Orsted has a lease contract, and no matter where you stand on offshore wind, you have to have a compelling case to halt a project that is in the advanced stages of development.

Attached is the supplemental complaint in the lawsuit Revolution Wind, LLC v. United States Department of the Interior, Case No. 1:25-cv-02999-RCL, filed in the U.S. District Court for the District of Columbia.

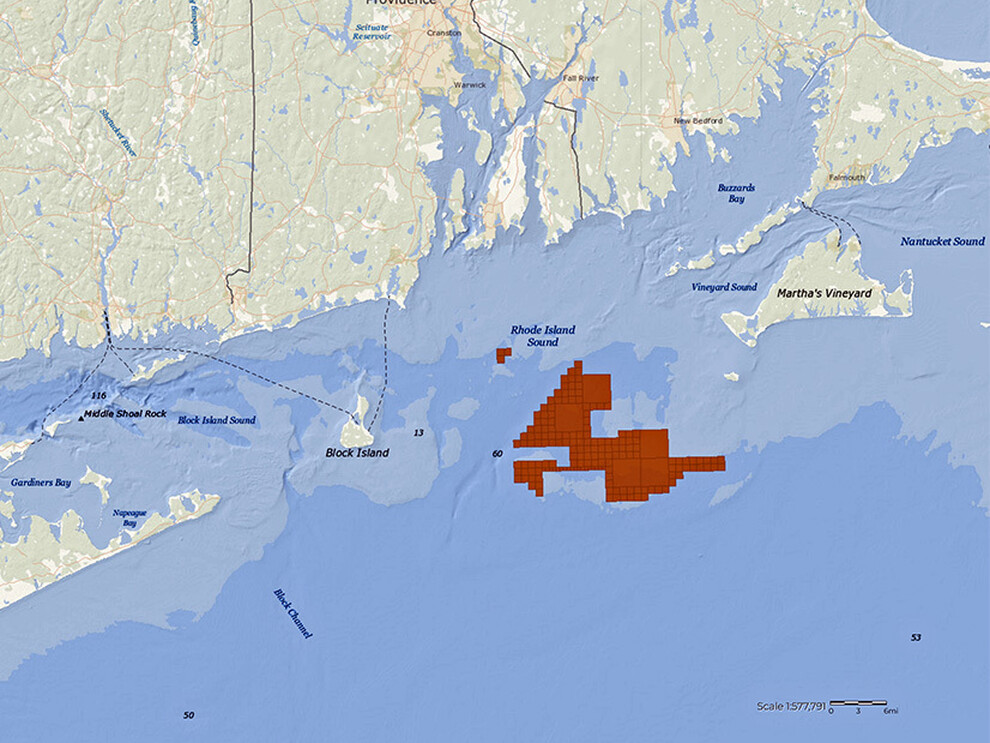

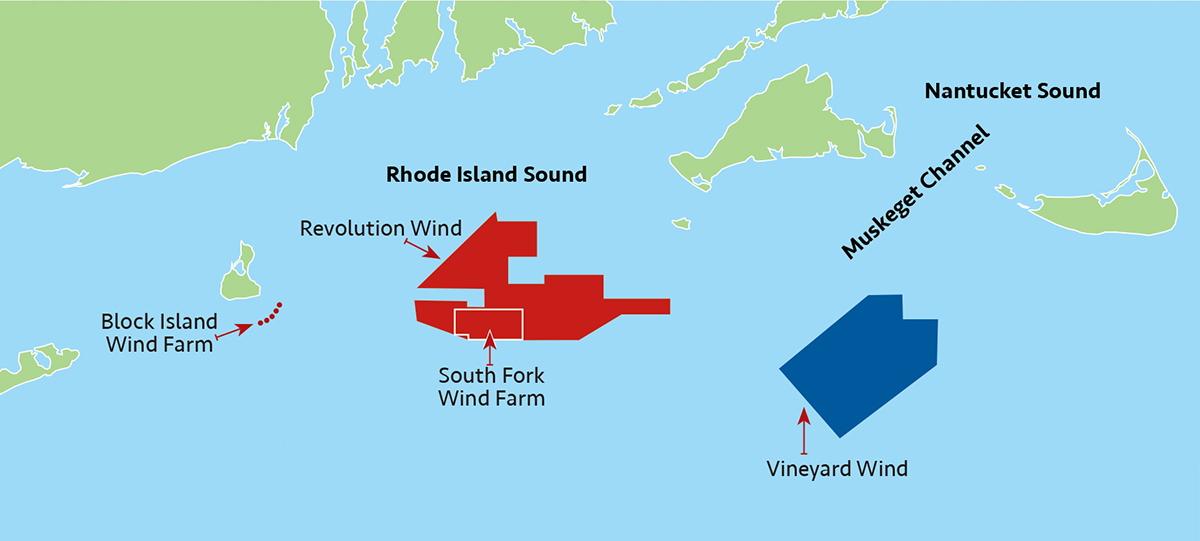

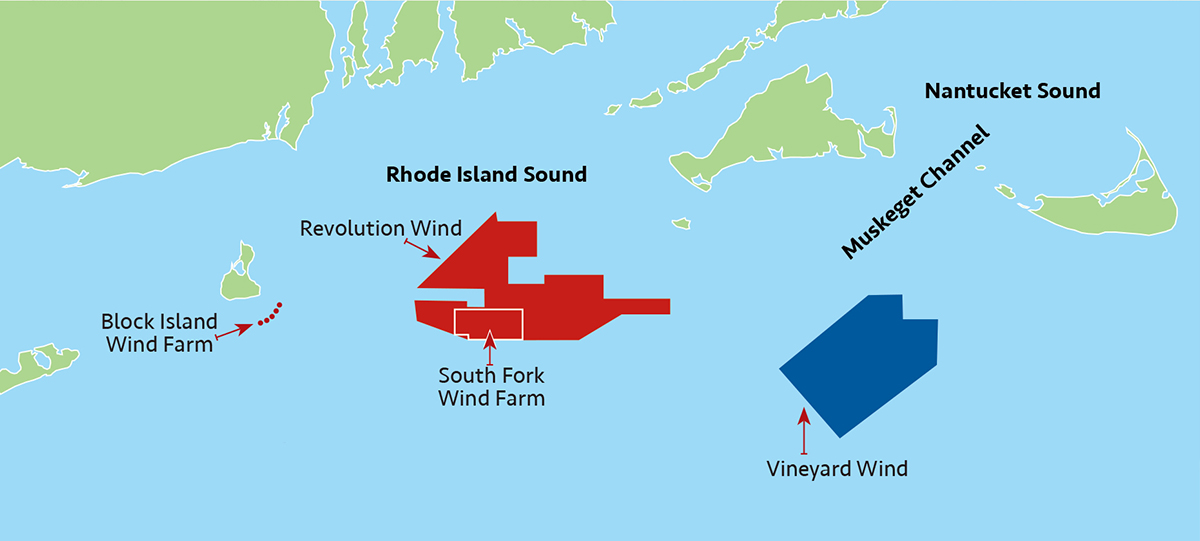

Judge Royce Lamberth granted an injunction allowing Orsted to resume work on the Revolution Wind project. BOEM halted work on the project one month ago.

Gov. Newsom and Danish Foreign Minister Lars Løkke Rasmussen

As is the case for most MOUs, the attached 8/22/2025 agreement between California and Denmark is long on promotion and short on substance. No funds are obligated and there are no work commitments.

The MOU made sense for Gov. Newsom in that he strengthened his green credentials by aligning with the country that is the spiritual leader for climate activists.

The benefits for Denmark were unclear, but the risks should have been apparent. The White House is fundamentally opposed to the climate and energy objectives identified in the MOU. Ørsted (50.1% govt owned) and other Danish business interests are very much dependent on decisions made by the US Federal govt.

Work on Ørsted’s Revolution Wind project has been halted by Interior Secretary Burgum. His decision is being challenged in court, but no matter what the outcome, offshore wind development will be difficult for Ørsted and other foreign companies going forward. The Secretary has broad regulatory authority under the OCS Lands Act, under which there is no such thing as “a fully permitted project.”

Meanwhile, California’s green status has taken a hit with the passage of S 237, which pragmatically authorizes new onshore drilling.

Lastly, as the chart below illustrates, Orsted’s problems didn’t begin in 2025.

