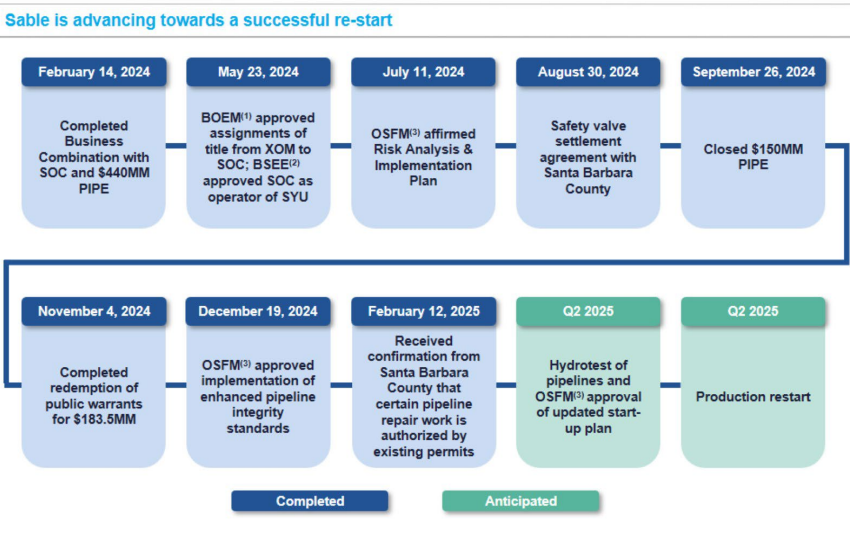

Attached is a recent Sable Offshore presentation for investors. Notably, Sable is now projecting to resume Santa Ynez Unit production in Q2 2025 (see slide below). John Smith thinks this is unrealistic, and I have to agree.

It’s tough for an offshore producer to succeed in California, but Sable is making a strong effort. Exxon must agree, because they have extended Sable’s first production deadline to 3/1/2026, which reflects a more plausible Q1 2026 restart. Additional extensions seem likely if necessary given that Exxon’s other options aren’t very attractive.

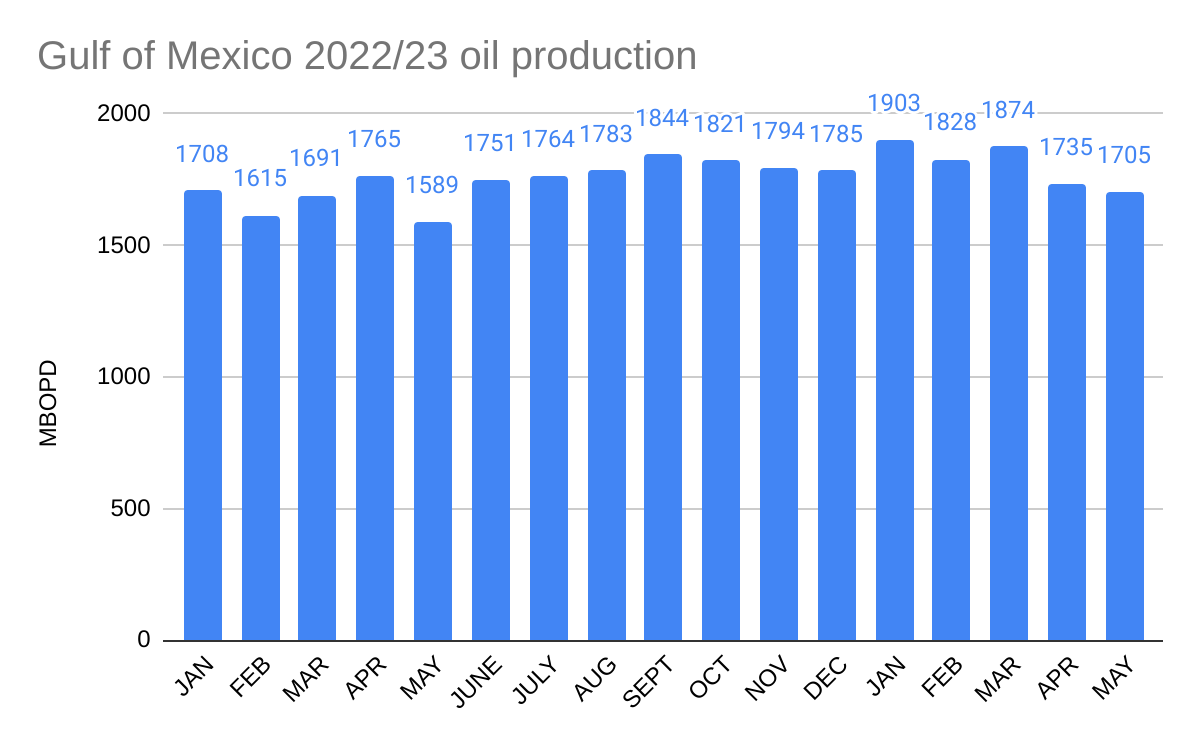

Gulf of Mexico 2023 oil production has dipped over the past 2 months, and is down 10% since January.

