Every deepwater platform installed since Feb. 2018, when Chevron installed its Big Foot tension leg platform (TLP), has been a Floating Production Unit (aka FPU or production semisubmersible). During that period, no new SPARs, FPSOs, or TLPs were installed.

The list (below) of these simpler, safer, greener FPUs has grown by two with the initiation of production at Shenandoah and Salamanca. Note the water depth range from 3725 to 8600 ft.

platform

operator

water depth (ft)

first production

Appomattox

Shell

7400

May 2019

King’s Quay

Murphy

3725

April 2022

Vito

Shell

4050

Feb 2023

Argos

bp

4440

April 2023

Anchor

Chevron

4600

Aug 2024

Whale

Shell

8600

Jan 2025

Shenandoah

Beacon

5840

July 2025

Salamanca

LLOG

6405

Sept 2025

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades is facilitatihg production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded in this post.)

All of the operators note the cost-saving similarities in their FPU designs. For example, Vito and Whale are very much the same despite the 4550′ difference in water depth.

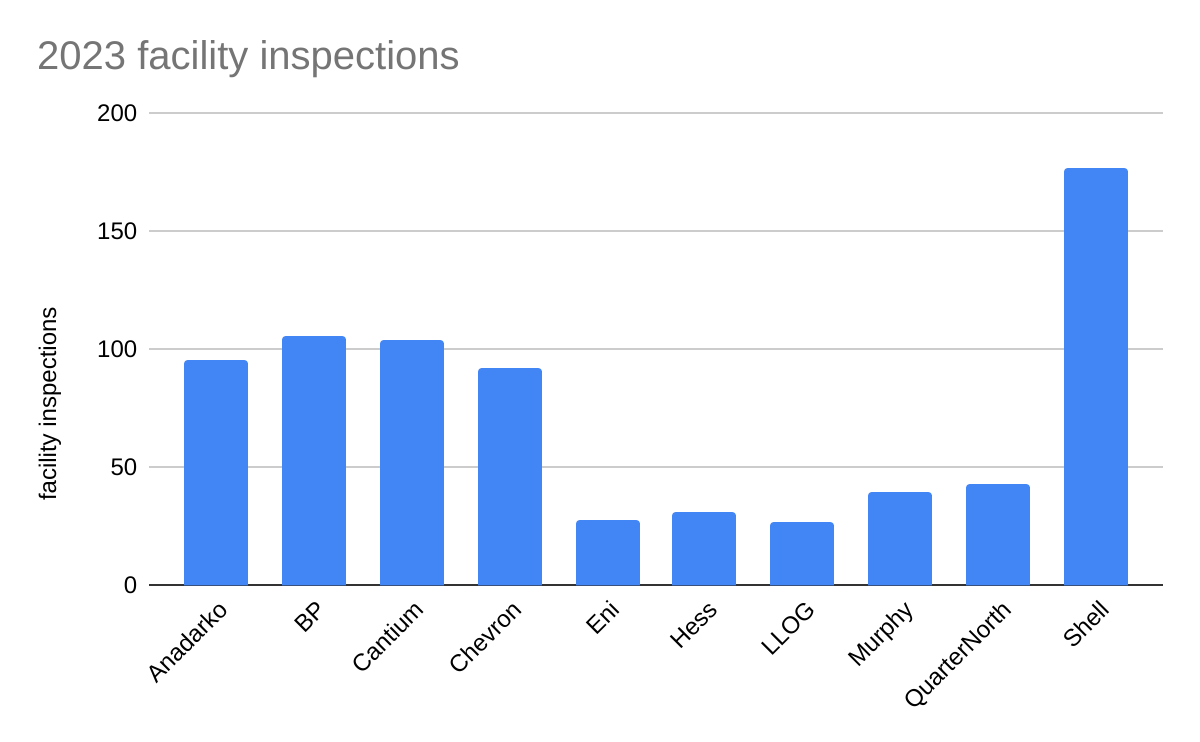

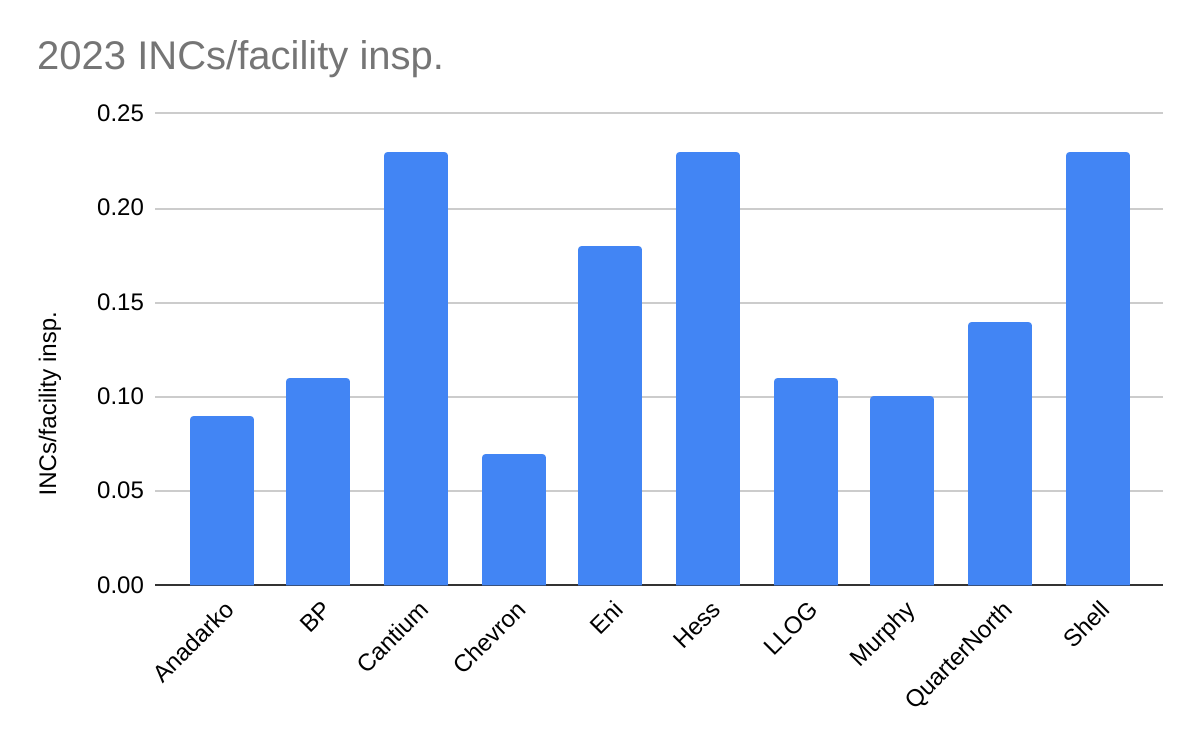

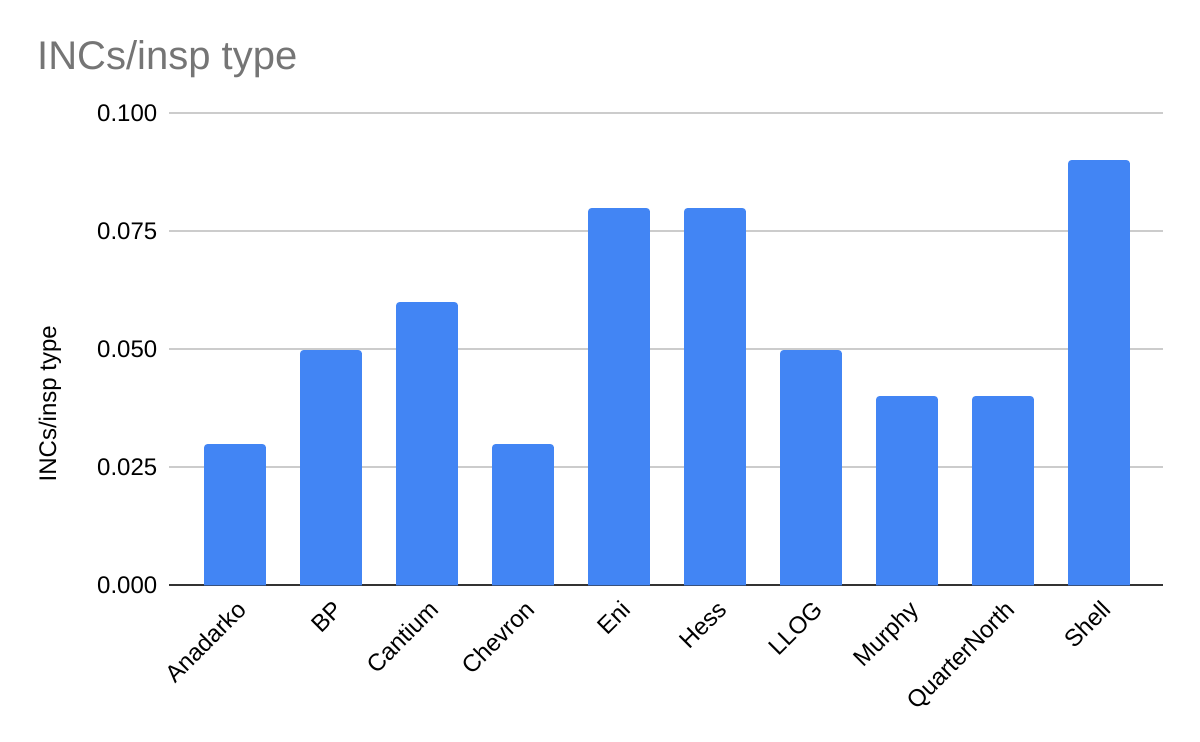

The 2024 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 3 facility inspections (0.33 INCs/facility inspection)

