Judge Royce Lamberth granted an injunction allowing Orsted to resume work on the Revolution Wind project. BOEM halted work on the project one month ago.

Posted in energy policy, Offshore Wind, Regulation, tagged BOEM, Orsted, injunction, Revolution Wind, Judge Lamberth on September 22, 2025| Leave a Comment »

Judge Royce Lamberth granted an injunction allowing Orsted to resume work on the Revolution Wind project. BOEM halted work on the project one month ago.

Posted in energy policy, Offshore Wind, Regulation, tagged BOEM, BSEE, COP, New England Wind, Vineyard Wind on September 4, 2025| Leave a Comment »

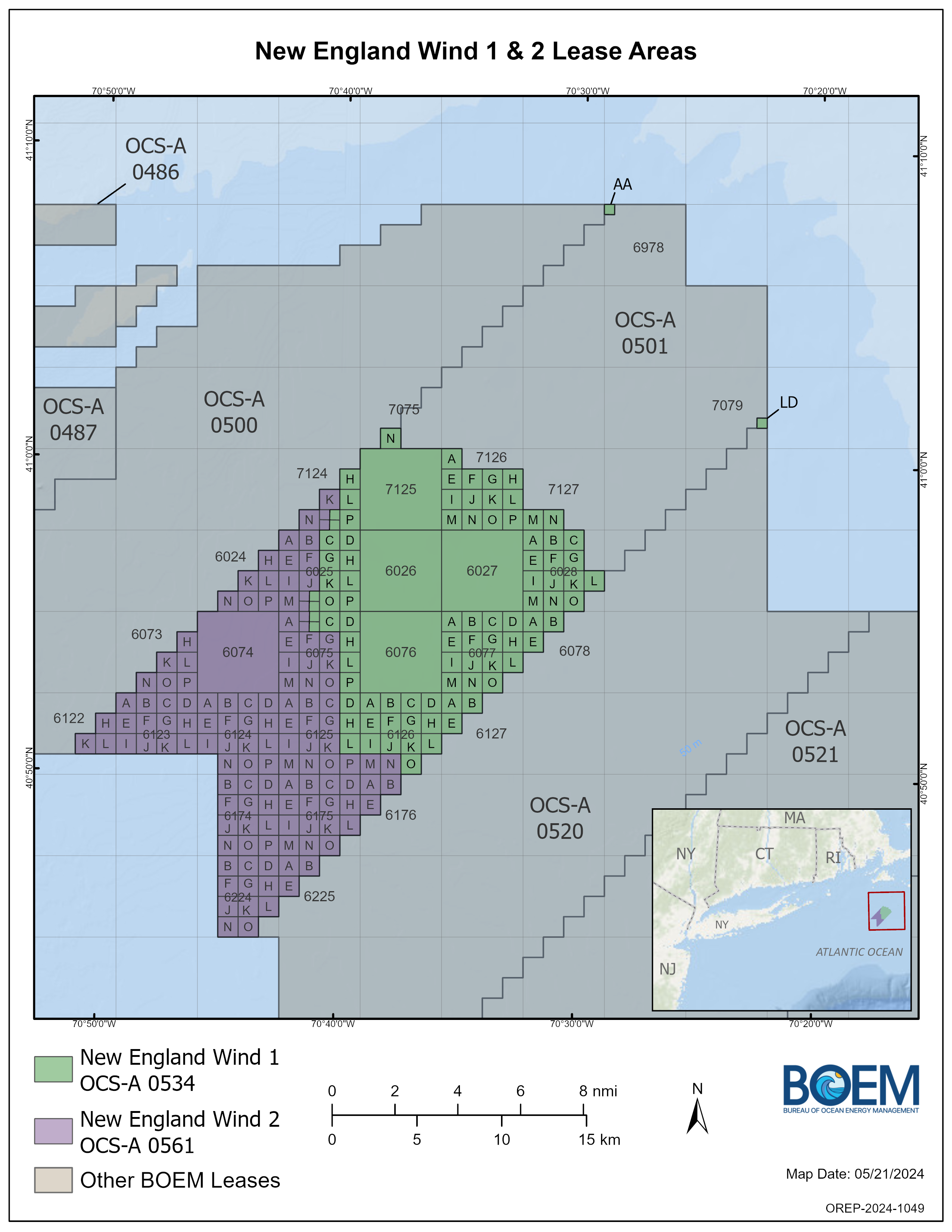

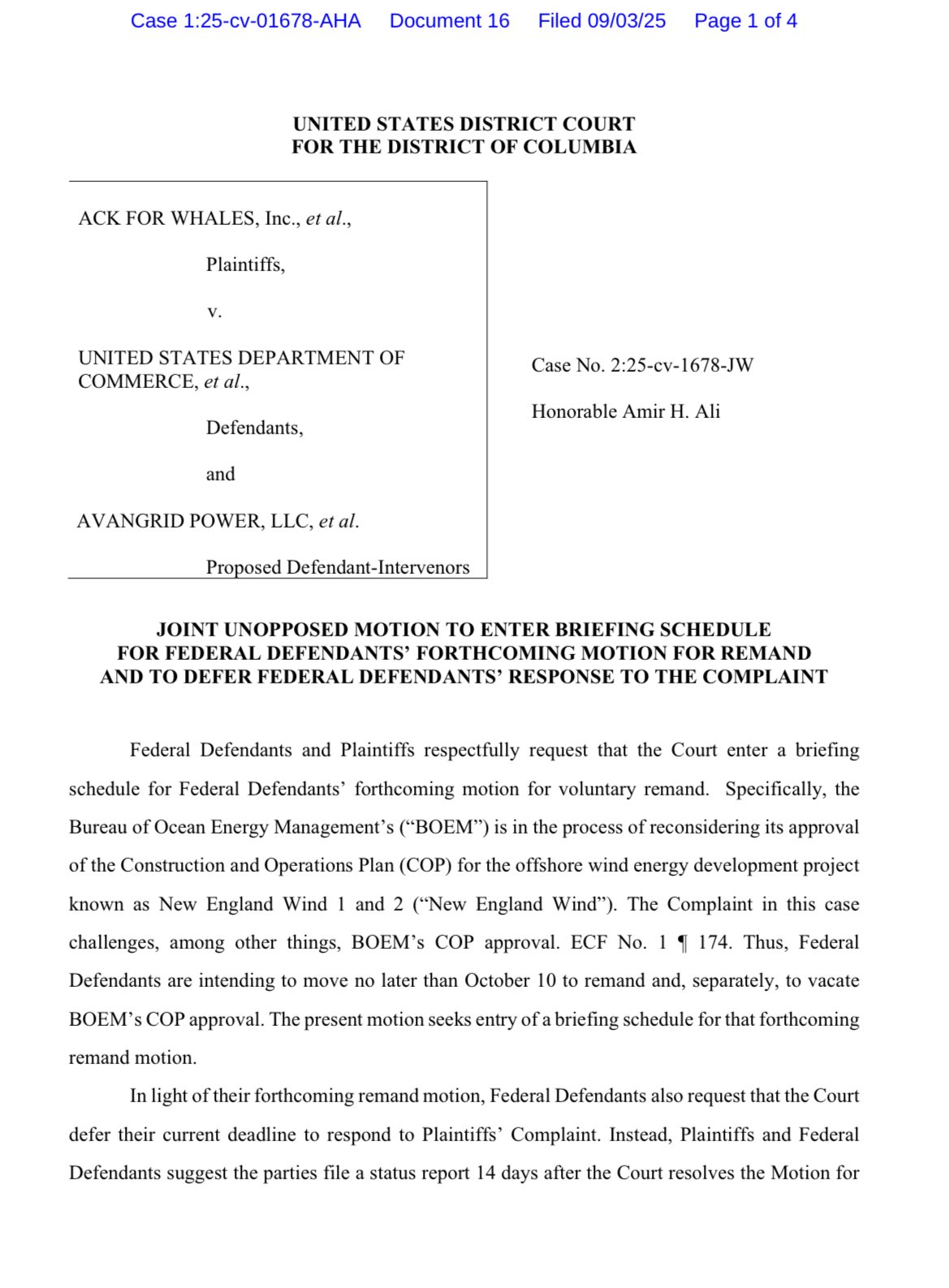

See below. BOEM is reconsidering its approval of the Construction and Operations Plan (COP) for New England Wind 1 and 2. The operator, Avangrid (Spain), is also a partner in the troubled Vineyard Wind project.

If you are keeping score, the approval of these COPs is being reconsidered:

Other projects: Work has been stopped on the Revolution Wind project. Work was previously halted on the Vineyard Wind and Empire Wind projects, but has been allowed to resume. BSEE has still not published its report on the Vineyard Wind turbine blade failure that occurred on 7/13/2024. Other projects have been suspended by the owners at their own initiative (e.g. Atlantic Shores South, Gulf of Maine, Starboard Wind, Vineyard Wind 2, Beacon Wind). Meanwhile, litigation abounds!

Coastal Virginia Offshore Wind is the project with the most assured long-term future.