2023 production is reasonably well aligned with the EIA forecast which shows new production being offset by declines in existing fields.

Last year, BOEM forecast that production would average 2.0 million bopd in 2023. That forecast was justification for curtailing BOEM’s Proposed 5 Year Leasing Program. For the first time in the history of the OCS program, the primary concern of the program managers was that production might be too high for too long! This stunning quote from the 5 year leasing plan explains why so few lease sales were proposed:

“BOEM’s short-term (20-year) production forecast for existing leases shows steady growth from 2022 through 2024 and declining thereafter (see Section 5.2.1). The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“

The 2019 annual production record remains intact at 1.897 million bopd, but could be exceeded in 2023 if (1) projected deepwater startups are on schedule, (2) prices remain above $70/bbl, (3) depletion is effectively managed, and (4) the hurricane season is again favorable

The “energy transition” will not affect oil and gas demand for the foreseeable future, more nuclear power plants are not being built, and shale has its limitations. We better not neglect what is left of the OCS oil and gas program.

U.S. crude oil production in the forecast averages 12.0 million b/d in 2022, up 0.8 million b/d from 2021. We forecast production to increase another 0.9 million b/d in 2023 to average almost 13.0 million b/d, surpassing the previous annual average record of 12.3 million b/d set in 2019.

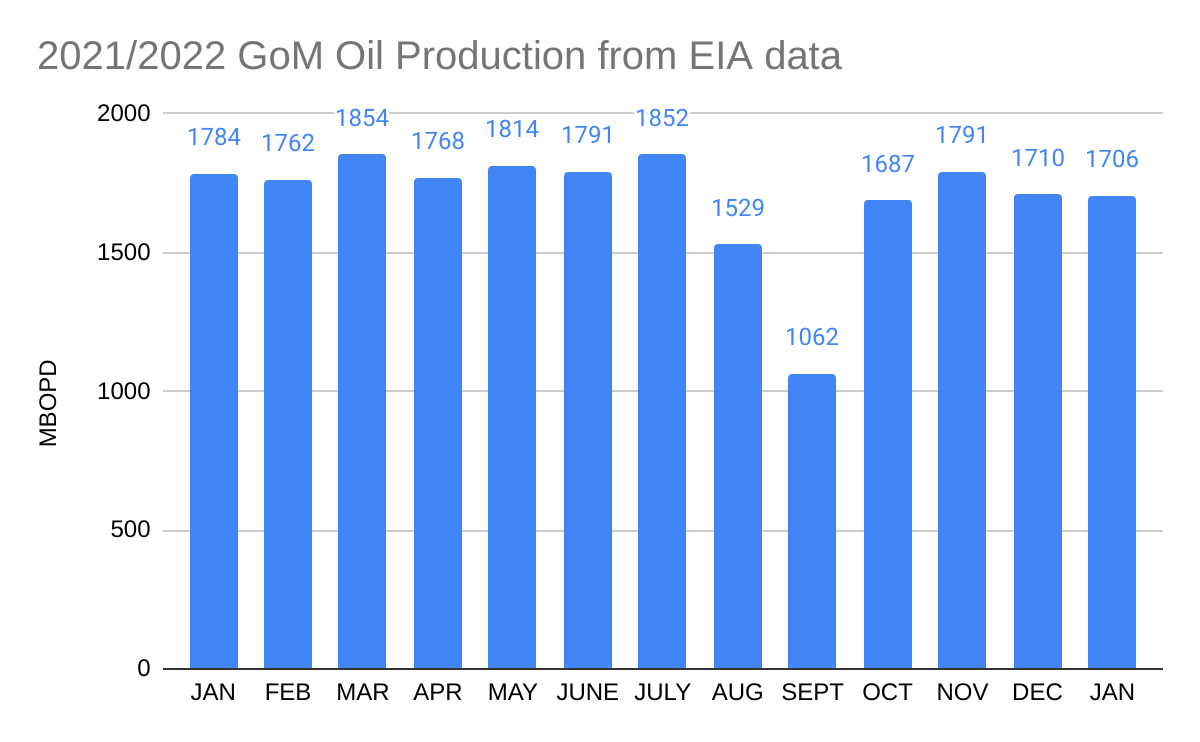

The short-term forecast doesn’t say how much of that production will come from the Gulf of Mexico. Last year, EIA forecast 2022 Gulf production to average 1.75 BOPD which seems about right based on the the most recent production data.