Chevron slide: Advances in seismic imaging help characterize deepwater development opportunities

A new JPT article features comments from BOE contributor Lars Herbst on advances in HPHT technology, control systems, sensors and transmitters, and automation that are facilitating the next era of deepwater development.

Well capping technology, which provides a tertiary well control capability, is an essential element of post-Macondo exploration and development. Lars points to the importance of BSEE’s unannounced drill program to verify that capping stacks can be transported and installed in a timely manner. Chevron expresses pride in leading a team that deployed and installed a capping stack in 6,200 feet of water in a drill monitored by BSEE. During that drill, a remotely operated vehicle (ROV) closed 10 valves to shut in a simulated well.

Exxon’s Jayme Meier aptly characterizes the challenge and excitement of deepwater development:

“You are floating on a surface, and you have to be able to pinpoint exactly where you’re going to land subsea hardware, exactly where you’re going to moor an FPSO and hit target boxes that are a few feet by a few feet, and they’re 6,000 ft below you,” she said. “It is the most exciting thing that I’ve ever been involved in. And it involves technology, technical know-how, and an ability to really plan the base plan and the contingency plan.”

Advances in deepwater technology are indeed impressive, but continuous improvement must always be the objective. In that regard, Lars rightfully emphasizes the importance of sustaining research through the industry’s up and down cycles.

“In the evolving landscape of Guyana’s oil and gas industry, few have managed to carve out a niche quite like Koaito Grant. A name synonymous with corporate photography, Grant’s journey from discovering his passion for capturing moments to becoming a sought-after photographer within the oil and gas sector is as inspiring as it is instructive.“

So true:“It’s the best feeling when a client reaches out and says you were very highly recommended by this or that person.” His professionalism and work ethic have been key differentiators. “I have a client that always asked if I was Guyanese because I’m always early for all projects and activities.”👍 💯

Reuters has published an interesting article on the Exxon/CNOOC vs. Chevron/Hess dispute scheduled for arbitration next year in Paris. According to Reuters (emphasis added):

“Getting the panel to consider the appraised value is central to Exxon’s claim that the deal is an asset acquisition disguised as a merger. Exxon believes the Guyana asset is so valuable that the merger would trigger a change of control and give Exxon and CNOOC a right of first refusal to the asset sale, the people said.“

The Exxon argument implies that Hess’s only major asset is its share of Stabroek, which is hardly the case. Hess’s 30% Stabroek share is without question an important asset with great long-term potential, but Hess is also a major player elsewhere, most notably in the Bakken formation in North Dakota and the Gulf of Mexico. Implying that Hess was a single asset acquisition is thus misleading:

In Q4 of 2023, Hess produced 194,000 boepd in the Bakken formation vs. a Stabroek share of 128,000 bopd.

In 2023, Hess produced 20 million barrels of oil in the GoM and 40 bcf of gas making them the 8th highest oil producer and 7th highest gas producer.

Hess acquired 20 GoM leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

Chevron and Hess GoM assets have significant potential for synergy. The combined company would be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell).