Posted in Offshore Wind, Regulation, energy policy, tagged Nantucket, SouthCoast Wind, US Dept. of the Interior, COP, Ocean Wind, EDP Renewables, ENGIE on September 2, 2025| Leave a Comment »

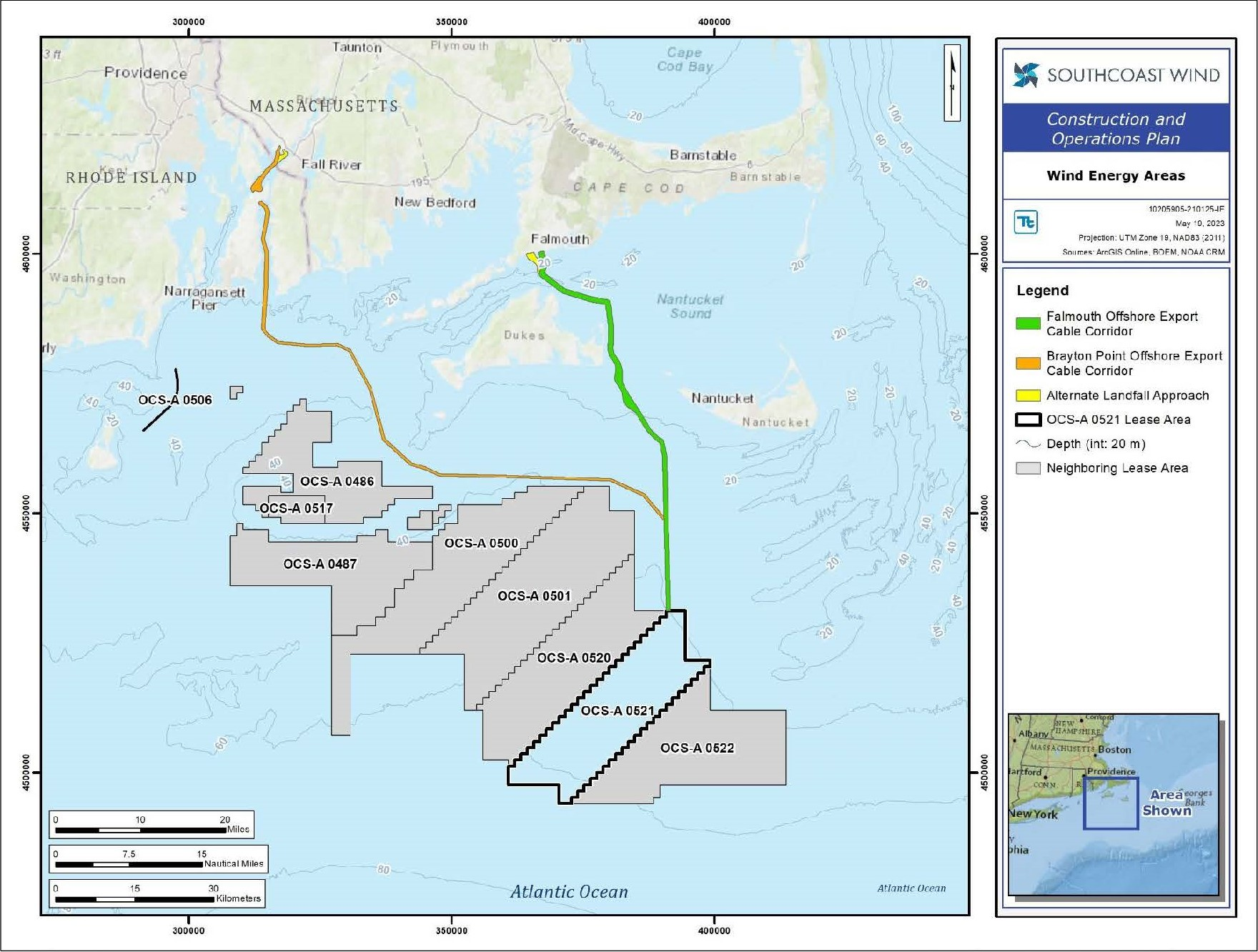

The Construction and Operations Plan (COP) for the SouthCoast Wind project was approved during the last week of the Biden Administration. That approval has been challenged by the Town and County of Nantucket. Ocean Wind, a joint venture of EDP Renewables (Portugal) and ENGIE (France), is the leaseholder.

As is the case for Maryland Wind, a court filing (attached) indicates that DOI is reconsidering the approval of the SouthCoast Wind COP. Construction has not begun on this project.

A further deferral of Federal Defendants’ responsive pleading deadline in this case is needed because Interior intends to reconsider its COP approval and will therefore be moving for a voluntary remand of that agency action by September 18, 2025.

Posted in Norway, Offshore Wind, tagged energy, Equinor, good money after bad?, Offshore Wind, Orsted, special shares on September 1, 2025| 1 Comment »

Equinor (2/3 Norwegian govt owned) is increasing its position in Ørsted (50.1% Danish govt owned). Given the ownership structure, public money is at risk for both countries.

The comments below are from a DN Norway article. They were made by CEO Torgrim Reitan after Equinor announced that the company will contribute NOK 10 billion (USD 1 billion) in Ørsted’s special share offering.

Given that the value of their initial NOK 26 billion (USD 2.6 billion) investment in Ørsted last fall has almost been cut in half, this is a bold move by Equinor. The company has been sharply criticized for its wind investments by private Norwegian investors.

