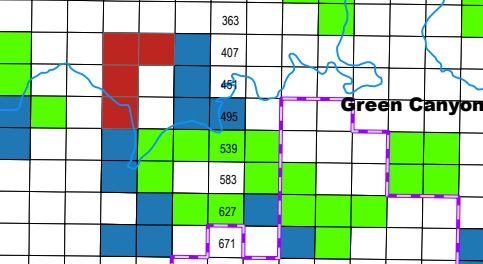

red=blocks receiving bids at BBG2; blue=BBG1 and Sale 261 leases; green=active leases issued prior to Sale 261

Although bidding at Sale BBG2 was rather subdued, Gulf heavyweights BP, Chevron, Shell, and Oxy/Anadarko, along with increasingly important Woodside Energy, competed for the 4 red blocks in the Green Canyon area (map above and table below). These elephant hunters presumably see excellent Paleogene (Wilcox) prospectivity in those blocks.

17 of the sale’s 38 bids (45%) and $32.8 milion of the sale’s $47 million in high bids (70%) were for these 4 blocks. BP’s $21 million bid for GC 404 was by far the sale’s highest bid.

Green Canyon Block No.

No. of bidders

High Bidder

Bid

404

5

BP

$21,009,990

405

2

BP

$885,99

448

5

Chevron

$4,967,067

492

5

Chevron

$5,887,188

At this time, the high costs and technical complexities (e.g. deepwaterand high pressure/high temperature reservoirs) limit Wilcox development to major oil companies and well financed, technically savvy independents. Expect some of the international majors that did not participate in BBG2 to acquire lease interest at a later date, which will again raise questions about the merits of joint bidding restrictions.

From AAPG graphic-Wilcox trend map. Eastern area can be subdivided into an outboard and inboard trend, with wells in the latter area showing variable thickness due to salt tectonics contemporaneous with deposition (From Zarra et al. 2019’s AAPG Search and Discovery article).

Imbedded below is a good presentation on the Paleogene Wilcox by Dr. Mike Sweet, Univ. of Texas:

Although no one was expecting a barnburner only 3 months after the previous sale, BBG2 was historically weak for a Gulf-wide sale. The table below compares BBG2 with the previous 4 Gulf sales, none of which were particularly impressive.

However, the sale was not without highlights. There was some spirited bidding for tracts in the Green Canyon area. BP’s bid was the highest of 5 for GC Block 404. BP bid $21 million for the block, 45% of the high bids sum for the entire sale. The BP bid was also $20 million higher than the next highest bid for that tract (ouch!).

Also interesting was Chevron edging Shell $5,887,188.00 to $5,501,240.00 to acquire GC Block 492.

Sale No.

257

259

261

BBG1

BBG2

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

3/11/2026

companies participating

33

32

26

30

13

total bids

2233

2842

3161

219

38

tracts receiving bids

2143

2442

2751

181

25

sum of all bids $millions

198.5

309.8

441.9

371.9

69.9

sum of high bids ($millions)

101.7

263.8

382.2

279.4

47.0

highest bid company block

$10,001,252 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

$18,592,086 Chevron KC 25

$21,009,990 bp GC 404

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

50 bp 61.0

6 Anadarko (Oxy) 4.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

61.0 bp

22.6 bp

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

14-Murphy

5-LLOG

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

For historical comparison purposes, Gulf Sale 206 drew $3.7 billion ($5.6 billion in today’s dollars) in 2008. Twenty-siz sales between 1972 and 2013 garnered more than $1 billion in high bids.

Gulf of America oil and gas lease sale BBG2 will be held tomorrow. The Notice of Sale is attached.

Although Big Beautiful Gulf 1 (BBG1) was rather lackluster, BBG 2 is unlikely to match it in terms of the number of bids and their sum. Prior to BBG1, there had been no lease sale for two years. BBG 2 is being held only 3 months later.

Given the short duration between sales, the bid evaluations for BBG1 are not yet completed. However, the sale notice advises that any block which received a bid in BBG1 is excluded from BBG2.