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2024, there were on average 3.4 inspections for every facility inspection.

District investigation reports are more timely and provide additional insights into safety performance. Impressively, Hess had no incidents warranting a District investigation, and was the only ranked operator with this distinction. I will comment more on the District reports in a future post

Chevron’s 2024 compliance record was among the best in the history of the US OCS oil and gas program. Was it the absolute best? Were it not for the FSI INC at a Unocal (Chevron) facility, one could unequivocally assert that it was. Further evaluation of that INC would be helpful. However, details on specific INCs are not publicly available, so the significance of that violation cannot be evaluated.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Chevron

1

0

1

2

117

0.02

311

0.006

BP

2

3

0

5

93

0.05

251

0.02

Anadarko

8

9

1

18

143

0.13

344

0.05

Hess

2

3

0

5

26

0.19

67

0.07

Walter

6

4

1

11

50

0.22

161

0.07

Shell

23

17

5

45

199

0.23

495

0.09

Cantium

24

8

0

32

123

0.26

537

0.06

Murphy

8

9

1

18

70

0.26

191

0.09

Arena

29

28

3

60

189

0.32

803

0.07

Gulf-wide

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2024, there were on average 3.4 inspections for every facility inspection

Not meeting the production facilities requirement to be ranked among the top performers, but nonetheless noteworthy, was the compliance record of BOE Exploration & Production (no relation to the BOE blog 😀). See their impressive inspection results below:

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

BOE

1

1

0

2

21

0.1

48

0.04

Transparency on inspections and incidents is important for a program that is dependent on public confidence. For independent observers to better evaluate industry-wide and company-specific safety performance, publication of the following information should be considered:

quarterly updates of the incident tables, as was once common practice

posting of violation summaries for inspections resulting in the issuance of one or more INCs

Four of the five simpler, safer, greener deepwater platforms featured on this blog are now producing. The 5th platform (Whale) is on location and scheduled to begin production later this year.

platform

operator

first production

King’s Quay

Murphy

April 2022

Vito

Shell

Feb 2023

Argos

bp

April 2023

Anchor

Chevron

Aug 2024

Whale

Shell

late 2024

These platforms are in 4000 to 8600′ of water, are expected to reach peak production rates of 100-150,000 boe/day, and have favorable emissions characteristics on a per barrel basis.