“We want a closer partnership with Ørsted. We are two leading companies in offshore wind, and we believe a closer collaboration could create significant value for both Ørsted’s and our own shareholders.”

“This industry is now going through its first real crisis. That makes it quite clear what’s needed. We know a lot about this from oil and gas. What often happens in such times is consolidation.”

“We want a closer partnership with Ørsted. We are two leading companies in offshore wind, and we believe a closer collaboration could create significant value for both Ørsted’s and our own shareholders.”

“In recent weeks, we’ve had conversations with Ørsted management, and we’ve also had conversations with the Danish state. But the discussions have primarily been with Ørsted.”

“Ørsted is in a difficult situation right now. For us, as an industrial and long-term owner, it’s important to be supportive and helpful in such a situation. That’s why we’re putting in nearly a billion dollars.”

“This is a difficult decision, because clearly a lot of equity capital needs to be raised, but we have a fundamental belief in the industry, and also in the company. Ørsted’s underlying portfolio is a strong one.”

“Going forward, this will increase our debt ratio somewhat—maybe by about two percentage points. But we’re starting from a very low debt ratio. So we can manage this within our financial framework. As for capital distribution in 2026 and beyond, we will remain competitive.”

Meanwhile, Equinor is the only major oil company that remains invested in US offshore wind energy. Equinor’s Empire Wind project continues to be highly divisive.

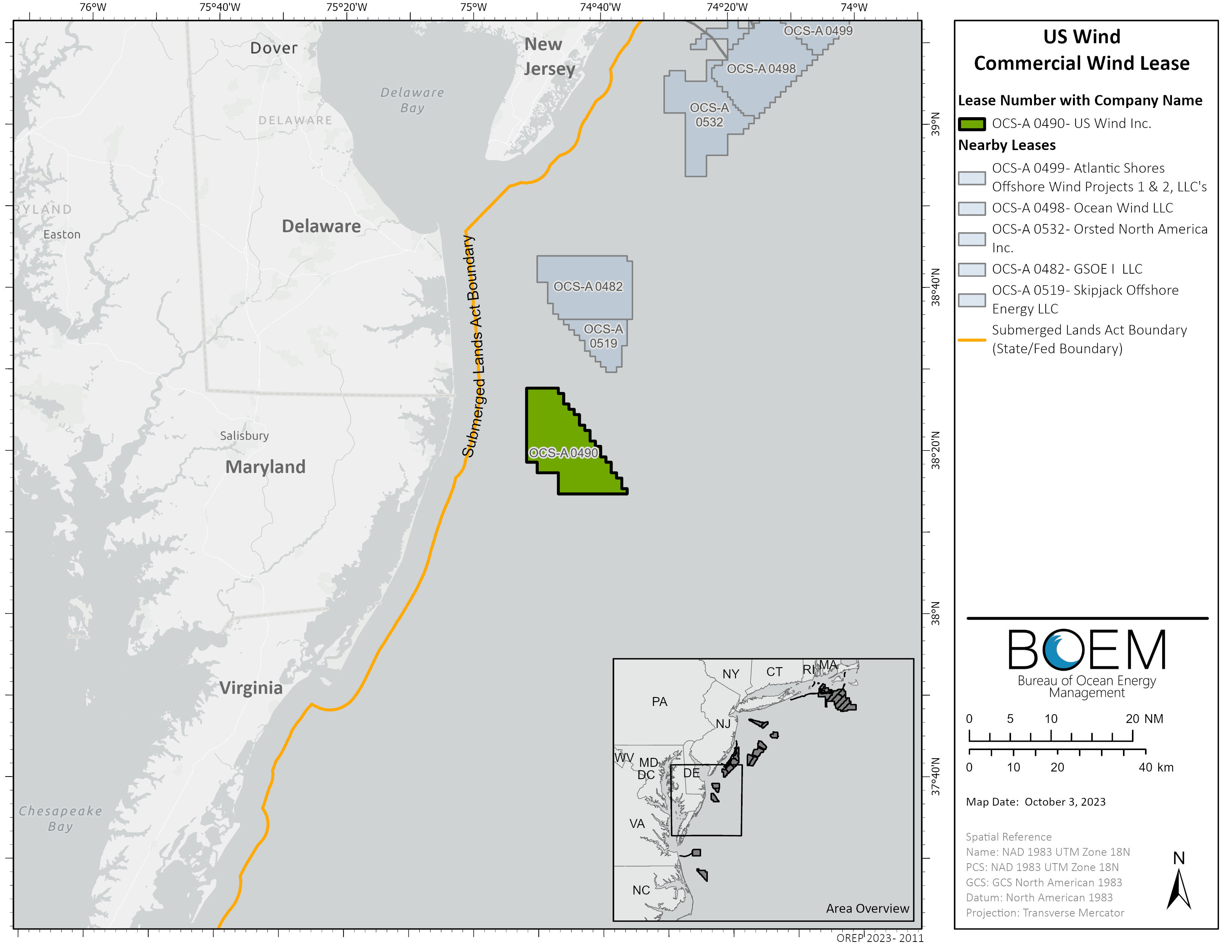

Posted in energy policy, Offshore Wind, tagged Federal local alliance, Maryland, Ocean City MD, US Dept. of the Interior, US Wind, wind litigation on August 27, 2025| Leave a Comment »

Historically, State and local governments have tended to be aligned, either for or against offshore energy (primarily oil and gas) leasing. However, a new (offshore) world order is emerging with local governments joining the new Administration in opposition to wind projects.

