Several actors have approached the ministry with a desire to be allocated two specific areas for storage of CO 2 . One area in the North Sea and one in the Barents Sea were therefore announced on 10 September in accordance with the storage regulations.

By the application deadline of 9 December, the ministry had received applications from five companies. The Ministry will process the received applications and allocate area in accordance with the storage regulations during the first half of 2022.

Contrast the situation in Norway with Exxon’s apparent attempt to acquire 94 Gulf of Mexico leases at Oil and Gas Lease Sale 257 solely for CCS purposes. BOEM’s Notice of Sale made no mention of CCS, and there had been no environmental or economic assessment of CCS activity.

And how much will the public pay for grand CCS ventures that (although interim measures) will take years to initiate, add new safety and environmental risks, and may never achieve their objectives? The public burden will no doubt include direct subsidies, tax credits, increased petrochemical prices, and the erosion of purchasing power associated with the resulting inflation pressures.

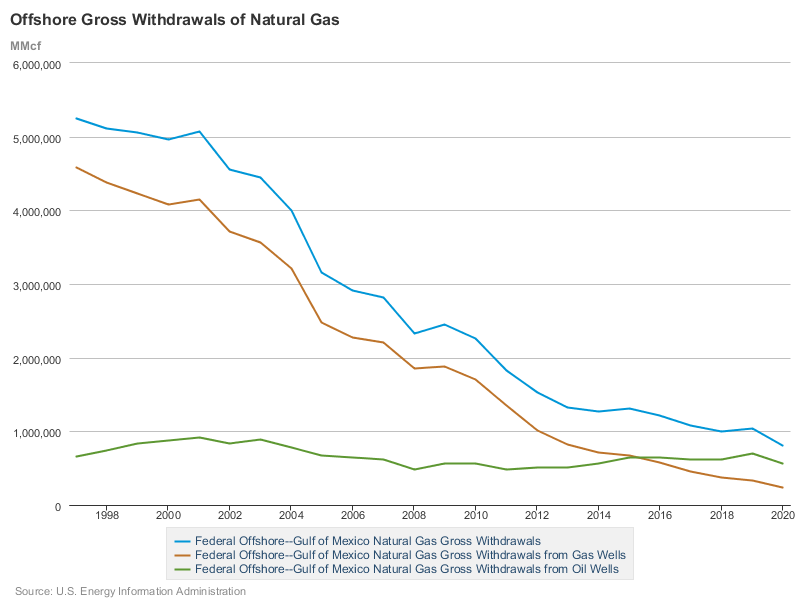

Offshore gas production (see chart below) has declined for the past 20 years and now accounts for only 4% of total US gas production, down from 20% in 2005 and 25% in the 1990s. Associated gas production (oil-well gas) has remained relatively constant owing to the strength in deepwater GoM oil production. 73% of 2020 gas production was from deepwater wells, and was mostly oil-well gas. Associated gas production surpassed nonassociated gas production (gas-well gas) in 2016 and the latter has continued to decline.

The case for natural gas has been well documented (see the EQT letter linked below). Recent natural gas advocacy has emphasized the carbon/GHG advantages given that methane (CH4) is essentially a hydrogen transporter that emits far less CO2 than other fossil fuels when burned. However, natural gas’s other important air quality advantages – low NOx. SO2, and particulate emissions – have greater local significance from a human health standpoint. Those who have ridden a bike behind a natural gas powered bus have no doubt experienced the natural gas advantage firsthand. These buses are literally a breath of fresh air!

Other environmental advantages of offshore natural gas, particularly nonassociated gas, receive less attention but are nonetheless significant. Advantages of nonassociated offshore gas include the following:

Fewer wells required than for shale gas

No risk of fresh water contamination

Platforms provide beneficial reef effects

Minimal space preemption and land disturbance relative to onshore gas production and wind/solar operations

Low facility density and navigation risks relative to wind operations;

Lower elevation and fewer view-shed, aesthetic, and aviation issues than for wind

Minimal avian risks relative to on- and offshore wind operations

Minimal spill risk relative to oil and associated gas production

Significantly less flaring than for oil well gas. While the overall % of US offshore gas production that is flared is low (approx. 1.0 -1.5% from 2016-2020 per EIA data), the % of gas-well gas that is flared has historically been less than 0.5%.

Low natural gas prices and competition from nimble and efficient shale operations have constrained offshore gas exploration. Ultradeep (subsurface) drilling has shown promise from a gas resource perspective but has proven to be expensive and operationally challenging. Some independent producers are still acquiring gas prone shelf tracts and that needs to be encouraged. Consideration should be given to incentives such as making nonassociated gas production royalty free. That would certainly seem preferable to subsidizing complex, expensive, and uncertain carbon disposal operations on offshore leases.

What, if anything, will the Judge say about the leases that are intended to be carbon sequestration sites? How can BOEM sell OCS leases for purposes that were neither announced nor environmentally assessed? What do EarthJustice and the other plaintiffs think about the sequestration bids given that the environmental community is split on CCS?

