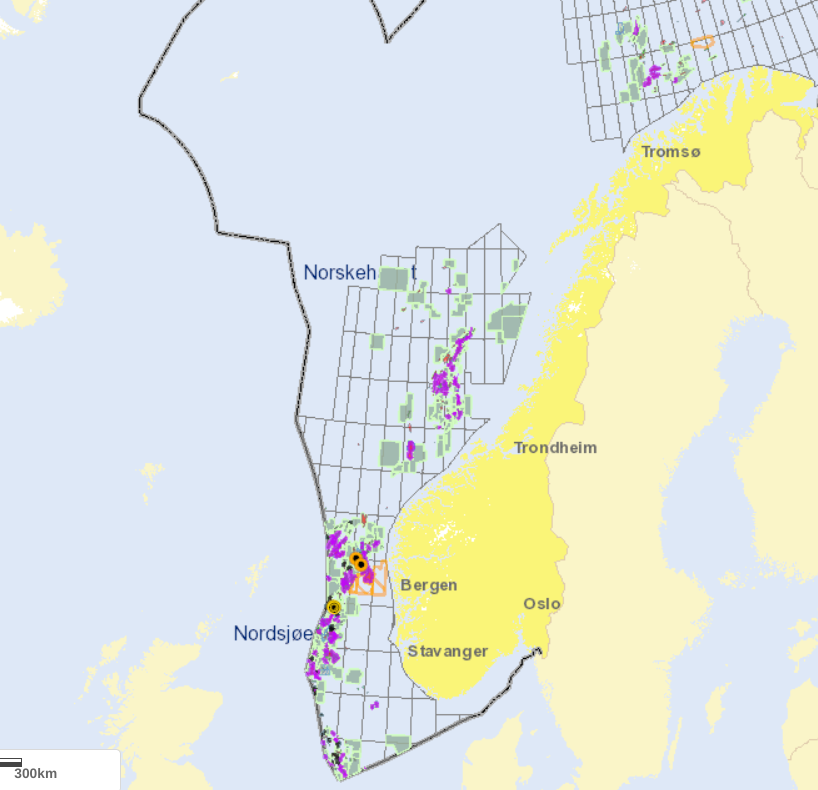

OSLO, June 28 (Reuters) – Norway’s government said on Wednesday it has given approval for oil companies to develop 19 oil and gas fields with investments exceeding 200 billion Norwegian crowns ($18.51 billion), part of the country’s strategy to extend production for decades to come.

“These are projects that will contribute to a continued high and stable output from Norway’s continental shelf as well as employment and value creation,” Minister of Petroleum and Energy Terje Aasland told a news conference.

The Bureau of Ocean Energy Management (BOEM) today announced proposed changes to modernize financial assurance requirements for the offshore oil and gas industry, in order to better protect American taxpayers from incurring the costs associated with the oil and gas industry’s responsibility to decommission offshore wells and infrastructure, once they are no longer in use. The proposed changes will publish in the Federal Register on June 29, which will open a 60-day public comment period that ends on August 28.

It looks like BOEM punted on the contentious issue of considering predecessors when determining financial assurance requirements:

The proposed regulatory changes would provide additional clarity and reinforce that current grant holders and lessees bear the cost of ensuring compliance with lease obligations, rather than relying on prior owners to cover those costs. BOEM is interested in public comments on the costs and benefits of considering predecessors when determining how much financial assurance a company must provide.

