Yesterday, Lars Herbst attended the EIA’s Annual Energy Outlook presentation. The slides are attached.

Below is a custom chart from the EIA data tables. While EIA predicts growth in renewable generating capacity, US oil and gas production are nonetheless projected to increase slightly through 2050.

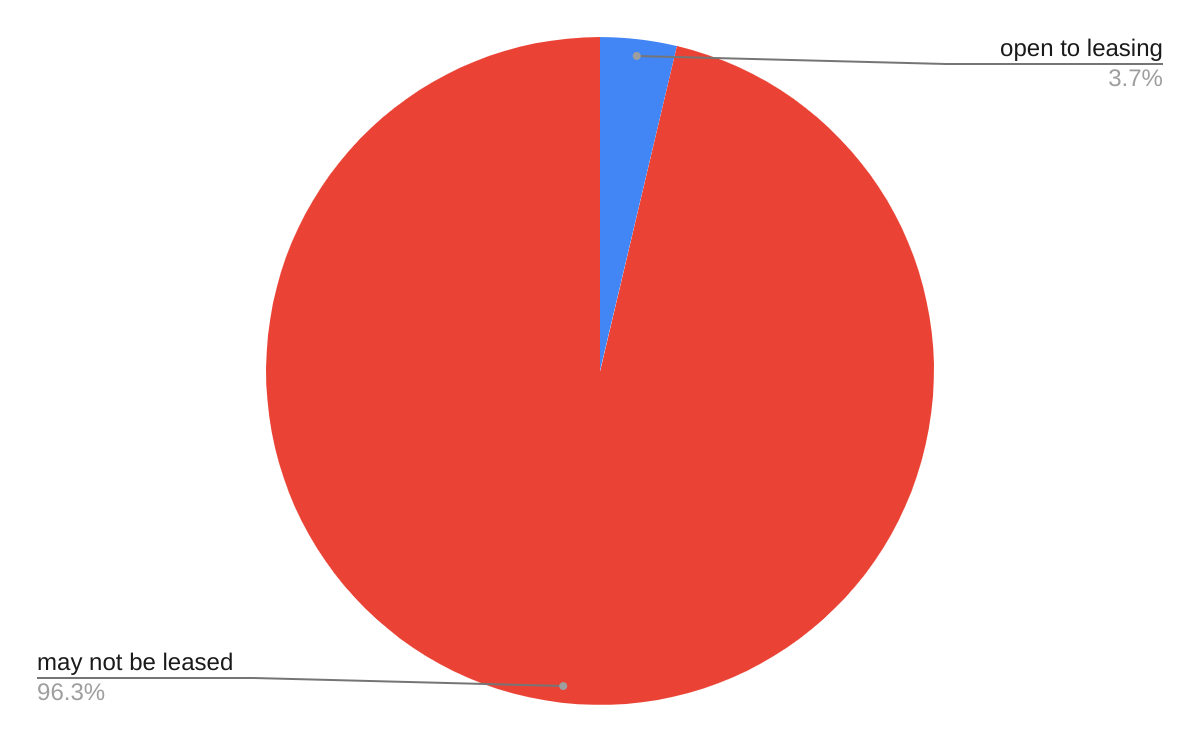

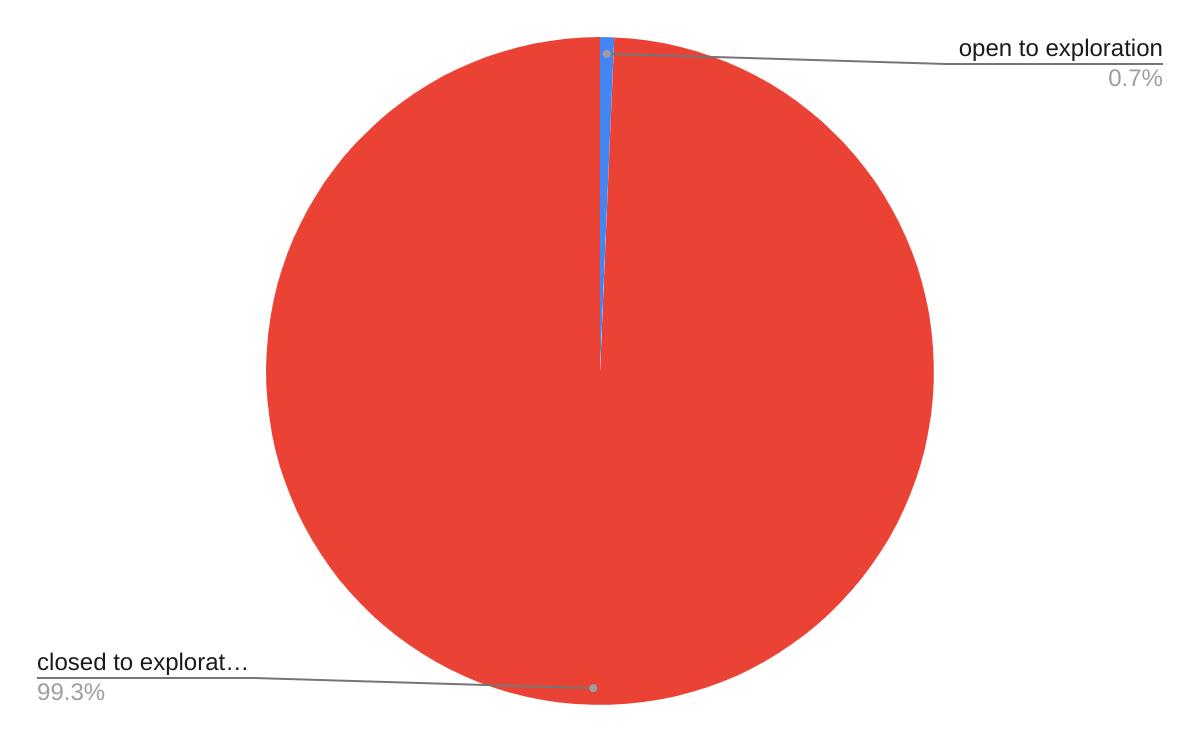

Of the 1.7 billion acres of Federal land on the US Outer Continental Shelf, only about 73 million acres in the Gulf of Mexico and 1 million acres in the Cook Inlet may be offered for oil and gas leasing. Official or de facto exclusions prohibit leasing in the entire US Atlantic, the entire US Pacific, all Alaska areas except the Cook Inlet, and most of the Eastern Gulf of Mexico. No other coastal nation has restricted access to oil and gas resources to this extent.

The number of active leases, currently 2153, has been at a historically low level for the past 2 years. Only 0.7% of our OCS is leased and thus open to exploration. 26% (552) of these leases are already producing, leaving a historically low number of nonproducing leases.

Oil is where you find it, not where you wish it was or want it to be. Denying access to all but a small portion of the OCS limits exploration strategies and prevents publicly owned resources from supporting our economy in the manner intended by the OCS Lands Act.