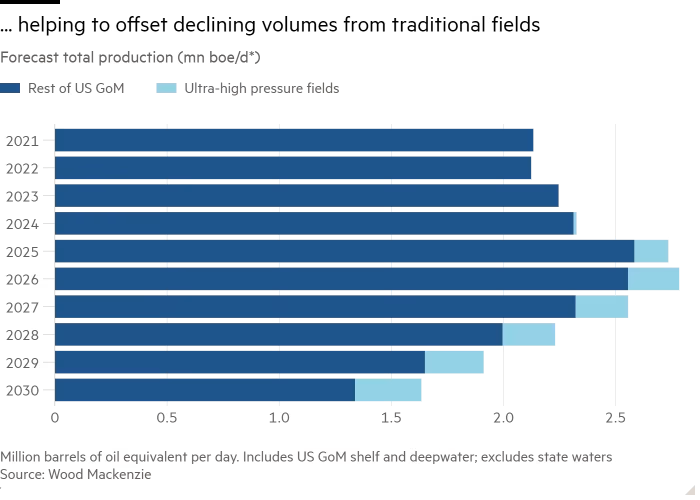

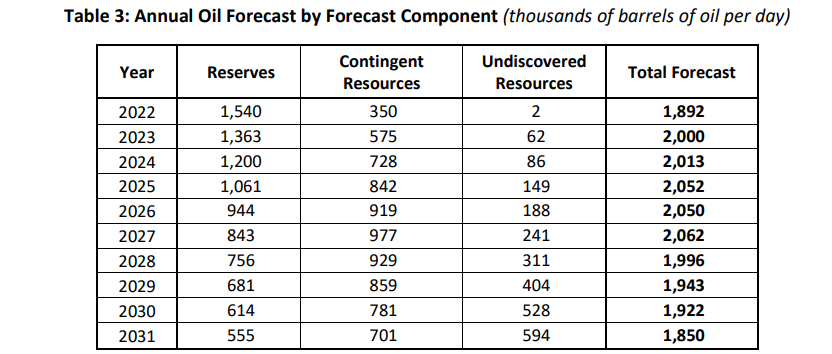

This is all good, but what is next? Will technological advances once again sustain GoM production? The short answer appears to be yes!

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades will facilitate production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded below.)

Chevron’s Anchor is the first deepwater, high-pressure development. Three similar deepwater hub platforms (table below) will begin production over the next 5 years. These host platforms will also facilitate additional production from nearby fields. Each will have production capacities of approximately 100,000 boe/day. Note the long lead times in achieving first production given the technological issues that had to be evaluated and addressed.