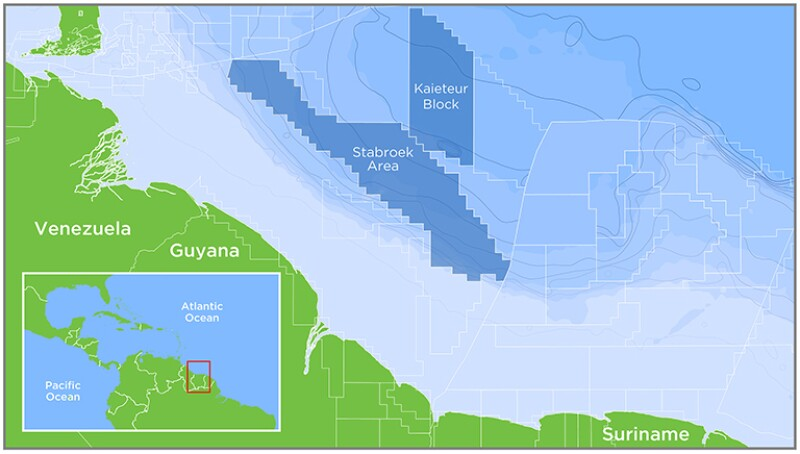

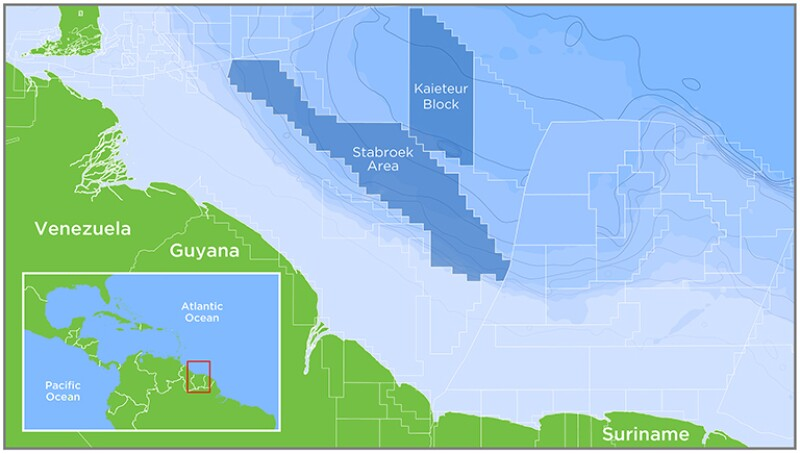

This dispute will continue to smolder given the delay in the arbitration hearings until May 2025. As previously mentioned, I believe the Government of Guyana should have intervened. I’m all for companies settling their disputes privately, but this dispute is over Guyanese resources, and the protracted delay could have implications for Guyana.

Rystad Energy projects a 10% annual compound growth rate for the subsea market from 2024 to 2027, with total spending anticipated to exceed $42 billion by the end of this period.

Brazil dominates the subsea umbilical risers and flowlines (SURF) market. Unsurprisingly, the US is lagging given the absence of a robust offshore leasing program and the dearth of deepwater discoveries in recent years.

An International Chamber of Commerce panel has set a May 2025 date for the hearing on the dispute over Chevron’s acquisition of Hess’s share of Guyana’s Stabroek field. This is a massive delay considering the impact of this arbitration case on Chevron’s purchase of Hess.

As noted in a previous post, the Exxon/CNOOC position seems to be a stretch. Chevron did not buy the Stabroek share; they bought the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership. The panel will decide, but given the May 2025 hearing date, we probably won’t know the outcome for a year.

The Guyanese government has not taken a position in this dispute, but in my opinion, there are reasons for them to be concerned. Stabroek is Guyana’s offshore gem, their most important economic asset. The dispute has to affect teamwork and communication.

From safety, environmental, and production standpoints, do you want feuding partners managing such an important national asset? Those are Guyanese resources that the Stabroek partners are licensed to produce. I would have liked to have seen the government tell them to get this resolved in 30 days or we’ll resolve it for them.

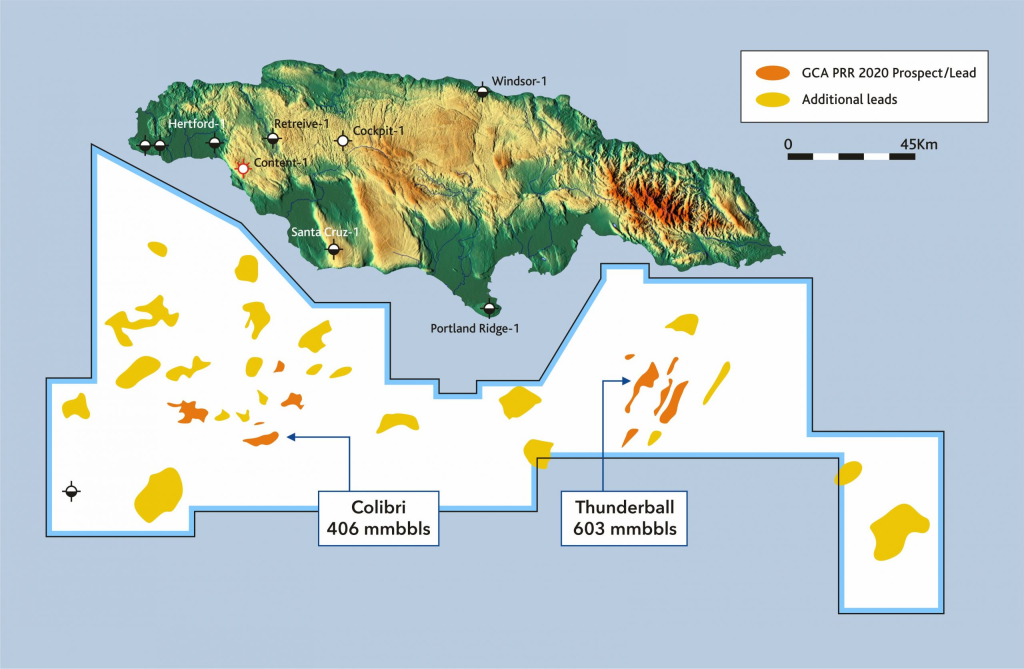

United Oil and Gas excels at promotion and isn’t shy about making bold statements. Can they find a strong partner and move their Jamaican exploration program forward?

