(from the BOE archives)

Vineyard Wind’s finest! Note the blade failures!

Wild Well Control!

Our North Atlantic District crew, Hyannis, Halloween 1981 <sigh>

Posted in Uncategorized, well control incidents, Offshore Wind, tagged Vineyard Wind, Nantucket, Halloween, costume awards, Wild Well Control on October 31, 2025| Leave a Comment »

(from the BOE archives)

Vineyard Wind’s finest! Note the blade failures!

Wild Well Control!

Our North Atlantic District crew, Hyannis, Halloween 1981 <sigh>

Posted in California, energy policy, Gulf of Mexico, Offshore Energy - General, tagged 5 year leasing plan, Beaufort Sea, California, Florida, leaked report, Mid Atlantic, North Atlantic, South Atlantic on October 31, 2025| Leave a Comment »

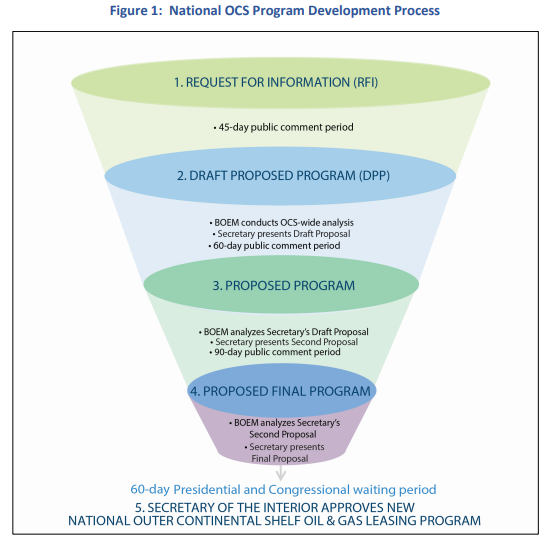

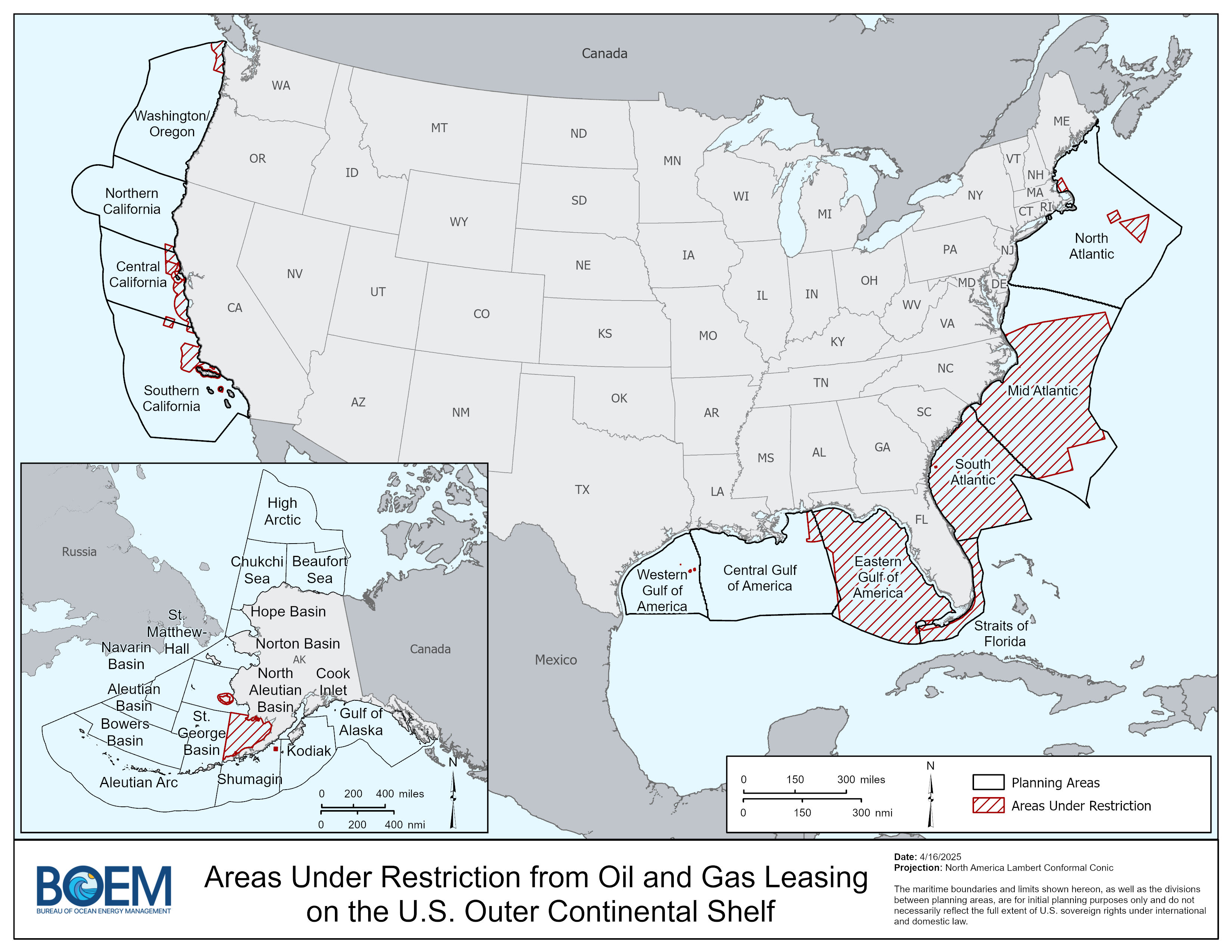

A leaked Dept. of the Interior (DOI) document will likely have little in common with the Draft Proposed Program (DPP, step 2 above). The DPP decisions will be made by the President, not by DOI staffers or managers.

According to media reports, the leaked document includes lease sales offshore New England, the Carolina’s and California. Unless the President revokes his own 2020 withdrawals, the Carolina’s are off-limits until 2032. Ditto for the Eastern Gulf within 125 miles from Florida. (See the map below.)

Including North Atlantic and offshore California in the DPP would unleash a firestorm of opposition. In the case of the North Atlantic, the acreage may not be sufficiently prospective to justify the fight.

To the extent that marine sanctuary determinations do not preclude California offshore leasing, the litigation and legislative battles probably would. In the unlikely event that a sale could be held, who would bid? Who wants to be the next Sable?

The Beaufort Sea is the most likely frontier area to be included in the DPP given plans to open ANWR, operational history, resource potential, and State support.

Assuming the South Atlantic withdrawal could be partially lifted, a small, targeted lease sale would be of great interest to petroleum geologists and could have significant economic and national security implications. The late Paul Post, the foremost expert on the petroleum geology of the US Atlantic, saw great potential in the paleo deep- and ultra-deepwater areas. He advocated exploration concepts proven successful in analogous West African and South American settings where massive discoveries have been made. Samuel Epstein, another prominent petroleum geologist, also believes the deepwater Atlantic has great resource potential.

Finally, the extent of the Florida buffer needs to be considered given the high resource potential of the Eastern Gulf. Be it 75, 100, or 125 miles, leasing beyond that buffer should be a priority.