Equinor (2/3 Norwegian govt owned) is increasing its position in Ørsted (50.1% Danish govt owned). Given the ownership structure, public money is at risk for both countries.

The comments below are from a DN Norway article. They were made by CEO Torgrim Reitan after Equinor announced that the company will contribute NOK 10 billion (USD 1 billion) in Ørsted’s special share offering.

“We want a closer partnership with Ørsted. We are two leading companies in offshore wind, and we believe a closer collaboration could create significant value for both Ørsted’s and our own shareholders.”

“This industry is now going through its first real crisis. That makes it quite clear what’s needed. We know a lot about this from oil and gas. What often happens in such times is consolidation.”

“We want a closer partnership with Ørsted. We are two leading companies in offshore wind, and we believe a closer collaboration could create significant value for both Ørsted’s and our own shareholders.”

“In recent weeks, we’ve had conversations with Ørsted management, and we’ve also had conversations with the Danish state. But the discussions have primarily been with Ørsted.”

“Ørsted is in a difficult situation right now. For us, as an industrial and long-term owner, it’s important to be supportive and helpful in such a situation. That’s why we’re putting in nearly a billion dollars.”

“This is a difficult decision, because clearly a lot of equity capital needs to be raised, but we have a fundamental belief in the industry, and also in the company. Ørsted’s underlying portfolio is a strong one.”

“Going forward, this will increase our debt ratio somewhat—maybe by about two percentage points. But we’re starting from a very low debt ratio. So we can manage this within our financial framework. As for capital distribution in 2026 and beyond, we will remain competitive.”

Meanwhile, Equinor is the only major oil company that remains invested in US offshore wind energy. Equinor’s Empire Wind project continues to be highly divisive.

“Ørsted is evaluating all options to resolve the matter expeditiously. This includes engagement with relevant permitting agencies for any necessary clarification or resolution as well as through potential legal proceedings, with the aim being to proceed with continued project construction towards COD in the second half of 2026.”

