CP’s acquisition of Marathon is an endorsement of shale production, most of which is from private lands. Sadly, these historically important OCS operators no longer have an interest in the Federal offshore sector.

Trinidad and Tobago (T&T), which has hadoil drilling operations since 1857, 2 years prior to the Drake well in Pennsylvania, closed another bidding round this week. In this Shallow Water Bidding Round, they received bids on 4 of the 13 blocks that were offered.

“These bid rounds are aimed at ensuring sustainable exploration and production and maximizing our country’s hydrocarbon resources. Following the successes of the 2021 Deep Water Competitive Bidding Round and the 2022 Onshore/Near Shore Competitive Bidding Round, this Shallow Water Competitive Bidding Round was the third in a series of bid rounds conducted by the Ministry of Energy and Energy Industries.”

Regular sales are even more important in the US given the small lease blocks and thus the need to have access to nearby resources for sustained production and efficient utilization of facilities.

Below are the blocks receiving bids in the T&T sale, and the size of those blocks. US lease blocks are approximately 23 sq km.

While checking for updates on the important Orphan Basin well, I looked at Newfoundland production data and found it surprisingly encouraging:

The pioneering Hibernia field has produced more than double the original resource estimate of 520 million barrels, and is still chugging along at about 60,000 bopd.

Hebron, the current top producer, is holding strong at 100,000+ bopd.

White Rose, which was in danger of being abandoned, is poised for a renaissance with the installation of the West White Rose concrete gravity structure.

Terra Nova is once again producing at near 2019 levels after a four year hiatus. The Terra Nova story has many important technical, management, regulatory, safety, and logistical elements, and presents good case study opportunities for Newfoundland academics (Memorial University?).

With prospects for production at Bay du Nord brightening and interesting targets like the Orphan basin being explored, pessimistic forecasts for Newfoundland’s resilient offshore sector may be a bit premature.

Sec. 12(a) of OCSLA (43 U.S. Code § 1341(a)): “The President of the United States may, from time to time, withdraw from disposition any of the unleased lands of the outer Continental Shelf.”

The language “from time to time” implies that withdrawing OCS lands from oil and gas leasing consideration is a casual exercise at the whim of the President for any particular reason. That is indeed how the provision has been implemented.

