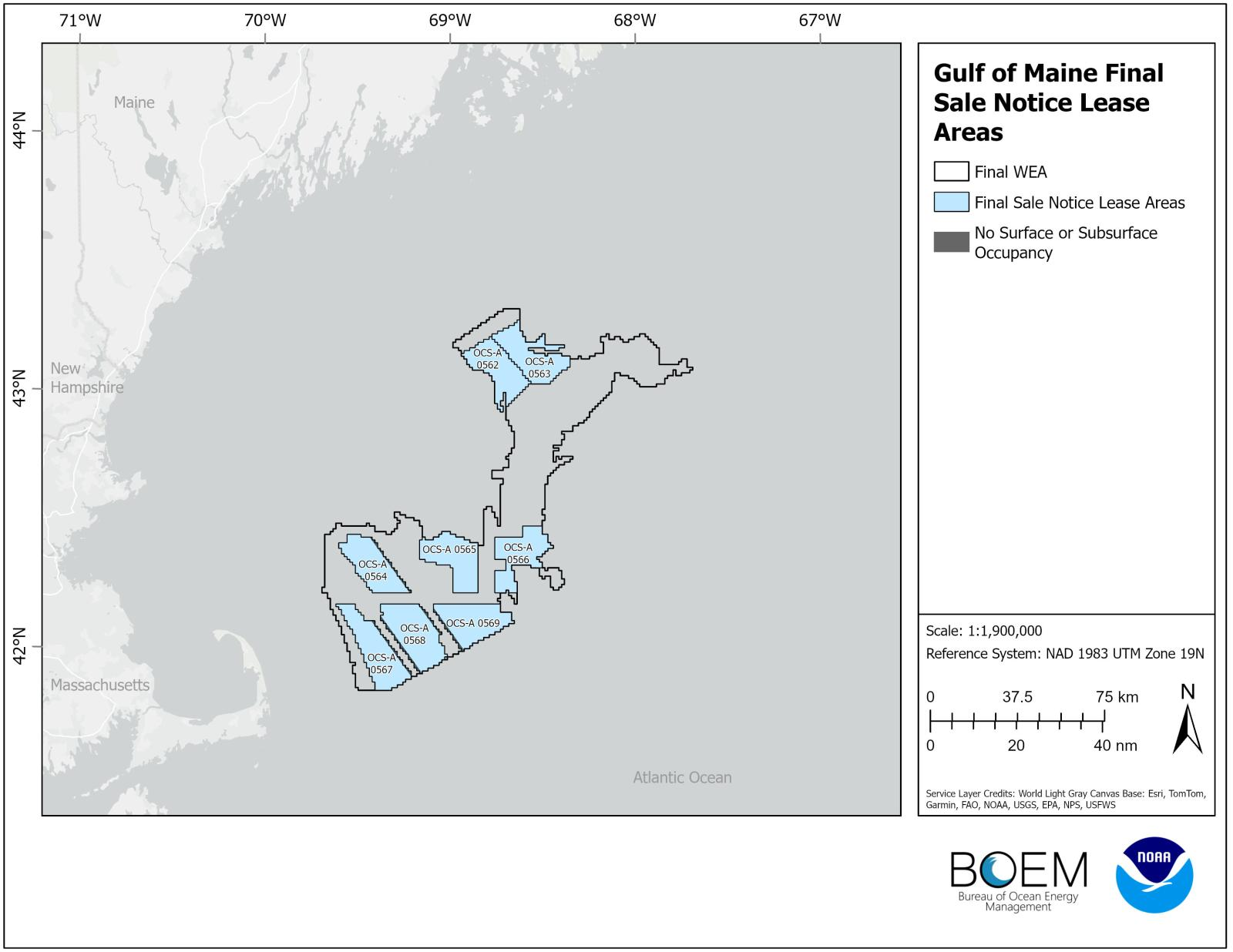

Gulf of Maine Final Lease Areas, Acres, and Assigned Region

Lease Area ID

Total Acres

Developable Acres

OCS-A 0562

97,854

97,854

OCS-A 0563

105,682

105,682

OCS-A 0564

98,565

93,756

OCS-A 0565

103,191

103,191

OCS-A 0566

96,075

96,075

OCS-A 0567

117,780

113,208

OCS-A 0568

124,897

116,363

OCS-A 0569

106,038

101,757

Total

850,082

827,886

Average

106,260

103,486

Note that the ave. lease size is 18.4 times larger than a typical Gulf of Mexico oil and gas lease