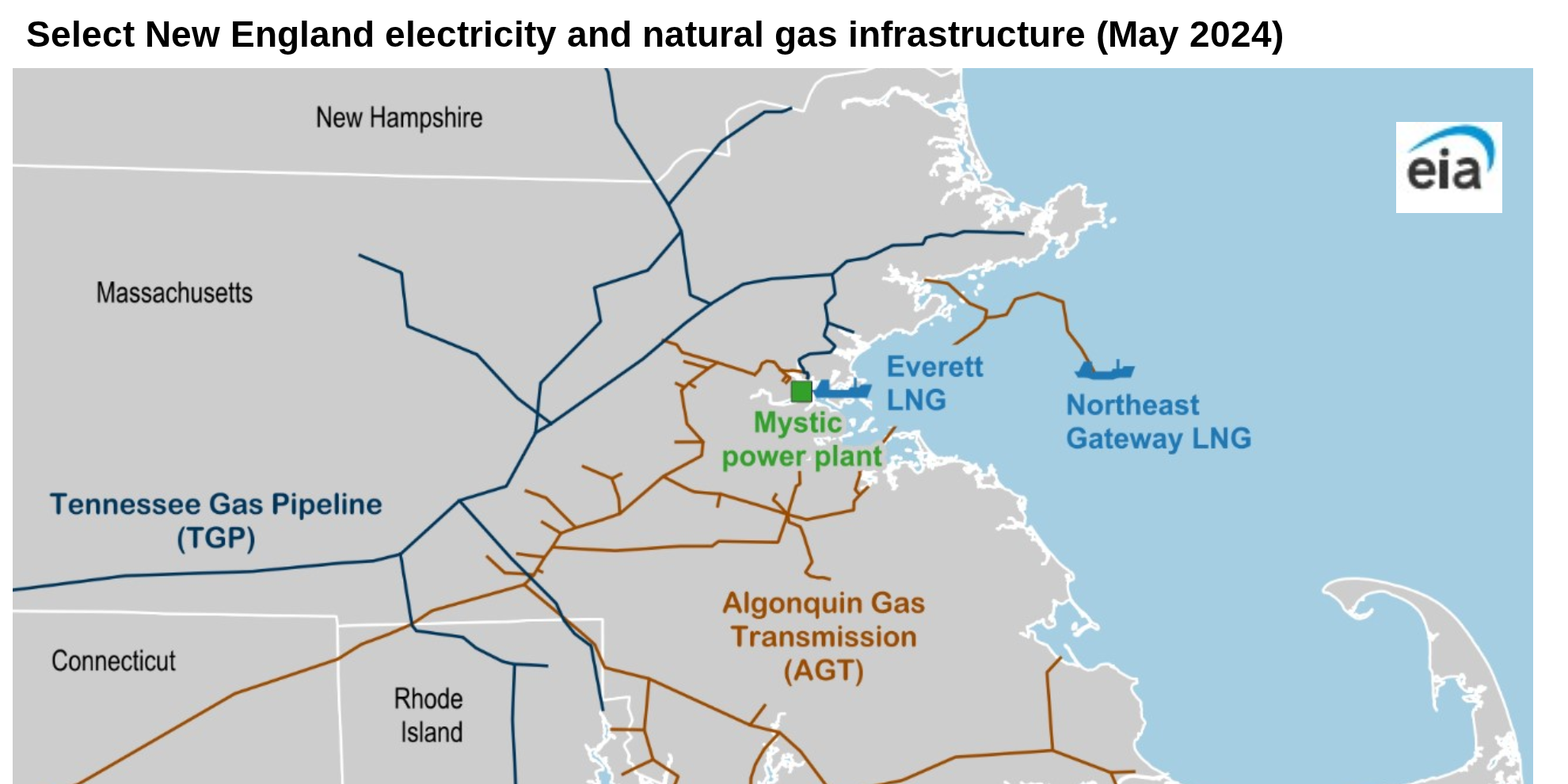

Posted in energy policy, natural gas, tagged electric prices, Everett LNG, Excellerate, Iraq, LNG imports, Marcellus Shale, Massachusetts, natural gas production on October 30, 2025| Leave a Comment »

Both are (or in the case of Iraq will soon be) LNG importers.

Why would a major oil and gas producer like Iraq be dependent on LNG imports?

And the Commonwealth of Massachusetts? Why would a state in the world’s no.1 gas producing country and not far removed from the massive Marcellus Shale reserves be importing LNG?