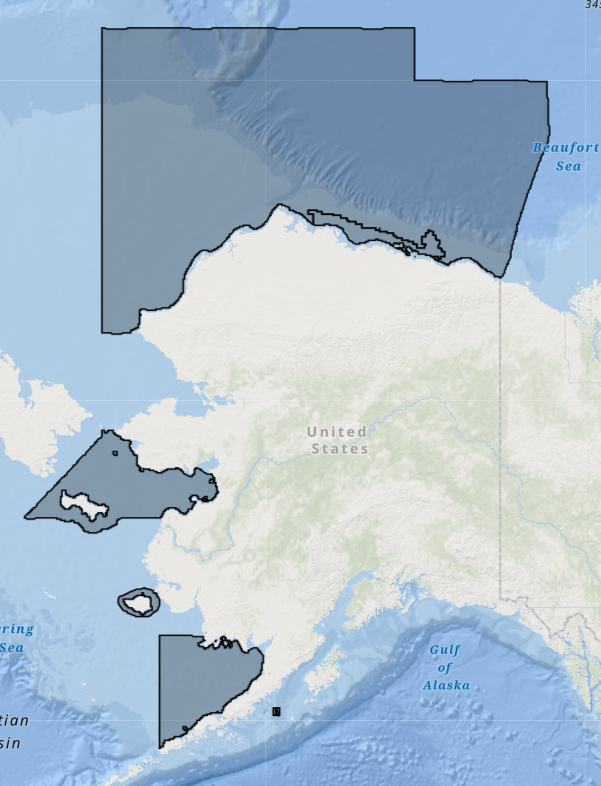

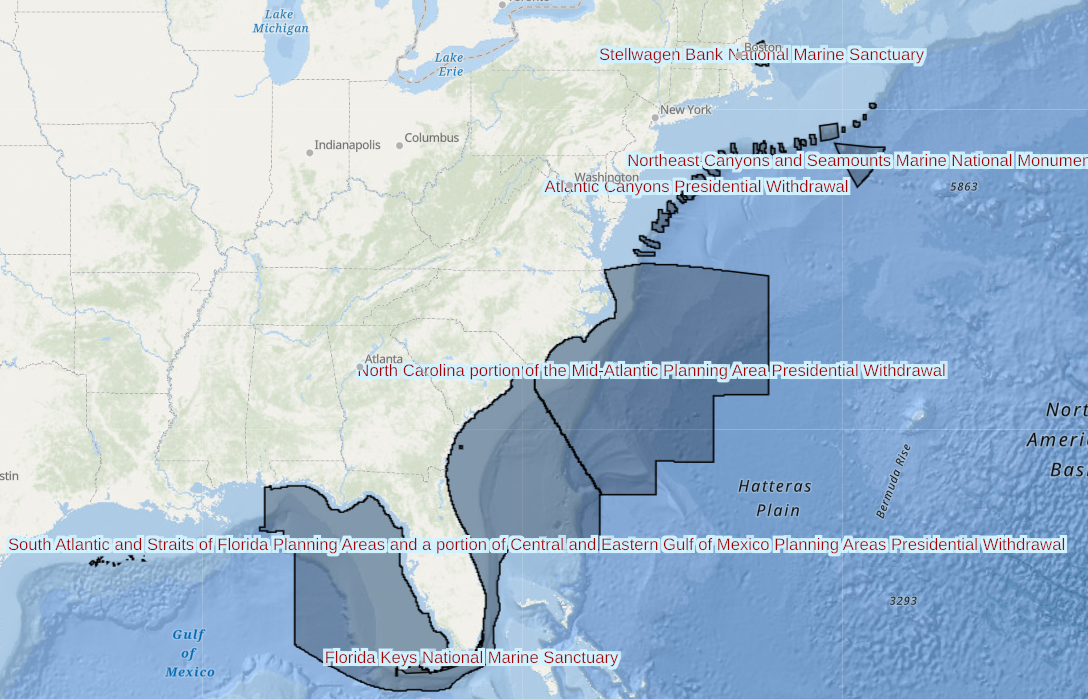

Alaska Presidential withdrawals are shaded (BOEM map)Atlantic and GoM withdrawals are shaded (BOEM map)

Over the last 8 years, Presidents Obama, Trump, and Biden have unilaterally exercised this authority without prior notice or opportunity for public comment. Their actions were timed to extend oil and gas leasing prohibitions well beyond their term in office (perhaps permanently), seek an edge in an upcoming election, or sacrifice OCS leasing in an attempt to placate opponents of another executive decision. More specifically:

In his last month in office, President Obama removed canyon areas of the Atlantic from leasing consideration “for a time period without specific expiration.”

In his last month in office, President Obama removed the Northern Aleutian planning area from leasing consideration “for a time period without specific expiration.”

Two months before the 2020 election, President Trump removed the South Atlantic planning area from leasing consideration through June 30, 2032.

Two months before the 2020 election, President Trump removed the Eastern Gulf of Mexico area from leasing consideration through June 30, 2032.

On March 13 2023, coincident with his approval of theWillow project (North Slope of Alaska), President Biden removed the remainder of the Beaufort Sea from leasing consideration “for a time period without specific expiration.”

In light of the rather cynical abuses of this authority and their potential economic and national security implications, Congress should consider repealing Sec. 12(a) of OCSLA or revising the language to limit the timing, scope, and duration of such withdrawals, and establish a process that prevents the withdraw of lands without fully considering the potential implications.