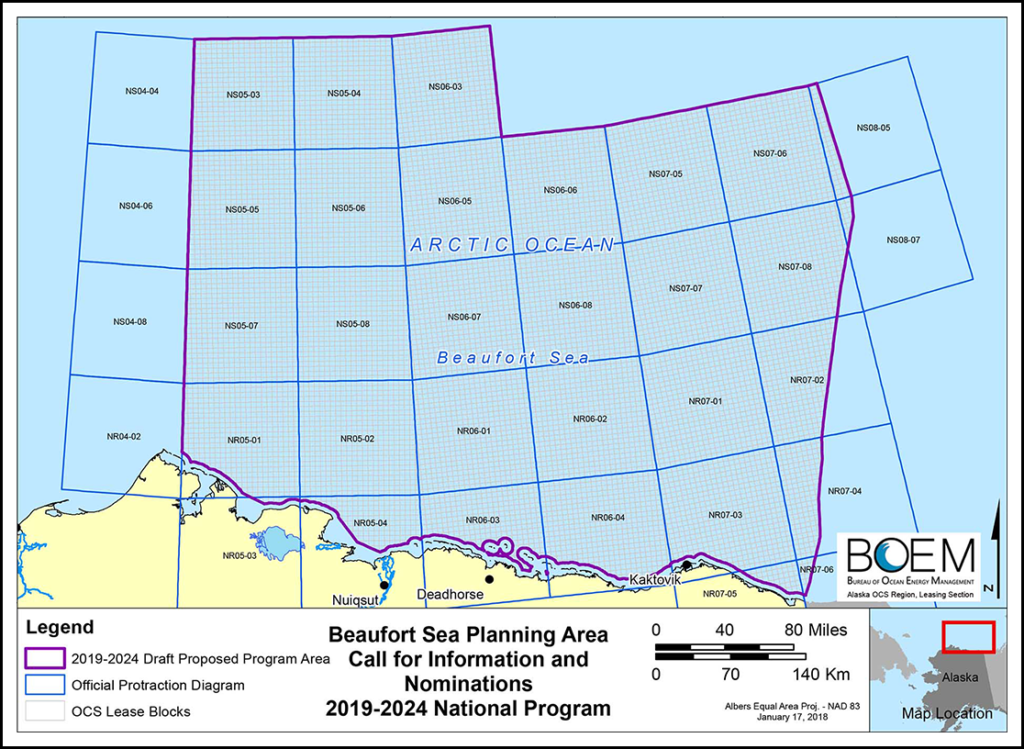

The shrinking of the OCS oil and gas program continues. In an attempt to placate opponents of the Willow project, the President has removed the entire Beaufort Sea from oil and gas leasing consideration. Unsurprisingly, the opponents of Willow are no less irate.

Under the authority granted to me in section 12(a) of the Outer Continental Shelf Lands Act, 43 U.S.C. 1341(a), I hereby withdraw from disposition by oil or gas leasing for a time period without specific expiration the areas designated by the Bureau of Ocean Energy Management as the Beaufort Planning Area of the Outer Continental Shelf that have not previously been withdrawn.

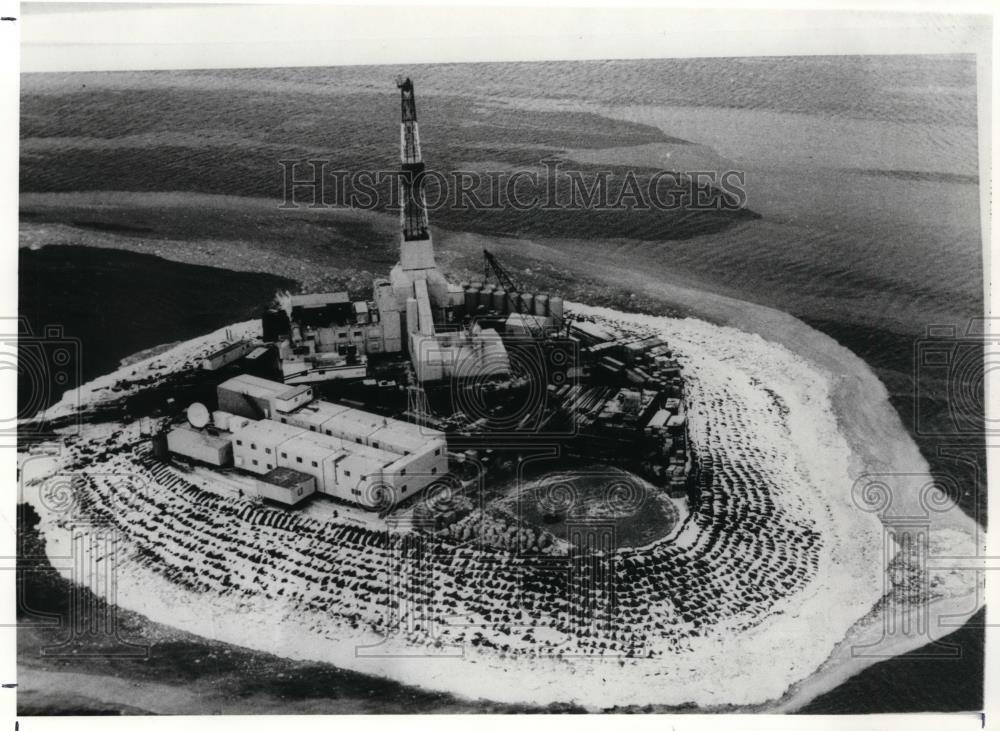

The 5 Hilcorp leases identified above (Northstar and Liberty projects) are all that remains of the once promising Beaufort Sea planning area.The Kulluk, pictured above, was a unique conical shaped and ice strengthened drilling vessel that operated in the US and Canadian Beaufort from 1983-1993.BP’s Mukluk well being drilled from an artificial island in the US Beaufort Sea in 1983. The $120 million exploratory well was the most expensive in history, but did not find commercial quantities of hydrocarbons.