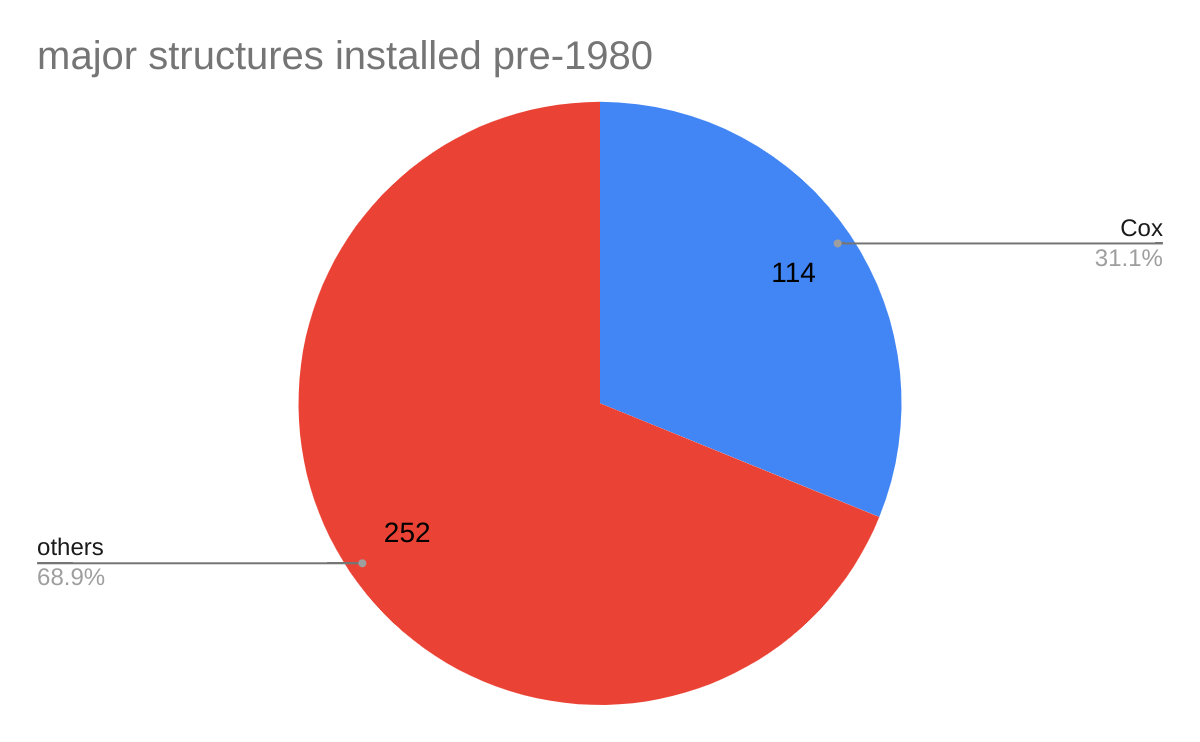

As illustrated in the charts below, Cox has the distinction of being the Gulf of Mexico (world?) leader in aging offshore platforms. Per BOEM data, Cox (includes affiliates Energy XXI GOM and EPL) operates more than 1/4 of all GoM platforms. 44% of these platforms were installed prior to 1980, 114 of which are major structures (defined in notes below). 27 of these major structures were installed prior to 1960!

Notes: (1) A major structure contains at least 6 well completions or more than 2 pieces of production equipment. (2) The platform numbers in an earlier post are incomplete in that they include only structures with helidecks.