Will the recent increase in oil prices influence bidding? Probably not given the longer term nature of offshore development and expectations that the current price spike will be of short duration. Onshore shale oil production is more responsive to price fluctuations.

BOEM: At this time, no bids have been received. In accordance with OBBBA, we will continue to hold leasing opportunities for Cook Inlet so that industry has a regular, predictable federal leasing schedule that ensures we achieve President Trump’s American Energy Dominance Agenda.

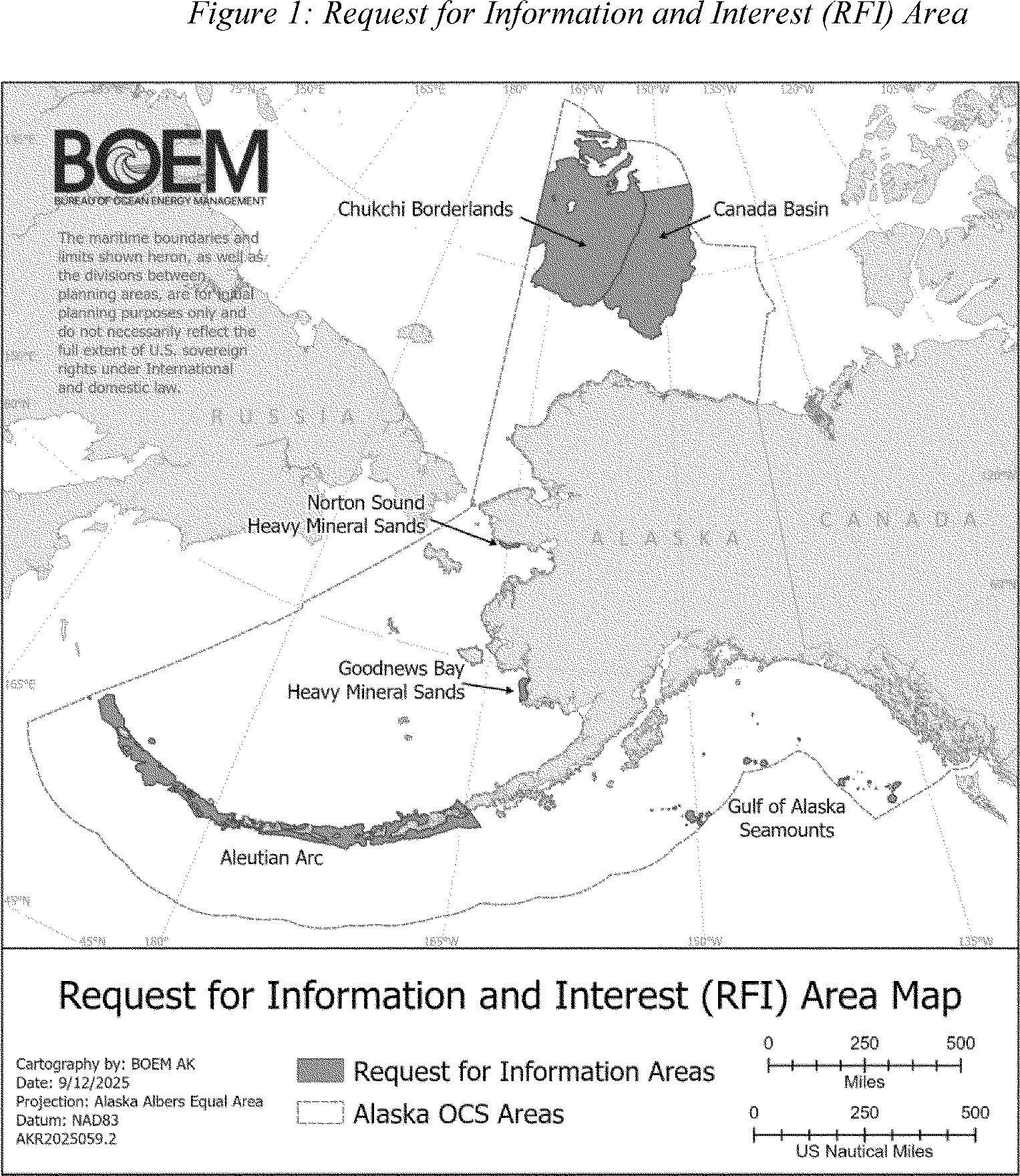

“The Bureau of Ocean Energy Management (BOEM) is initiating the first steps that could potentially lead to a lease sale for minerals on the Outer Continental Shelf (OCS) offshore Alaska by publishing this request for information and interest (RFI).”

While the majors and large independents garner most of the attention, smaller companies are an integral part of the mosaic that is the Gulf of America petroleum province. Some focus on producing and identifying remaining reserves on the shelf; others partner in deepwater projects.

Sale participants like Arena, Cantium, Walter, W&T, Beacon, Kosmos, and Houston Energy are well established Gulf leaseholders. Red Willow has attracted attention as a successful Southern Ute energy corporation.

The sale was beautifully conducted by BOEM, and Leslie Beyer – Assistant Secretary for Land and Minerals Management, Dept of the Interior – and Matt Giacona, Acting BOEM Director, delivered strong messages in support of the OCS oil and gas program.