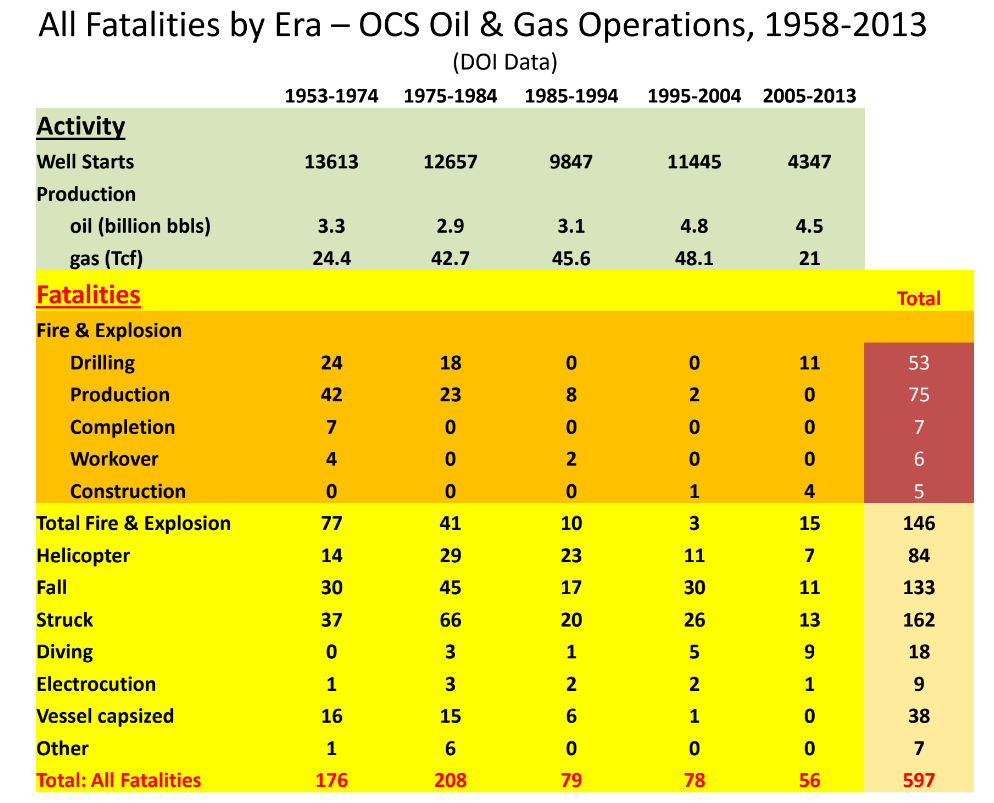

Per yesterday’s post, below are US OCS fatality data from a 2014 presentation. Ten year intervals were selected for 1975-2004. The longer 1953-1974 era was selected so the activity indicators (well starts and production) would be comparable with the next 3 intervals. The last interval (2005-2013) was limited because the presentation was prepared in 2014.

Fire/explosion fatalities exceeded fall/struck fatalities only in the first interval (1953-1974). As one would expect, the fire/explosion deaths were associated with a limited number of better known incidents (e.g. Main Pass 41, Bay Marchand, Macondo). While the overall trend is favorable, fall/struck incidents and helicopter fatalities at offshore platforms have proven to be more chronic.

I hope to update these data in the not too distant future.

The most common causes of offshore fatalities and serious injuries, falls and being struck by equipment, receive little media attention because there is no blowout, oil spill, or fire. However, these are often the most difficult types of incidents to understand and prevent. Human and organizational factors predominate, and prevention is dependent on a strong culture that emphasizes worker engagement, awareness, teamwork and mutual support, effective training and employee development, risk assessment at the job, facility, company, and industry levels, stop-work authority, innovation, and continuous improvement.

