Forbes (USGS map of active wind turbines): “The U.S. Wind Turbine Database contains more than74,695 wind turbines built since 1980, spread between 1,699 wind power projects in 45 states. However, thousands of wind turbines are reaching the end of their operational lifespan and need to be either repowered to make way for updated (often larger) turbines or entirely decommissioned to allow for new uses of the land they occupy. Unfortunately, there is no uniform legal framework to regulate the steps involved, nor is there an accepted industry-wide set of best practices, and the environmental costs are considerable.”

Forbes: “As is often the case when new technologies come to market, unintended downstream consequences are not always immediately obvious to the players. Enthusiasm for clean energy initially pushed the first wind turbines into existence in the U.S. without considering the environmental and monetary costs that would be involved in either upgrading or bringing projects to a close later in their life cycle. “

“At the heart of the dispute are rules from the federal Bureau of Ocean Energy Management – BOEM – which require energy producers in the Outer Continental Shelf to provide a bond to pay for well, platform, pipeline and facilities cleanup if the operating company fails to do so.”

“These insurance companies and their unreasonable demands for increased collateral pose an existential threat to independent operators like W&T.”

Comment: If insuring offshore decommissioning is so risk-free and lucrative, why aren’t other companies entering the market?

“Several states, including Texas, are challenging the BOEM rule and in one case they specifically cite W&T as an example of how the rule could be misused to irreparably harm energy producers.“

Comment:As previously posted, the concerned States should propose alternative solutions that would promote production while also protecting taxpayer interests. Arguing that decommissioning financial risks are not a problem is neither accurate nor a solution.

“In over 70 years of producer operations in the Gulf of Mexico, the federal government has never been forced to pay for any abandonment cleanup operations associated with well, platform facility, or pipeline operations.”

Comment: Shamefully, from the standpoints of both the offshore industry and the Federal government, that statement is no longer true. The taxpayer has now funded decommissioning operations in the Matagorda Island Area offshore Texas (BSEE photo below) and more significant decommissioning liabilities loom.

I’m not typically aligned with the sponsors of the attached “Plug Offshore Wells Act,” but the call for transparency is understandable given that taxpayer funds are, for the first time, being used to decommission offshore platforms in the Matagorda Island area of the Gulf of Mexico, massive liabilities associated with the Cox bankruptcy loom, and the Hogan and Houchin saga drags on without resolution.

The bill would require an annual report on well, platform, and pipeline decommissioning including applications, deadlines, and enforcement actions. BSEE does have a good facility infrastructure page for the GoM, but much of the information called for in H.R. 9168 is not publicly available.