The term “string of pearls” was used about 30 years ago to describe discoveries in the Beaufort Sea and on adjacent Alaska lands. Although they were modest individually (by Arctic standards), the sense was that these discoveries would collectively support sustained production in the region. While there has been some success in that regard, the optimistic expectations have not been realized.

Below is a recent United Oil & Gas presentation to prospective investors. Previous Jamaica posts.

The government’s decision to require that a capping stack be located in Guyanais prudent. Although the need for a capping stack is dependent on multiple barrier failures and is thus extremely low, the environmental and economic consequences of a prolonged well blowout warrant timely access to this tertiary well control option.

A capping stack must be properly maintained and deployable without delay. In that regard, BSEE has a good program for testing Gulf of Mexico capping stack readiness. Capping stack drills are an important post-Macondo addition to the unannounced oil spill response program that dates back to 1981.

“Troy Naquin, BSEE New Orleans District, observes as a capping stack is carefully lowered onto the deck of ship to be transported more than 100 miles offshore for a drill designed to test industry’s ability to successfully deploy it in case of an emergency, May 8, 2023.” BSEE photo/Bobby Nash

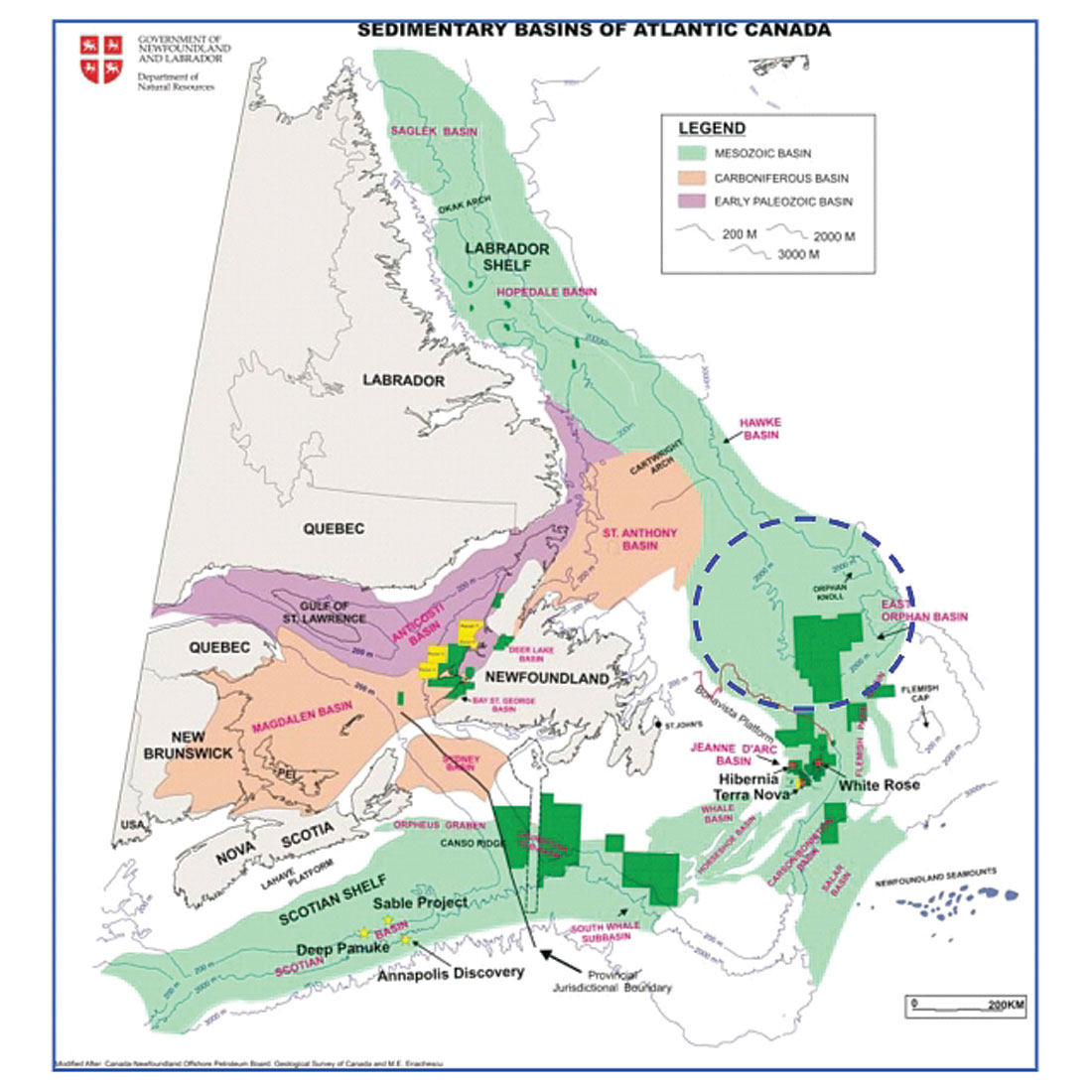

The DrillMAX is en route from Guyana to drill the Persephone wildcat well 500 km NE of Newfoundland in the highly prospective Orphan basin (3000 m water depth). This looks like the farthest from shore any well has been drilled in the Atlantic. The late spring date is prudent.This is definitely a well to watch because of the resource potential and difficult operating conditions.

As we wait for the International Chamber of Commerce (ICC) arbitration panel to rule on the Exxon-CNOOC-Chevron-Hess Stabroek dispute, key excerpts from Chevron’s SEC filing about their merger with Hess are pasted below. The text highlighted in red is particularly interesting.

If the ICC arbitration panel rules that the right-of-first-refusal (ROFR) provision applies, the Chevron filing says that the merger is off and Hess continues as Stabroek’s 30% owner. If that statement is correct, Exxon and CNOOC cannot obtain the Hess share. Their only benefit from the challenge would be to deny their rival Chevron from participating in the block or to receive payment from Chevron for approving the ownership change.

It’s also noteworthy that Exxon initially showed support for the deal (quote below).