Most recently, and consistent with previous speculation, the Federal govt announced its intent to revoke approval of the Construction and Operations Plan for the US Wind project offshore Maryland and Delaware. (See the attached court filing.) This project is not yet in the construction phase.

Particularly noteworthy, as has been the case for other wind projects offshore Mid-Atlantic and New England states, is the alignment of Federal and local (coastal) govts in opposition to State policies.

Specifically, with regard to the US Wind project, the positions of State and local leaders couldn’t differ more:

Ocean City MD Town Manager Terry McGean:

“This is an extremely positive development in our fight against the irresponsible and costly US Wind project,” McGean said to WBOC on Monday. “We have stated all along that the approval of this project was fast and tracked without adequate public input and that approvals ignored significant risks to our economy, fishing industry, marine mammals, and the horseshoe crab. We are glad that our concerns are finally being taken seriously.”

“For the past eight years, Ocean City has voiced strong opposition to the proposed US Wind project. Unfortunately, we believe this project was fast-tracked and that our serious concerns have been largely ignored throughout the review process.“

Contrast the above comments with this statement from MD Governor Wes Moore:

“Canceling a project set to bring in $1 billion in investment, create thousands of good paying jobs in manufacturing, and generate more Maryland-made electrical supply is utterly shortsighted,” the Governor’s statement reads in part. “The President’s actions will directly lead to utility-rate hikes by taking off most promising ways for Maryland to meet its looming energy generation challenges.”

Such sharply divergent views are also evident in other coastal states. Offshore wind could be a factor in the upcoming gubernatorial race in NJ. The pro-wind energy candidate has the support of large environmental NGOs, while her opponent is supported by grass roots environmental groups that strongly oppose wind projects.

Posted in energy policy, Offshore Wind, Regulation, tagged BOEM, interference with other uses, national security, Orsted, Revolution Wind, shutdown order on August 23, 2025| Leave a Comment »

The Revolution Wind shutdown order is attached. The letter cites concerns about national security and interference with other offshore activities.

Excerpt from Ørsted’s response:

“Ørsted is evaluating all options to resolve the matter expeditiously. This includes engagement with relevant permitting agencies for any necessary clarification or resolution as well as through potential legal proceedings, with the aim being to proceed with continued project construction towards COD in the second half of 2026.”

Posted in energy policy, Offshore Wind, Regulation, tagged activity halted, BOEM, Orsted, Revolution Wind on August 22, 2025| Leave a Comment »

