Germany has a very strong Green lobby that has now become part of the ruling coalition. Despite an anti-fossil fuel discourse, the Greens have now apparently accepted the necessity of at least one fossil fuel, perhaps not least because Germany has plans to shut down all of its nuclear power plants by the end of this year.

Declines in drilling activity and discoveries suggest that higher real oil prices are on the horizon. We may be fortunate enough to escape significant price hikes and supply disruptions over the next couple of years, but they are coming.

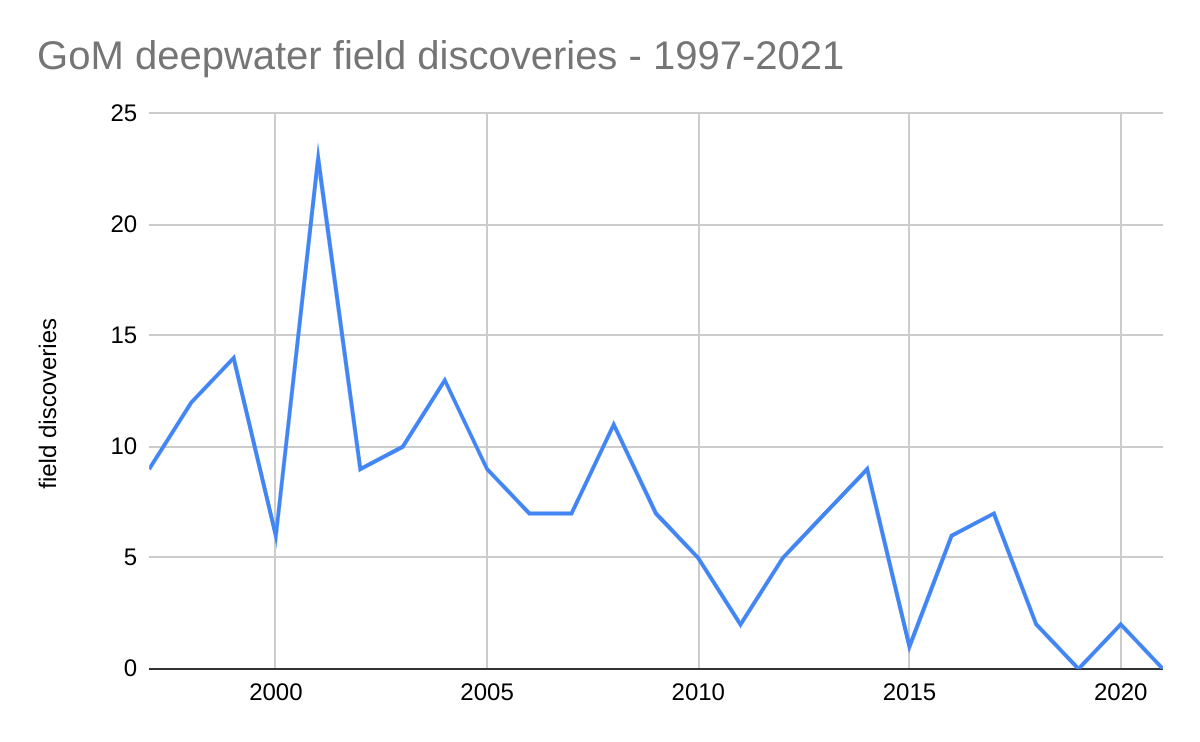

US offshore trends are even more troubling. Per BOEM’s database, no deepwater fields were discovered in 2021 and there were only 2 discoveries in the past 3 years (see chart below). HartEnergy reports 5 announced discoveries in 2021, none of which has been determined by BOEM to be commercially producible. Regardless of the status of those 2021 determinations, recent discoveries have not been sufficient to reach and sustain GoM production volumes at the 2019 peak (August) of 2.044 million BOPD. 2019 was the first year since 1982 without a confirmed deepwater discovery and the trend (below) is not encouraging. Schlumberger data through 2016 indicated GoM depletion rates greater than 20%, and the subsequent low discovery rates do not bode well for future production trends.