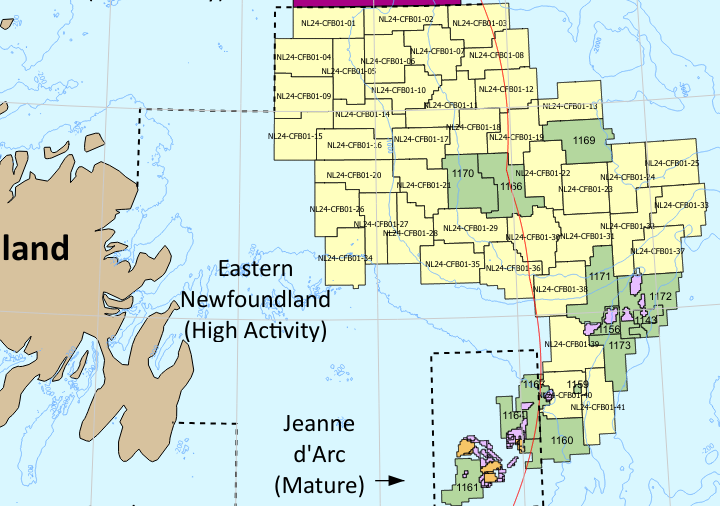

Per rig tracker data, the Stena DrillMAX has been on location at Exxon’s Orphan Basin wellsite since Sunday (19 May). The site is 317 miles (510 km) NE of St. John’s in Block 1169 (~3000 m water depth).

Per this very good resource assessment report for the Govt. of Newfoundland and Labrador, “the Orphan Basin area demonstrates a potentially prolific petroleum system with four main plays (reservoirs and associated seals) sourced by various source rocks (Upper Jurassic, Cretaceous, and Paleogene).“

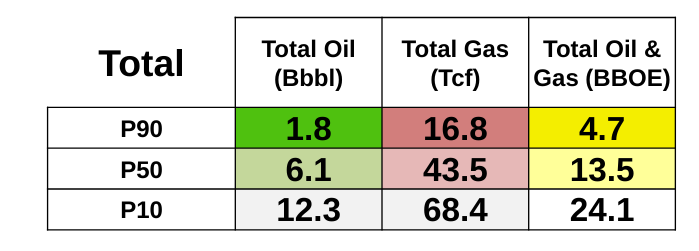

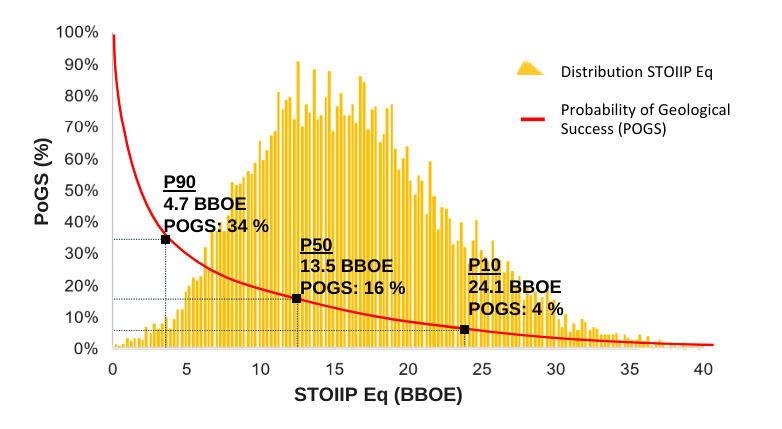

Unrisked resource estimates (theoretical pending confirmation by drilling) at the 90, 50, and 10% probability levels for the Orphan Basin blocks offered for licensing in Nov. 2022:

Taking into account the risks of the geologic model not accurately reflecting the reservoir, seal, charging, and trap components of the petroleum system, the probability of finding 13.5 billion drops to 16% (see plot below). This is still a high probability for a massive wildcat discovery.

This is why you move a state-of-the-art drillship thousands of miles to drill a single exploratory well at a remote location in the North Atlantic. The most likely outcome is negative or inconclusive findings, but the potential for such a major discovery justifies the investment.

The PGOS curve quantifies the probability of success in finding the identified volume of resources in the new Orphan Basin blocks (e.g. there is a 34% chance of finding 4.7 billion BOE and a 16% chance of finding 13.5 billion BOE).