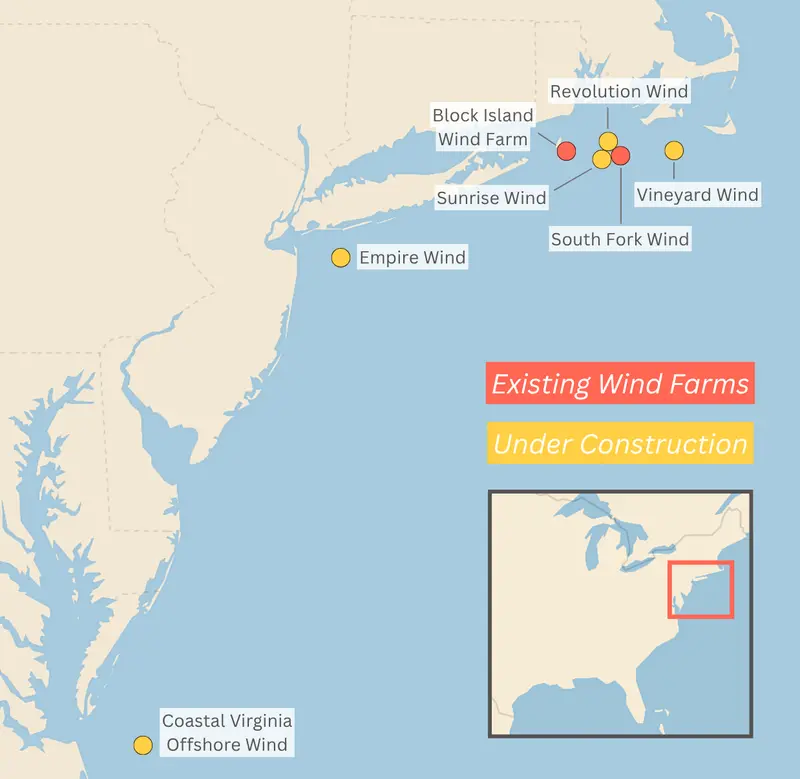

Posted in energy policy, Offshore Wind, Regulation, tagged energy policy, US offshore wind update, whiplash for wind industry on October 28, 2025| Leave a Comment »

US offshore wind policy went from this (12/11/2023):

US offshore wind update:

The long list of US offshore wind projects has diminished:

Posted in Offshore Energy - General, California, Regulation, tagged California, Exxon, Fire Marshal, pipeline inspection, regulatory fragmentation, Sable Offshore, Santa Ynez Unit on October 27, 2025| Leave a Comment »

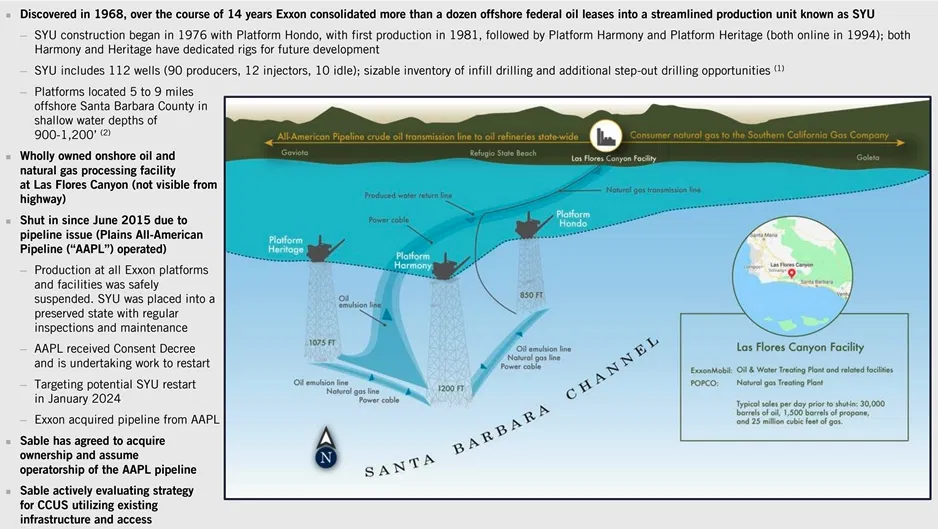

John Smith shared the attached Santa Ynez Unit regulatory update for the 8 state agencies that have oversight roles (see regulatory fragmentation).

John notes that Exxon’s March 26 contractual deadline for Sable to have the SYU up and running is fast approaching. What will Exxon do in the likely event that Sable fails to meet that deadline? Does Exxon want to re-enter the SYU legal and regulatory quagmire?

The SYU’s 500+ million barrels of oil, 3 deepwater platforms, and onshore processing facilities are an enormous prize, but is that prize attainable?