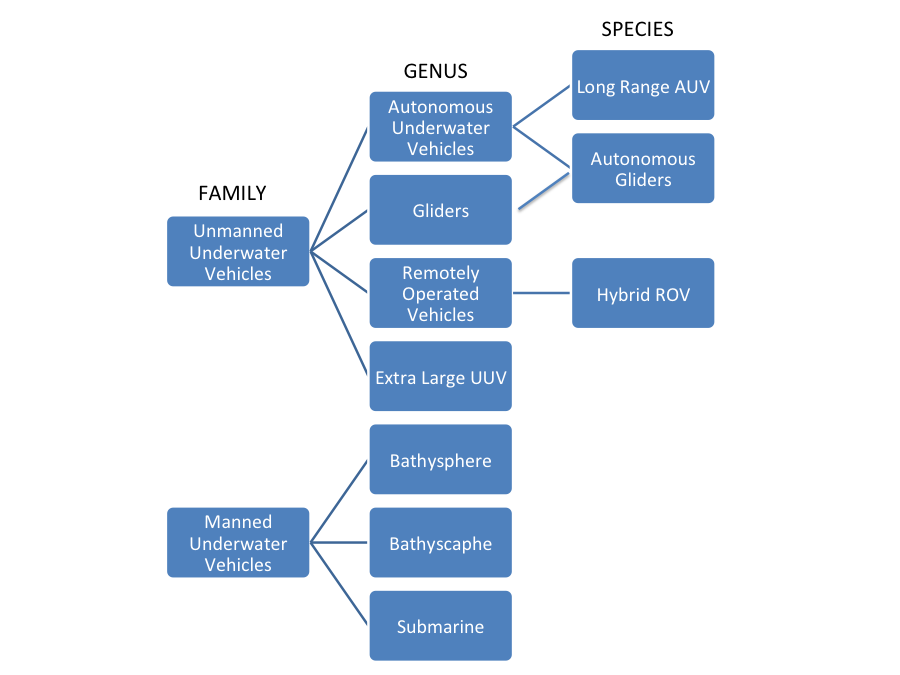

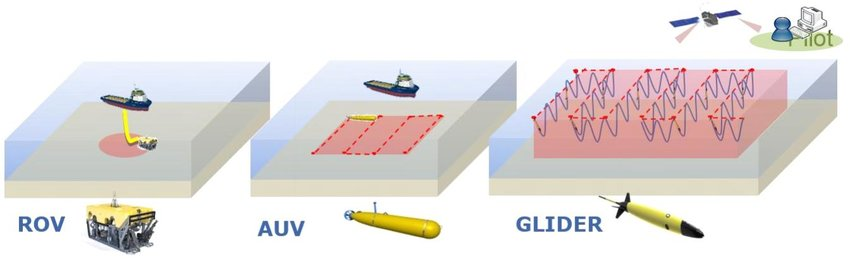

From the outset, deepwater oil and gas exploration and development were not dependent on divers or manned submersibles – far too dangerous. UUVs are used for maintenance, inspections, surveys, positioning equipment, and other operational purposes.

UUV technology advanced with demand as deepwater discoveries drove worldwide exploration and production. In 2021, deepwater (>1000′) leases accounted for 93% of GoM oil production and 76% of the gas production. For comparison, in 1985 only 6.0% of the oil and 0.8% of the gas were from deepwater leases.

In 2021, TechnipFMC won NOIA’s Safety in Seas Award for the Gemini® ROV System which can dive for a month at a time and change tools subsea instead of on deck. The Gemini® ROV System also includes a blowout preventer intervention system that supports well control and pipe shearing functions.

Below is a taxonomy for UUVs. The linked article provides further details. Gliders are particularly useful for surveying given the large distances they can cover (last image).

The preliminary NTSB report was posted on 1/18/2023, but the final report has still not been published. Status update:

Will the investigators consider longstanding regulatory fragmentation issues? The most recent Coast Guard – BSEE MOA for fixed platforms added to helideck regulatory uncertainty by assigning decks and fuel handling to BSEE and railings and perimeter netting to the Coast Guard. This is the antithesis of holistic, systems-based regulation.

So at this time, some theories on the culprits appear to have dropped out. Those that are still in play include various versions of the Ukrainian rental yacht narrative and the Hersh account. Hopefully, the responsible parties will be identified, but given the political stakes, this is becoming increasingly unlikely.