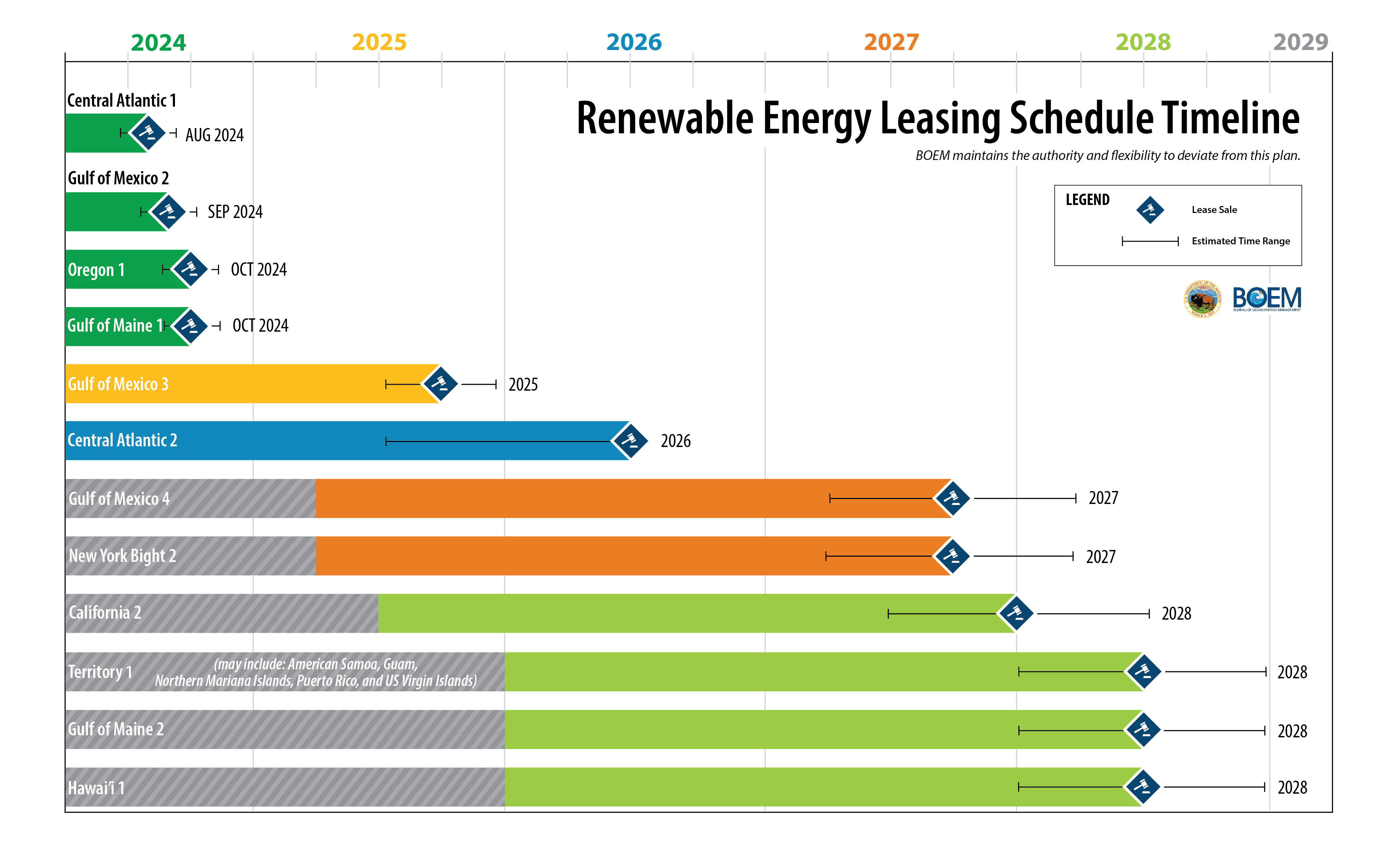

Today’s Gulf of Maine sale will likely be the last wind lease sale for at least a year.

Per a provision in the “Inflation Reduction Act,” no offshore wind leases may be issued after 12/20/2024, the one year anniversary of the last oil and gas lease sale (no. 261).