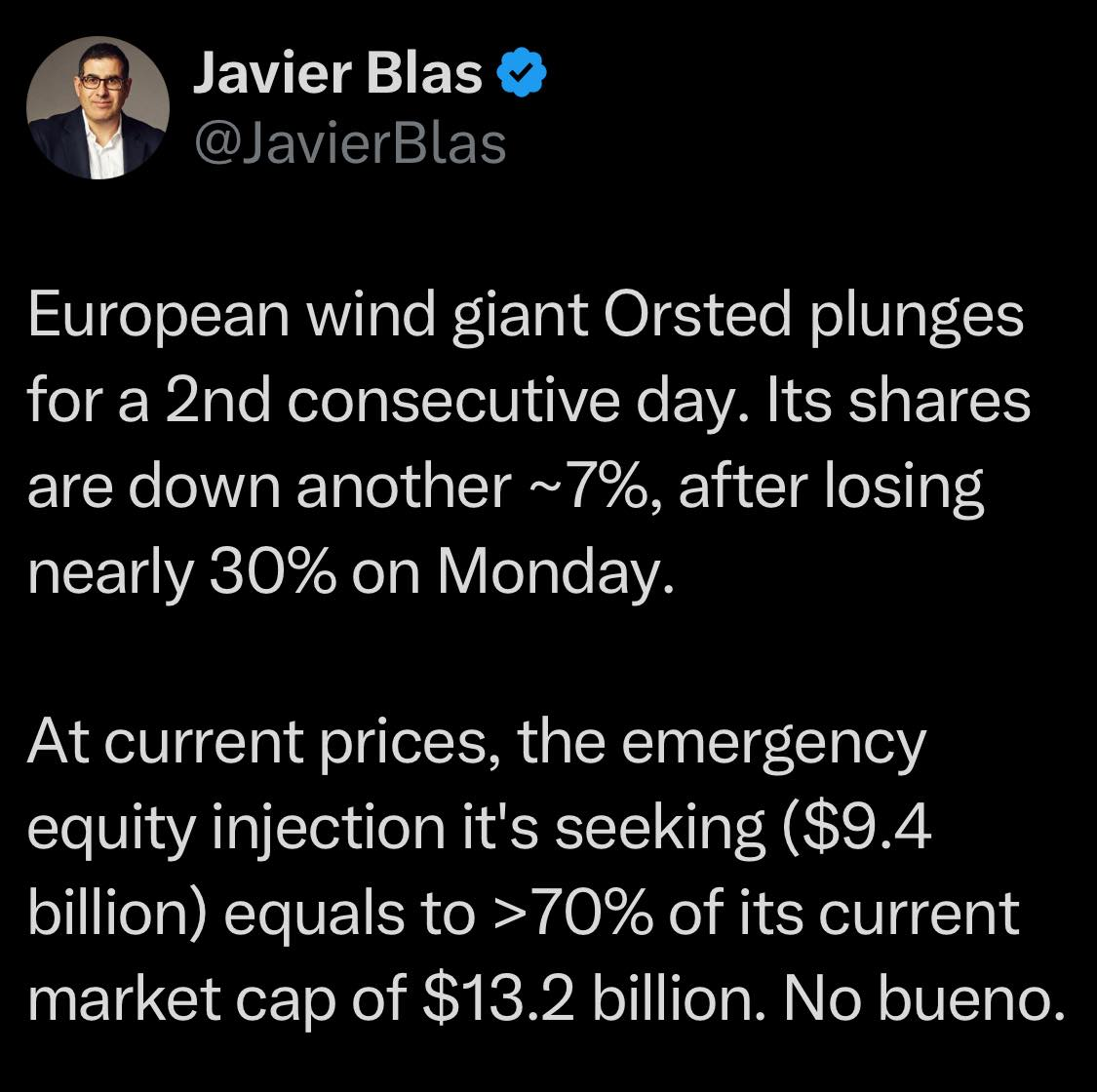

Following the announced $9 billion rights offering to shore up its finances, Orsted’s long-term issuer credit rating has been downgraded to BBB- by S&P, just one step above junk.

Ørsted’s stock price plummeted on Monday following the announcement of a $9.4 billion rights issue to fund the Sunrise Wind project. The share price has remained depressed (chart below).

Also, although Ørsted attributes its financial woes to the change in US policies, it’s apparent in the second chart (5 year trend) that the decline in Ørsted’s valuation has been ongoing since 2021.

In March, Fitch downgraded Ørsted’s rating to BBB from BBB+, and its subordinated rating to BB+ from BBB-. Further downgrades would seem to be a distinct possibility.

Meanwhile, decommissioning financing for the 3 Ørsted projects under construction in the US Atlantic is far from assured:

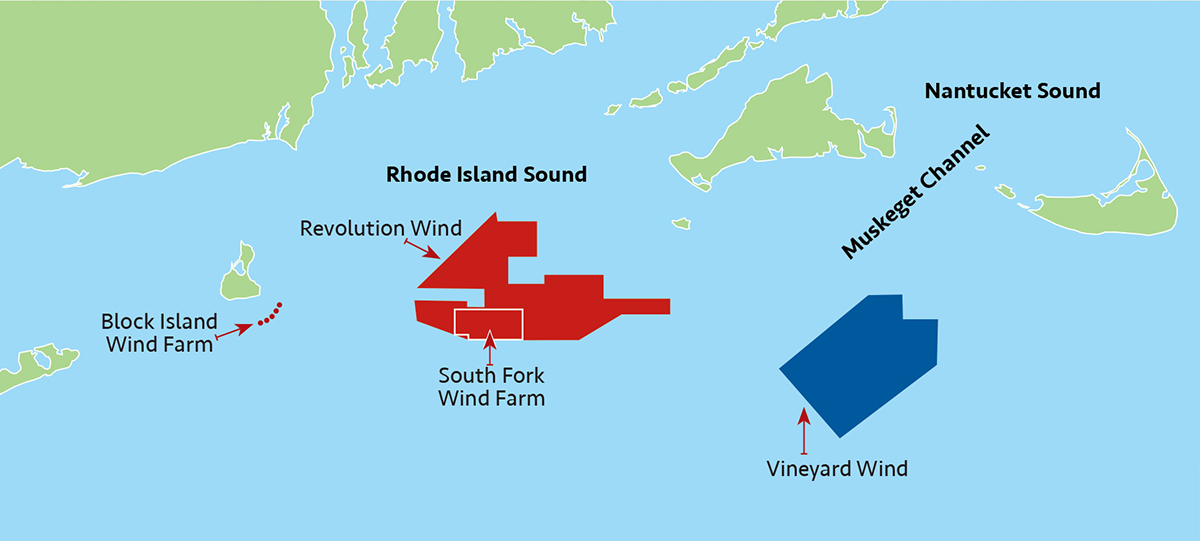

Revolution Wind:As they did for Vineyard Wind, BOEM approved Ørsted’s request to defer full decommissioning financial assurance until 15 years after the beginning of construction (see attached letter). This approval was prior to the Renewable Energy Modernization Rule (effective June 29, 2024), which eliminated the need for such waivers.