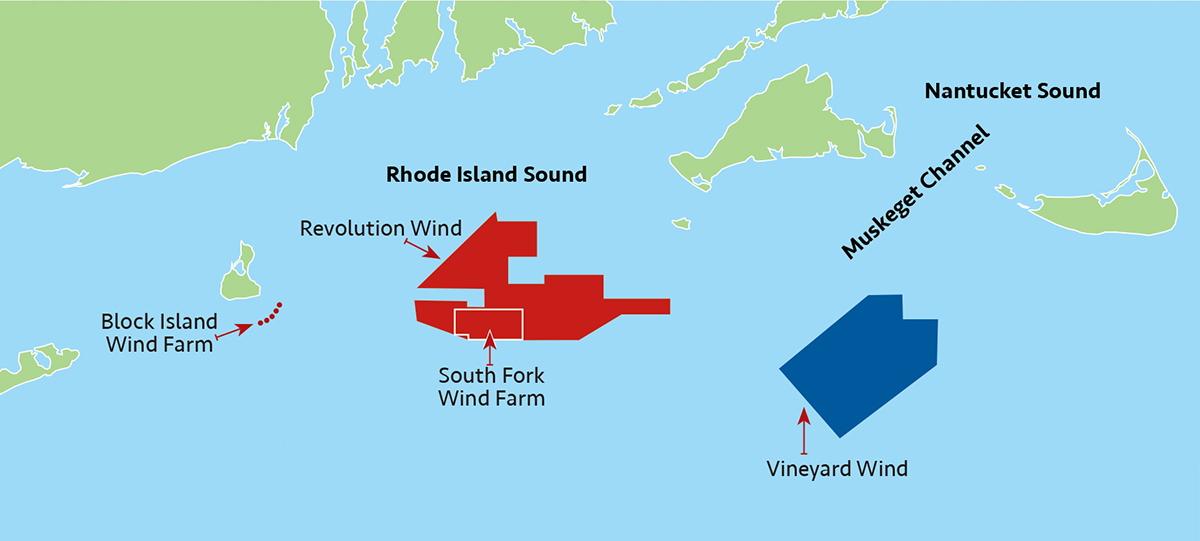

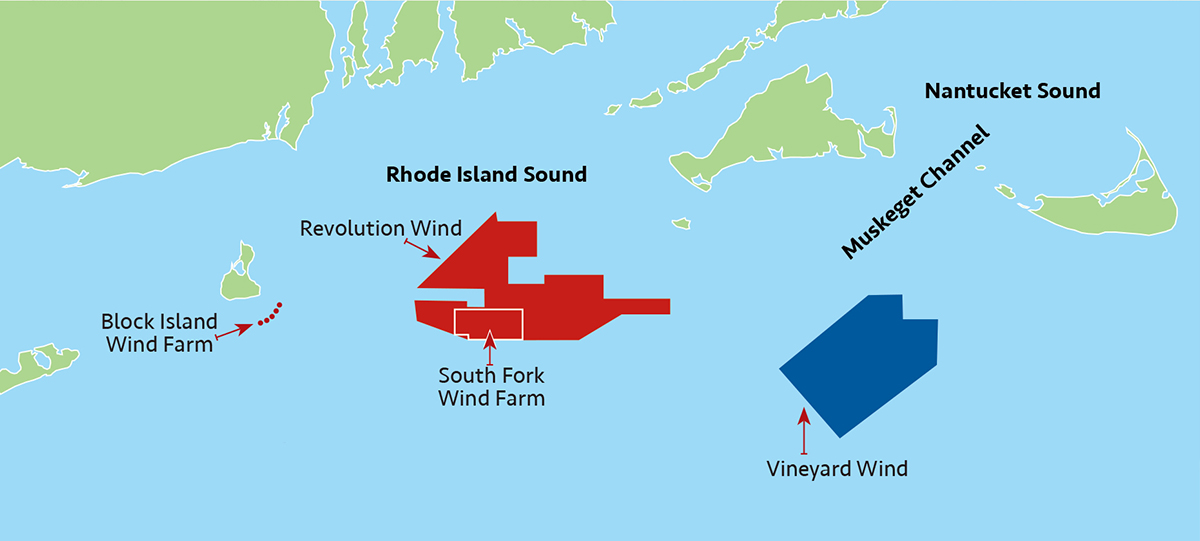

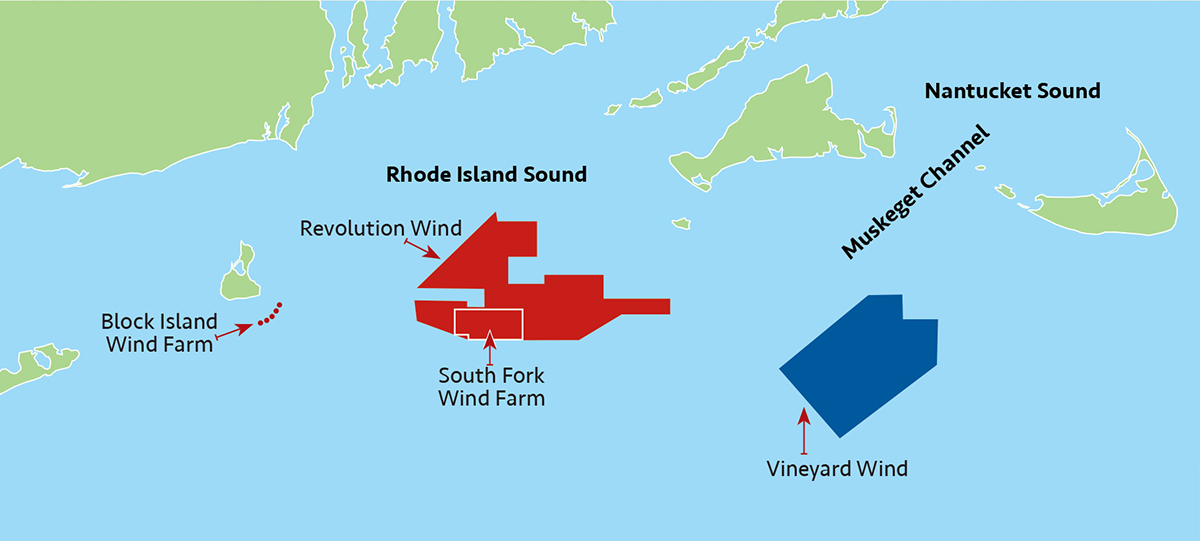

The Bureau of Ocean Energy Management (BOEM) is halting activity on the Revolution Wind project off the coast of Rhode Island and Connecticut. No details on this decision have been provided.

According to Ørsted, all of Revolution Wind’s foundations and almost 70 per cent of the turbines have been installed.

