A post from last March discussed the high and seemingly unfair royalty and rental rates for new leases in the shallow waters of the Gulf of Mexico shelf. A 50% increase in the shelf royalty rate for lease sales 259 and 261 combined with rather punitive rental rates have likely contributed to the sharp decline in bidding for shelf lease blocks (see table below).

This decline in shelf bidding is unfortunate because the smaller companies that operate in the shallow waters of the Gulf are critical to sustaining the production infrastructure. These companies are also significant producers of environmentally favorable nonassociated (gas-well) natural gas.

lease sale

shelf blocks with bids (excluding CCS bids)

sum of high shelf bids ($million, excluding CCS bids)

BOEM has completed their evaluation of the Sale 261 shelf bids (see below). Each of these blocks received only a single bid, and every bid was accepted. Ironically, the invalid CCS bids for blocks that have no oil and gas value, were the first to be accepted. This was also the case for Sales 257 and 259.

Company

Block

high bid ($) per acre ($)

date accepted

Byron

SM 60

128,750 25.75

2/2

Byron

SM 70

182,235 33.32

2/20

Cantium

GI 35

125,000 25.00

2/20

Cantium

GI 36

125,000 25.00

2/20

Cantium

MP 314

125,000 25.00

3/12

Cantium

SP 63

125,000 25.00

3/12

Arena

EI 231

135,000 27.18

2/20

Arena

EI 277

135,000 27.18

2/20

Arena

EI 281

135,000 27.18

2/20

Arena

EI 340

135,000 27.18

2/20

Arena

EI 343

135,000 27.18

2/20

Arena

WD 119

135,000 26.75

3/12

Focus

V 152

121,152 25.16

2/20

Repsol

36 CCS bids

187,200 (1) 32.50

1/23

(1) All of the Repsol bids were $32.50/ac. Total bids varied by block size, but were $187,200 for the 5760 acre blocks.

Suggestions:

Seek a legislative fix to the Inflation Reduction Act😉 provision that established a 1/6 royalty rate floor for all OCS leases (formerly the royalty rate was 1/8 for leases on the shelf).

In the interim, administratively lower the royalty for shelf leases to 1/6 (from 18 3/4%).

For future oil and gas lease sales, accept all high bids that exceed the specified minimum bid (currently $25/ac for the shelf). The Gulf of Mexico shelf has been extensively explored and developed for 70 years. While prospects remain, they are generally marginal as evidenced by the recent lease sale results. Fair market value is what any company is willing to bid (above the specified minimum).

Focus on assuring that lease purchasers are technically qualified to minimize safety risks, and that financial assurance for decommissioning (for new and existing leases owned by the high bidder) has been fully addressed.

Rincon Island and the onshore facility were constructed in 1959 and used for oil and gas production. In December 2017, Rincon Island Limited Partnership, the most recent lessee, transferred its lease interests to the State after becoming financially insolvent. Phase 1 of decommissioning included the plugging and abandonment of all oil and gas wells and removal of service equipment at Rincon Island.

The proposed Phase 2 project, analyzed within the Environmental Impact Report (executive summary attached), would prudently retain Rincon Island and the Rincon Island Causeway in their current configuration. Phase 3 will prepare Rincon Island and the Onshore Facility to be leased for yet-to-be determined new uses.

In light of the TikTok drama in Washington, I thought I’d take another look at Chinese ownership of Gulf of Mexico oil and gas leases.

A year ago, it was reported that State owned China National Offshore Oil Corp. (CNOOC) was considering an exit from its operations in the US, Canada, and the UK because of sanctions concerns. That may still be the case for other properties, but CNOOC has retained its Gulf of Mexico lease interests.

Per BOEM lease data, CNOOC continues to own 25% and 21% interest respectively in the important Stampede (Green Canyon 468, 511, and 512) and Appomattox (Mississippi Canyon 391, 392, and 393) deepwater projects. CNOOC reports are positive on those operations, noting that the production wells have performed better than expected.

CNOOC also owns interest in five other GoM leases. No CNOOC lease interest has been assigned to other companies in the past two years.