However, as a colleague commented just after the sale, it was beautiful but not big. He and I expected more given the time since the last sale and the attractive terms.

Below is a comparison with the previous 3 Gulf sales. More to follow.

Sale No.

257

259

261

BBG1

date

11/17/2021

3/29/2023

12/20/2023

12/10/2025

companies participating

33

32

26

30

total bids

2233

2842

3161

219

tracts receiving bids

2143

2442

2751

181

sum of all bids $millions

198.5

309.8

441.9

371.9

sum of high bids ($millions)

101.7

263.8

382.2

279.4

highest bid company block

$10,001,252.00 Anadarko AC 259

$15,911,947 Chevron KC 96

$25,500,085 Anadarko MC 389

$18,592,086 Chevron KC 25

most high bids company sum ($millions)

46 bp 29.0

75 Chevron 108.0

65 Shell 69.0

50 bp 61.0

sum of high bids ($millions) company

47.1 Chevron

108 Chevron

88.3 Hess

61.0 bp

most high bids by independent

14-DG Expl.

13-Beacon 13-Red Willow

22-Red Willow

14-Murphy

1excludes 36 leases improperly acquired for carbon disposal purposes; 2excludes 69 leases improperly acquired for carbon disposal purposes; 3excludes 94 leases improperly acquired for carbon disposal purposes

BOEM informs (post below) that Wednesday’s BBG1 oil and gas lease sale will be streamed live here at 10 AM ET. Given that this is the first sale in two years and the first BBG sale, some dignitaries may be in attendance.

On December 10, we will host the Big Beautiful Gulf 1 oil and gas lease sale, our first under the One Big Beautiful Bill Act.

“Natural gas and LNG are fast becoming the gravitational center of the global energy system, but some energy experts said the world is only beginning to grasp the scale of what’s to come.” ~Natural Gas Intelligence