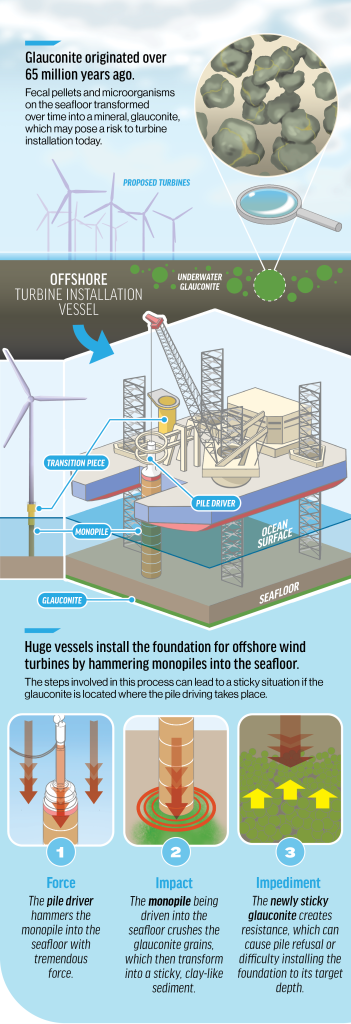

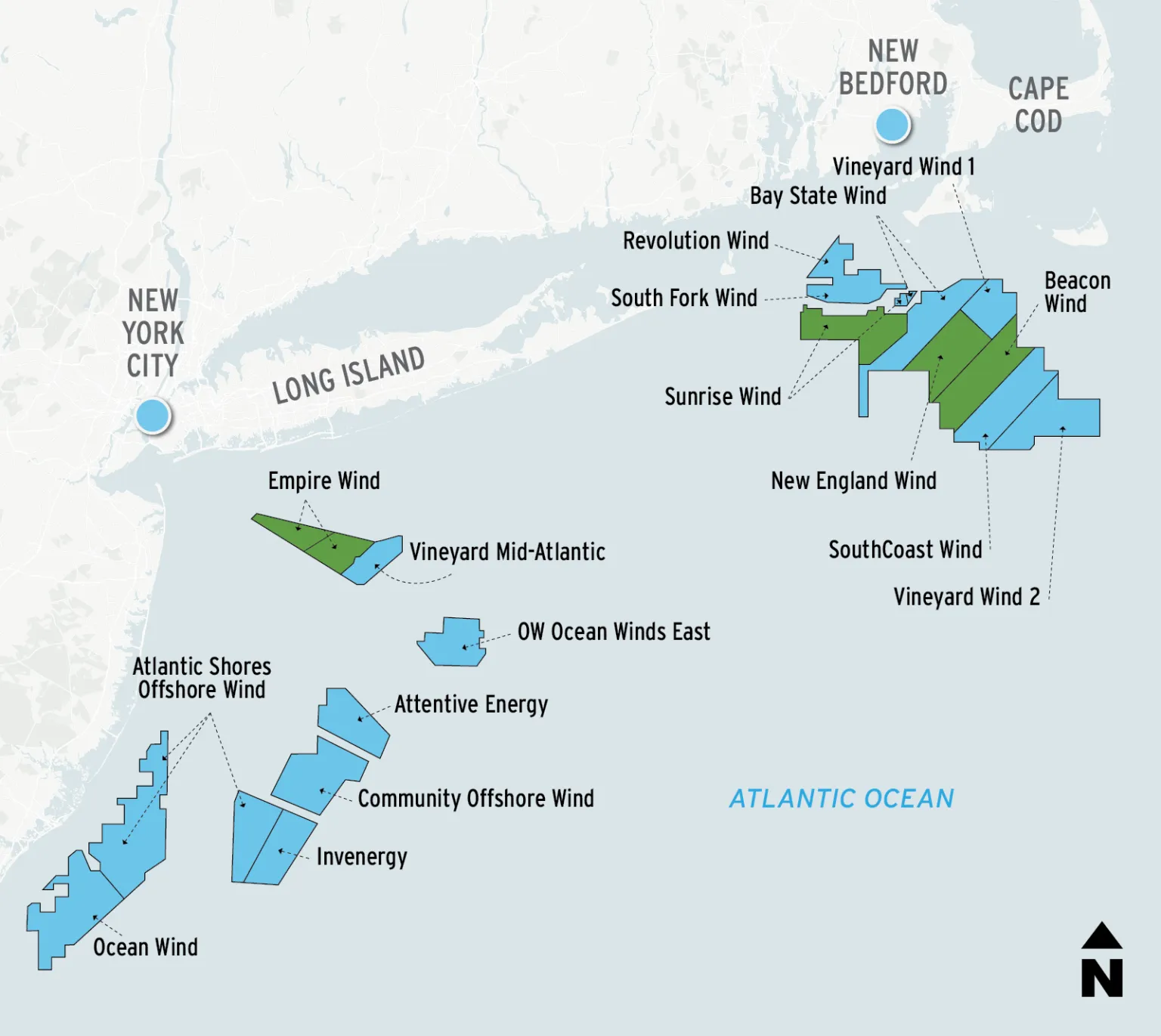

Illustration credit: Kellen Riell / The New Bedford LightGlauconite has been identified within the boundaries of lease areas marked with green. Credit: Kellen Riell / The New Bedford Light

Anastasia Lennon has published several informative articles in the New Bedford Light on the challenges posed by the presence of glauconite on North Atlantic wind leases. The above illustrations explain those challenges and identify where glauconite has been found to date. Per her latest article:

Preliminary geotechnical analysis for New England Wind, an Avangrid project, showed a risk of turbine pile foundation refusal in 50 of nearly 130 