In JPMorgan’s view, the stage is set for a potential decline of as much as 50% in oil prices through the end of 2027, taking Brent crude down to the low $30s per barrel range from its current level of around $63.50.

Will bearish forecasts by JPMorgan and others temper bidding at the highly anticipated, and long awaited, Gulf lease sale to be held on 12/10/2025? Probably not for these reasons:

Given the longer term nature of deepwater development, production will not begin for years following lease issuance. Note that anticipated first production for 3 new high-pressure deepwater projects, Kaskida, Sparta, and Tiber, will be 23, 16, and 21 years after the field discovery dates.

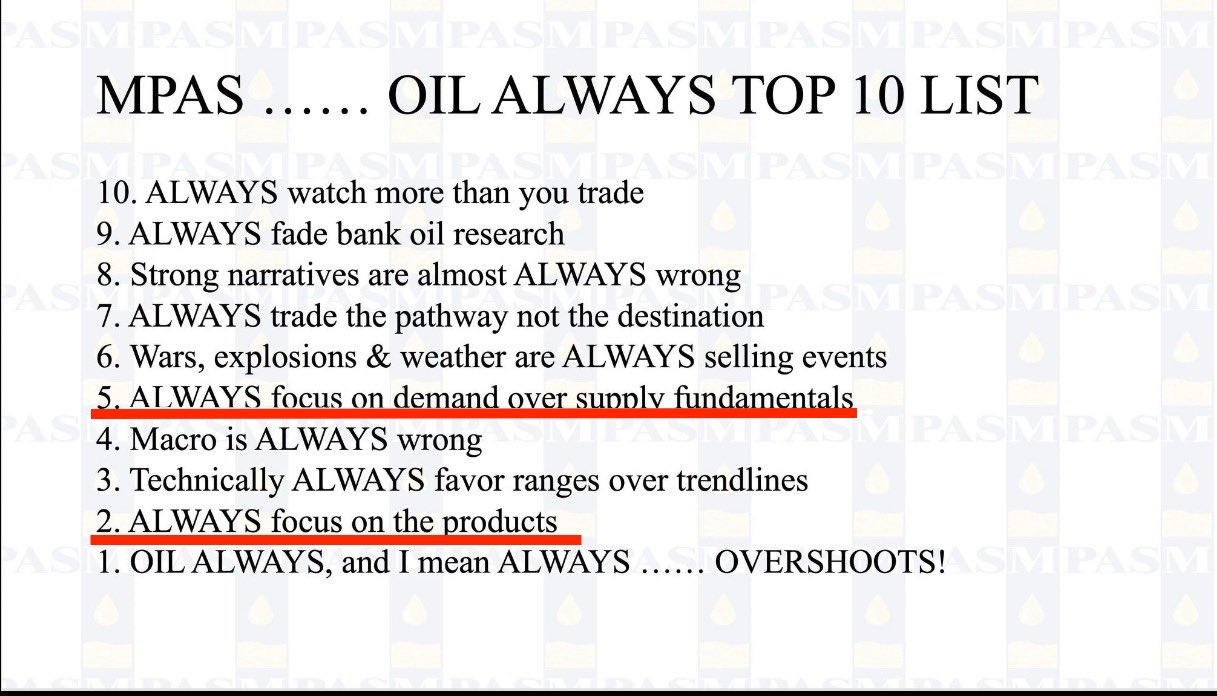

To the extent that price forecasts are reliable at all (see no. 9 in the image below), the degree of uncertainty for longer term forecasts is particularly high.