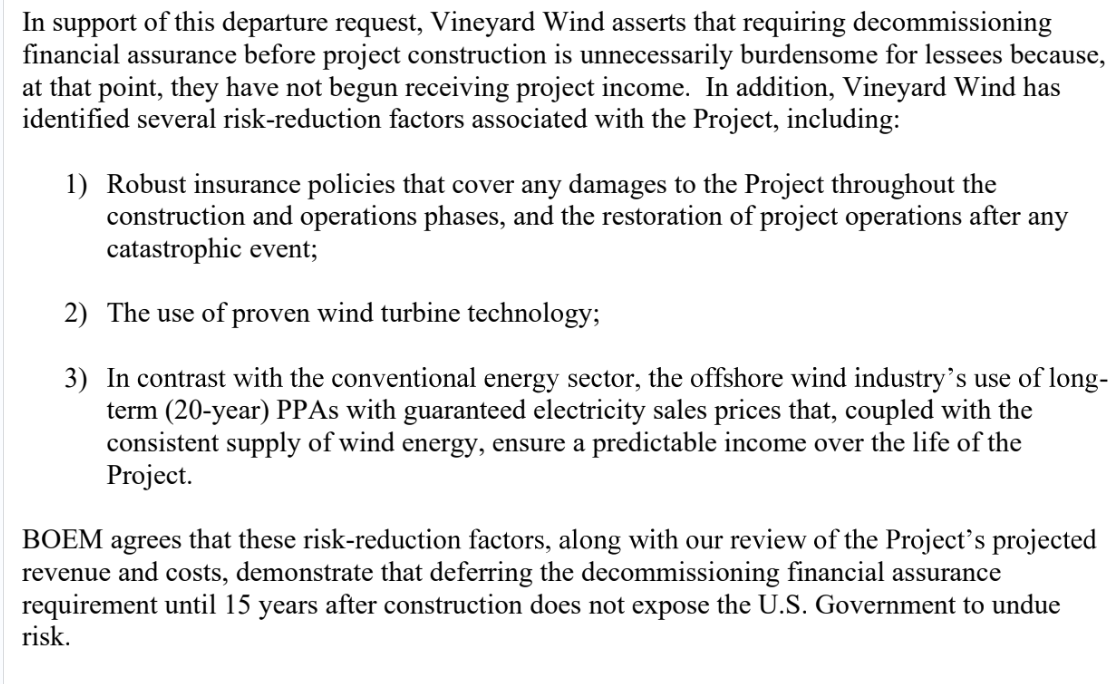

Comments on the 3 risk reduction factors cited in the letter:

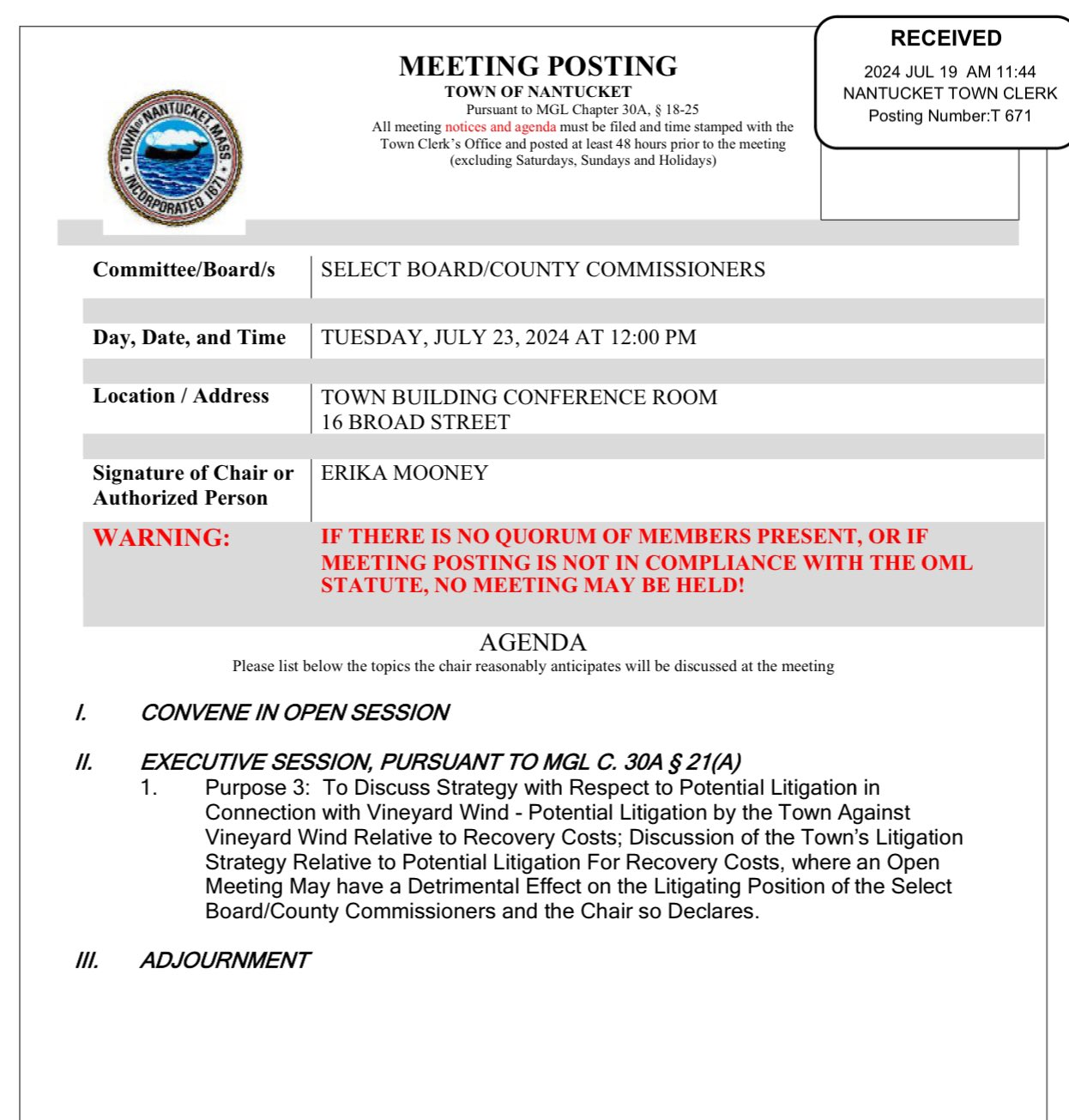

Factor 1: Those “robust insurance policies” may soon be tested given the costs associated with the turbine blade incident and potential law suits. (The notice pasted below informs that Nantucket officials will meet on Tuesday to consider litigation. A question for attorneys is the extent to which Nantucket is compromised by their good “Good Neighbor Agreement” with Vineyard Wind. That agreement essentially calls on Nantucket to promote the Vineyard Wind projects in return for payments that seem modest relative to the economic benefits from tourism and fishing.)

Factor 2: To the extent that GE Vernova Haliade-X 13 megawatt turbines are proven technology (and that is very much in doubt), the use of proven technology doesn’t prevent premature abandonment associated with unexpected incidents.

Factor 3: Reliable power generation and predictable long-term income remain to be demonstrated.

