🚨BREAKING: Sec. @DougBurgum announces he will PAUSE leases for ALL large-scale offshore Wind projects immediately.

"Today we're sending notifications to the five large offshore wind projects that are under construction, that their leases are being suspended due to national… pic.twitter.com/lFPyMscALr

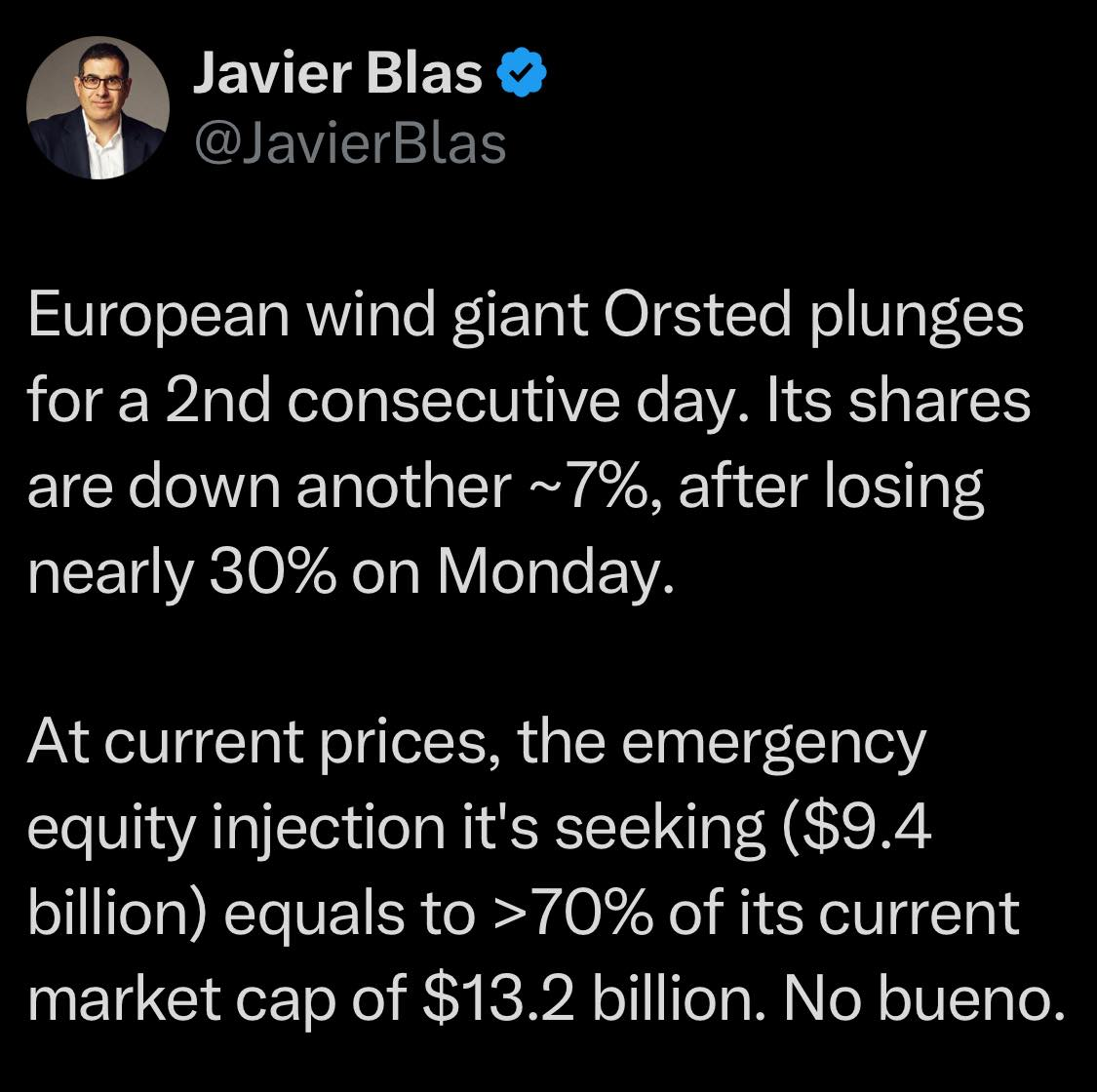

Ørsted’s stock price plummeted on Monday following the announcement of a $9.4 billion rights issue to fund the Sunrise Wind project. The share price has remained depressed (chart below).