Revolution Wind is a partnership between Ørsted and Global Infrastructure Partners’ Skyborn Renewables.

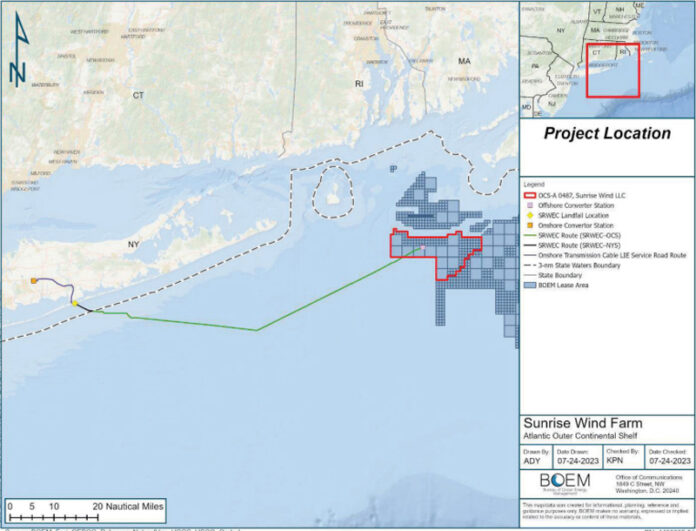

Posted in decommissioning, Offshore Wind, tagged Atlantic wind, Ørsted stock price, decommissioning, Equinor, financial assurance, Orsted, Revolution Wind, South Fork Wind, Sunrise Wind on August 14, 2025| 1 Comment »