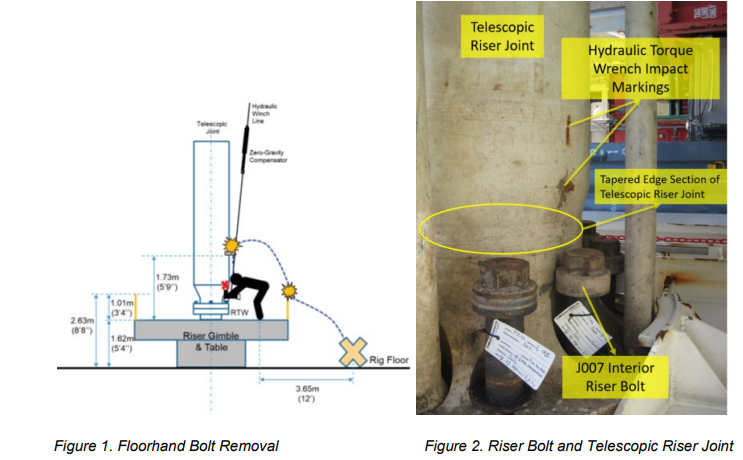

While unlatching the lower Marine Riser Package from the Blowout Preventor in preparation for ship relocation, a crewmember was lifted into the air after being struck by a hydraulic torque wrench (HTW), hitting a riser clamp approximately six feet above the elevated work deck before falling to the rig floor. The crew member was given first aid and transported to the drillship’s hospital, where he was later pronounced deceased.

In an upcoming post, BOE will provide historical fatality data by cause and operations category.

HOUSTON — Oil and gas industry leaders say they’ve seen a big shift in tone from the Biden administration over the past year, helping to smooth over one of the president’s rockiest relationships.