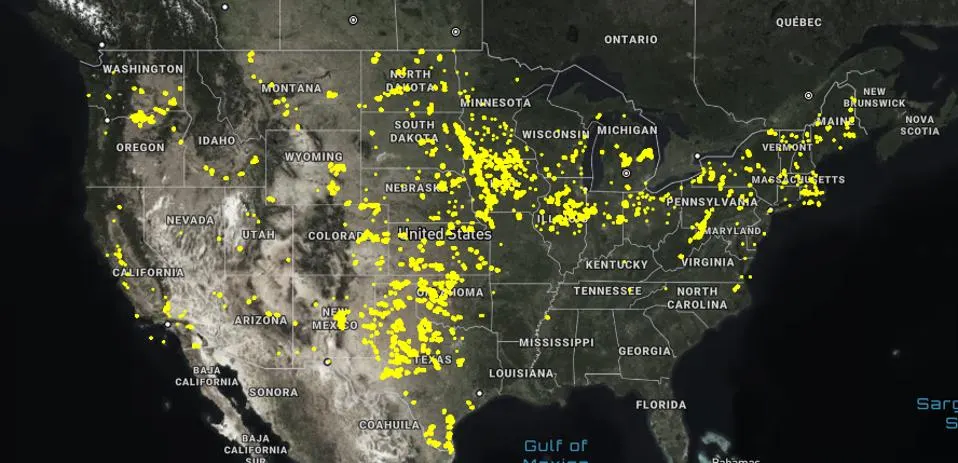

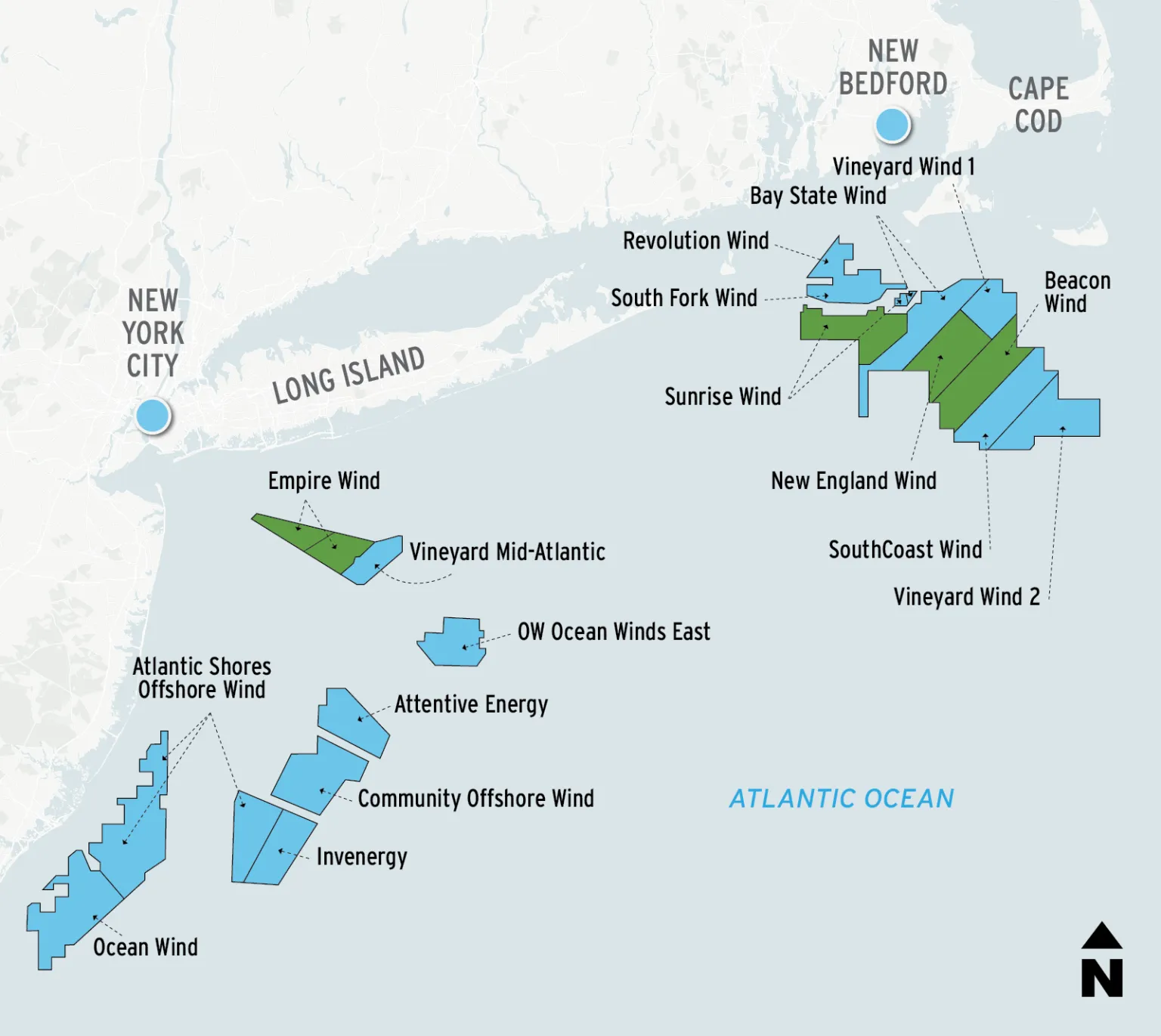

BOEM’s land rush approach to offshore wind leasing will add up to 1086 turbine towers and 28 offshore substations (OSSs) in the Atlantic just from active projects with approved Records of Decision (RODs). (See the table below.) Another 17 active Atlantic commercial projects have yet to reach the ROD stage. Those projects should increase the total number of structures to >3000. Five more Atlantic wind lease sales are scheduled.