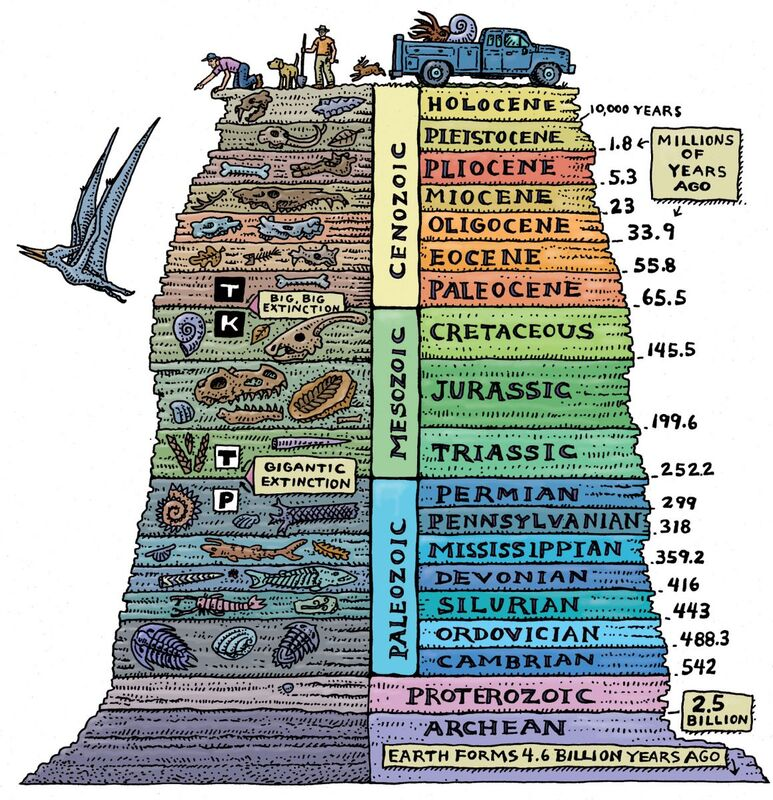

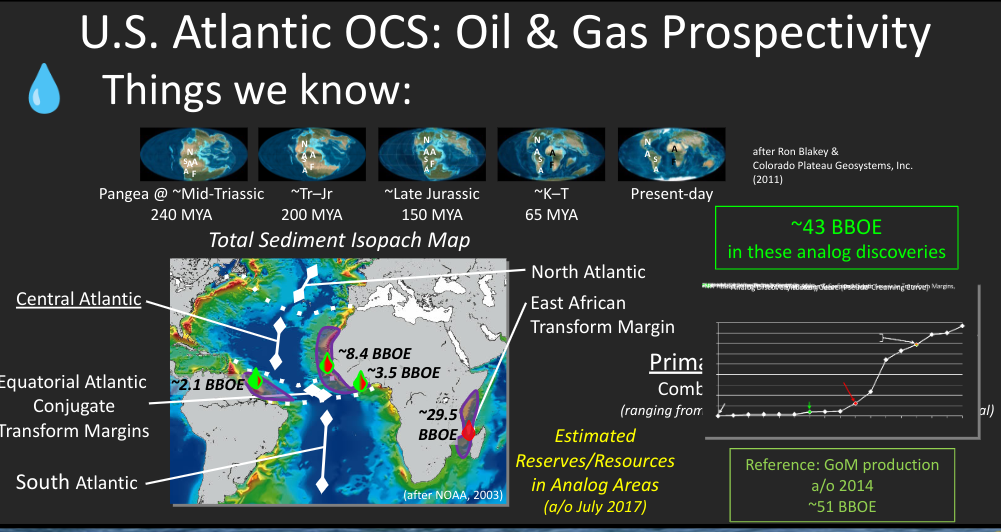

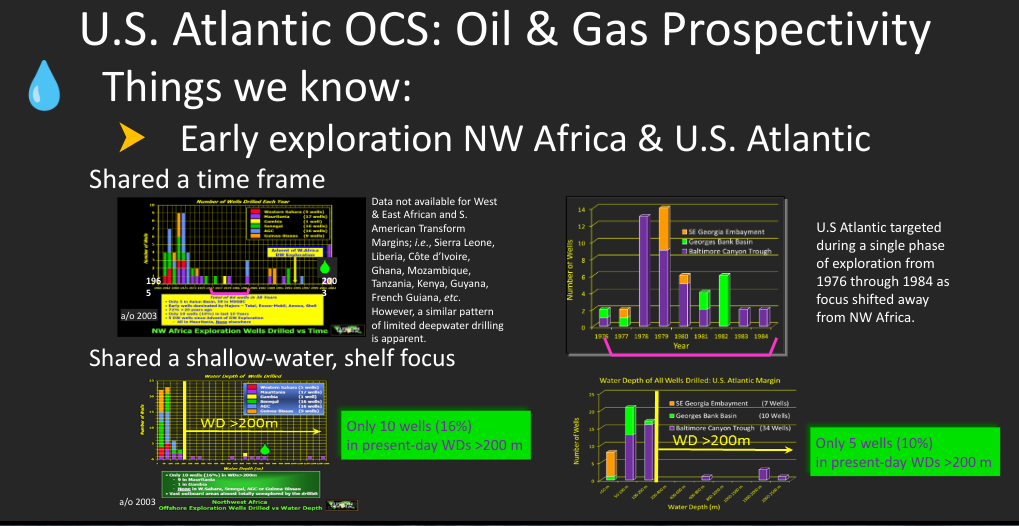

Until the late Triassic period, Virginia, the Carolinas, and Georgia were cojoined with Mauritania and Senegal as part of the Pangea super-continent. These Pangea neighbors share a common ancient geology.

Paul Post believed the untested West African analogs in the US Atlantic were highly prospective, and could contain >20 billion BOE. Paul was not alone in his thinking about Atlantic resource potential. Sadly, Paul is no longer with us 😥, so I’m sharing a few of his slides as a reminder of his important work. I have also attached his 2016 report and am linking the 2021 update.

Given the current Atlantic moratoriums and the steep legal, social, and political barriers that would have to be cleared, evaluating the US Atlantic is not imminent. However, nearly all Atlantic nations and their Caribbean and North Sea cousins have exploration programs and some have been wildly successful. Oil and gas consumption will be stable or growing for the foreseeable future, and it’s important to better understand the petroleum potential of our Atlantic continental margin.