I welcome foreign investment in our offshore program, and see little downside in Chinese entities owning minority shares of OCS leases. GoM lease ownership does advance CNOOC’s understanding of deepwater exploration and development technology, but that knowledge can also be acquired elsewhere, sometimes in partnership with US companies (as is the case in Guyana).

Pictured: pig for cleaning gas pipelines. Will Nord Stream’s suit against the insurers unplug investigation findings?

Nord Stream AG has sued insurers Lloyds and Arch in the English High Court for failing to pay for pipeline damage incurred during the Sept. 2022 Baltic Sea explosions. The estimated pipeline repair costs range from €1.2 to €1.35 billion, and Nord Stream is seeking €400 million from the insurers.

Could this litigation help us learn more about the findings of the official Nord Stream investigations? After 17 months of investigation, Denmark recently concluded that “there are not sufficient grounds to pursue a criminal case in Denmark.” Only nineteen days before Sweden had announced that “Swedish jurisdiction does not apply and that the investigation therefore should be closed.” These weak announcements at the end of lengthy investigations seem too convenient, and may lend credence to Hersh’s Nord Stream account or a recent variation that implicates the UK. Germany is presumably still investigating, and it remains to be seen whether they will release findings.

Could the parties in the Nord Stream case pursue documents or testimony from the Swedish, Danish, or German investigation teams? Both sides in this case, Nord Stream AG and the insurers, would benefit from details that could help identify the responsible parties.