project

turbine towers

offshore substations

Coastal VA Offshore Wind

202

3

Revolution Wind

100

2

Sunrise Wind

94

1

Atlantic Shores South

200

up to 10

Ocean Wind 1

98

up to 3

Vineyard Wind 1

100

2

Empire Wind 1 & 2

147

2

New England Wind (phases 1&2)

150

5

Per the Construction and Operations Plan (COP) for Vineyard Wind, the topsides for a conventional electrical service platform (ESP) (also known as an offshore substation or OSS) are 45 x 70 x 38 m, which is larger in surface area than a typical 6-pile oil and gas platform (~30 x 30 m), and is comparable in size to a large jackup drilling rig.

The Atlantic Shores plan calls for 10 small, 5 medium, or 4 large OSSs. (Uncertainty regarding the number and types of structures seems rather common in wind COPs.) The large OSSs have topsides that are 90 m by 50 m and rise to 63 m above MLLW. These are large offshore structures whether for wind or oil and gas.

Per BOEM, the “Rule to Streamline and Modernize Offshore Renewable Energy Development” is intended to “make offshore renewable energy development more efficient, [and] save billions of dollars. Unfortunately, the savings associated with relaxed financial assurance requirements translates to increased risk for power customers and taxpayers.

BOEM signaled their intentions on offshore wind (OSW) decommissioning three years ago when they granted a precedent setting financial assurance waiver to Vineyard Wind. Despite compelling concerns raised by commenters, the “streamlining” regulations codified this decision.

No one knows what the financial future will be for wind projects and the responsible companies. Financial assurance should therefore be established when the structures are installed, not years into the future as allowed by the revised regulations. What leverage will BOEM have then?

Nordsee One substation, Germany. Rystad Energy projects 137 new power substations offshore continental Europe this decade, requiring $20 billion in total investment.

The limited media coverage of the lawsuit originated from a single Reuters article. Apparently Reuters learned about the suit and reached out to the litigants. Their article quoted Louisiana Attorney General Liz Murrill as follows:

“This is a really egregious direct assault on intermediate level producers of oil and gas, and that affects a lot of business in our state,” Murrill told Reuters in an interview.

That quote is all we have from the AGs. Why the absence of announcements:

Interest in working with industry and the Federal govt to seek policy solutions that best address OCS decommissioning issues? (This would be encouraging.)

State of Louisiana, Louisiana Oil & Gas Association, State of Mississippi, State of Texas, Gulf Energy Alliance, Independent Petroleum Association of America and U S Oil & Gas Association

Defendant:

Deb Haaland, U S Dept of Interior, Bureau of Ocean Energy Management, Elizabeth Klein, Steve Feldgus and James Kendall

Case Number:

2:2024cv00820

Filed:

June 17, 2024

Court:

US District Court for the Western District of Louisiana

Presiding Judge:

James D Cain

Referring Judge:

Thomas P LeBlanc

Nature of Suit:

Other Statutes: Administrative Procedures Act/Review or Appeal of Agency Decision

Cause of Action:

28 U.S.C. § 2201 Constitutionality of State Statute(s)

Decommissioning financial assurance issues are complex!

This blog has raised significant concerns about BOEM’s decommissioning financial assurance rule, and will continue to comment on decommissioning policy. That said, decommissioning issues are complex and have challenged industry and government in the US and internationally for decades. Add well plugging practices, corrosion, storm risks, reefing vs. total removal, alternative uses for old platforms, and pipeline and seafloor equipment abandonment to the myriad of financial issues and you get a sense of the breadth and complexity of decommissioning issues.

Decommissioning is unique in that the issues divide sectors of the offshore industry that are typically aligned (majors vs. smaller producers). The environmental community is also divided with the reefing and fishing advocates opposing those who insist on complete removal.

Given these divisions, and decommissioning’s operational, environmental, and political complexities, highly partisan assertions are common. A recent article about the financial assurance rule includes a number of such assertions, and provides a framework for discussing some of the more prominent issues. Excerpts from the article and my comments follow.