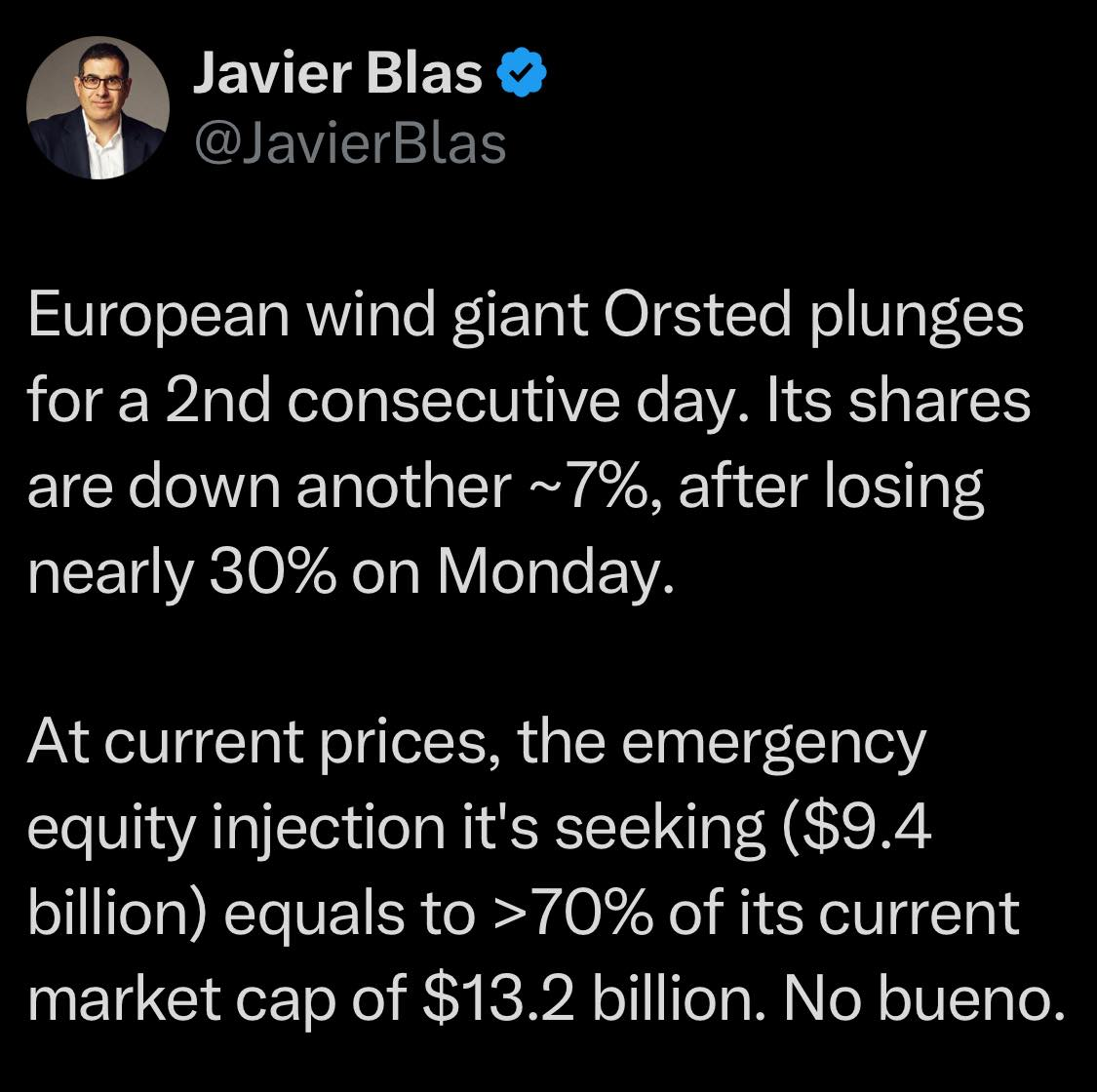

Ørsted’s stock price plummeted on Monday following the announcement of a $9.4 billion rights issue to fund the Sunrise Wind project. The share price has remained depressed (chart below).

Also, although Ørsted attributes its financial woes to the change in US policies, it’s apparent in the second chart (5 year trend) that the decline in Ørsted’s valuation has been ongoing since 2021.

In March, Fitch downgraded Ørsted’s rating to BBB from BBB+, and its subordinated rating to BB+ from BBB-. Further downgrades would seem to be a distinct possibility.

Meanwhile, decommissioning financing for the 3 Ørsted projects under construction in the US Atlantic is far from assured:

According to Ørsted, almost 70% of the turbines are installed at Revolution Wind and the first foundations have been installed at Sunrise Wind. South Fork Wind, 12 turbines and an offshore substation, is complete.

Given Ørsted’s strained finances, will BOEM now opt to require decommissioning assurance as provided for in 30 CFR § 585.517?

Ørsted’s situation is atypical in that the Danish government owns a majority (50.1%) stake in the company and Equinor, which is 2/3 Norwegian govt owned, holds a 9.8% stake. How will government ownership factor into BOEM decisions regarding decommissioning assurance? Note that Norwegian govt lobbying may have been one of the factors influencing the decision to allow the resumption of construction on Equinor’s Empire Wind project.

Meanwhile, two Danish opposition parties are calling for the state to relinquish its ownership stake in Ørsted.

Posted in decommissioning, Offshore Wind, Regulation, tagged decommissioning, financial assurance, Offshore Wind, US Dept. of the Interior, Vineyard Wind on August 11, 2025| Leave a Comment »

The Dept. of the Interior is reviewing offshore wind regulations including “the Renewable Energy Modernization Rule, as well as financial assurance requirements and decommissioning cost estimates for offshore wind projects…”

Concerns about offshore wind financial assurance were first raised on this blog in response to a precedent setting waiver of the “pay as you build” requirement. Vineyard Wind was authorized to defer providing the full amount of required decommissioning financial assurance until year 15 of actual operations. The waiver request, which had been denied in 2017, was resubmitted in 2021 and approved. This questionable decision was consistent with the administration’s enthusiastic promotion of accelerated offshore wind development.

BOEM’s streamlining rule codified the deferred financial assurance option. The rule authorizes the transfer of decommissioning risks from developers to taxpayers and consumers by (1) not requiring any additional supplemental financial assurance at the Construction and Operations Plan (COP) approval stage, (2) not requiring supplemental assurance at the installation stage, and (3) providing for incremental supplemental assurance post-installation (e.g. for Vineyard Wind, the full amount is not due until 15 years after installation). See the rule’s previous and current language in the table below (emphasis added).

30 CFR 585.516 – What are the financial assurance requirements for each stage of my commercial lease?

| financial assurance required before BOEM will: | language prior to 4/24/2024 “modernization” rule | current language |

| Approve your COP | A supplemental bond or other financial assurance, in an amount determined by BOEM based on the complexity, number, and location of all facilities involved in your planned activities and commercial operation. The supplemental financial assurance requirement is in addition to your lease-specific bond and, if applicable, the previous supplement associated with SAP approval. | There is no supplemental bond requirement at the COP approval stage. |

| Allow you to install facilities approved in your COP | A decommissioning bond or other financial assurance, in an amount determined by BOEM based on anticipated decommissioning costs. BOEM will allow you to provide your financial assurance for decommissioning in accordance with the number of facilities installed or being installed. BOEM must approve the schedule for providing the appropriate financial assurance coverage. | A supplemental bond or other authorized financial assurance in an amount determined by BOEM based on anticipated decommissioning costs of the proposed facilities. If you propose to incrementally fund your financial assurance instrument, BOEM must approve the schedule for providing the appropriate financial assurance. |

The current financial assurance language is fuzzy enough that BOEM could deny deferred funding requests and require full financial assurance at the time facilities are installed. However, revising the language to clearly require that assurance be fully demonstrated prior to installation would provide clarity and eliminate the deferral option going forward.

The more difficult challenge may be adjusting financial assurance requirements for the projects already under construction. It’s also important to ensure that parent corporations are not shielded from decommissioning and other liability risks.