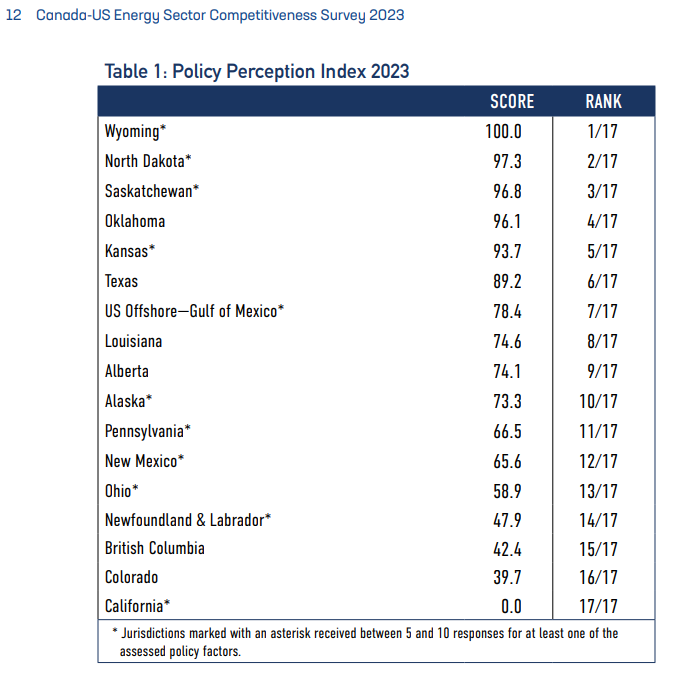

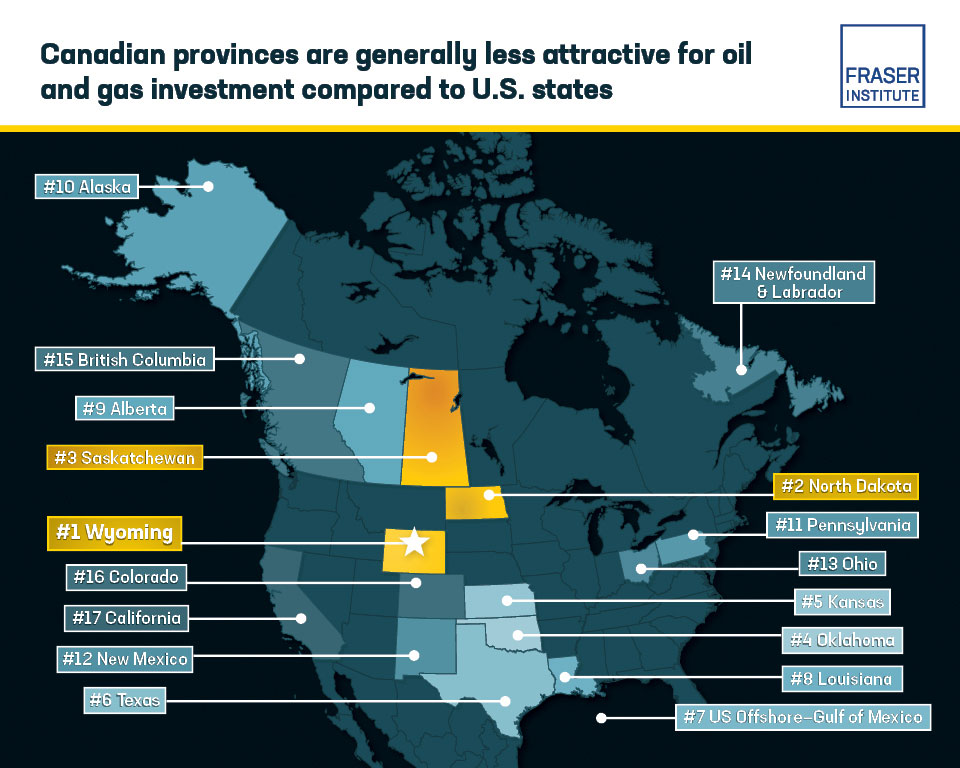

The Fraser Institute’s 2023 Canada-US Energy Sector Survey of senior executives in the upstream oil and gas sector provided data for assessing the competitiveness of US and Canadian jurisdictions. The resulting perception index (below) ranked Wyoming at the top with a score of 100.0 and California at the bottom with a score of 0.0. Perhaps one or more of the respondents have been mired in the California decommissioning quagmire. ☹

(2) the Secretary may not issue a lease for offshore wind development under section 8(p)(1)(C) of the Outer Continental Shelf Lands Act (43 U.S.C.1337(p)(1)(C)) unless— (A) an offshore lease sale has been held during the 1-year period ending on the date of the issuance of the lease for offshore wind development; and (B) the sum total of acres offered for lease in offshore lease sales during the 1-year period ending on the date of the issuance of the lease for offshore wind development is not less than 60,000,000 acres.

Lease Sale 261 was held on 12/20/23. Absent legislative action, no wind leases may be issued after 12/20/24 unless another oil and gas lease sale is held prior to that date. Given that the minimalist 5 year oil and gas leasing plan, which is being challenged, does not propose a sale until 2025, wind lease issuance will likely be suspended at the end of the year. (Note: I wonder if the legislative restriction also applies to lease assignments from existing owners to new owners? Probably not, but that would be very significant given the current state of the offshore wind industry.)

Perhaps the wind program should be required to develop 5 year leasing plans, as is the case for the oil and gas program. This might facilitate a more holistic approach to wind energy development and ease concerns about cumulative impacts.