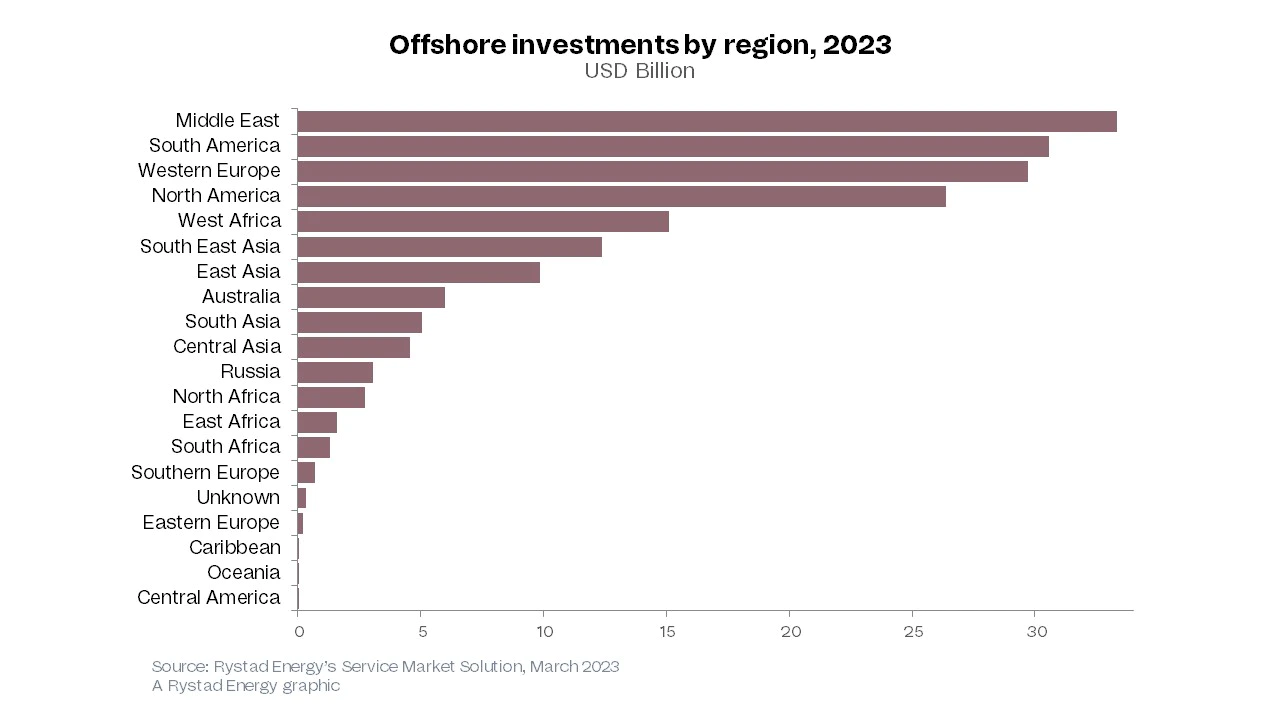

The offshore oil and gas (O&G) sector is set for the highest growth in a decade in the next two years, with $214 billion of new project investments lined up. Rystad Energy research shows that annual greenfield capital expenditure (capex) broke the $100 billion threshold in 2022 and will break it again in 2023 – the first breach for two straight years since 2012 and 2013.

Offshore activity is expected to account for 68% of all sanctioned conventional hydrocarbons in 2023 and 2024, up from 40% between 2015-2018.

Washington, DC — Today, U.S. Senator Joe Manchin (D-WV), Chairman of the Senate Energy and Natural Resources Committee, released the following statement on the Department of the Interior’s (DOI) unprecedented delay in releasing a five-year leasing plan.

“Monday night, the Department of the Interior made it painfully clear – again – that they are putting their radical climate agenda ahead of our nation’s energy security, and they are willing to go to great lengths to do it. The earliest that Interior will release a legally required program for 2023-2028 offshore oil and gas leasing will be the end of this year. That’s 18 months late. This is the first time in our nation’s history that we haven’t had a 5-year leasing program released before the old plan expired. Every other Administration, Democrat and Republican, has managed to follow the law in a timely fashion.

“Let me be clear – this is not optional. The Outer Continental Shelf Lands Act mandates that the Secretary of the Interior “shall prepare” this program to “best meet national energy needs.”

“What is even more terrifying is that on top of this disturbing timeline, Interior refuses to confirm if they intend to actually include any lease sales in the final plan, which is an issue I sounded the alarm about when Secretary Haaland appeared before the Senate Energy and Natural Resource Committee on May 19, 2022. I will remind the Administration that the Inflation Reduction Act also prevents them from issuing any leases for renewables, like offshore wind or onshore solar unless there are first reasonable lease sales for oil and gas that actually result in leases being awarded. And I will hold their feet to the fire on this.”

Senator Manchin and the Alaska delegation criticized the DOI decision memo for Sale 258. The memo implied that the highest allowable royalty rate was chosen to minimize bidder interest and limit future production. Unfortunately, the “Inflation Reduction Act,” which mandated these lease sales, was not particularly helpful in creating interest in the less attractive OCS tracts like those in the Cook Inlet and the shallower waters of the Gulf of Mexico.

Sec. 50261 of the IRA raised the minimum allowable royalty rate from 12 1/2% to 16 2/3%, while capping the maximum rate at 18 3/4%. This provision favors deepwater operators, typically majors and large independents, whose royalty rates were capped at 18 3/4%, the same rate as for previous OCS sales.

Conversely, the IRA royalty provisions penalize the smaller companies and gleaners who are critical to sustaining shallow water (shelf) operations, including environmentally favorable nonassociated (gas-well) natural gas production, by raising the minimum royalty rate to 16 2/3%. DOI exacerbated IRA’s impact by electing to charge the highest allowable royalty rate for Cook Inlet and GoM shelf leases. The net result was a 50% royalty rate increase from prior sales (12.5 to 18.75%).

The table below illustrates the royalty rate implications of the IRA language and the DOI decisions.

Area

Sale

Date

% royalty: <200m water depth

% royalty: >200m water depth

Cook Inlet

244

6/21/2017

12.5

12.5

GoM

256

11/18/2020

12.5

18.75

GoM

257

11/17/2021

12.5

18.75

Cook Inlet

258

12/30/2022

18.75

18.75

GoM

259

3/29/2023

18.75

18.75

Notes:

The base primary term for GoM shelf leases is only 5 years vs. 10 years for leases in .>800 m of water.

In lease year 8 and beyond the rental rates are nearly double for shelf leases vs. deepwater leases ($40/ac vs. $22/ac).