Last week, BOEM announced the acceptance of all 69 of Exxon’s Sale 259 carbon sequestration bids. This is despite these facts: (1) Exxon’s intentions were known, (2) there were no provisions for CCS bidding in the Notice of Sale, (3) no environmental review of CCS leasing was conducted, and (4) there are no procedures for evaluating CCS bids.

Absent some type of legislative maneuver, carbon sequestration is not authorized under these leases. If Exxon is just acquiring the leases for evaluation purposes in preparation for a possible CCS sale in the future, their lease acquisitions may be okay. If they are planning on retaining these leases for actual sequestration operations, that is not okay, at least not until a competitive process has been established for awarding or reclassifying such leases.

It’s also noteworthy that there was a second bidder for th blocks (in red above). Presumably that company, Focus Exploration, was interested in acquiring the tract for oil and gas exploration purposes. However, the Focus bid was a bit lower, so Exxon got the tract.

Along with Cox Operating, six affiliates also filed: MLCJR , M21K, EPL Oil & Gas, Cox Oil Offshore, Energy XXI Gulf Coast, and Energy XXI GOM.

The BOEM platform data base lists only Cox Operating (276 platforms), EPL (10 platforms), and Energy XXI GOM (26 platforms) as current operators of OCS platforms. However, according to the Cox Operating website, the company operates 600 producing wells on 500 structures. Presumably, ~200 of those structures are in State waters.

In 2020, the OPEC price war drove oil prices down, while stay-at-home orders and well shut-ins associated with the COVID-19 global pandemic sharply reduced production.

The debtors’ assets suffered significant damage from five named storms and hurricanes during 2020 and 2021, leading to further reductions in production. Comment: According to BSEE, 7 tropical systems affected GoM operations in 2021, so the number of storms is not in dispute. The extent to which maintenance or preparedness issues contributed to the damage is unknown.

In 2020, a foreign-flagged vessel struck a platform owned by one of the debtors resulting in major damage and substantial losses of production. Comment: Apparently, this is the incident being cited. According to the BSEE report, the operator (Cox) was not at fault. Per BSEE: (1) The navigational lights and foghorn on the platform were maintained and in operational order, (2) the allision was not due to any platform related error, and (3) the platform’s operator and safety system responded in accordance with the regulations.

At this time, the debtors’ production volume is half what it was in 2019. Comment: Comparing the 2019 and 2022 production data, OCS oil and gas production are down by about 30% and 40% respectively. However, the 50% reduction figure seems reasonable given the likelihood of further reductions in State water production and in 2023.

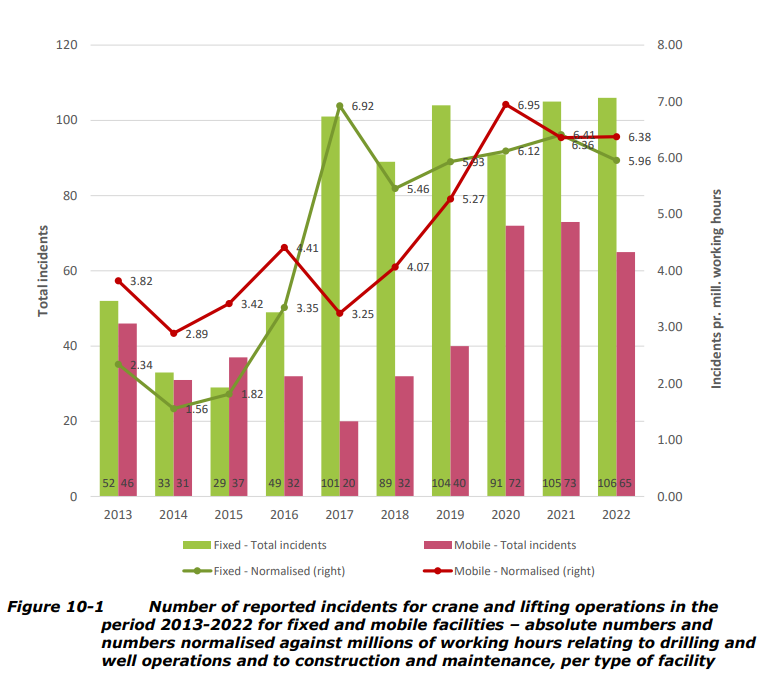

A recent fatal incident involving a person working on an offshore oil and gas facility has provided a tragic reminder of the risks of work involving the rigging, manipulation and movement of loads, including people and equipment.