The date of the next oil and gas lease sale is anyone’s guess. Next week’s elections are, of course, the elephant in the room. However, there is also an enormous ruling by a Federal judge in Maryland that would halt the issuance of Gulf of Mexico oil and gas leases and the approval of operating plans effective Dec. 20, 2024. Ironically (or perhaps not?), this is the same date after which no wind leases may be issued absent an oil and gas lease sale.

Chevron and industry trade associations have appealed Judge Boardman’s ruling. (Given the enormous implications of that ruling on current and future Gulf of Mexico production, I’m curious as to why Chevron is the only major producer that is a party in this appeal. Chevron was also the only producer that was a party in the litigation overturning the restrictive Sale 261 lease sale provisions. I’m assuming there is some legal or tactical reason for the absence of participation by Shell, bp, and Oxy?)

Finally, given the legislation linking future wind sales with oil and gas sales, are the Sierra Club et al, the plaintiffs in this case, comfortable with Judge Boardman’s decision? Perhaps they are okay with the judge’s ruling given the absence of any planned Atlantic wind leasing until 2026?

2024 will be the first year since 1958 without a single OCS oil and gas lease sale. There would not have been a sale in 2023 either were it not for a legislative mandate. The only 2022 lease sale was a micro-sale in the Cook Inlet that resulted in only a single bid. So, at the end of 2024 three years will have elapsed with only one meaningful sale, and that sale was mandated by Congress.

The current plan is for these de facto sanctions on US offshore production to continue. The Dept. of the Interior’s 5 year leasing plan includes a maximum of 3 sales, by far the fewest sales in any 5 year plan in OCS program history.

Meanwhile, the sanctions on Venezuelan production were further eased with the understanding that the Maduro regime would hold fair elections. To the surprise of no one, the evidence strongly suggests that those elections were not fair. Nonetheless, the sanctions on production have not been reimposed.

Apparently, the climate activists who have imposed their will on the OCS oil and gas program have less influence over our policy toward Venezuela. Or perhaps the production (and consumption) of Venezuelan oil is cleaner and greener (🙃 sarcasm intended!)

API is challenging the Dept. of the Interior’s 5 year oil and gas leasing plan, which includes the fewest lease sales in program history. That challenge was filed on 12 February, 60 days after Secretary Haaland approved the 5 plan and the first day appeals could be filed pursuant to 43 U.S. Code § 1349.