“This costly rule became final on April 15, 2024, but in the 10 months since its initial proposal, BOEM did nothing to alleviate concerns for smaller companies that comprise of 76 percent of oil and gas operators in the Gulf.“

Comments:

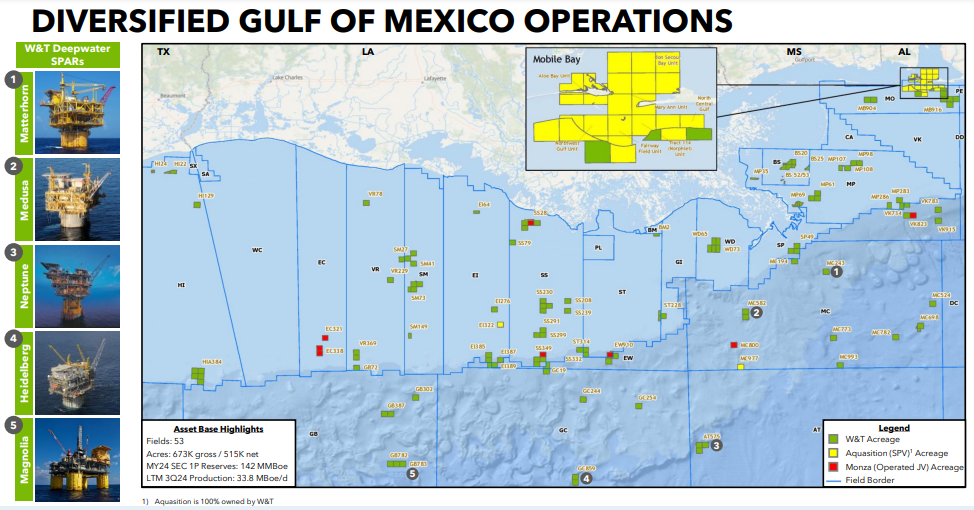

While I concur that shelf operations and the independent companies that conduct them are important, 94% of OCS oil production and 80% of the gas (2023 data) were from deepwater facilities (>1000′ WD) which are largely the domain of the majors (although the participation of independents in the deepwater sector is increasing).

In 2023, four majors – Shell, bp, Oxy (Anadarko) and Chevron – accounted for 2/3 of the Gulf’s total oil production.

1467 of the remaining 1527 GoM platforms are in <1000 feet of water and are almost exclusively operated by small producers. So 96% of the platforms are producing only 6% of the oil and 20% of the gas.

This dichotomy presents a major challenge for BOEM which must protect the public from decommissioning liabilities without unfairly penalizing small producers.

Having worked for respected political appointees from both parties, my experience has been that the smaller producers (somewhat surprisingly) have more political influence than the majors. For this reason, along with the general lack of attention to financial assurance issues in the early years of the offshore program, the standard bond requirement was ridiculously low for much of the program’s history, and supplemental financial assurance assessments were typically inadequate (and still are which is why the new rule was promulgated).

Attention to decommissioning issues grew exponentially in the early 1990s. Prior to that time, platform removal, like well plugging, was classified as “abandonment,” a term that was considered too harsh when bankruptcy issues and the Brent Spar controversy in the North Sea attracted worldwide attention.

“Records obtained via the Freedom of Information Act show private meetings between Interior officials and representatives of the major oil companies as they cooperated on this rule.“

Comments:

The linked FOIA records are not at all problematic. They pertain to meetings prior to the publication of the draft rule, which are appropriate and desirable.

Some of these meetings were in response to BOEM’s request for input regarding their review of the OCS oil and gas program. Such meetings are particularly helpful when a new administration is trying to assess the direction of the program.

Indeed 42 of the 71 pages in the FOIA were official industry comments in response to the BOEM request.

Per the Regulations.gov docket on the financial assurance rule, BOEM also met with stakeholders after the proposed rule was published. Those meetings are allowed as long as the regulator simply receives input and does not signal decisions regarding the content of the final rule.