Meanwhile, the latest skirmish between Sable and the Office of the State Fire Marshal (OFSM) pertains to metal loss anomalies and inspection tool tolerances. The dispute is summarized in the linked filing.

Sable contends that the Fire Marshal’s letter contradicts guidance from OSFM staff and provides examples. Sable goes a step further at the end of their response by calling for the FIre Marshal to coordinate better with the experts on his staff:

“We respectfully request that, given this background, you coordinate further with the expert team at OSFM and revisit the statements in your October 22nd letter.”

It’s not looking good for a quick resolution of these issues.

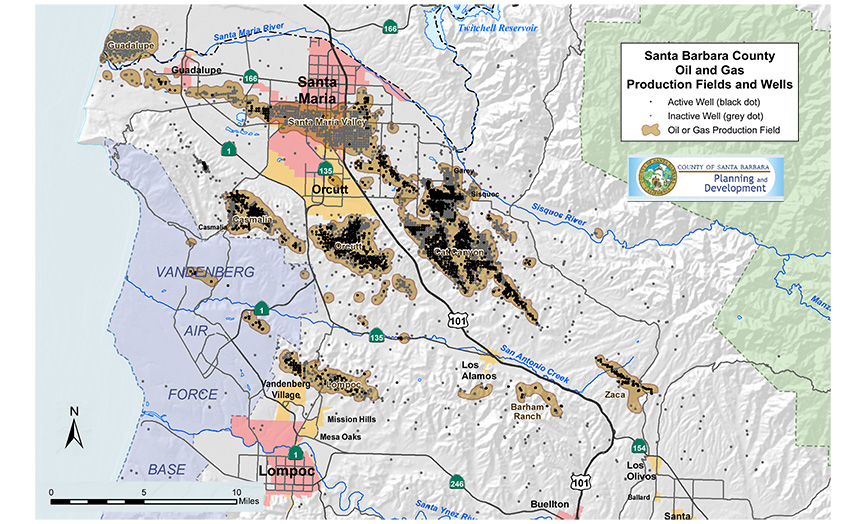

Posted in California, climate, energy policy, pipelines, Regulation, tagged 3-2 vote, Board of Supervisors, no new wells, oil and gas ordinance, Santa Barbara County on October 24, 2025| 1 Comment »