The sale has to live up to its name Big Beautiful Gulf 1 (BBG1). 😉

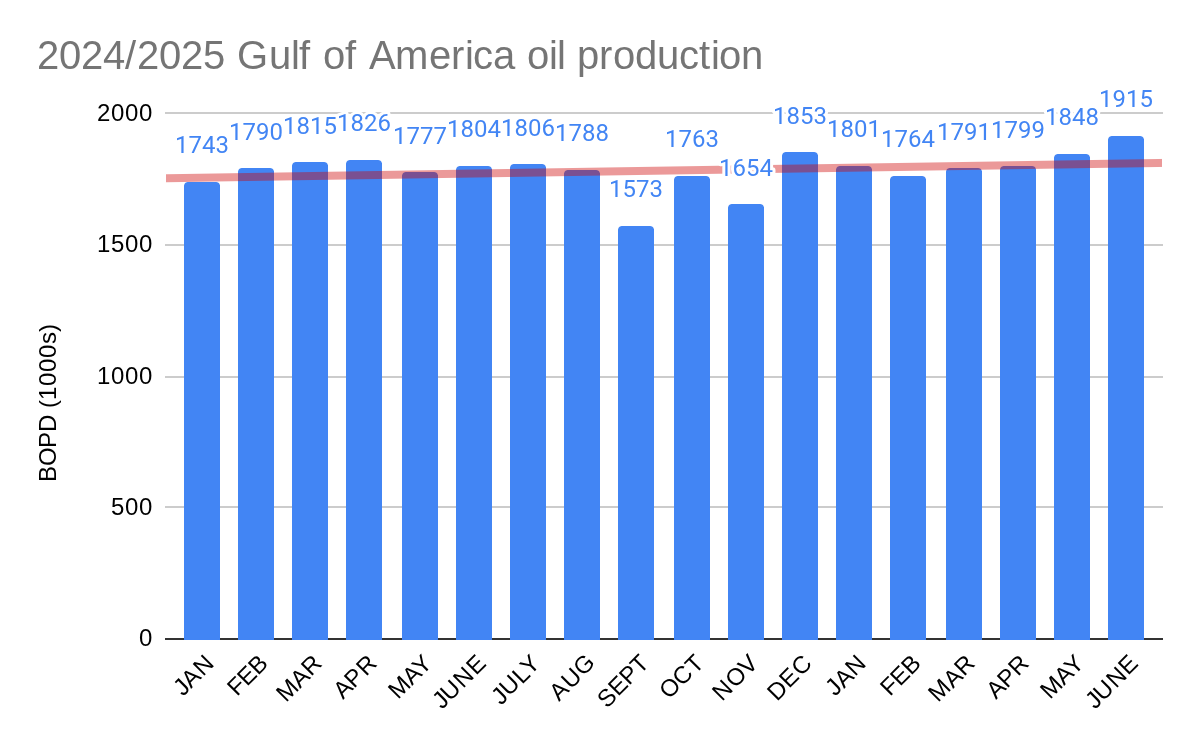

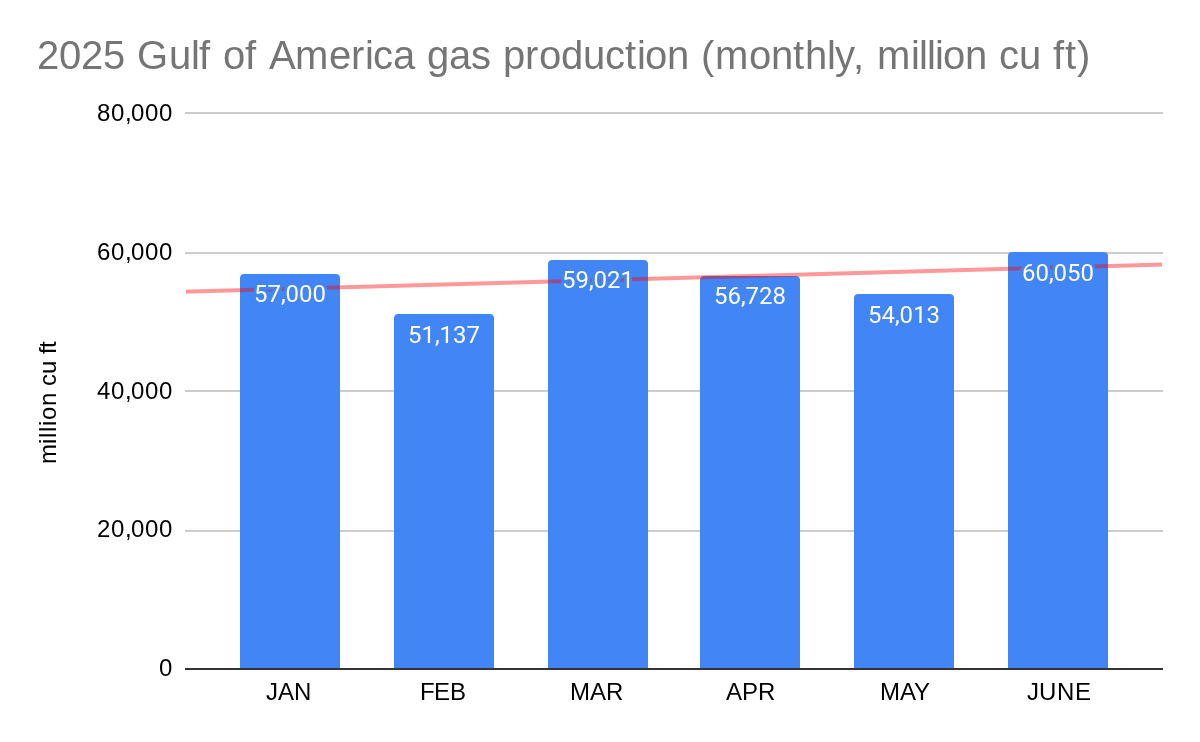

The average oil production rate for the Gulf OCS was 1.915 million bopd in June, the highest rate since Oct. 2023 and thus the highest in the history of the Gulf of America 😉.