Also, although Ørsted attributes its financial woes to the change in US policies, it’s apparent in the second chart (5 year trend) that the decline in Ørsted’s valuation has been ongoing since 2021.

In March, Fitch downgraded Ørsted’s rating to BBB from BBB+, and its subordinated rating to BB+ from BBB-. Further downgrades would seem to be a distinct possibility.

Meanwhile, decommissioning financing for the 3 Ørsted projects under construction in the US Atlantic is far from assured:

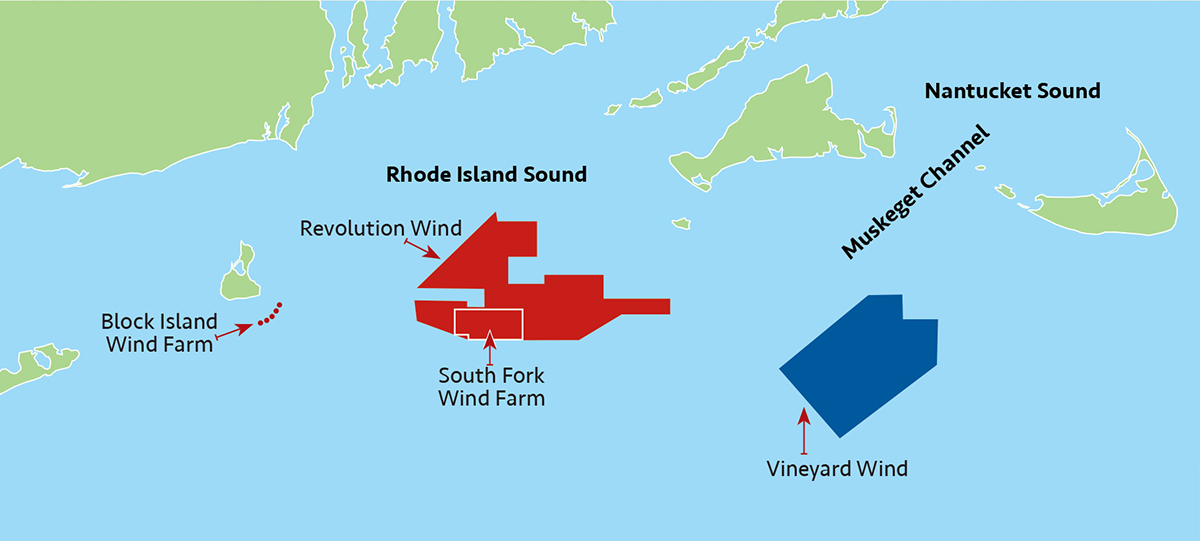

Revolution Wind:As they did for Vineyard Wind, BOEM approved Ørsted’s request to defer full decommissioning financial assurance until 15 years after the beginning of construction (see attached letter). This approval was prior to the Renewable Energy Modernization Rule (effective June 29, 2024), which eliminated the need for such waivers.

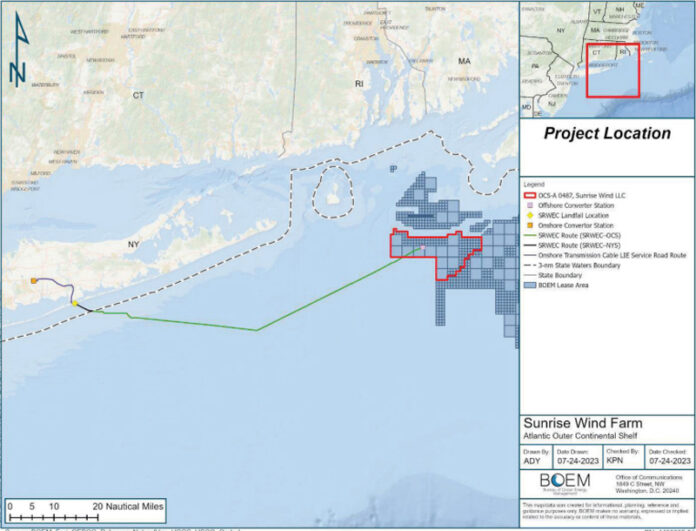

Sunrise Wind: Ørsted is now solely responsible for funding and constructing this project given the company’s failure to find investment partners. Presumably, decommissioning financial assurance was not required given BOEM’s latitude under the so-called “Modernization Rule.”

