(b) LEASE SALE 257 REINSTATEMENT.— (1) ACCEPTANCE OF BIDS.—Not later 30 days after the date of enactment of this Act, the Secretary shall, without modification or delay— (A) accept the highest valid bid for each tract or bidding unit of Lease Sale 257 for which a valid bid was received on November 17, 2021; and (B) provide the appropriate lease form to the winning bidder to execute and return.

Foremost energy experts like Daniel Yergin understand that oil and gas will be critical to our economy and security for decades, and that offshore production is an important component of our energy supply chain. Unfortunately, our massive outer continental shelf has, from an oil and gas standpoint, been effectively reduced to the central and western GoM.

Opportunities in the GoM are being seriously constrained by the extended pause in leasing. A lease sale has not been held for 615 days, the longest US offshore leasing gap since the 1950’s.

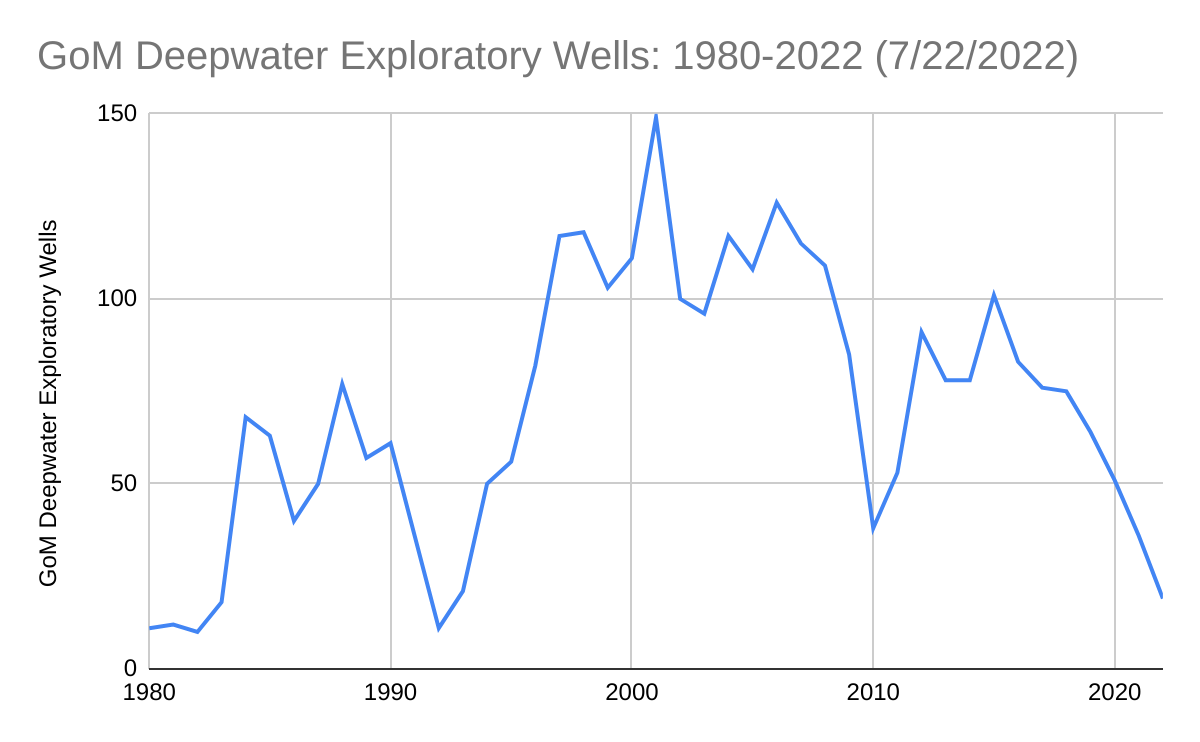

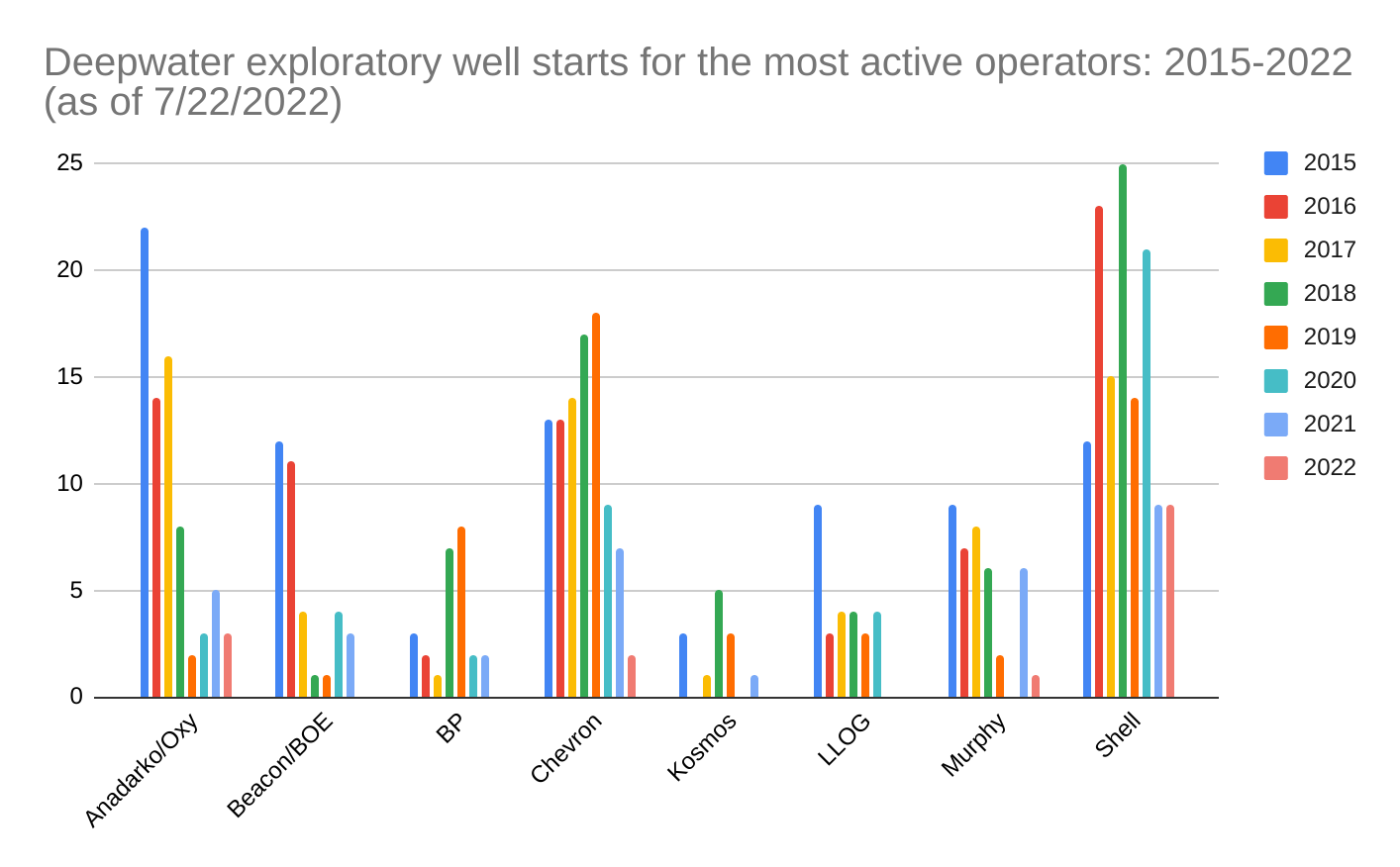

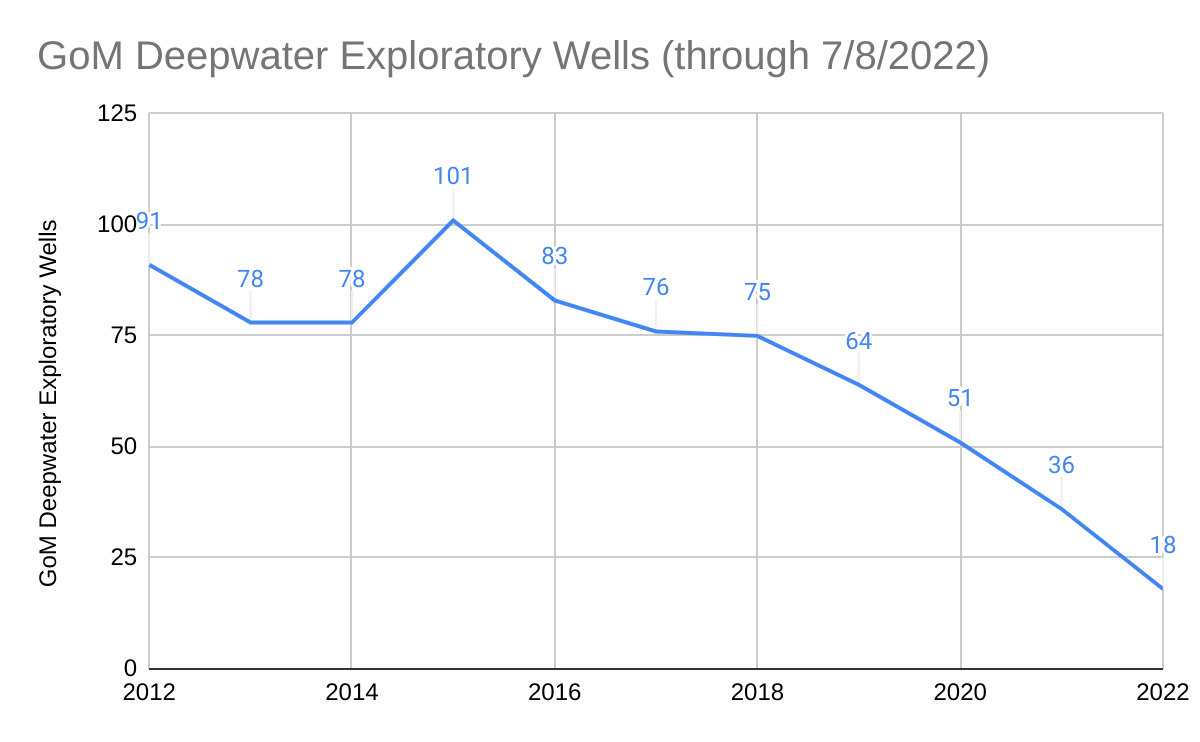

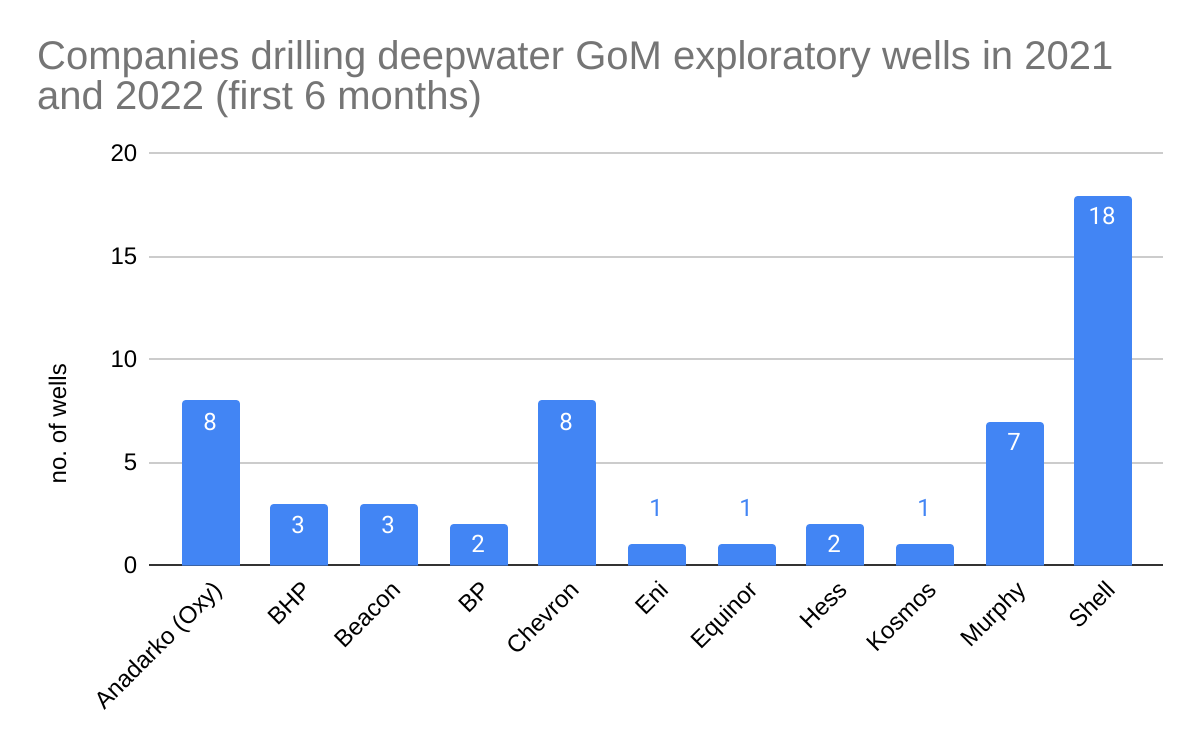