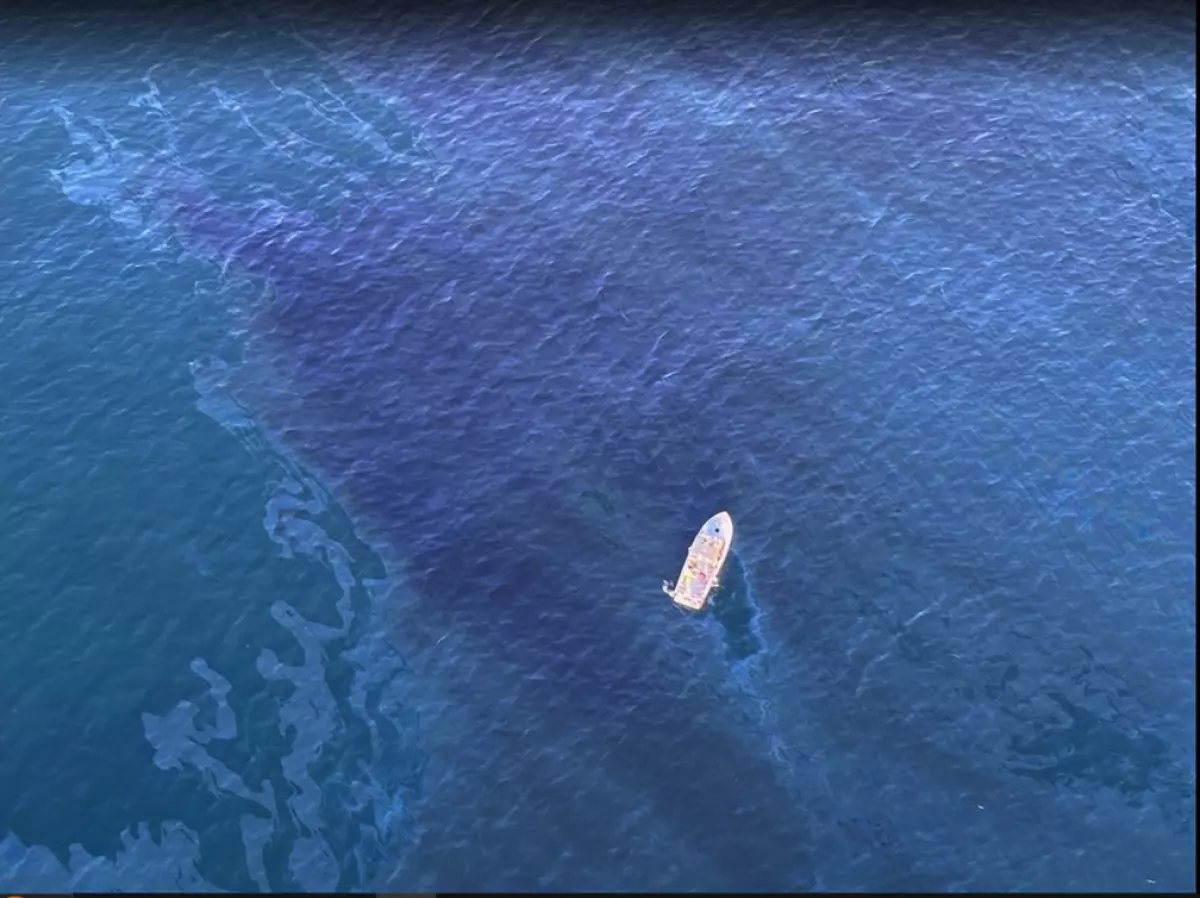

Test results came back from the Office of Spill Prevention and Response – part of the Department of Fish and Wildlife – indicating the natural oil source, said Richard Uranga, US Coast Guard public affairs specialist.

“From the first initial stages, they were tracking that from the samples,” he said. “The oil rig samples were not the same as the oil that was gathered from the oil sheen.”

So why did the LA Times report shortly after the sheen was detected that it was not from natural causes, and attribute that finding to the Coast Guard? It was too soon for the lab results to be back. Was a platform spill the desired narrative?

Chevron continues to operate in Venezuela and is a beneficiary of the easing of US sanctions that facilitated the resumption of oil exports. Is the government of Guyana okay with Stabroek partners helping to support the regime that claims much of their offshore oil?

On the other hand, what about Exxon’s Stabroek partner, state-owned China National Offshore Oil Corp.? CNOOC has a 25% share of the Stabroek block (vs. 45% for Exxon and 30% for Hess) as a result of their takeover of (Canadian) Nexen in 2013. The CNOOC acquisition of Nexen was similar to Chevron’s acquisition of Hess. Was Exxon okay with that change in ownership?

CNOOC hasn’t released any public statements on the Stabroek dispute, but appears to be aligned with Exxon. Presumably, CNOOC also wants a larger share of the Stabroek pie. Is the Government of Guyana okay with an ally of Venezuela increasing their influence and having access to geologic, reservoir, and operational data for the Stabroek block? CNOOC is also partnered with Exxon on the block they acquired at the most recent licensing round.

Given the national security implications, is the Government of Guyana okay with leaving the resolution of this dispute to an ICC tribunal in Paris?

According to the LA Times, the Coast Guard said the sheen was not from natural causes, but the Coast Guard press releases don’t say that. One of the nearby platforms could have been the source as could a pipeline or vessel. We’ll see what, if anything, the investigators find.