- The UK Met Office told Recharge that the historic trend of wind speeds in Britain was downwards. “The UK annual mean wind speed from 1969 to 2024 shows a downward trend, consistent with that observed globally. There have been fewer occurrences of maximum gust speeds exceeding 40/50/60 knots in the last two decades compared to the 1980s and 1990s.”

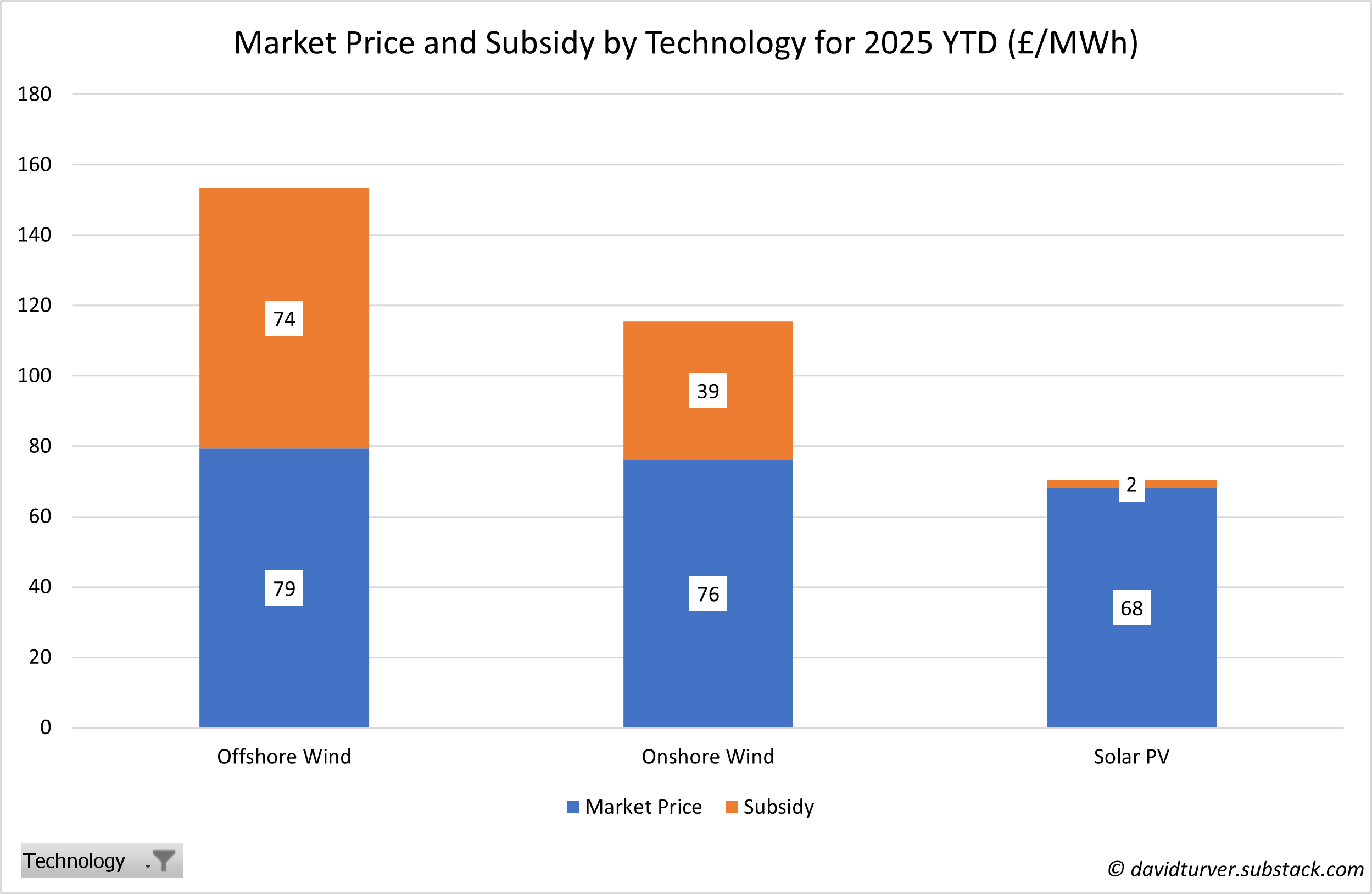

- Citigroup informs that load factors for both onshore and offshore wind are falling behind capacity growth in Britain’s turbine fleet.

- Per the Citigroup analysts, the increasing focus on wind wakes in UK waters has led to a ballooning number of disputes between developers.

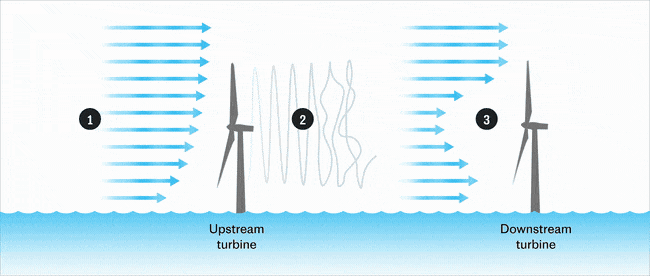

- Entire wind farms can influence each other through large-scale wake effects. These farm wakes have been observed to extend more than 100 km downstream from a wind farm and can cut the yield of turbines in the wake by tens of percents.

- In addition to wake losses, local turbulence in the wake regions creates significant unsteady fatigue loads on the downstream turbines, which shorten their working life.