Reserve replacement and sustained production are dependent on exploration. The charts below illustrate the decline in GoM exploratory drilling and the reduced activity by some of the more important operating companies.

Per BSEE data, the number of exploratory well starts averaged only 3/month for the last 18 months (chart 2). This level of activity is the lowest since the early days of deepwater operations (chart 1). There was even more drilling during the post-Macondo moratorium (2010-2011).

ConocoPhillips and Exxon have not drilled a GoM exploratory well since 2016 and 2018 respectively. Activity by other operators has also declined significantly (chart 3). BP has not spudded an exploratory well since Sept. 2021.

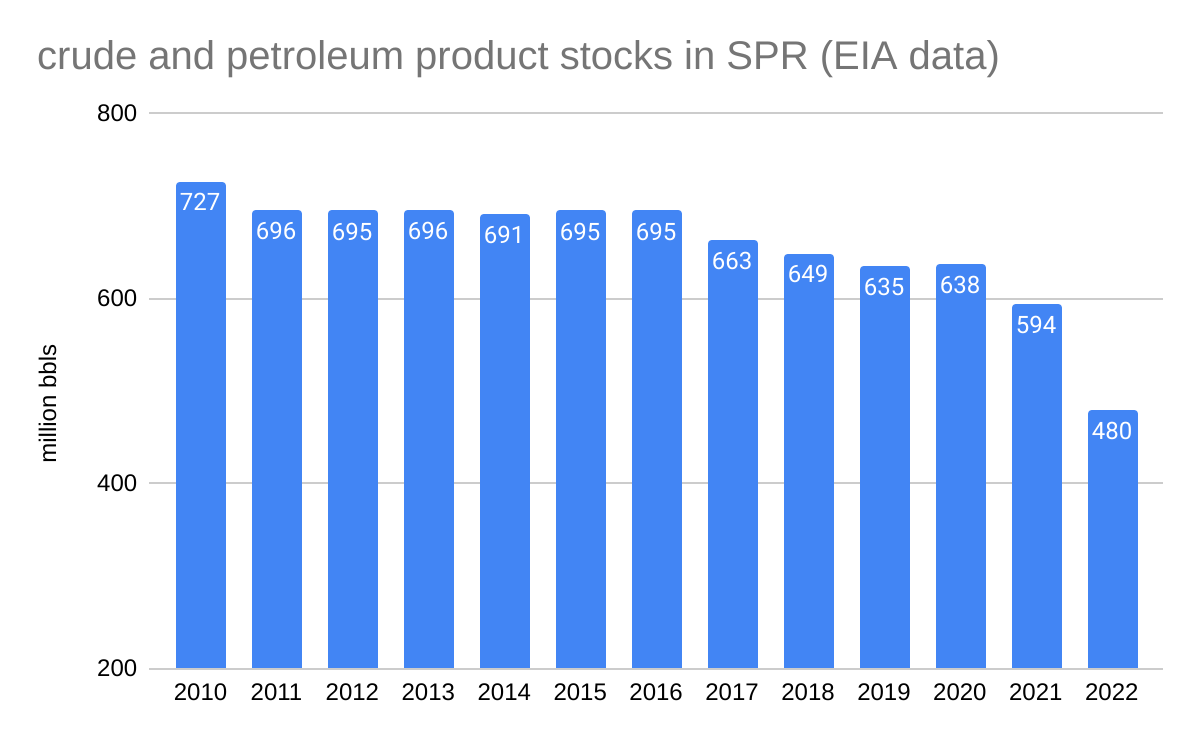

…that the SPR legislation authorized the sale of large volumes of oil for the purpose of easing worldwide prices. Per section 151 of the statute, which was passed following the oil embargoes in the 1970’s, the SPR was intended todiminish the vulnerability of the United States to the effects of a severe energy supply interruption.