p. 32: With respect to the Stabroek ROFR (as defined in the section entitled “The Merger—Stabroek JOA”), if the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close. Some of these conditions are not in Hess’ or Chevron’s control.

Further, subject to any then ongoing arbitration relating to the Stabroek JOA, either Chevron or Hess may terminate the merger agreement if the merger has not been completed by October 22, 2024, (or April 22, 2025 or October 22, 2025, if the applicable end date is extended pursuant to the merger agreement) or by such later date as the parties may mutually agree.

p. 81: The Stabroek JOA contains a right of first refusal (the “Stabroek ROFR”) provision that, if applicable to a change of control transaction and properly exercised, provides the Stabroek Parties with a right to acquire the participating interest in the Stabroek Block held by the Stabroek Party subject to such transaction (at a value that is based on the portion of the value of the change of control transaction that reasonably should be allocated to such participating interest and is increased to reflect a tax gross-up) only after, and conditioned on, the closing of such transaction. Chevron and Hess believe that the Stabroek ROFR does not apply to the merger due to the structure of the merger and the language of the Stabroek ROFR provisions.

p. 82: On October 24, 2023, shortly after the merger was announced, Exxon issued the following statement, indicating its support for the merger: “Hess has been a valued partner in Guyana since 2014 and we look forward to continuing our successful operations in the Stabroek block with Chevron, pending the deal closing.” However, Exxon and CNOOC subsequently informed Chevron and Hess that they believe the Stabroek ROFR applies to the merger. Hess, Chevron, Exxon and CNOOC subsequently engaged in discussions regarding the applicability of the Stabroek ROFR to the merger.

If the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close, and, pursuant to the terms of the Stabroek JOA, the Exxon affiliate and the CNOOC affiliate would cease to have rights under the Stabroek ROFR with respect to the merger. In that event, Hess would remain an independent public company and would continue to own its participating interest in the Stabroek Block. Based on the express terms of the Stabroek JOA, Chevron and Hess do not believe there is any material likelihood that the circumstances described in this paragraph will occur.

p. 118: In addition, with respect to the Stabroek ROFR, if the arbitration does not result in a confirmation that the Stabroek ROFR does not apply to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close.