from BOEM data

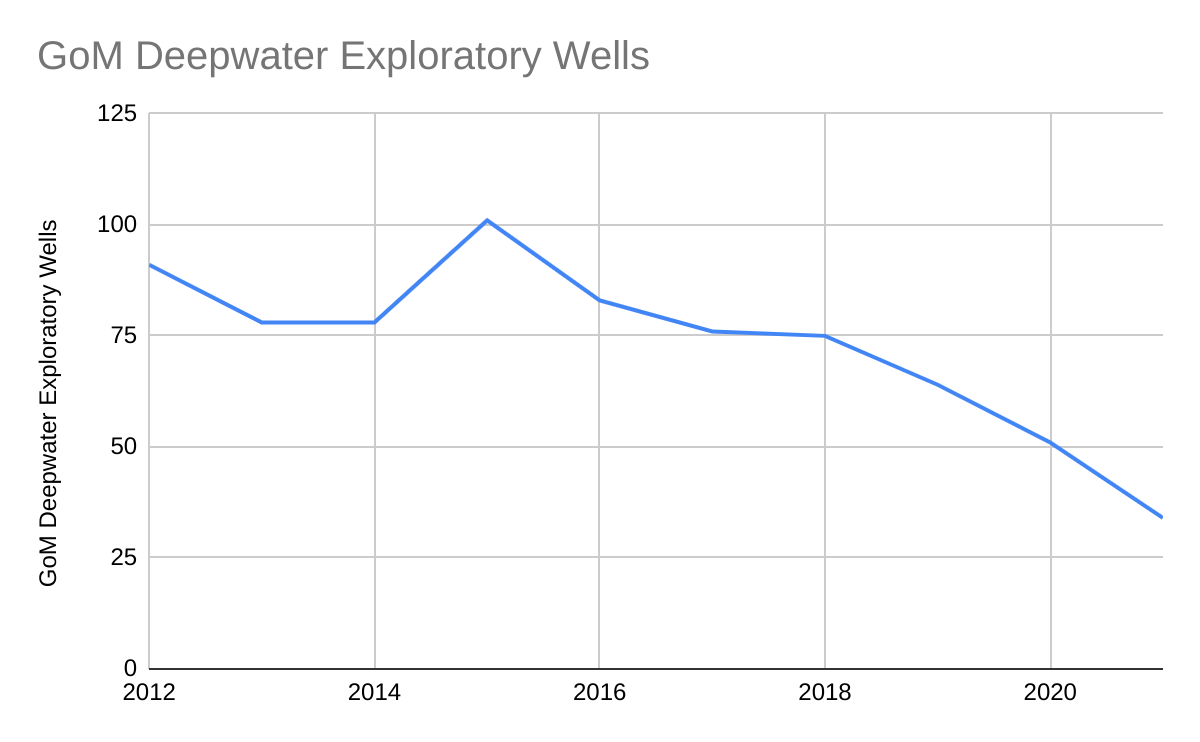

You can’t make discoveries without drilling and only 9 companies drilled deepwater GoM exploratory wells in 2021 (34 wells total). With the Pacific in decommissioning mode, the Atlantic and Eastern GoM off-limits, limited options offshore Alaska, and the decline of the GoM shelf, the deepwater GoM is the only important US offshore production option. The exploration numbers below are therefore concerning.

The shale revolution made the US a net oil exporter, but skepticism about shale production forecasts suggests the need for other supply sources. Given the shale uncertainty and the unrealistic expectations regarding the energy transition, greater US dependence on imported oil is on the horizon. This bodes well for OPEC, but not so well for US and international consumers.

Meanwhile, the US Dept. of Energy shows no evidence of concern about oil and gas production. Although oil and gas account for about 70% of our energy consumption, there has been no mention of either on the DOE homepage for months. DOE does express a strong interest in “energy justice.” Perhaps they can explain how increased imports and higher energy prices benefit the poor. They should also explain how oil imports are environmentally and economically superior to domestic oil and gas production, when the reality is exactly the opposite.

DOE provided nearly $684 million to eight coal projects, resulting in one operational facility. Three projects were withdrawn—two prior to receiving funding—and one was built and entered operations, but halted operations in 2020 due to changing economic conditions. DOE terminated funding agreements with the other four projects prior to construction.

DOE provided approximately $438 million to three projects designed to capture and store carbon from industrial facilities, two of which were constructed and entered operations. The third project was withdrawn when the facility onto which the project was to be incorporated was canceled.

So DOE’s actual success ratio was 0.182 (2 for 11) – not very compelling.

With regard to proposals for offshore carbon sequestration, who will be liable for future cost overruns, operating losses, infrastructure failures including pipeline and well leaks, and decommissioning costs? Who ensures that there will never be any leakage from CO2 disposal reservoirs? Does all of this fall on the Federal government?

Corporations that want to engage in carbon sequestration for commercial or other purposes should fund the projects with their own revenues or fees charged to the companies whose emissions they are collecting. The Outer Continental Shelf is publicly owned and those wishing to dispose of substances should pay a usage fee, be responsible for all costs, and be liable for pollution and damages.

An old offshore platform in the U.S. Gulf of Mexico is set to be converted into a working fish farm, creating a blueprint for future aquaculture re-use projects and providing repurposing options for old oil and gas assets.

Congratulations to the Gulf Offshore Research Institute (GORI) and Innovasea on their plans to transform an offshore Texas gas platform into a working fish farm.

For the complete list of alternative uses for offshore oil and gas platforms, see our Rigs-to-Reefs+++ page.

At the behest of Congress, coastal areas and beaches are now designated as Unusually Sensitive Areas (USAs). Given that any offshore liquids pipeline has the potential to affect coastal waters or beaches, the rule would seem to require that all such pipelines be included in Integrity Management Programs, which are mandatory for pipelines that could affect USAs. (The IMP requirements would almost certainly apply to all DOT regulated offshore pipelines. Their applicability to DOI/producer pipelines is less certain. Of course, very little is clear and consistent in US offshore pipeline regulation.)