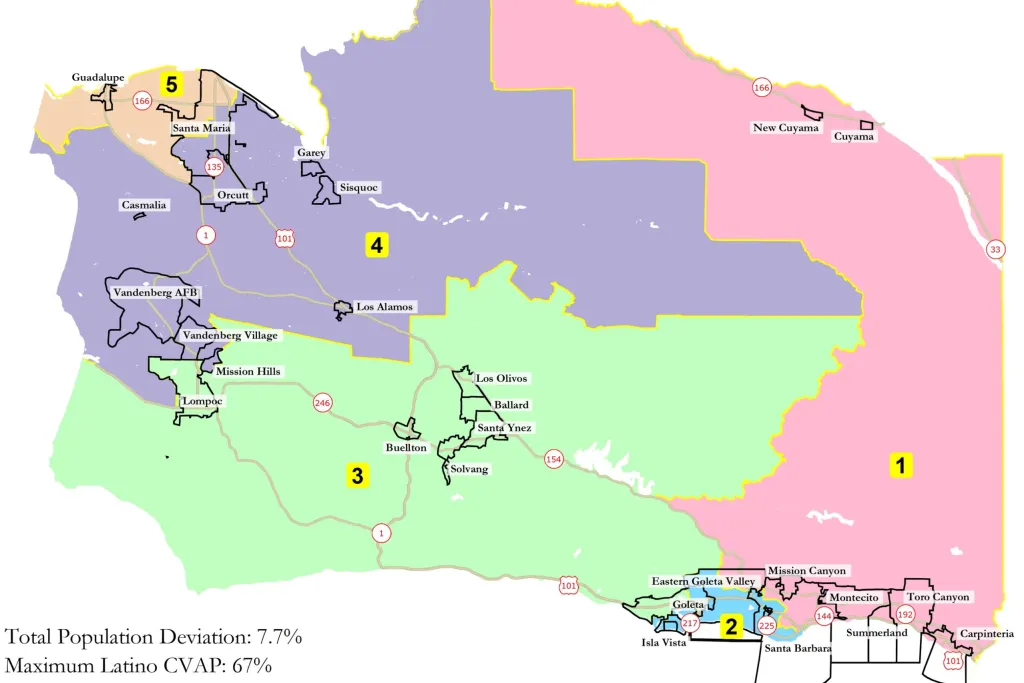

The Santa Barbara County Board of Supervisors voted 3-2 to proceed with developing a new ordinance that will ban new and operating oil and gas wells in the County.

In essence, the 3 Supervisors from South County (Districts 1-3) voted to euthanize an industry that is largely in North County (Districts 4 and 5). Those 3 supervisors, not the marketplace, are terminating a historically important industry. See the maps below.

Supervisors Laura Capps of the Second District, Joan Hartmann of the Third District and Roy Lee of the First District voted for the ordinance.

Supervisor Steve Lavagnino of the Fifth District, where I once lived, correctly noted that the North County only has two industries that allow people to support themselves well after high school: agriculture, and oil and gas.

Ah, but it’s the industry’s fault according to Supervisor Hartmann. She asserted that companies have known since the 1950s about the dangers of climate change, and could have led the way to be part of the solution. How dare they respond to market forces instead of climate ideologues!

Of course, this is the same three vote coalition that is aligned with the Coastal Commission in opposition to the restart of the Santa Ynez Unit, which would benefit the County significantly.

Finally, note that the three supervisors voting for the ordinance represent the districts with the highest income levels and lowest poverty rates. Those opposing the ordinance represent the districts that will be most affected, and have the lowest income levels and highest poverty rates. (See the table below; Information courtesy of Grok AI.)

| District | Approx. Median Household Income (2022) | Key Areas Included | Notes |

| 1 | $120,000–$140,000 | Carpinteria, Summerland, Montecito, parts of Santa Barbara | Affluent coastal communities; high home values (~$1.5M+ median) |

| 2 | $95,000–$115,000 | Santa Barbara city, Goleta, Isla Vista | Mix of urban professionals, students, and tech; university influence lowers median slightly. |

| 3 | $80,000-$95,000 | Santa Ynez Valley, Buellton, Solvang, Lompoc | Rural/agricultural with tourism; moderate incomes from wine industry and military base |

| 4 | $70,000–$85,000 | Lompoc, Vandenberg area, parts of Santa Maria | industrial and defense-related; higher poverty rates (~15–20%). |

| 5 | $60,000–$75,000 | Santa Maria, Guadalupe | Agricultural North County; majority Latino population; lowest incomes due to farm labor. |

Poverty rates: ~8–10% in Districts 1–2 vs. 18–25% in Districts 4–5

Posted in Gulf of Mexico, Offshore Energy - General, Regulation, tagged BOEM, BSEE, Federal shutdown, INCs, inspections, permitting, Warren Buffett on October 23, 2025| Leave a Comment »

Good: OCS oil and gas permitting and inspections appear not to be significantly affected by the govt shutdown to-date. 14 planning documents were approved on Oct. 21, and 37 drilling permits have been approved in Oct. (through 10/21).

152 facility inspections were conducted from 10/1 through 10/19. Natural Resources Worldwide (NRW), which is currently the operator of just one Cox legacy platform, has the dubious distinction of being the Shutdown’s Shut-in Leader. 16 Incidents of Non-Compliance (9 warnings and 7 component shut-ins) were issued to NRW during a single facility inspection in October.

Bad: This level of effort is not sustainable given limits on offsetting funds from fees, rentals, etc.

Ugly: The personnel who are performing these duties are not being paid during the shutdown. The longer the shutdown drags on, the greater the hardship on those individuals and their families. Shameful!