While deepwater development typically requires more time, the higher rental penalty for delayed shelf production (which must be approved by BSEE) is not warranted. $40/acre or $240,000 per year (plus inspection and permitting fees) is a high cost for a marginal shelf lease.

Cook Inlet Sale 244 drew 14 high bids totaling more than $3 million. Sale 258 drew only 1 bid of $64,000. While many factors influence lease sale participation, the 50% increase in royalty rate certainly made the Cook Inlet leases less attractive.

Other than the increased royalty rate, the terms for both Cook Inlet sales were essentially the same. The primary lease term was 10 years and the minimum bonus bid was $25/hectare for both sales. The rental rate was increased by only $3/hectare ($13 to $16).

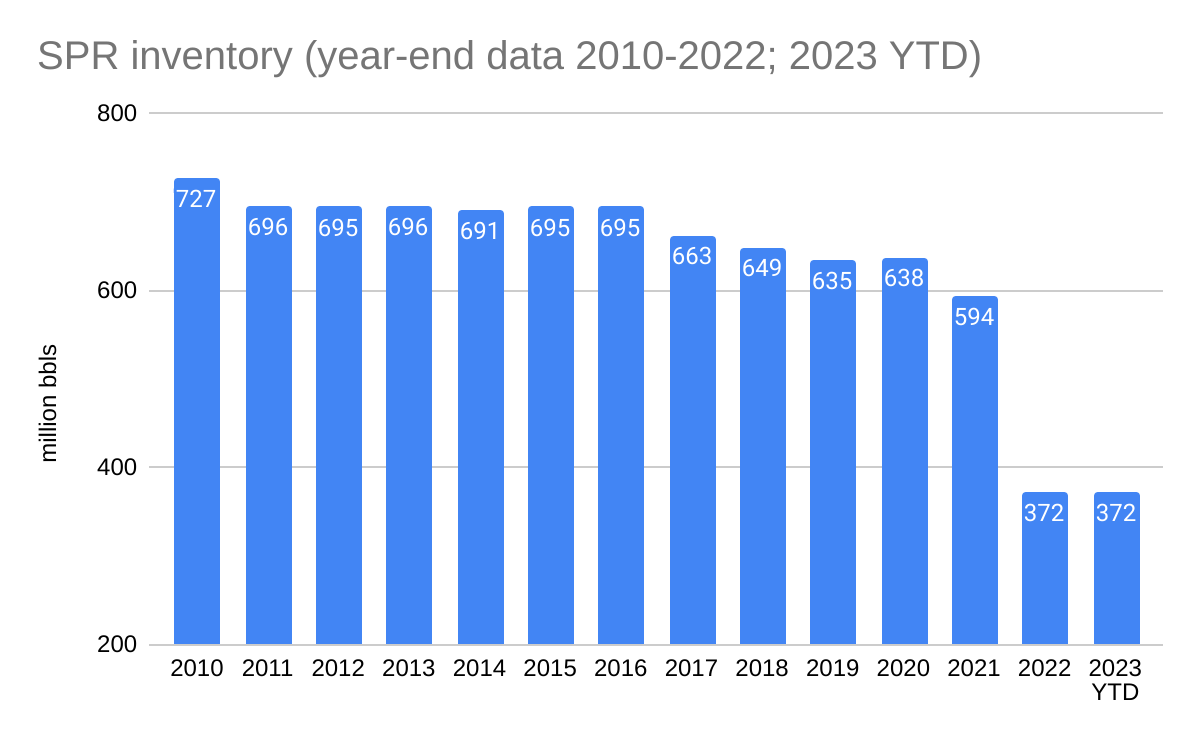

That is the amount of oil the US government has “borrowed” from the Strategic Petroleum Reserve without replacing. At $80/bbl, that’s ~$28 billion worth of oil. Not refilling the SPR exposes the US to much greater costs, in terms of economic and national security risks. Those who were around during the 1970’s certainly remember the embargoes and the resulting disruptions that led to the establishment of the SPR.

This is the hole we are in as a result of non-emergency SPR sales for price moderation purposes. Meanwhile, Congress has proposed the following legislation:

The last bill is interesting, but has little chance of passing and would be difficult to implement given other legislative, judicial, and administrative constraints on leasing and production. Having a plan is one thing; implementing it is quite something else.