South Fork Wind: As is the case with Sunrise Wind, BOEM presumably allowed Ørsted to defer financial assurance for decommissioning as permitted by the “Modernization Rule.”

According to Ørsted, almost 70% of the turbines are installed at Revolution Wind and the first foundations have been installed at Sunrise Wind. South Fork Wind, 12 turbines and an offshore substation, is complete.

Given Ørsted’s strained finances, will BOEM now opt to require decommissioning assurance as provided for in 30 CFR § 585.517?

Ørsted’s situation is atypical in that the Danish government owns a majority (50.1%) stake in the company and Equinor, which is 2/3 Norwegian govt owned, holds a 9.8% stake. How will government ownership factor into BOEM decisions regarding decommissioning assurance? Note that Norwegian govt lobbying may have been one of the factors influencing the decision to allow the resumption of construction on Equinor’s Empire Wind project.

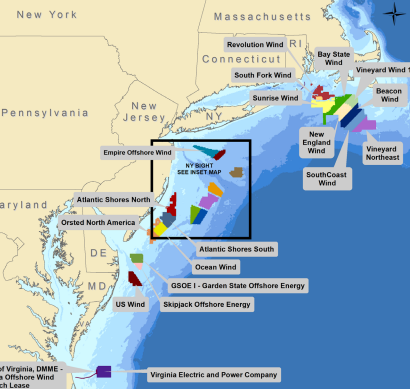

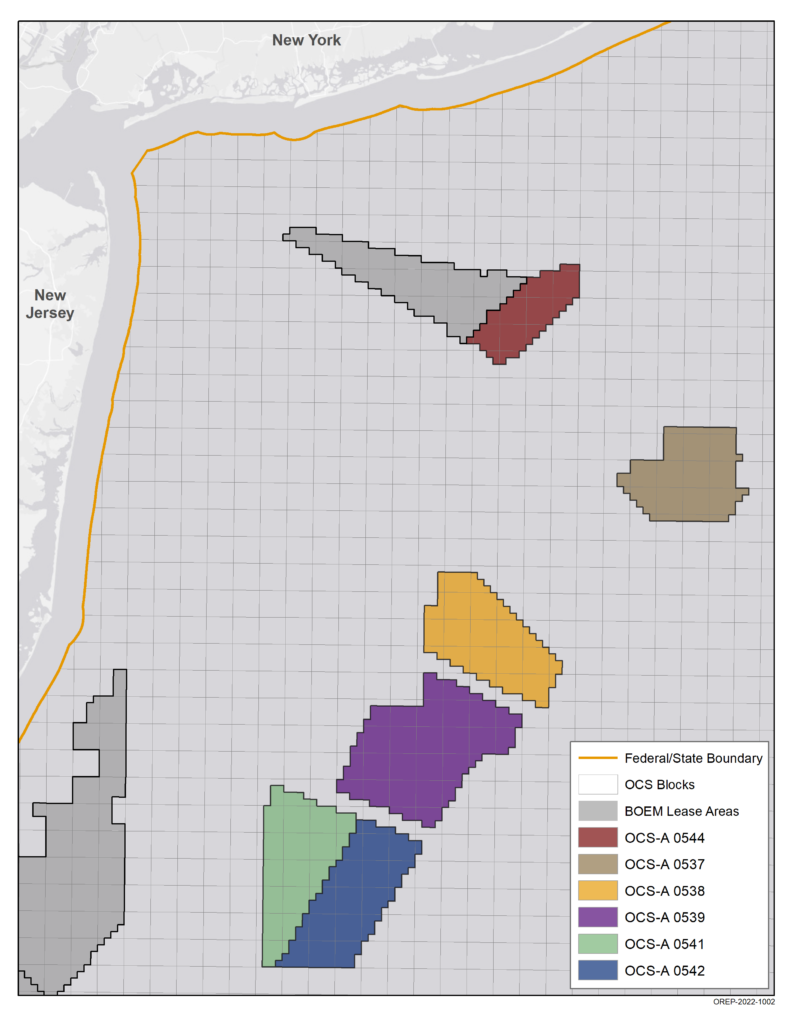

Bidding at the February 2022 Atlantic (NY/NJ) wind saleseemed incomprehensible given the economic and political uncertainties associated with offshore wind development.The 6 leases garnered bids ranging from $285 million to an astounding $1.1 billion, with total high bids of $4.37 billion! The Administration’s victory message correctly boasted that this was the “nation’s highest grossing competitive energy lease sale in history.”