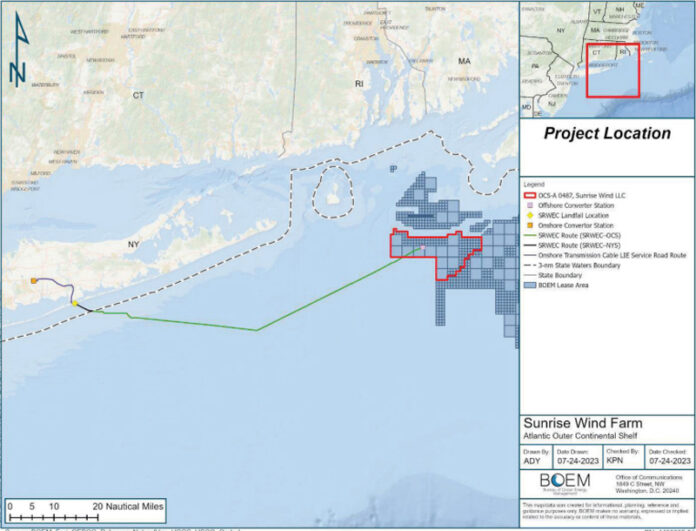

Sunrise Wind: Ørsted is now solely responsible for funding and constructing this project given the company’s failure to find investment partners. Presumably, decommissioning financial assurance was not required given BOEM’s latitude under the so-called “Modernization Rule.”

South Fork Wind: As is the case with Sunrise Wind, BOEM presumably allowed Ørsted to defer financial assurance for decommissioning as permitted by the “Modernization Rule.”

According to Ørsted, almost 70% of the turbines are installed at Revolution Wind and the first foundations have been installed at Sunrise Wind. South Fork Wind, 12 turbines and an offshore substation, is complete.

Given Ørsted’s strained finances, will BOEM now opt to require decommissioning assurance as provided for in 30 CFR § 585.517?

Ørsted’s situation is atypical in that the Danish government owns a majority (50.1%) stake in the company and Equinor, which is 2/3 Norwegian govt owned, holds a 9.8% stake. How will government ownership factor into BOEM decisions regarding decommissioning assurance? Note that Norwegian govt lobbying may have been one of the factors influencing the decision to allow the resumption of construction on Equinor’s Empire Wind project.

Equinor’s investment of over 26 billion kroner in the Danish wind power company Ørsted has so far been a financial disaster – and now it’s going from bad to worse.

“We are very negative about the whole green initiative, as the return on the investments they make is far too low. When they also buy minority stakes in other green companies that we cannot count on, such as Ørsted, it means that we would rather own other oil companies.” Gaute Eie, Eika Kapitalforvaltning

The market has long been concerned that Equinor will throw money at renewable projects with low or no profitability.

In a recent note, Pareto analysts Tom Erik Kristiansen and Olav Haugerud point out that the Ørsted writedown does not bode well for Equinor’s own US projects either. They foresee a writedown of up to $1.1 billion, given that Equinor faces the same type of challenges as Ørsted.

Eie believes there is no reason why Equinor in particular should have a green initiative:

Aker BP is not doing green, Vår Energi is not doing green, and all the big oil companies are going back on this. Then we’ll see if Equinor has the guts to buy even more Ørsted shares, because now it’s 35 percent cheaper. If they do, we’ll have even fewer Equinor shares.

Sissener believes Equinor should rather focus on dividends and concentrate on oil and gas projects.

– We generally stay away from companies where the state is a major owner, because there you have to be so politically correct all the time. What we need are shareholder-friendly board representatives who know how to run a business and maintain control. In a broader perspective, this helps to destroy trust in Norwegian business.