As one would expect, the recent Huntington Beach pipeline spill is among the incidents cited in the justification for this regulation. More surprisingly, the Santa Barbara well blowout was also cited. This incident occurred 53 years ago, was the result of a reckless drilling program, and had nothing to do with production operations or pipelines.

As noted in a recent BOE post, the regulatory regime for offshore pipelines is badly in need of overhaul. DOT and DOI, with inconsistent jurisdictional boundaries, regulations, and approaches, have primary responsibility and multiple regulatory entities have roles.

Lastly, PHMSA seems to have inadvertently posted a highlighted copy of the new regulation. Nothing at all scandalous (looks like someone was highlighting potential talking points), but possibly amusing to other regulation nerds. 😃

Several actors have approached the ministry with a desire to be allocated two specific areas for storage of CO 2 . One area in the North Sea and one in the Barents Sea were therefore announced on 10 September in accordance with the storage regulations.

By the application deadline of 9 December, the ministry had received applications from five companies. The Ministry will process the received applications and allocate area in accordance with the storage regulations during the first half of 2022.

Contrast the situation in Norway with Exxon’s apparent attempt to acquire 94 Gulf of Mexico leases at Oil and Gas Lease Sale 257 solely for CCS purposes. BOEM’s Notice of Sale made no mention of CCS, and there had been no environmental or economic assessment of CCS activity.

And how much will the public pay for grand CCS ventures that (although interim measures) will take years to initiate, add new safety and environmental risks, and may never achieve their objectives? The public burden will no doubt include direct subsidies, tax credits, increased petrochemical prices, and the erosion of purchasing power associated with the resulting inflation pressures.

Sen. Joe Manchin III (D-W.Va.), a critical swing vote, has rejected a provision (in the “Build Back Better Bill”) that would prohibit all future drilling off the Atlantic and Pacific Coasts, as well as the eastern Gulf of Mexico, according to three people familiar with the matter

Offshore gas production (see chart below) has declined for the past 20 years and now accounts for only 4% of total US gas production, down from 20% in 2005 and 25% in the 1990s. Associated gas production (oil-well gas) has remained relatively constant owing to the strength in deepwater GoM oil production. 73% of 2020 gas production was from deepwater wells, and was mostly oil-well gas. Associated gas production surpassed nonassociated gas production (gas-well gas) in 2016 and the latter has continued to decline.

The case for natural gas has been well documented (see the EQT letter linked below). Recent natural gas advocacy has emphasized the carbon/GHG advantages given that methane (CH4) is essentially a hydrogen transporter that emits far less CO2 than other fossil fuels when burned. However, natural gas’s other important air quality advantages – low NOx. SO2, and particulate emissions – have greater local significance from a human health standpoint. Those who have ridden a bike behind a natural gas powered bus have no doubt experienced the natural gas advantage firsthand. These buses are literally a breath of fresh air!

Other environmental advantages of offshore natural gas, particularly nonassociated gas, receive less attention but are nonetheless significant. Advantages of nonassociated offshore gas include the following:

Fewer wells required than for shale gas

No risk of fresh water contamination

Platforms provide beneficial reef effects

Minimal space preemption and land disturbance relative to onshore gas production and wind/solar operations

Low facility density and navigation risks relative to wind operations;

Lower elevation and fewer view-shed, aesthetic, and aviation issues than for wind

Minimal avian risks relative to on- and offshore wind operations

Minimal spill risk relative to oil and associated gas production

Significantly less flaring than for oil well gas. While the overall % of US offshore gas production that is flared is low (approx. 1.0 -1.5% from 2016-2020 per EIA data), the % of gas-well gas that is flared has historically been less than 0.5%.

Low natural gas prices and competition from nimble and efficient shale operations have constrained offshore gas exploration. Ultradeep (subsurface) drilling has shown promise from a gas resource perspective but has proven to be expensive and operationally challenging. Some independent producers are still acquiring gas prone shelf tracts and that needs to be encouraged. Consideration should be given to incentives such as making nonassociated gas production royalty free. That would certainly seem preferable to subsidizing complex, expensive, and uncertain carbon disposal operations on offshore leases.

In 2019, the United States emitted 970 million metric tons less than in 2005, with 525 million metric tons of that emissions reduction resulting from replacing coal with natural gas in power generation. Said another way: since 2005, in the United States, all emissions reduction efforts combined have had less impact than coal to gas switching alone.

The emissions associated with the production of natural gas are dwarfed by the emissions reduction of switching from the consumption of coal to gas.

Meanwhile, China, which produced only 3% of the world’s natural gas but the majority of the world’s coal, saw its methane emissions increase by an amount roughly equivalent to adding a second Europe to the world.