The intense bidding was driven by the lure of subsidies, guaranteed power sales, unprecedented Federal and State promotion, peak climate activism, inattention to mounting public opposition, and irrational expectations regarding the role of offshore wind in powering the regional economy.

The table below summarizes the sale results and the current status for the 6 leasesissued following the 2/2022 sale. One lease has been essentially terminated by the partners and the State. The other leases are in holding patterns in the planning phases.

high bidder

lease #

acres

bid ($millions)

status

Bluepoint Wind (EDP, ENGIE, Global Infrastructure Partners)

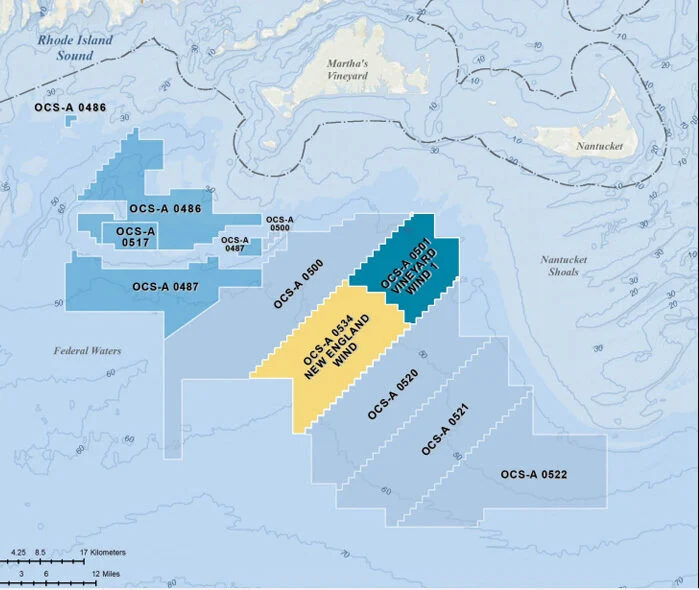

The first US commercial offshore project, Vineyard Wind, has proven to be a major step backward for the wind industry. After being granted questionable financial and quality assurance waivers to reduce costs and “allow Vineyard Wind to adhere to its construction schedule,” the July 2024 turbine blade failure and subsequent lightning strike have raised new questions about the technology, industry, and regulatory regime. The report on the blade failure, which should arguably be a precursor to the resumption of Atlantic wind development, has yet to be released.

The one shining light, relatively speaking, for Atlantic wind development, has been Coastal Virginia Offshore Wind. That large project is on track to be completed at the end of 2026. Although the cost has risen about nine per cent, to $10.7 billion, that increase is understandable given the higher than anticipated costs for upgrading the onshore network.