…that SPR oil could be sold to all entities including Chinese companies that are also buying oil from Russia, the country being boycotted. How absurd is that? (The confirmation of one such transaction is pasted below.)

This blog does not normally cover onshore leasing; pontificating about offshore issues is challenging enough😉. However, Randall Luthi – the former head of the MMS (and thus the US offshore program) – is now dealing with similar issues to those being experienced in the offshore sector.

“The bad news is the sale was 18 months late, was approximately 75% smaller than originally planned, had a huge number of state director deferrals, and offered many less-than-desirable leases,” testified Randall Luthi, who serves as chief energy advisor to Gov. Mark Gordon. “In summary, it was a long-awaited, but paltry sale.”

According to Luthi, the federal government controls approximately 67% of Wyoming’s mineral estate, and nearly 50% of its surface.

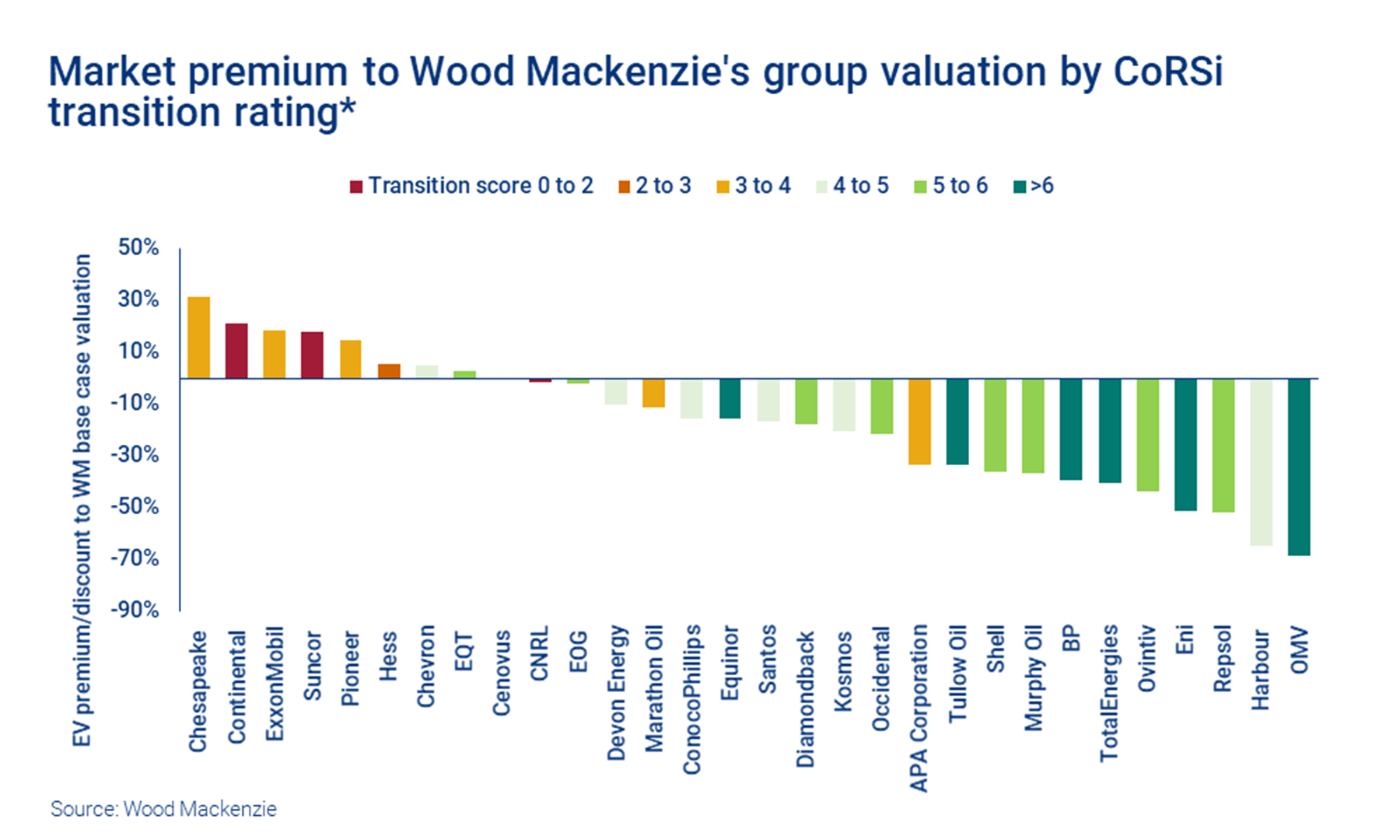

Per Wood Mackenzie, companies with low transition scores (i.e. the purer oil and gas plays) command higher valuations. I’d like to see the scores for other US independents.

“First, investors piled into the pure play oil and gas producers that are most leveraged to oil prices, much as they would in any upcycle. US independents led the sector rise through early June before the oil price and shares fell back over the last month.“

“Euro Majors are also reaping the earnings and cash flow boom. Share price performance has been strong relative to the wider stock market, but most have lagged their US peers. US Majors have long commanded a premium rating to their European counterparts, partly a function of the relatively high rating of the US stock market. The gap though has widened.”

Given the differences in our views on energy policy, particularly with regard to oil and gas, this WP opinion piece is pretty reasonable. The Post acknowledges the continued need for oil and gas, and the importance of domestic production. That said, two statements in the paragraph pasted below warrant immediate comment.

“In reality, neither argument is convincing. The Biden administration’s proposal — which opens the door to up to 11 potential lease sales, 10 in the Gulf of Mexico and one off the coast of Alaska — would have little impact on current energy prices. It would take between five and 10 years to produce oil after a new offshore lease issuance, according to the Interior Department, while more than three-quarters of already-leased offshore federal waters are not in production.”

The purpose of the 5 year leasing plan is to minimize future energy supply and security risks, not to reduce current prices. However, acknowledgement of the importance of offshore production and support for regular lease sales could influence market psychology.