Warren Buffett’s proposal would stop deficit spending and address the root cause of shutdowns:

Buffett: “I could end the deficit in five minutes. You just pass a law that says that any time there’s a deficit of more than three percent of GDP, all sitting members of Congress are ineligible for re-election.“

Posted in Offshore Energy - General, California, energy policy, tagged Exxon, Sable Offshore, Santa Ynez Unit, OS&T, Chris Wright, Energy Dept., CZMA, Refugio Spill on October 22, 2025| 3 Comments »

In a post on X, Chris Wright commented:

“Only in California! Newsom is blocking oil production off California’s coast from reaching their own refineries, driving gasoline prices even higher for Californians! Now, this oil production will have to be shipped elsewhere, lowering gas prices for other areas— just not for California! This is the opposite of common sense!”

BOE was a fan of Chris Wright long before he became Energy Secretary, and I agree that the resumption of Santa Ynez Unit production is economically desirable for California and the nation. However, his comment implies that OS&T processing and tanker transport is a realistic option, and I do not believe that is the case.

John Smith and I have discussed Sable’s OS&T announcement on a number of occasions, and we don’t see a reasonable path forward for this option. In addition to the significantly higher capital and operational costs and the need to acquire and retrofit a suitable floating production, storage, and offloading vessel (FPSO), the legal and permitting challenges could be even more complex than for the pipeline option (as daunting as that may sound).

The OS&T option would require a revised development and production plan, and the associated environmental review (almost certainly an EIS). An EIS would not favor this option, and the California Coastal Commission would surely rule that the OS&T/tanker alternative was inconsistent with their CZM plan. (Keep in mind that the SYU/OS&T production in the early 1980’s was approved prior to the passage of the Coastal Zone Management Act.) The Secretary of Commerce could overrule the Commission’s consistency determination, but legal objections to the override would likely delay the project for years and have a good chance of success.

Onshore processing and pipeline transportation using existing facilities is clearly the environmentally and economically preferable option. The only reasonable path forward for Sable or Exxon is to continue to pursue the onshore pipeline approvals. Federal attention should focus on jurisdiction over that pipeline, which is inherently an interstate line because it transports OCS production, and State actions that are blocking interstate commerce.

Finally, keep in mind that the SYU would still be producing today were it not for the entirely preventable pipeline rupture and the resulting Refugio oil spill. Plains Pipeline, the party responsible for this ugly incident, is no longer the owner, but that doesn’t comfort coastal residents; nor does it absolve the companies that transported their oil through the line from all responsibility.

The Refugio spill will be discussed further in an upcoming post.