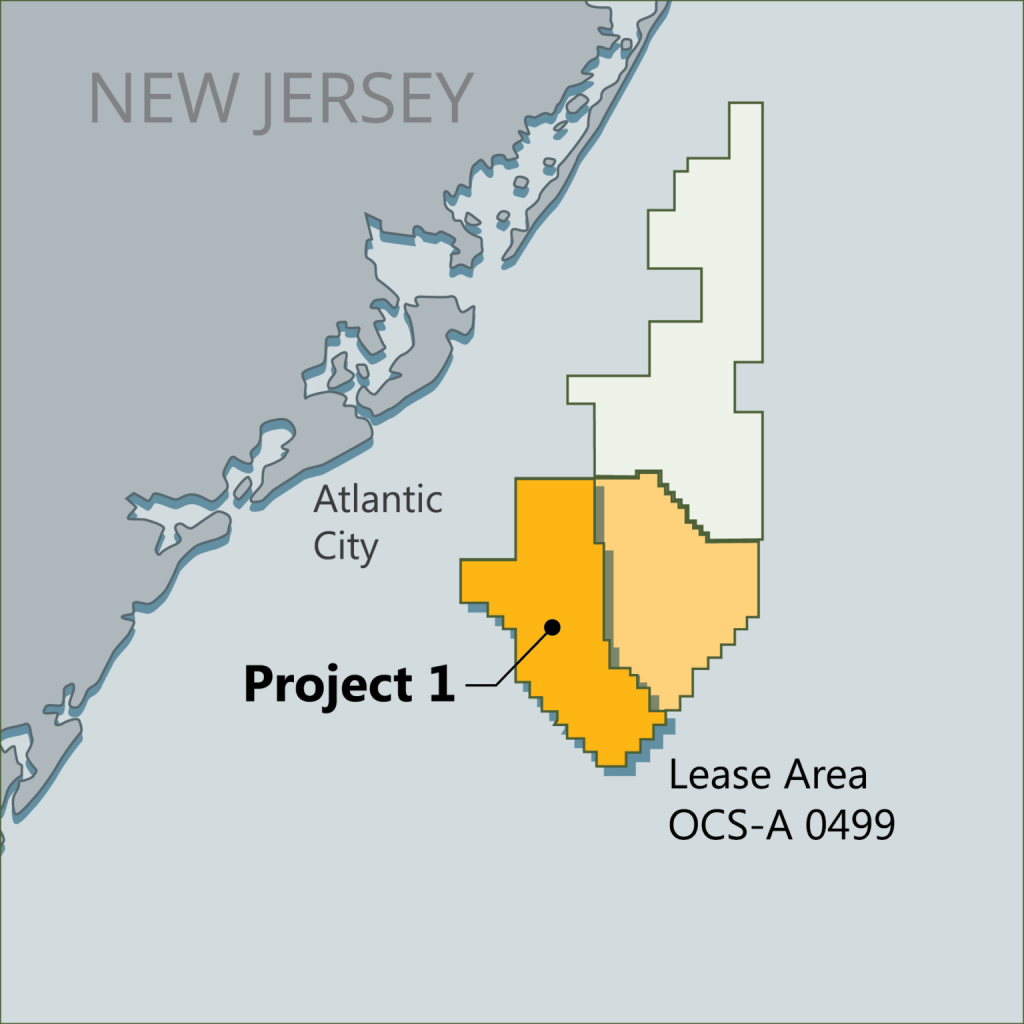

In February, EPA Region 2 asked the agency’s Environmental Appeals Board to remand Atlantic Shores’ air emissions permit back to the Region for reconsideration. That remand (attached) was granted on 14 March over the objections of Atlantic Shores Offshore Wind.

Atlantic Shores Offshore Wind still exists despite the exit of 50% partner Shell and a $940 million write down by the remaining owner EDF. The diagram depicts Atlantic Shores South (0499) and North (0549) lease areas.

EDF intends “to preserve the company and its future development.” Whether or not they can hold the leases indefinitely without pursuing development remains to be seen. BOEM’s diligence regulations for offshore wind projects are vague, and neither the Construction and Operations Plans nor BOEM’s Record of Decision (Atlantic Shores South) include work schedules.

Does EDF have the right to sit on the lease until the financial and regulatory environment is attractive? That is not allowed for oil and gas leases, and rightfully so. (See a related post on Total’s wind lease.)

The analysis does account for emissions related to and resulting from blade failures, which would warrant emergency repairs or replacement activities.

The decision to group Vineyard Wind 1, New England Wind 1 and New England Wind 2, as a single stationary source is both legally questionable and could have the effect of masking localized emission spikes.

Insufficient consideration of cumulative vessel emissions could lead to 1-hour NO₂ exceedances.

The emissions from pile driving are not adequately modeled in isolation or synergistically.

Groups and individuals opposing Atlantic wind projects sent the attached letter to Interior Secretary Doug Bergum asking for the withdraw of wind permits.