Natural gas production, which is now primarily from oil wells (i.e. associated gas) and is thus more closely linked to oil production rates, increased by >10% in June to over 60 bcf. As was the case for oil, gas production was the highest since Oct. 2023.

It is now peak hurricane season, so the eyes of production forecasters are focused on the tropics. Few need to be reminded about what happened 20 years ago when Hurricanes Katrina and Rita roared through the Gulf, preceded by Hurricane Ivan “The Terrible” one year earlier. Those 3 hurricanes triggered major improvements in hurricane preparedness, particularly with regard to stationkeeping capabilities.

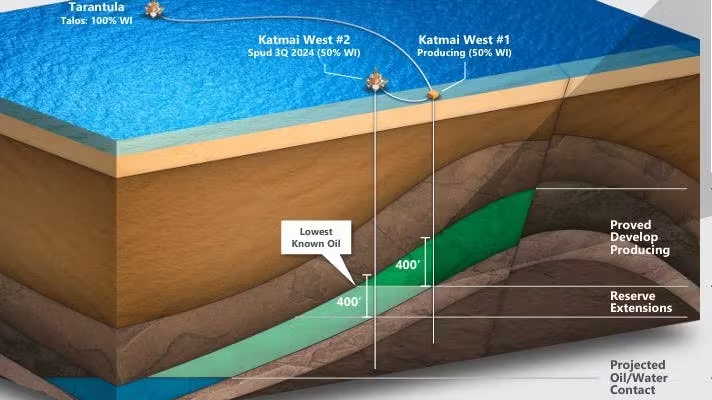

Talos announced successful drilling results at the Daenerys prospect (Katmai West #2) in the Gulf of America (Walker Ridge blocks 106, 107, 150, and 151).

Daenerys is a good example of the evolution of deepwater project ownership, which was once exclusively the domain of major international oil companies. Over the past 20 years, participation by independents increased gradually, followed by smaller independents and informed investment companies.

Impressively, the Daenerys partnership (table below) includes a tribe that has the same % ownership as a super-major, and a highly efficient investment company owned by a single person.

Talos (operator)

large US independent

27.0% share

Shell

international supermajor

22.5%

Red Willow

private company owned by the Southern Ute Tribe

22.5%

Houston Energy

private independent focused on deepwater energy resources

Trinidad’s Prime Minister Kamla Persad Bissesar: “Trinidad will not wait for the end of any energy era,” she said. “Our principle is simple: investment goes where it is welcomed and stays where it is well treated.”

The PM of a country with an oil production history that predates the Drake well in Pennsylvania leaves no doubt about her support for deepwater development. Her candid and clear messaging is most refreshing.