The old and tired arguments about non-producing leases have been frequently addressed on this blog. When you purchase leases, you are not buying oil and gas. You are buying only the opportunity, for a limited period of time, to explore for these commodities. The current percentage of producing leases is actually rather high by historical standards. For more on this topic, see this and this.

In particular, the Energy and Interior Secretaries would benefit from a visit to a deepwater production facility. They would no doubt be impressed and would be better able to make informed decisions affecting US offshore leasing, exploration, and development.

The offshore workers would be respectful and would welcome the opportunity to discuss the technology, safety precautions, and environmental protection measures.

My involvement with Ohmsett dates back to the 1970s when EPA operated the facility and I was on the Ohmsett Interagency Technical Committee. The facility fell into disrepair in the late 1980s. Thanks largely to the vision and initiative of my Minerals Management Service (MMS) colleague Ed Tennyson and the enactment of the Oil Pollution Act of 1990, the MMS began restoring the facility in 1990 and resumed testing activities in 1992. Senator Frank Lautenberg (NJ) and a host of dignitaries participated in the grand reopening event.

“The (worldwide) drop in reserves is driven by the 30 billion barrels of oil produced last year, plus a significant reduction in undiscovered resources, to the tune of 120 billion barrels. The US offshore sector has contributed the largest total to that drop, where 20 billion barrels of oil will remain in the ground, largely thanks to leasing bans on federal land.“

The decline in reserves should come as no surprise to those who follow the US offshore sector. Note the sharp decline in exploratory drilling in the (updated chart below) and the calls for action on this blog a year ago and more recently.

The OCS oil and gas program requires a sustained, consistent commitment by government and industry. Such a consistent commitment, even though required by legislation, is difficult to achieve in our political system, .

The commitment by the oil and gas industry has also been uneven and in some cases disappointing. BOE continues to be troubled by the reduction in exploration by some companies and the decision by others, including leading US companies with a long history of Gulf of Mexico operations, to exit the US offshore sector completely (see the chart below). The exploration decline began before the leasing shutdown (now 600 days in duration). Inconsistent signals from the Federal government and corporate directors, market considerations, and competing investment opportunities are major factors, but there are no doubt other considerations. Constructive dialogue to address these issues is badly needed.