The groups cite serious problems with the National Marine Fisheries Service (NMFS) Letters of Authorization (LOA) for Incidental Take of endangered and threatened species. The LOAs authorized cumulative Takes of 548 individuals from a population of around 338.

The groups’ “no list” (project analysis deficiencies):

No EIS for the NMFS Incidental Take Authorization

No consideration of the impact of harassment in the Biological Opinion including cumulative impacts

No harassment authorization for the turbine installation ship

No consideration of using suction caissons instead of pile driving

No consideration of sediment plumes from ocean currents flowing through wind facilities

No assessment of a project’s contribution to the overall effects of multiple wind projects

No consideration of continuous operating noise

No consideration of physical presence-based harassment

In the wake of last week’s lackluster Atlantic wind lease auction (summarized above), an excellent Renewable Energy World article documents the sharp decline in participation and bidding since the massive February 2022 sale of 6 leases offshore NY and NJ. That sale garnered bids ranging from $285 million to an astounding $1.1 billion, with total high bids of $4.37 billion! The sale was touted as the “nation’s highest grossing competitive energy lease sale in history.” The extravagant bidding, which made little sense then, seems downright irrational now.

Even the December 2022 California offshore lease sale, where development will be dependent on more expensive floating turbines, attracted substantially higher bids for leases (5) smaller than those auctioned last week.

The highly promoted Gulf of Mexico wind auctions were busts with the first sale receiving only one bid for $6.5 million and the second being cancelled due to lack of interest.

Major oil companies like bp and Shell seem to have exited the market for new US offshore wind leases. That leaves Equinor (2/3 Norwegian govt ownership) as the only major oil company pursuing US offshore wind leases.

“Today’s lease sale reflects the forward momentum we are seeing to power millions of American homes with clean energy and create good-paying, climate jobs,” said White House National Climate Advisor Ali Zaidi. “With nine commercial-scale projects approved in the last three years and more to go, we are using every available tool to grow the American offshore wind industry as we strengthen the nation’s power grid and tackle the climate crisis.”

BOEM’s land rush approach to offshore wind leasing will add up to 1086 turbine towers and 28 offshore substations (OSSs) in the Atlantic just from active projects with approved Records of Decision (RODs). (See the table below.) Another 17 active Atlantic commercial projects have yet to reach the ROD stage. Those projects should increase the total number of structures to >3000. Five more Atlantic wind lease sales are scheduled.

project

turbine towers

offshore substations

Coastal VA Offshore Wind

202

3

Revolution Wind

100

2

Sunrise Wind

94

1

Atlantic Shores South

200

up to 10

Ocean Wind 1

98

up to 3

Vineyard Wind 1

100

2

Empire Wind 1 & 2

147

2

New England Wind (phases 1&2)

150

5

Per the Construction and Operations Plan (COP) for Vineyard Wind, the topsides for a conventional electrical service platform (ESP) (also known as an offshore substation or OSS) are 45 x 70 x 38 m, which is larger in surface area than a typical 6-pile oil and gas platform (~30 x 30 m), and is comparable in size to a large jackup drilling rig.

The Atlantic Shores plan calls for 10 small, 5 medium, or 4 large OSSs. (Uncertainty regarding the number and types of structures seems rather common in wind COPs.) The large OSSs have topsides that are 90 m by 50 m and rise to 63 m above MLLW. These are large offshore structures whether for wind or oil and gas.

Per BOEM, the “Rule to Streamline and Modernize Offshore Renewable Energy Development” is intended to “make offshore renewable energy development more efficient, [and] save billions of dollars. Unfortunately, the savings associated with relaxed financial assurance requirements translates to increased risk for power customers and taxpayers.

BOEM signaled their intentions on offshore wind (OSW) decommissioning three years ago when they granted a precedent setting financial assurance waiver to Vineyard Wind. Despite compelling concerns raised by commenters, the “streamlining” regulations codified this decision.

No one knows what the financial future will be for wind projects and the responsible companies. Financial assurance should therefore be established when the structures are installed, not years into the future as allowed by the revised regulations. What leverage will BOEM have then?

Nordsee One substation, Germany. Rystad Energy projects 137 new power substations offshore continental Europe this decade, requiring $20 billion in total investment.