platform

operator

discovery date

first production

Kaskida

bp

2006

2029

Sparta

Shell

2012

2028

Shenandoah

Beacon

2009

2025

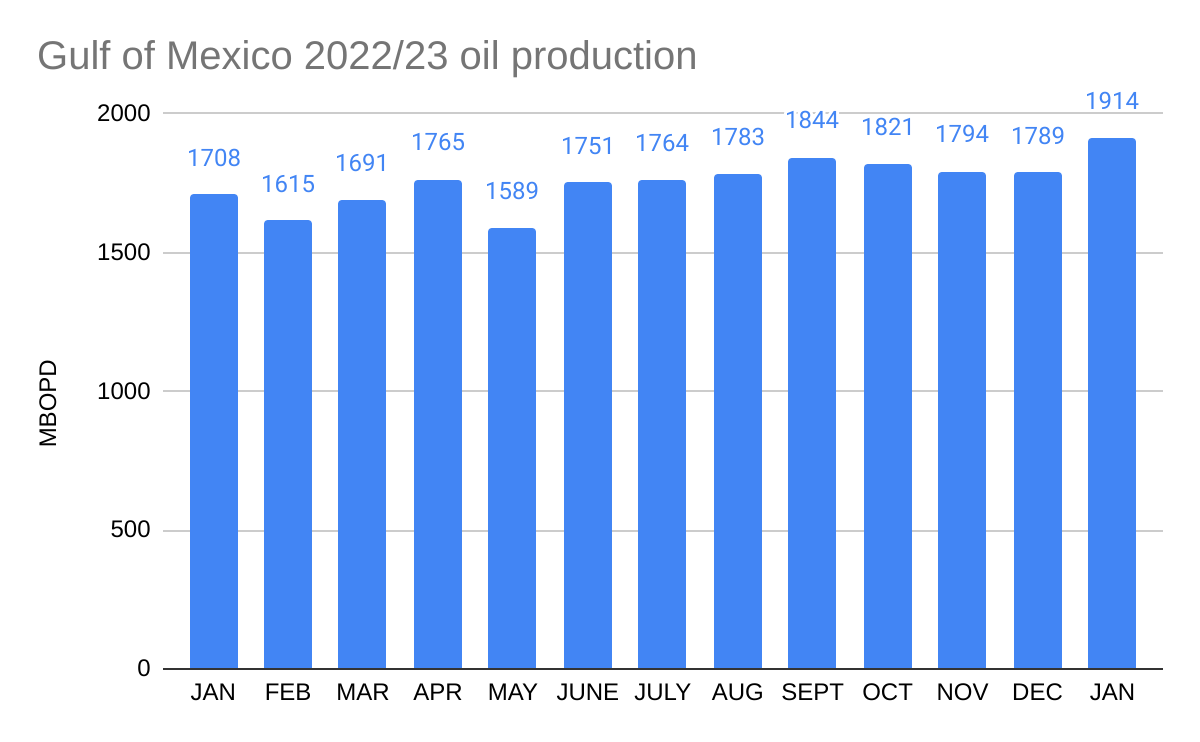

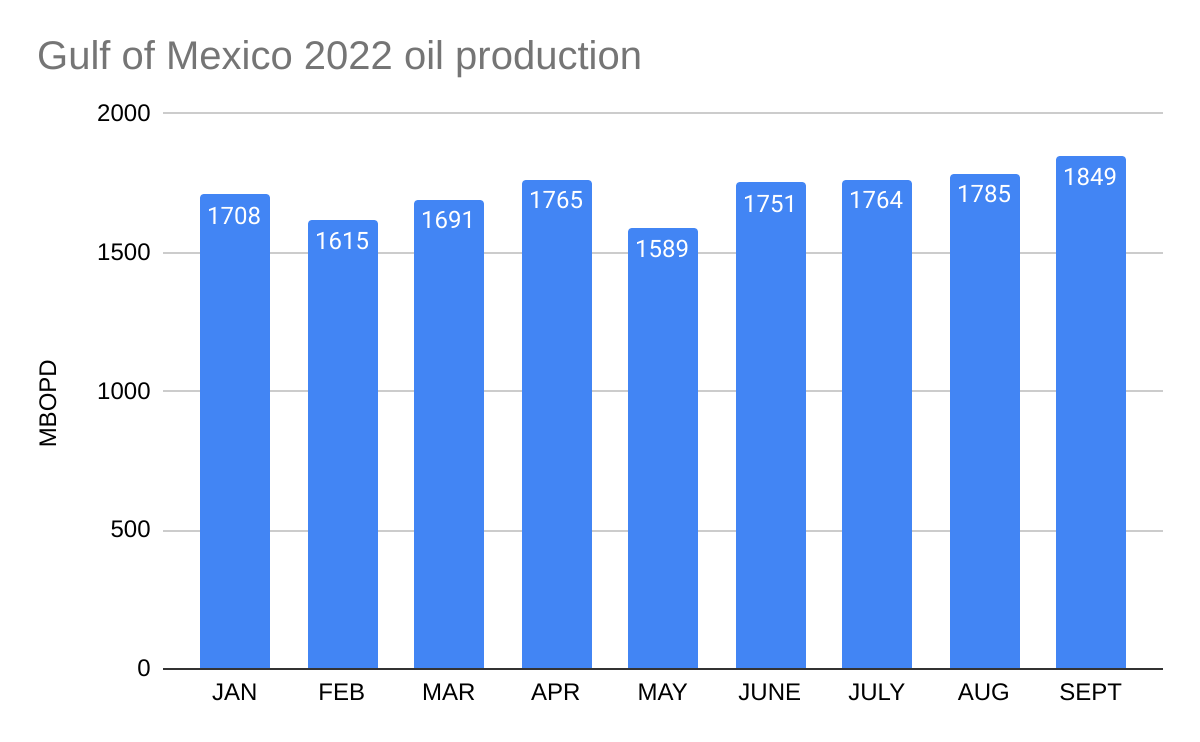

Wood Mackenzie sees these high pressure projects as the key to sustaining GoM production rates. Their projections for 2024 and 2025 seem optimistic based on 2024 YTD data, which adds to the importance of the projected new production.