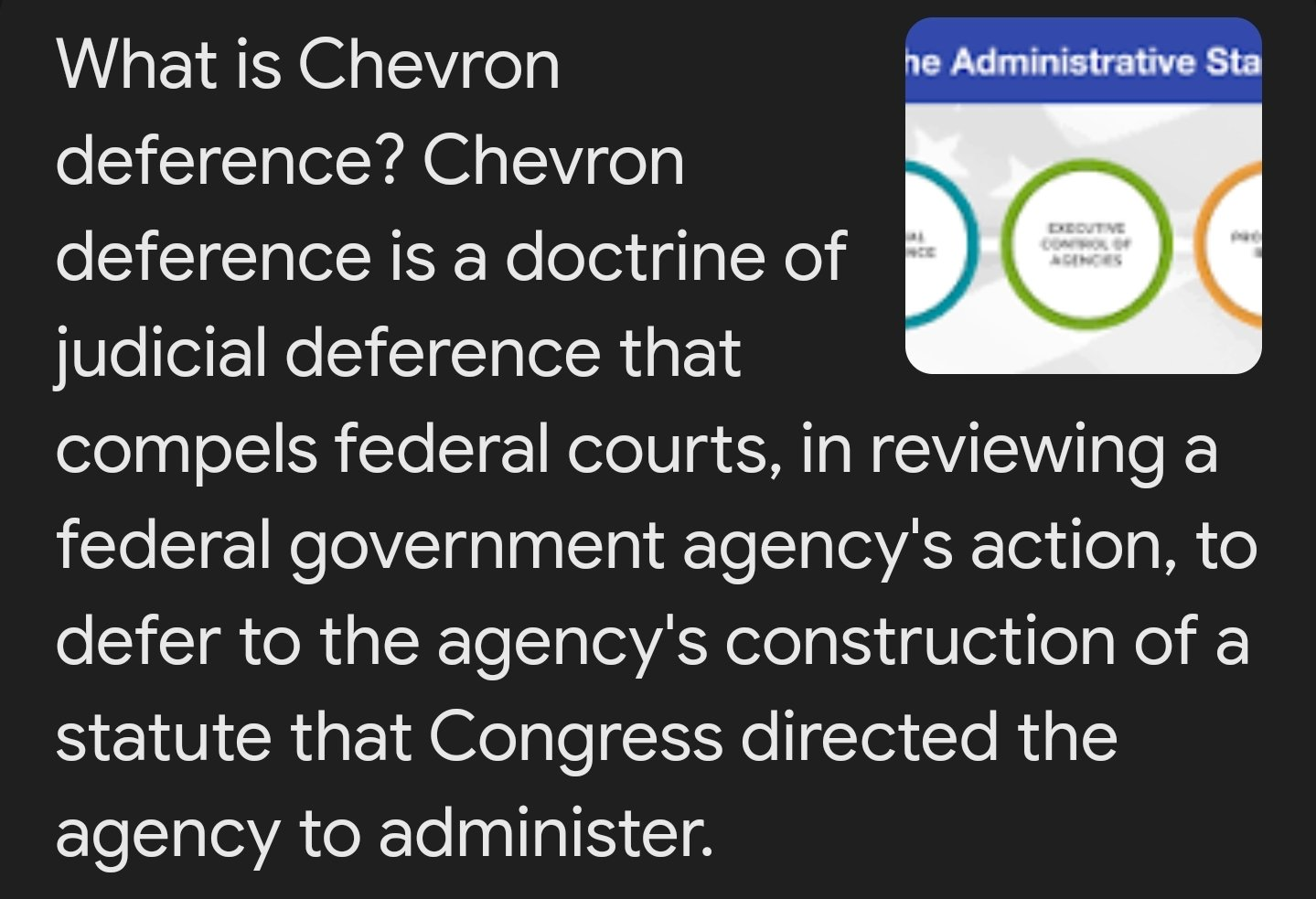

18 weeks after the API suit was filed, the Supreme Court overturned the Chevron Doctrine. That doctrine (described above) instructed judges to defer to agency interpretations when the language in a law was unclear.

Extending the Secretary’s general safety and environmental authority for OCS operations to include global climate considerations is a stretch and the type of interpretive administrative decision that the Supreme Court struck down.