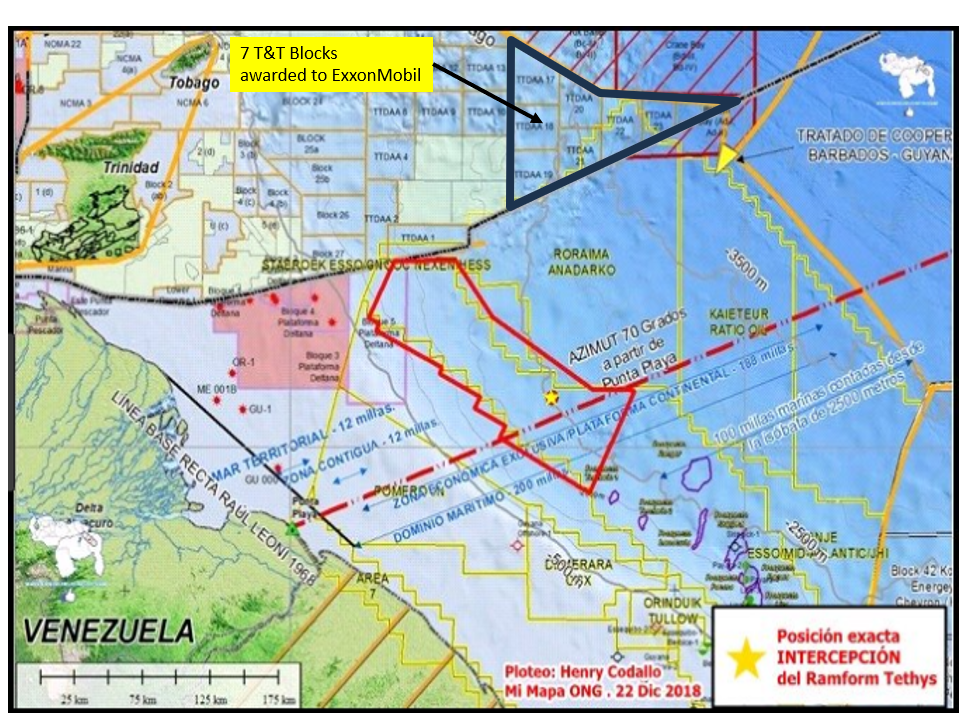

Consistent with her policy guidance, T&T signed a Production Sharing Contract with Exxon for a massive deepwater tract (Block Trinidad and Tobago Ultra Deep 1, map below). Per Ms. Persad Bissessar:

“Today’s signing underscores our government’s commitment to strengthening national energy security and to unlocking the full value of our hydrocarbon resources through discipline, policy, competitive terms and trusted partnerships.”

Although another Guyana is unlikely, the enormous lease block presents a great opportunity for Exxon. The consolidated block spans 7,765 square kilometers in the Eastern Tobago Basin in water depths exceeding 2,000 meters. By comparison, Trinidad and Tobago’s total surface area is about 5,128 square kilometers and a typical Gulf of America lease block is only 23 sq km. (Think about that! The size of US offshore lease blocks, which are the world’s smallest, needs to be reconsidered.)

Based on press reports, Exxon will carry out seismic acquisition within 12 months, followed by geological and geophysical studies, and drill up to 2 exploratory wells during the initial phases of the contract. (Reports differ as to whether one of those wells is mandatory, but presumably that won’t be an issue.)

Does this impressive deal reduce the likelihood that America’s largest oil company, which has essentially abandoned the Gulf of America except for its (fading?) carbon disposal ambitions, will participate in the upcoming Gulf lease sale? Politically, failure to participate would not seem to be very astute given the Administration’s promotion of domestic production and energy dominance.

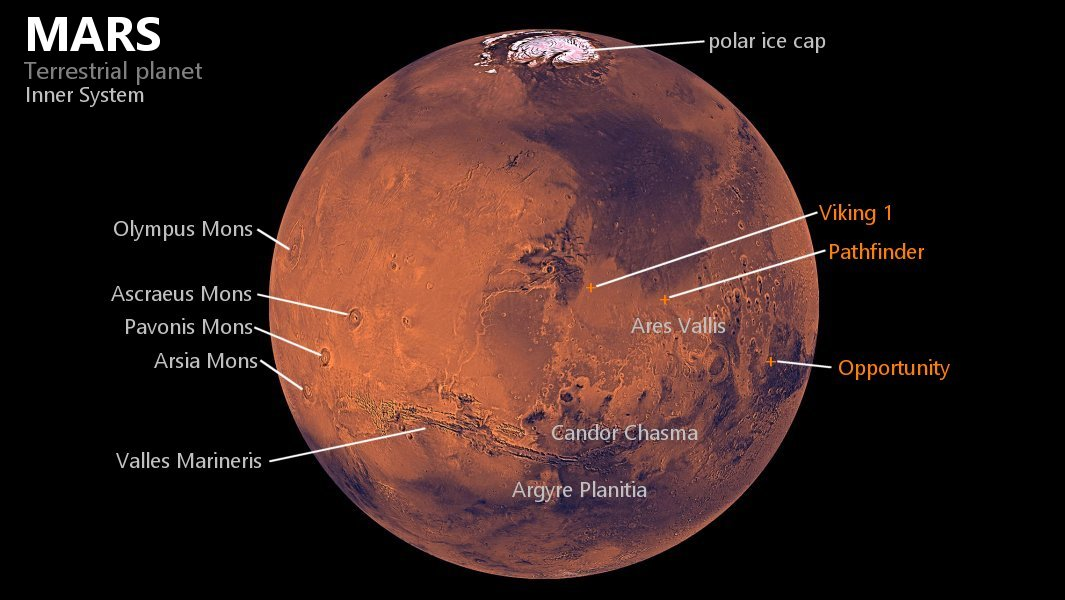

In light of the recent NASA/SpaceX advances in rocketry, a manned mission to Mars seems inevitable, perhaps within the next 5 years. See the SpaceX Mars landing video below.