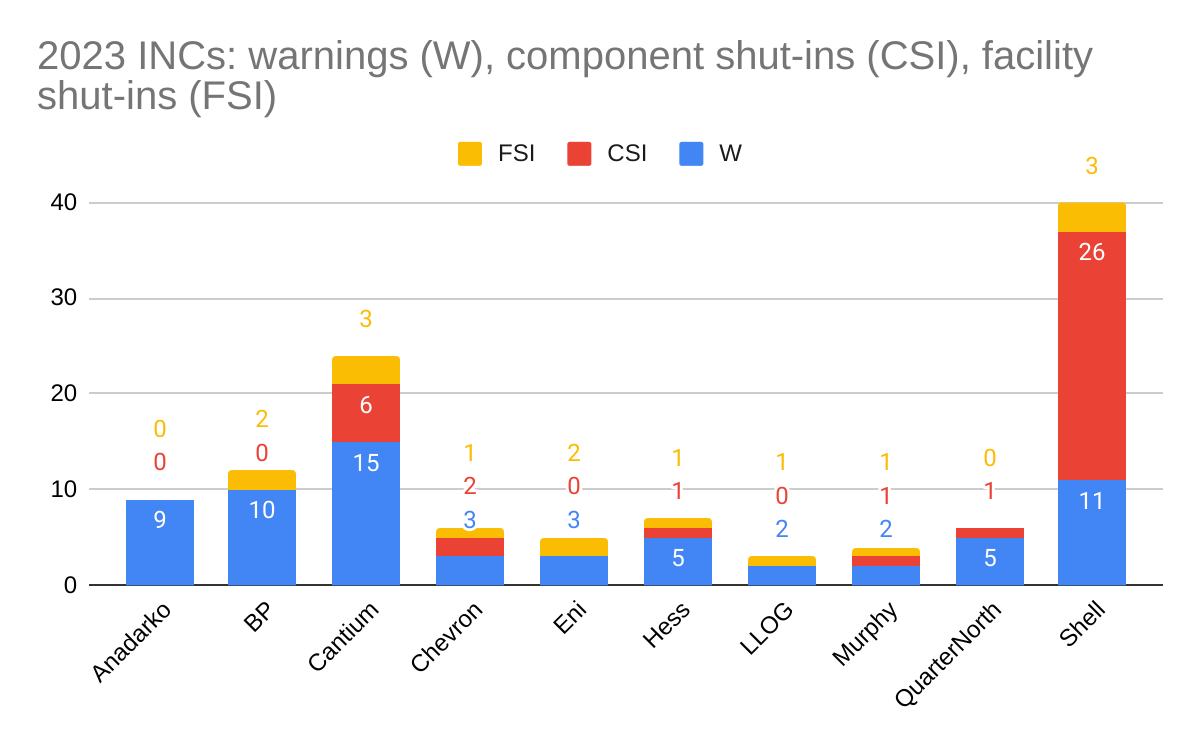

The Honor Roll companies for 2023 (listed alphabetically) are Anadarko, bp, Cantium, Chevron, Eni, Hess, LLOG, Murphy, QuarterNorth, and Shell.

BOE Honor Roll criteria:

Must average <0.3 incidents of noncompliance (INCs) per facility-inspection.

Must average <0.1 INCs per inspection-type. (Note that each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). On average, each facility-inspection included 3.3 types of inspections in 2023. Here is a list of the types of inspections that may be performed.

Must operate at least 3 production platforms and have drilled at least one well (i.e. you need operational activity to demonstrate compliance and safety achievement).

May not have a disqualifying event (e.g. fatal or life-threatening incident, significant fire, major oil spill). Due to the extreme lag in updates to BSEE’s incident tables, district investigations and media reports are used to make this determination.

platforms

2023 well starts

2023 (10 mos.) oil prod. (million bbls)

2023 (10 mos.) gas prod. (bcf)

Anadarko

10

11

66

60

BP

7

11

105

65

Cantium

96

10

5

6

Chevron

8

10

67

39

Eni

3

1

6

13

Hess

3

3

18

36

LLOG

10

7

25

35

Murphy

7

4

42

57

QuarterNorth

9

1

13

23

Shell

20

20

141

140

Also noteworthy:

Zero shut-in violations for Anadarko in 2023

<1 INC for every 10 facility inspections for Anadarko, Chevron, and Murphy

<1 INC for every 20 inspections (all types) for Anadarko, bp, Chevron, LLOG, Murphy, and QuarterNorth