Despite the international focus on lifting operations over the past 30 years, Norwegian and US data do not suggest improved performance. PSA Norway’s “Trends in risk level on the Norwegian Continental Shelf” report shows an increase in lifting incident rates for both fixed and mobile facilities over the past 10 years (first chart below).

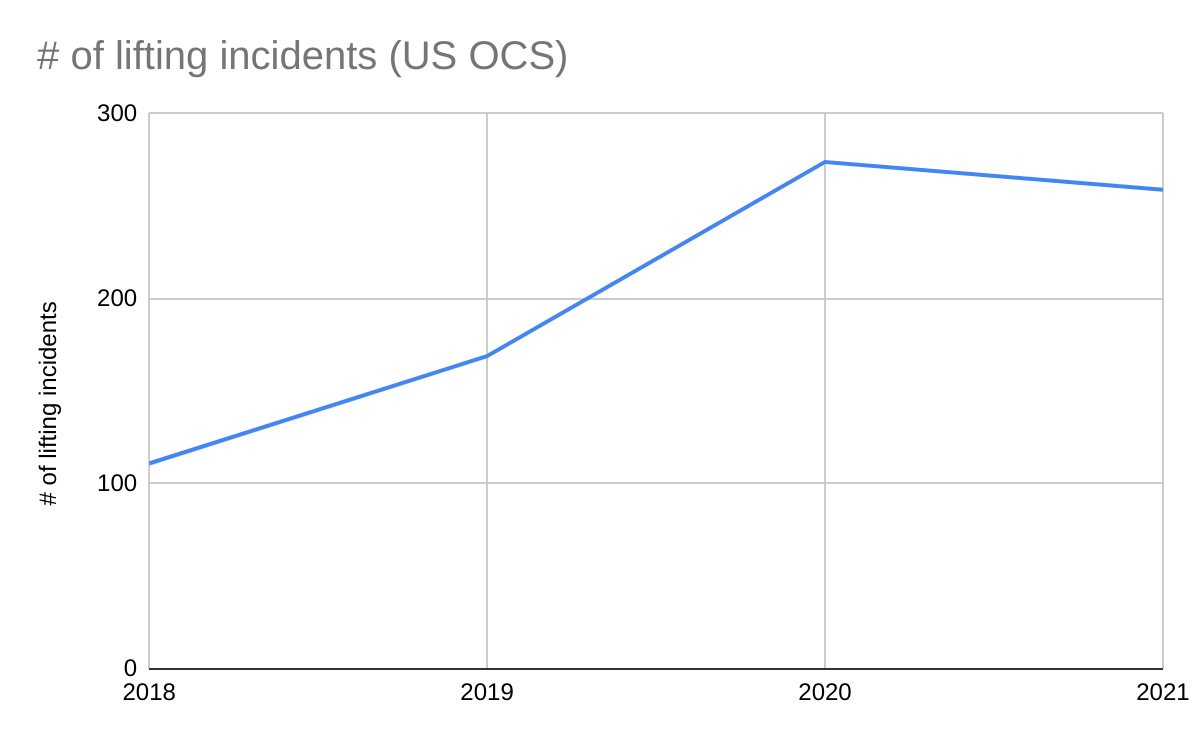

Similarly, recent lifting data from BSEE’s incident tables (summary below) and Jason Mathew’s June 2022 presentation (pages 48-63) suggest that lifting risks are not being effectively mitigated. Why are industy/regulator messages regarding hazard identification and controls not achieving the desired results? Perhaps a fresh look and renewed dialogue are needed.

Crane or personnel/material handling incident (as used in 30 CFR 250.188(a)(8)) refers to an incident involving damage to, or a failure of, the crane itself (e.g., the boom, cables, winches, ballring), other lifting apparatuses (e.g., air tuggers, chain pulls), the rigging hardware (e.g., slings, shackles, turnbuckles), or the load (e.g., striking personnel, dropping the load, damaging the load, damaging the facility) at any time during exploration, development, or production operations on the OCS. This includes all incidents of shock loading that, upon inspection, reveals damage to any part of the crane, lifting apparatus, rigging hardware, or load. Personnel handling incidents include events involving swing ropes, personnel baskets, and any other means to move personnel. Material handling incidents include any activities involving the loading and unloading of material and moving it on, off, or around an OCS facility.