Who is going to pay the enormous cost of sequestration on the Outer Continental Shelf – platforms, wells, pipelines, processing equipment, maintenance, monitoring, decommissioning, and more? The Federal government (i.e. taxpayers) features large in this grand scheme, and will no doubt be assuming most of the economic and performance risks. And all of these costs are for disposal purposes, not for offshore energy production of any kind.

Together with the bipartisan infrastructure bill enacted in November, which included more than $12 billion in funding for carbon capture and carbon removal technologies, the Build Back Better legislation would hand fossil fuel companies nearly every item on their carbon capture wishlist.

More than half of GoM oil production was shut-in for 13 days in September and several hundred thousand BOPD were shut-in for the rest of the month. The result was a 42% reduction in production from pre-Ida (July) levels.

All production has now been restored so the December EIA figures should give us a good read on stablized post-Ida production.

From an offshore perspective, this report is more moderate than expected. No major complaints.

The report was issued the Friday after Thanksgiving. Was there a desire to minimize attention?

The report does not include a recommendation on raising royalty rates. DOI will continue to study such actions (prudent decision).

BSEE estimates current liability for “orphaned infrastructure” at only $65 million. They must be using a very narrow definition of orphaned infrastructure.

“Financial assurance coverage should be strengthened.” (Few would argue with that statement.)

“BSEE and BOEM will carefully consider comments on the 2020 proposed financial assurance rule.” (Deja vu? Expect a long, slow process.)

BOEM will establish a “fitness to operate standard.” Comments: (1) This is an old concept that has proven to be difficult to execute. Hold companies accountable, make them demonstrate financial assurance, and don’t pander to bad actors (see the case of Hogan and Houchin) (2) Why is BOEM establishing this standard and not BSEE, the safety bureau? (The division of responsibilities between BOEM and BSEE has created serious overlap, inefficiency, and confusion and needs to be addressed.)

“BOEM should consider advancing alternatives to the practice of area-wide leasing.” Tract selection makes sense in frontier areas with little operational history. It would have been perfect for the Mid- or South Atlantic or the EGoM, all of which were cynically removed from future leasing consideration by the previous President just before the 2020 election. The Central and Western Gulf of Mexico is too mature for a return to tract selection; employing that approach after 40 years of area-wide leasing is likely to generate less revenue and production.

The text below, excerpted from the Infrastructure Bill (signed 2 days before Sale 257), requires the Federal government to provide funding for commercial CCS projects. $2.5 billion is appropriated. Given these incentives, how does BOEM possibly issue leases for CCS purposes when there was no public notice (as required by 30 CFR § 556.308) that CCS bids would be accepted at the oil and gas lease sale?

SEC. 40305.

e) Large-scale Carbon Storage Commercialization Program.--

``(1) In general.--The Secretary shall establish a commercialization program under which the Secretary shall provide funding for the development of new or expanded commercial large-scale carbon sequestration projects and associated carbon dioxide transport infrastructure, including funding for the feasibility,site characterization, permitting, and construction stages of project development.

(h) Authorization of Appropriations.--There is authorized to be appropriated to the Secretary to carry out this section $2,500,000,000 for the period of fiscal years 2022 through 2026.

Were it not for the surprising CCS bidding, which was accomplished without public notice, last week’s Gulf of Mexico sale would have been pretty ordinary – $177 million on 214 tracts.