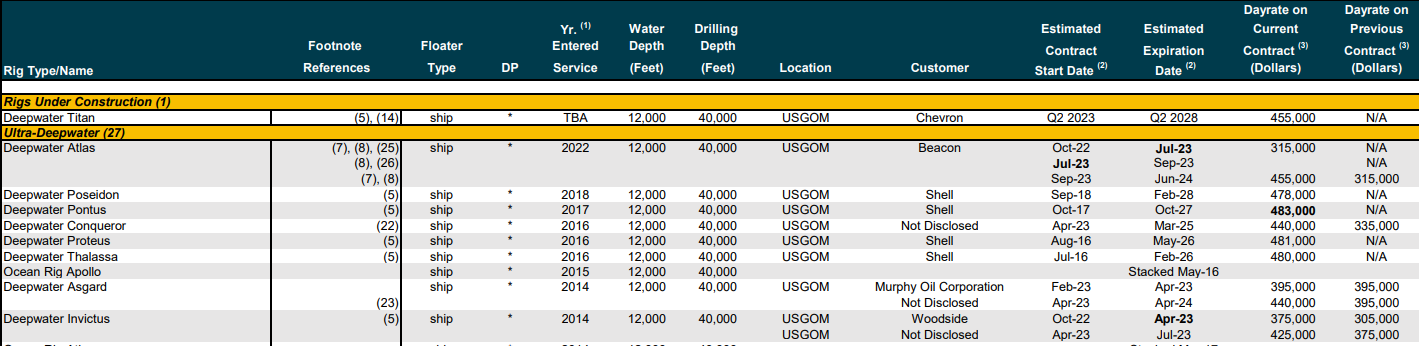

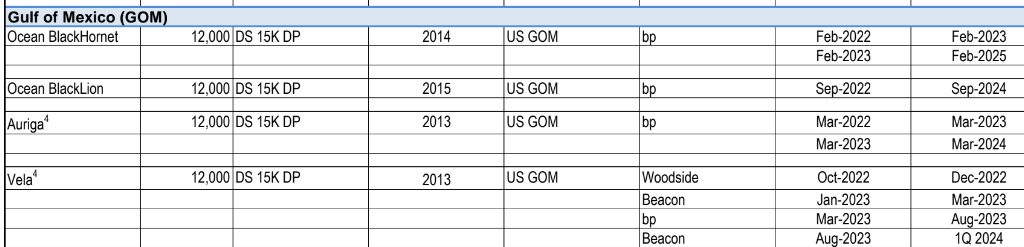

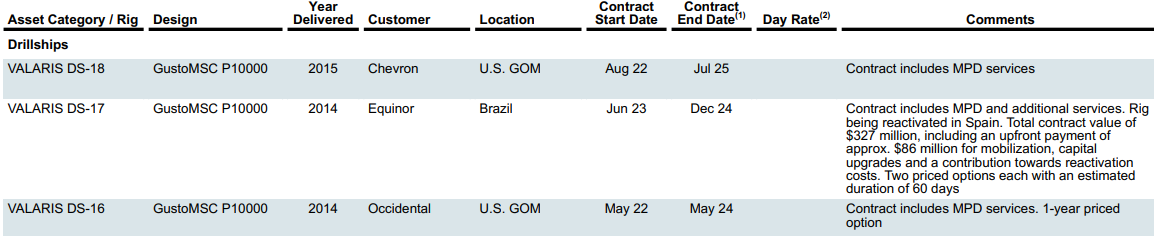

Based on drilling contractor rig activity reports, the table below lists 19 deepwater MODUs under or soon to begin contracts in the GoM. (Further details are pasted at the end of this post.) Per the Valeris report, platform rigs are operating on bp’s Thunder Horse and Mad Dog platforms. Per the BSEE borehole file, Arena and Cantium continue to drill development wells on the GoM shelf.

Prior to the installation of these platforms, the last deepwater platform addition was Shell’s Appomattox in 2018. That gap in deepwater platform installations was the longest since Bullwinkle was installed in 1988.

The 5 new structures will increase the deepwater platform count by 9% from 56 to 61, and in the next few years should account for approximately 1/4 of GoM oil production.

Last year, BOE featured 5 deepwater platforms that were under construction: Shell’s Vito and Whale, Murphy’s King’s Quay, bp’s Argos, and Chevron’s Anchor. These floating production units are noteworthy for their lighter, smaller designs. King’s Quay was the first to produce, beginning last April. The spotlight is now on Vito which began producing today. Vito’s peak production should reach 100,000 boe. The other 3 platforms are expected to begin production this year or next.

“BOEM’s short-term (20-year) production forecast for existing leases shows steady growth from 2022 through 2024 and declining thereafter (see Section 5.2.1). The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“