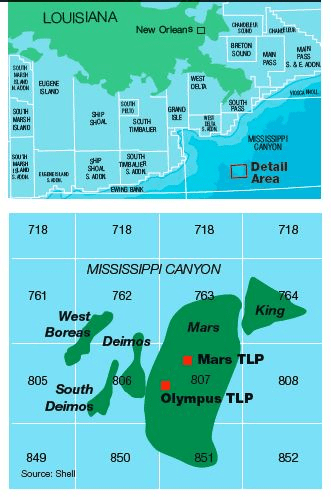

While the space program generates more media buzz given the sci-fi appeal, the achievements of the offshore oil and gas industry are similarly impressive. The Gulf of America has its own Mars, a massive deepwater project that has been ongoing and expanding for 30 years, and may ultimately produce more than 1 billion barrels of oil equivalent (boe).

Like a mission to Mars, the successful development of deepwater oil and gas resources is a technical marvel that requires:

Identifying prospects deep beneath the seafloor using advanced subsurface imaging capabilities.

Drilling exploratory wells from floating rigs, using advanced stationkeeping systems that maintain a precise location on the water surface.

Drilling deep beneath the seafloor while transmitting real-time geologic, temperature, and pressure data to the rig and distant onshore locations.

Ensuring well integrity by installing and cementing multiple strings of protective casing.

Processing production at buoyant surface facilities designed to withstand worst case storm conditions.

Connecting clusters of subsea wells to a host surface facility that may be many miles away.

Increasing ultimate recovery with reservoir engineering studies and advanced well completion practices.

Life on the planet Mars will be dependent on technology developed for the offshore Mars and other deepwater projects.

In light of the TikTok drama in Washington, I thought I’d take another look at Chinese ownership of Gulf of Mexico oil and gas leases.

A year ago, it was reported that State owned China National Offshore Oil Corp. (CNOOC) was considering an exit from its operations in the US, Canada, and the UK because of sanctions concerns. That may still be the case for other properties, but CNOOC has retained its Gulf of Mexico lease interests.

Per BOEM lease data, CNOOC continues to own 25% and 21% interest respectively in the important Stampede (Green Canyon 468, 511, and 512) and Appomattox (Mississippi Canyon 391, 392, and 393) deepwater projects. CNOOC reports are positive on those operations, noting that the production wells have performed better than expected.

CNOOC also owns interest in five other GoM leases. No CNOOC lease interest has been assigned to other companies in the past two years.

I welcome foreign investment in our offshore program, and see little downside in Chinese entities owning minority shares of OCS leases. GoM lease ownership does advance CNOOC’s understanding of deepwater exploration and development technology, but that knowledge can also be acquired elsewhere, sometimes in partnership with US companies (as is the case in Guyana).

“Stampede,” Gulf of Mexico: Hess 25% owner and operator, Chevron 25% owner

Most importantly, both companies have excellent safety and compliance records as evidenced by their Honor Roll achievements.

Hess is an attractive company with impressive assets. Were there other suitors?

Chevron is currently a partner on the Stampede, Esox, and Tubular Bells deepwater projects that are operated by Hess. There is thus an established deepwater development relationship.

The acquisition of Hess means that Exxon and Chevron will now be partners in Guyana. That should be interesting.

Chevron’s CEO Mike Wirth is quoted as saying “We’ve got too many CEOs per BOE, so consolidation is natural.” That comment seems a bit self-serving, but makes sense from the perspective of an acquiring CEO. Employees of the companies being acquired may have a somewhat different view.

In the Gulf of Mexico, will the combined company be greater than the sum of the parts in terms of lease acquisition, exploration, and development?

Will combining the companies limit the diversity of geological assessments and exploration strategies?

Consolidation affects participation in workshops and on committees engaged in assessing technology and developing standards. More limited participation in these activities, which are critical to offshore safety, was a justified concern of my former boss, the late Carolita Kallaur.

Add Hess to the list of important offshore operators that, for all intents and purposes, no longer exist. This list includes (among others): Amoco, Arco, Texaco, Getty, Gulf, Unocal, Sun, Anadarko, BHP, Mobil, Phillips (or Conoco), Noble Energy, Pennzoil, Kerr-McGee, and Newfield.