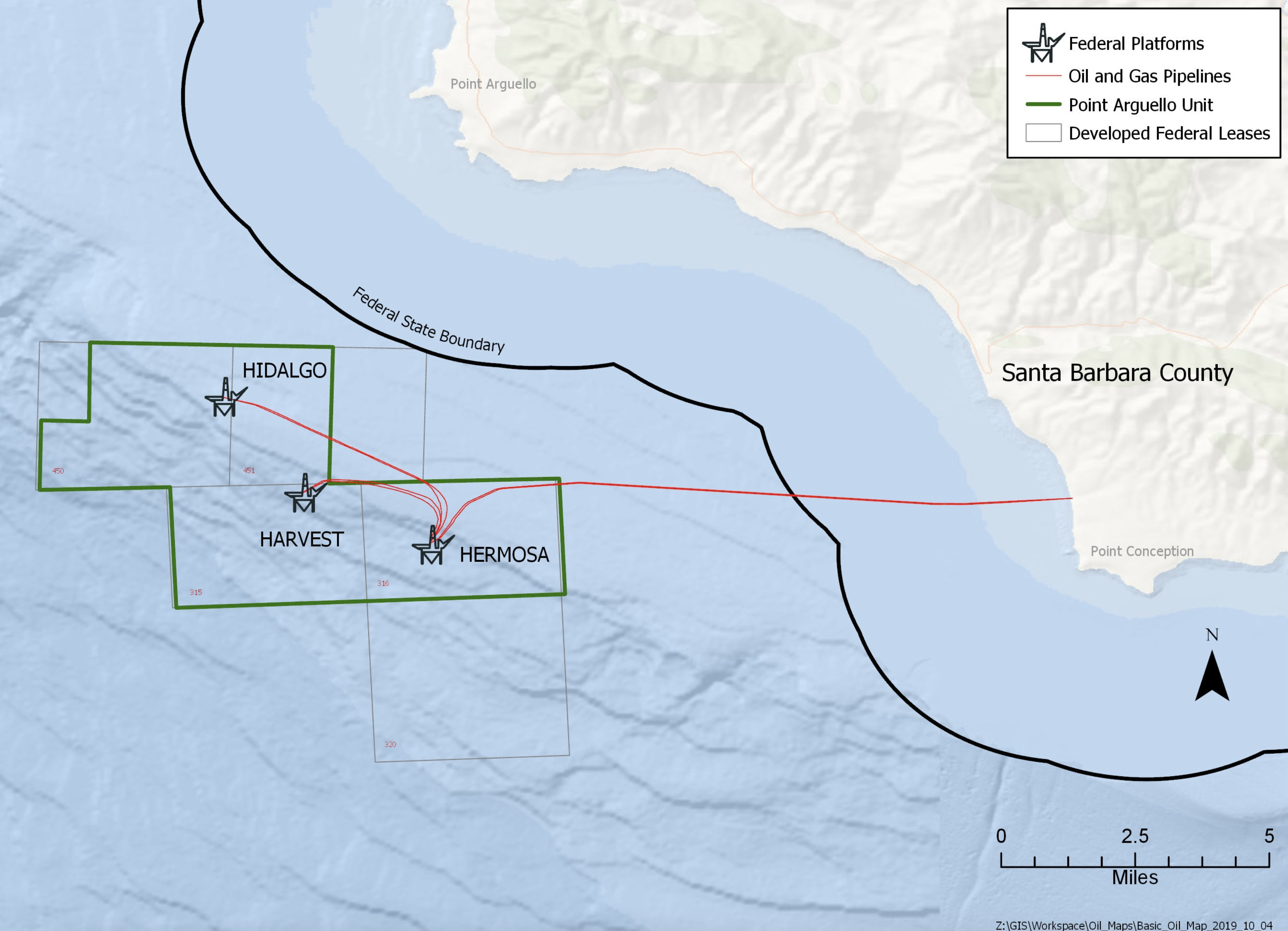

A 1981 lease sale offshore California was quite another matter. That sale (no. 53) set records that will never be surpassed. A single lease (OCS-P 0450) encompassing a little more than 5000 acres was sold to Chevron and Phillips for an astounding $333 million. This equates to$1.013 billion in 2021 dollars. That single bid (in 1981 dollars) exceeds the total high bids for any Gulf of Mexico sale since 2015.

High bids for Sale 53 totaled $2.3 billion ($7.0 billion in 2021 dollars!) for only 81 tracts. A GoM sale in 2008 received $3.7 billion in high bids, but that was for 603 tracts.

Unfortunately, production from lease 0450 never met expectations. Platform Hidalgo (0450) and the other two Pt. Arguello field platforms (Harvest and Hermosa) are no longer producing and are in the process of being decommissioned. An interesting criminal case involving Platform Harvest, then operated by Texaco, will be discussed at a later date.

One sale was for oil and gas leases. That sale was carefully planned and publicly announced in accordance with established BOEM regulations and procedures. Proposed and final notices of sale were published for public review. The final notice was published in the Federal Register on 10/4/2021. 32 companies participated in the sale.

The second sale was for CCS purposes. That sale was unannounced and had only one participant. That sale was facilitated by a provision in the Infrastructure bill that was signed just 2 days before the lease sale. There was no public notice.

(b) Leases, Easements, or Rights-of-way for Energy and Related Purposes.--Section 8(p)(1) of the Outer Continental Shelf Lands Act (43 U.S.C. 1337(p)(1)) is amended--

(1) in subparagraph (C), by striking ``or'' after the semicolon;

(2) in subparagraph (D), by striking the period at the end and inserting ``; or''; and

(3) by adding at the end the following:

``(E) provide for, support, or are directly related to the injection of a carbon dioxide stream to sub-seabed geologic formations for the purpose of long-term carbon sequestration.''.

(c) Clarification.--A carbon dioxide stream injected for the purpose of carbon sequestration under subparagraph (E) of section 8(p)(1) of the Outer Continental Shelf Lands Act (43 U.S.C. 1337(p)(1)) shall not be considered to be material (as defined in section 3 of the Marine Protection, Research, and Sanctuaries Act of 1972 (33 U.S.C. 1402)) for purposes of that Act (33 U.S.C. 1401 et seq.).(d) Regulations.--Not later than 1 year after the date of enactment of this Act, the Secretary of the Interior shall promulgate regulations to carry out the amendments made by this section.

This will be an interesting challenge for the DOI folks (BSEE/BOEM?) charged with writing the regulation given the jurisdictional issues related to capturing onshore CO2 and transporting it to the OCS. Also, when was this provision added to the infrastructure bill and did its apparent obscurity and delayed enactment give certain parties some type of competitive advantage at the sale?