The docket shows that BOEM had 8 listening sessions with advocates for independent producers. These included 2 sessions with the Gulf Energy Alliance and 6 sessions with individual independent producers.

BOEM also had 2 listening sessions with Oceana, a prominent environmental organization, and multiple sessions with tribal organizations.

The only sessions with representatives from major producers were a single session with API and a single session with Shell, the Gulf’s largest producer.

These meetings (after the proposed rule was published) are noted in the docket as required.

I am concerned that many listening session documents (from all sides of the decommissioning financial assurance issue) were removed from the docket at the direction of OIRA/OMB, purportedly because they included privileged information. This is rather troubling given the number of deletions and the complete absence of information about those meetings. What types of privileged information were these organizations providing and why is there no information whatsoever on these meetings? At a minimum, a list of attendees and general summary for each meeting should have been posted, as was our practice in the past.

“Big Oil must think it won’t miss the small competitors the rule will drive from the market.“

Comments:

There is important synergy between the major producers and independents, and no reason for driving smaller companies from the market.

The independents are critical to sustaining the shelf infrastructure and the associated service companies, which helps to facilitate deepwater development. Majors also benefit from partnering with independents on lease acquisitions, development projects, and lease assignments.

Financial assurance for decommissioning of transferred assets is the one area of significant conflict, particularly when there have been multiple ownership changes since the facilities were initially transferred.

“Historically, joint and several liability protected these small businesses from the financial demands of surety bonds.”

Comments:

Surety bonds, or other forms of financial assurance, have always been required. As previously noted, the amounts were often inadequate.

Joint and several liability was not established in the regulations until May 22,1997. Whether companies are liable for facilities transferred prior to that date has yet to be considered in court.

1130 of the 1527 remaining GoM platforms were installed prior to May 22,1997. Many of these platforms were no doubt transferred prior to that date, which means the liability of the initial owner is uncertain.

Predecessor liability does not apply to new wells and platforms constructed by the current lessees.

Joint and several liability was never intended to relieve current lessees from their financial assurance responsibility, which is why assignors were required to provide such assurance. BOEM is correct in strengthening their enforcement of this requirement.

“The new rule is largely silent on joint and several liability, causing some uncertainty.”

Comment: The joint and several liability provision remains in place at 30 CFR 250.1701(a) BOEM has added language to part 556.704, to clarify, correctly in my opinion, that they may withhold approval of any transfer or assignment of any lease interest if the financial assurance requirements have not been satisfied.

Companies may not be able to acquire the needed financial assurances because the market likely will not even exist.

Comment: The history of small producer failures is no doubt a concern to financial institutions. BOEM offers multiple financial assurance options, some of which have been questioned on this blog. If a company can’t qualify, it’s not the responsibility of the public to assume their decommissioning risks.

What makes matters worse is that all this cost covers a risk that is effectively a rounding error historically and in the context of the royalties flowing from the offshore oil and gas industry. According to BOEM, taxpayers have borne decommissioning liability totaling $58 million – from a single company that lacked predecessor owners of the platform to call on to cover unfunded cleanup costs.

Those who seek to minimize the Federal government’s risk exposure should consider the findings in the 2024 GAO report. Per that report, “BOEM held about $3.5 billion in supplemental bonds to cover between $40 billion and $70 billion in total estimated decommissioning costs as of June 2023.”

When will we find out who will be paying the hundreds of millions needed to decommission long-idled Platforms Hogan and Houchin in the Santa Barbara Channel?

Decommissioning financial assurance is a responsibility of lessees, not the taxpayer.