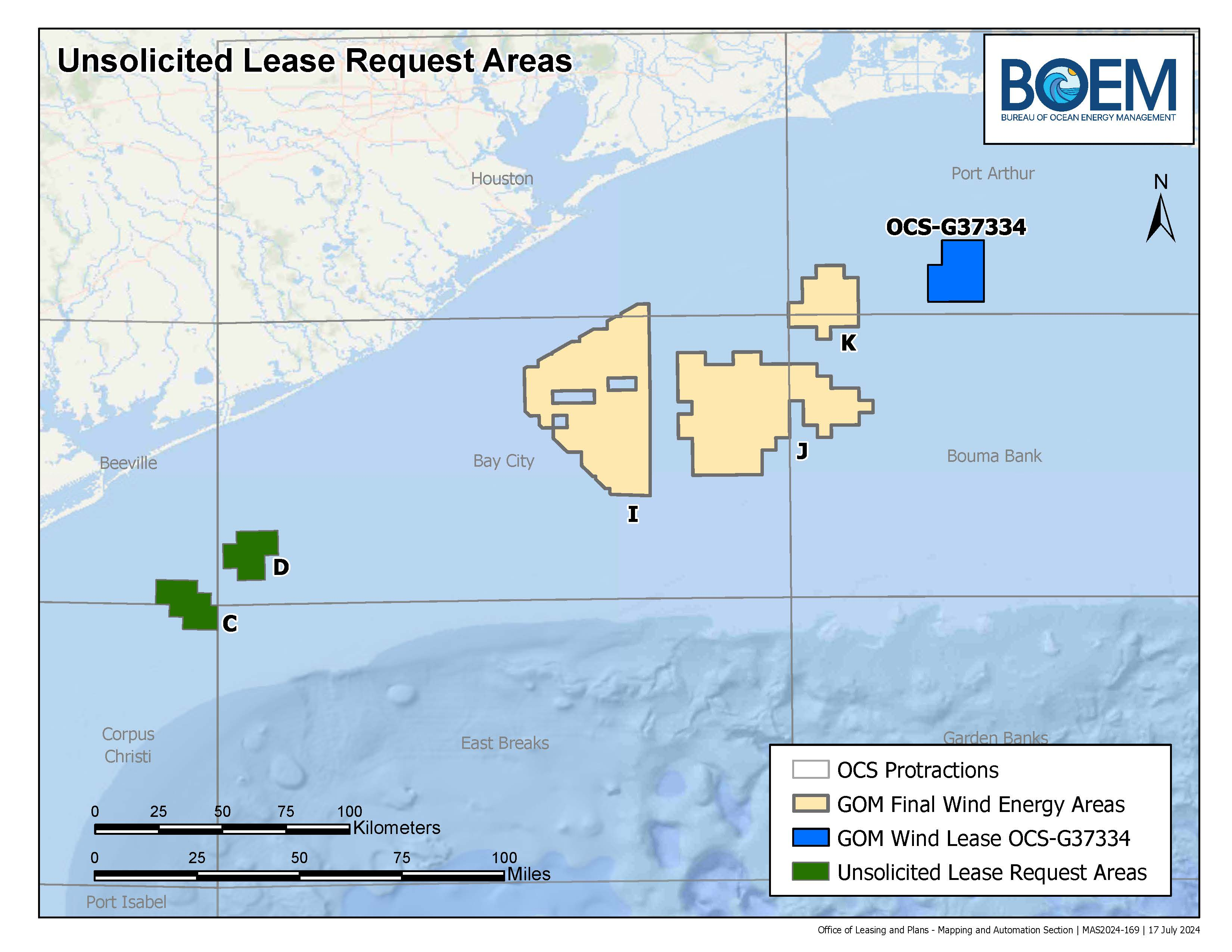

Hercate lease request – C & D. Wind areas that were considered for 2nd GoM sale – I, J, & K. Active RWE lease – blue.

GoM wind leasing update:

BOEM’s highly promoted 2023 GoM wind sale was a bust. The sole bidder, the German company RWE, acquired a single lease.

BOEM’s second GoM wind sale failed to get off the ground. Because only one company expressed interest in participating, that sale has been cancelled.

BOEM is now surveying interest in other GoM areas as a result of an unsolicited lease request from Hercate Energy.

If BOEM does not receive competing indications of interest, they may (and probably will) issue a noncompetitive lease to Hecate.

BOEM calls Hercate an “industry leader.” However, per their website, Hecate is mainly a solar energy company with only 2 wind projects. Both of those wind projects are onshore (Kentucky), and are “in development” (i.e. not yet operating). Hercate is no doubt a fine company, but have they demonstrated the technical expertise and financial strength needed for offshore wind development?

BOEM’s aggressive wind leasing policy stands in stark contrast to their current oil and gas policy. Not a single oil and gas sale will be held in 2024. Were it not for a provision in the “Inflation Reduction Act,” the last 3 GoM sales (257, 259, and 261) would probably not have occurred.

The new 5 year oil and gas leasing plan confirms that the Dept. of the Interior (DOI) has no intention of fulfilling their statutory oil and gas leasing mandate. In announcing the new 5 year plan, DOI boasted that the plan includes the fewest sales (3) of any plan in the history of the program. DOI strongly implied that the only reason those 3 sales were included was to sustain the wind program.,

When we drafted the OCSLA amendments that authorize offshore wind leasing, we envisioned complementary and synergistic programs, not a dogmatic pro-wind bias. As experts like Daniel Yergin have repeatedly warned, the notion that wind energy can eliminate the need for oil and gas is pure folly.

“We will do everything we can to make sure that the market is supplied well enough to ensure as low price as possible for American consumers,” Hochstein told the newspaper. “I think that we have enough in the SPR if it’s necessary.” ~Amos Hochstein, Special Presidential Coordinator for Global Infrastructure and Energy Security.

Maybe they should remove “Energy Security” from his impressive title since that seems to be a low priority.

Apparently it’s fine (and environmentally friendly) to deplete strategic oil reserves to reduce prices prior to an election, but not to hold regular oil and gas lease sales in the adjacent Gulf of Mexico. 2024 will be the first year without an OCS lease sale since 1958, and the Administration bragged about the new 5 year leasing plan having the fewest proposed sales in history!

“Consistent with the requirements of the Inflation Reduction Act (IRA) concerning offshore conventional and renewable energy leasing, the Department of the Interior today published the final 2024–2029 National Outer Continental Shelf Oil and Gas Leasing Program (Program) with the fewest oil and gas lease sales in history.

These three lease sales are the minimum number that will enable the Interior Department’s offshore wind energy program to continue issuing leases in a way that will ensure continued progress towards the Administration’s goal of 30 gigawatts of offshore wind by 2030.”