turbine locations, or about 40%, according to 2023 records obtained through a Freedom of Information Act request.

The mineral’s behavior poses a “significant risk” to offshore wind development, said BOEM, the federal regulator of offshore wind, in a paper last year.

A Bell 212 helicopter is in the news following the crash that killed Iran’s President and Foreign Minister. Given the difficult weather conditions and mountainous terrain, the crash was most likely an accident.

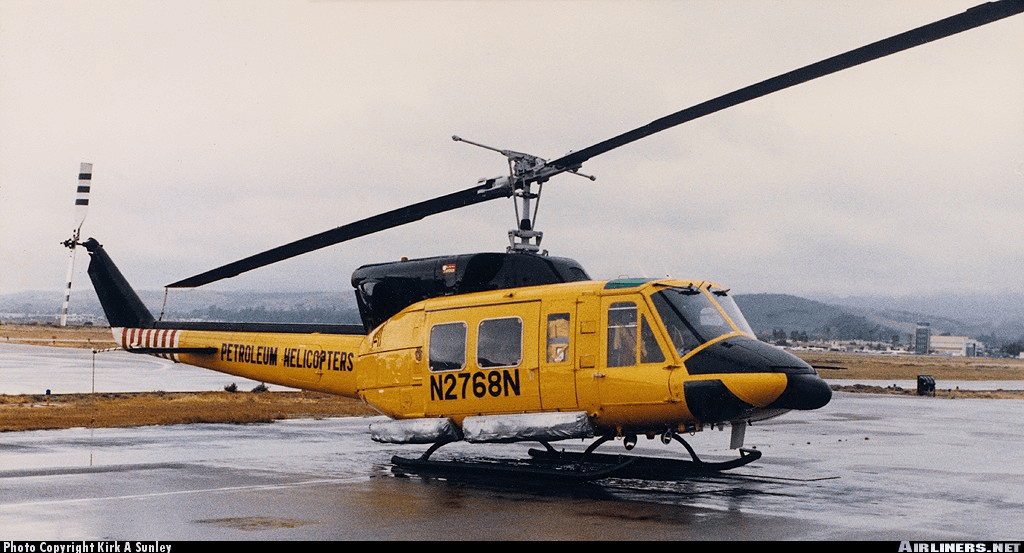

As noted in this vintage newsletter (p. 8), we flew to Georges Bank drilling rigs in the early 1980’s in a Bell 212 contract helicopter, owned and operated by Petroleum Helicopters Inc (PHI).