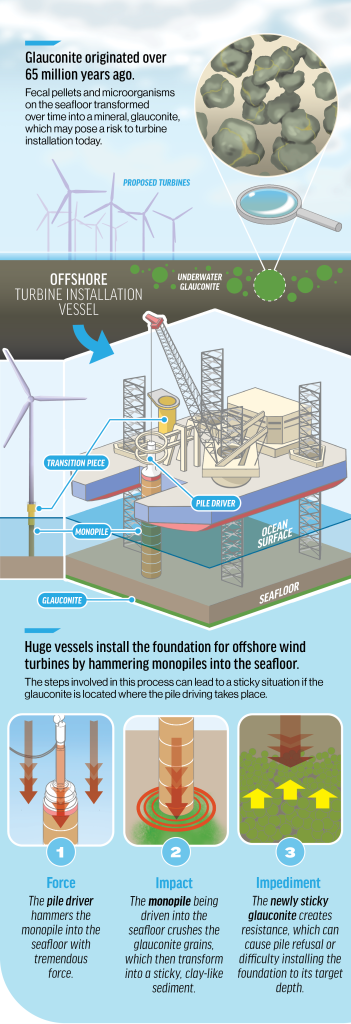

Illustration credit: Kellen Riell / The New Bedford LightGlauconite has been identified within the boundaries of lease areas marked with green. Credit: Kellen Riell / The New Bedford Light

Anastasia Lennon has published several informative articles in the New Bedford Light on the challenges posed by the presence of glauconite on North Atlantic wind leases. The above illustrations explain those challenges and identify where glauconite has been found to date. Per her latest article:

Preliminary geotechnical analysis for New England Wind, an Avangrid project, showed a risk of turbine pile foundation refusal in 50 of nearly 130 turbine locations, or about 40%, according to 2023 records obtained through a Freedom of Information Act request.

The mineral’s behavior poses a “significant risk” to offshore wind development, said BOEM, the federal regulator of offshore wind, in a paper last year.

BOEM’s “Rule to Streamline and Modernize Offshore Renewable Energy Development” is intended to “make offshore renewable energy development more efficient, [and] save billions of dollars. Unfortunately, the savings associated with relaxed decommissioning financial assurance requirements translates to increased risk for customers and taxpayers.

BOEM signaled their intentions on offshore wind (OSW) decommissioning three years ago when they granted a precedent setting financial assurance waiver to Vineyard Wind. Despite compelling concerns raised by commenters, the “streamlining” regulations have codified this decision.

Cape May County, New Jersey, was among the commenters objecting to BOEM’s departure from the prudent “pay as you build” financial assurance requirement. The County commented as follows (full comment letter attached):

“[e]nergy-utility projects are in essence traditional public-private partnerships where technical and financial risks are transferred to the private sector in exchange for the opportunity to generate revenues and profit. Under the proposed rule, the Federal government is instead transferring risks associated with decommissioning to the consumer rather than to the private sector.”

Cape May added:

“[w]hile BOEM believes that if a developer becomes insolvent during commercial activity that a solvent entity would assume or purchase control, the County believes this is a risky assumption as the most likely reason for default is that a constructed wind farm developer is unable to meet its contractual obligations set forth under a Power Purchase Agreement (PPA) because its energy production revenues are not in excess of its operating costs. A change of hands would not remove these circumstances or make the project profitable.”

Cape May and others also commented on the threat of premature decommissioning as a result of storm damage. In response, BOEM asserts that these risks have been addressed in the latest standard for North American offshore wind turbines (Offshore Compliance Recommended Practices: 2022 Edition (OCRP-1-2022)). However, design standards, particularly those for offshore facilities, are not static. The recommended practice for OSW is likely to change multiple times in the coming years as storm, operating, and turbine performance data are updated and analyzed. The design standard for Gulf of Mexico platforms has been repeatedly refined and improved and is now in its 22nd edition.

In their response to public comments on the decommissioning risks, BOEM repeatedly asserts that they can adjust the amount and timing of required financial assurance as they monitor a lessee’s financial health. Unfortunately, a company’s finances can change quickly and BOEM’s options will be limited when it does. Increasing the financial burden on a struggling company that is providing power to a regional power grid will not be a simple proposition.