·

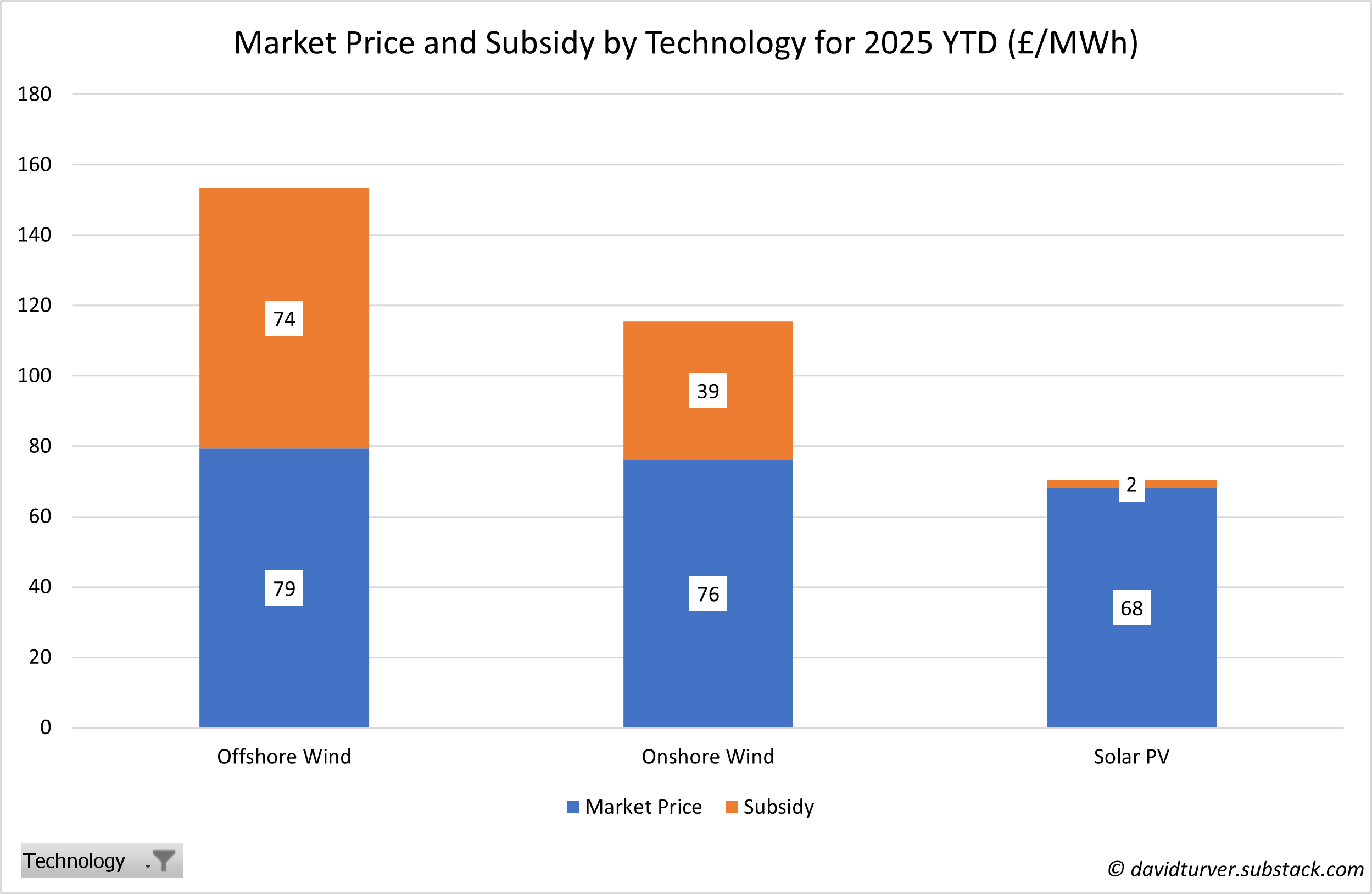

Posted in decommissioning, Offshore Wind, UK, tagged David Turner, decommissioning, financial assurance, JL Daeschler, UK wind energy, wind subsidies on October 21, 2025| 1 Comment »

JL Daeschler informs that UK offshore wind energy is 82% foreign-owned. Foreign companies are thus the primary beneficiaries of the UK’s generous renewable energy subsidies (chart below).

David Turner comments as follows in his informative piece on UK wind energy:

“We have been warning for some time that it is crazy for a developed economy to try and run its electricity generation system using technologies that are dependent on the weather. Even though there has been only a relatively modest decline in wind output this year, the operators and owners of wind farms are learning the hard way that it is very difficult to run a business that is at the mercy of the vagaries of the weather. Many of these companies are up to their eyeballs in debt. They better hope the wind blows hard this Autumn and Winter so they can collect higher subsidies, or they will be in real trouble.“

We have consistently raised concerns about decommissioning financial assurance for offshore wind facilities. Turner echoes those concerns noting that the wind industry’s “perilous finances are an even bigger reason to insist that proper funds are set aside to fund decommissioning or the long-suffering taxpayer will be on the hook for another hidden cost of renewables.“

Interesting case: Delaware litigation on approval of the Coastal Construction Permit for the Maryland Offshore Wind Project

Posted in decommissioning, energy policy, Offshore Wind, Regulation, tagged Coastal Construction Plan, court filing, decommissioning, Delaware litigation, Maryland Offshore Wind, public comment, US Wind on October 29, 2025| Leave a Comment »

The Dept. of the Interior is currently reconsidering approval of the Construction and Operations Plan for the Maryland Offshore Wind Project (US Wind).

Attached is a court filing challenging Delaware’s approval of the Coastal Construction Plan for that project. Some interesting points from the filing:

Read Full Post »