The Bell 212 was chosen by the USGS aviation expert because of its range, reliability, and IFR capabilities that enabled flying in limited visibility. Because of difficult fog conditions on Georges Bank, drilling rigs were sometimes not visible until we were descending to land.

For the most part, the offshore industry has replaced Bell 212 helicopters with newer models, but the 212 was in use for many years and had an excellent performance record.

PHI Bell 212 prepares to land at a platform in the Gulf of Mexico, 1974, Vertiflite.

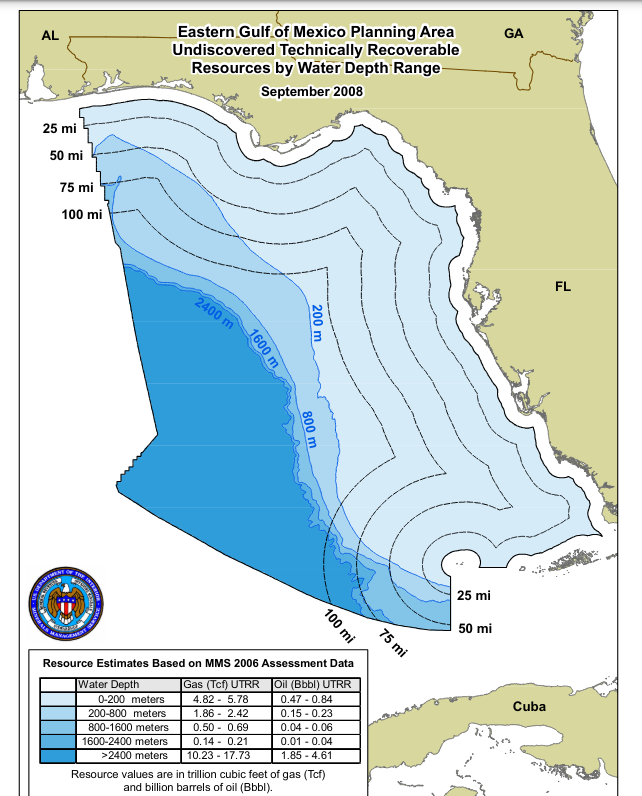

Florida HB 1645 (attached) was signed by Gov. DeSantis on 5/15/2024. The bill boosts natural gas, prohibits offshore wind turbines, and deletes references to climate change and greenhouse gases in state law. Given the State’s support for traditional energy sources, is it time to renew the dialogue about exploration and production in the Eastern Gulf of Mexico (EGOM)?

HB 1645 prohibits offshore and coastal wind development (p. 30), acknowledges that natural gas is critical for power resiliency, prohibits zoning regulations that restrict gas storage facilities and gas appliances (p.8), and relaxes permitting requirements for pipelines <100 miles long.

Given Florida’s energy preferences as expressed in this legislation, the State could assist regional energy planners by better defining its position on oil and gas leasing in the EGOM. What limits, in terms of lease numbers and minimum distances from shore, would best improve Florida’s energy supply options while further minimizing environmental risks?

As illustrated on the map below, the petroleum geology of the EGOM and Florida’s preferences are likely aligned in that the best prospects for oil and gas production are in deep water and more than 100 miles from the State’s coast.Does Florida support a 100 mile buffer?

The 4/20/2010 Macondo blowout was a tragic failure that has been, and will continue to be, discussed at length on this blog. We should also acknowledge that prior to Macondo 25,000 wells were drilled on the US OCS over a 25 year period without a single well control fatality, an offshore safety record that was unprecedented in the U.S. and internationally. We should also applaud recent advances in well integrity and control, including the addition of capping stack capabilities that further reduce the risk of a sustained well blowout.

Florida’s independent thinking on energy policy is commendable. That independence is contingent on importing petroleum products and natural gas from elsewhere in the Gulf region. Securing that supply over the intermediate and longer term should be a priority for Florida. In that regard, EGOM production is an important consideration.