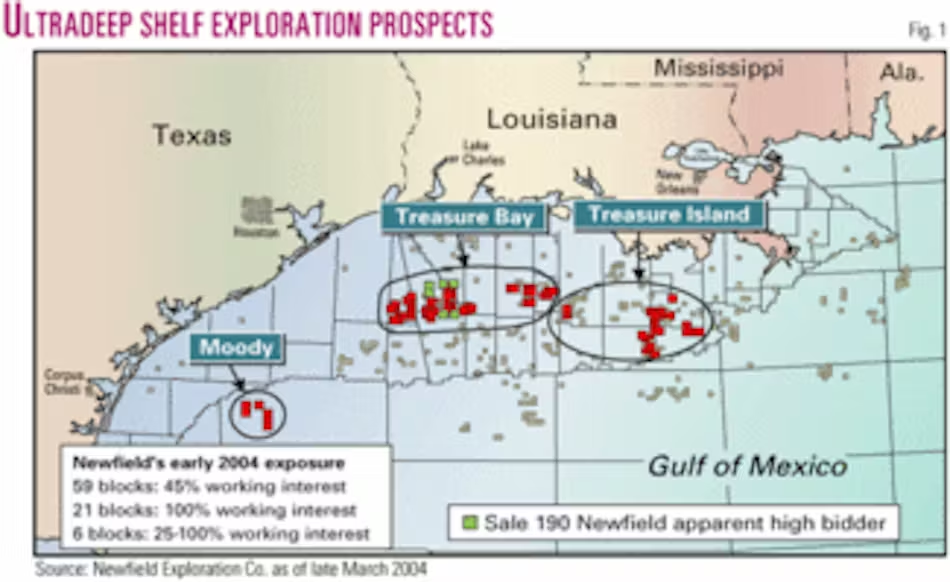

Demand and high well producibility are stimulating exploration in the high pressure, high temperature Western Haynesville (Texas) and other ultradeep onshore gas prospects. Is it time to revisit ultradeep gas on the Gulf of America shelf? See the above targets map from 2004.

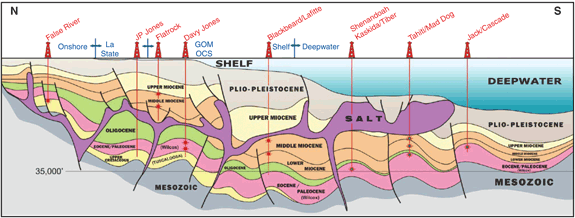

20 years ago Newfield, Exxon, and McMoRan drilled pioneering ultradeep wells targeting gas-prone reservoirs below salt welds in Miocene and older formations (diagrams below). The water depths were <100 feet but well depths exceeding 30,000 feet, and high temperatures and pressures, pushed the limits of drilling technology at the time. Noteworthy wells:

Blackbeard West (Exxon): Spudded in early 2005 in 70 feet of water in South Timbalier Block 168. The target was gas in Miocene sands at 27,000-32,000 feet total depth. Drilling reached 30,067 feet by 2006, but was prudently suspended due to extreme pressures, temperatures (up to 600°F), and technical challenges with equipment.

Blackbeard West, part 2: In 2008, McMoRan re-entered the well with upgraded equipment and drilled to a record 32,997 feet below the mudline. They encountered hydrocarbon shows in multiple zones, including potential gas pay in Middle and Deep Miocene sands below 30,000 feet, validating the ultradeep concept.

Followup McMorRan wells:

Blackbeard East (2010-2011): Drilled to 33,400 feet in South Timbalier Block 144, logged potential hydrocarbons in Sparta and Vicksburg sands.

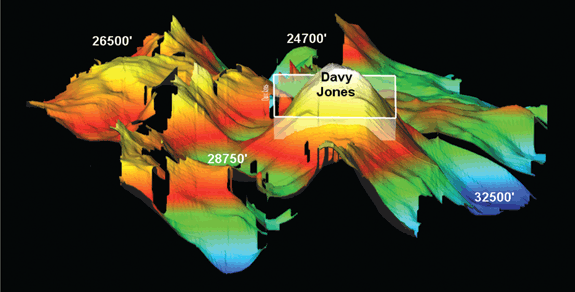

Davy Jones (2009-2010): South Marsh Island Block 230 in 20 feet of water; reached 29,122 feet; discovered gas in Wilcox sands, but faced flow-testing challenges.

Lafitte (2011): Eugene Island Block 223, found additional pay in ultradeep Miocene zones. These wells targeted gas reservoirs but encountered operational hurdles.

Also, note that a company targeting hydrocarbons below 25,000 feet (true vertical depth subsurface) may earn an additional 3 years on their lease. (See the Notice for next week’s lease sale.) Will improved technology and demand expectations finally open the ultradeep gas frontier?