- Wind wakes grow with turbine size. Bigger wind turbines deliver financial economies of scale, but don’t greatly increase the total power per unit area because they must be spaced farther apart

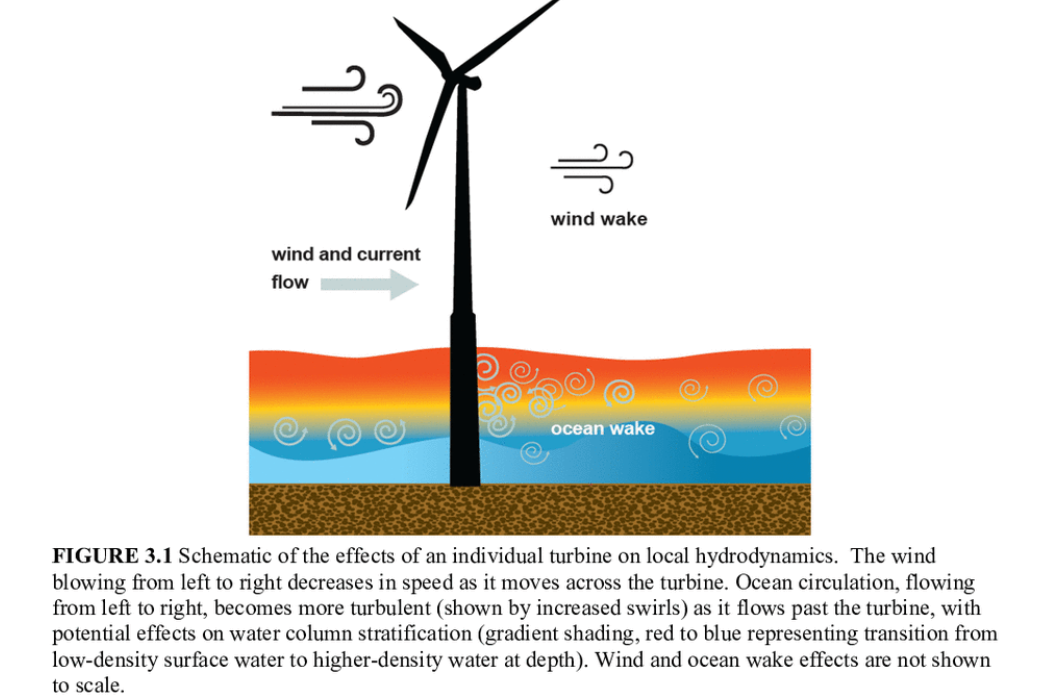

- A recent study shows that hydrodynamic conditions in the ocean altered by wind wakes can strongly influence marine primary production (phytoplankton).

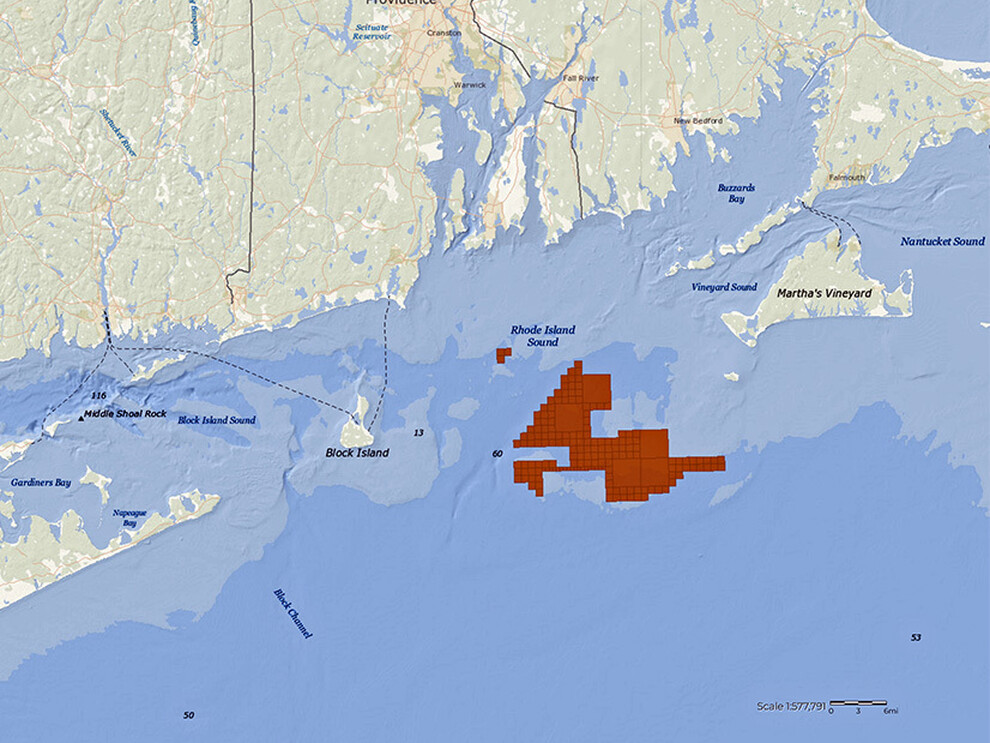

- The US National Academy of Sciences advised BOEM about the hydrodynamic effects of wind turbines and the potential implications for the endangered North Atlantic right whale (see figure below).

Wind resource management is reminiscent of the early years of oil production when the “law of capture” reigned supreme and wasteful production practices were a self-defense mechanism.

Interesting case: Delaware litigation on approval of the Coastal Construction Permit for the Maryland Offshore Wind Project

Posted in decommissioning, energy policy, Offshore Wind, Regulation, tagged Coastal Construction Plan, court filing, decommissioning, Delaware litigation, Maryland Offshore Wind, public comment, US Wind on October 29, 2025| Leave a Comment »

The Dept. of the Interior is currently reconsidering approval of the Construction and Operations Plan for the Maryland Offshore Wind Project (US Wind).

Attached is a court filing challenging Delaware’s approval of the Coastal Construction Plan for that project. Some interesting points from the filing:

Read Full Post »