Every deepwater platform installed since Feb. 2018, when Chevron installed its Big Foot tension leg platform (TLP), has been a Floating Production Unit (aka FPU or production semisubmersible). During that period, no new SPARs, FPSOs, or TLPs were installed.

The list (below) of these simpler, safer, greener FPUs has grown by two with the initiation of production at Shenandoah and Salamanca. Note the water depth range from 3725 to 8600 ft.

platform

operator

water depth (ft)

first production

Appomattox

Shell

7400

May 2019

King’s Quay

Murphy

3725

April 2022

Vito

Shell

4050

Feb 2023

Argos

bp

4440

April 2023

Anchor

Chevron

4600

Aug 2024

Whale

Shell

8600

Jan 2025

Shenandoah

Beacon

5840

July 2025

Salamanca

LLOG

6405

Sept 2025

The efficiencies achieved with the simpler platform designs combined with the high pressure (>15,000 psi) technology developed over the past 2 decades is facilitatihg production from the highly prospective Paleogene (Wilcox) deepwater fans. (For those interested in learning more about the geology, see the excellent presentation by Dr. Mike Sweet, Univ. of Texas, that is embedded in this post.)

All of the operators note the cost-saving similarities in their FPU designs. For example, Vito and Whale are very much the same despite the 4550′ difference in water depth.

Meanwhile, two new floating production units, Beacon’s Shenandoah and LLOG’s Salamanca are now on line. More on this and bp’s Tiber announcement in an upcoming post.

NOAA is touting marine aquaculture and has published Programmatic Environmental Impact Statements for Aquaculture Opportunity Areas (AOAs) in the Gulf of America and offshore Southern California. This is a positive step.

While the focus of these EIS documents is on distinct AOAs separated from oil and gas facilities, NOAA might also have discussed the potential for synergy with existing platforms. The reef effect of platforms can be sustained and new fishery ventures supported by converting older platforms to aquaculture facilities (Rigs-to-Roe/Redfish/Rockfish) rather than decommissioning them.

According to a paper published in 2014 by marine ecologist Dr. Jeremy Claisse of Cal Poly Pomona, the oil and gas platforms off the coast of California are the most productive marine habitats per unit area in the world. “Even the least productive platform was more productive than Chesapeake Bay or a coral reef in Moorea,” said Dr. Love. (Milt Love, UCSB biologist)

The table below captures the shorter public comments and provides links to the longer ones. They are listed in the order they were posted on Regulations.gov.

commenter

summary/link

anonymous

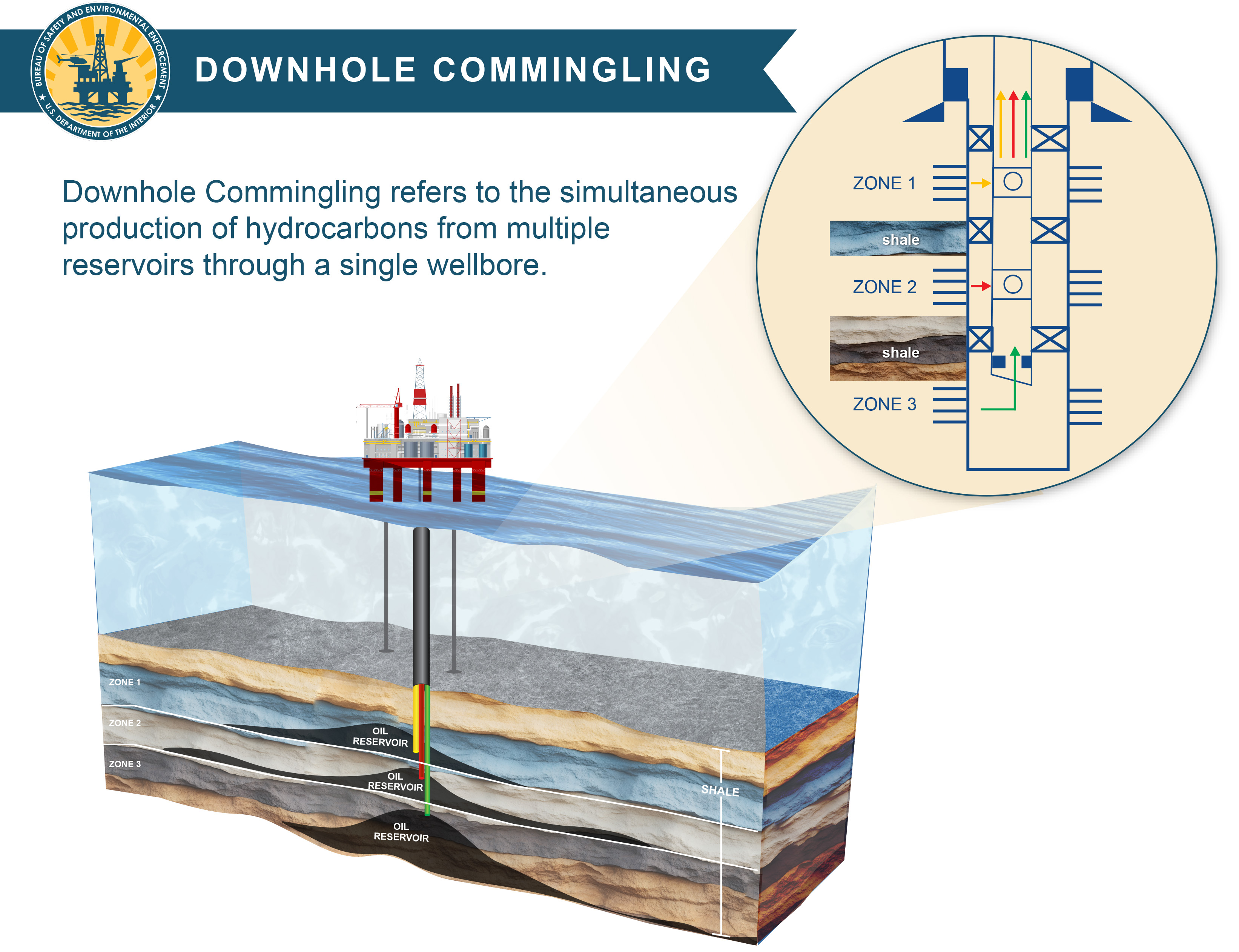

I recommend under no circumstance that we allow the onsite worker to approve the commingling of bore holes because there is extreme significant safety and environmental hazards that exist. The best alternative is to have an environmental engineer and environmental scientist approve any commingling

…your regulatory proposal is inconsistent with the federal law, the best available science on protecting the health and lives of children, and the legal mandate that agency decision-making does not deprive children of their fundamental constitutional rights…

I support updating the regulations to align with the One Big Beautiful Bill Act, but I encourage BSEE to ensure that safety standards and environmental protections remain the highest priority in all commingling approvals. Clear guidance for industry compliance and transparent public reporting would also strengthen confidence in this rule.

Ananda Foster

Regulations need to catch up with technology and we have not had a chance to do that yet. If you allow them on throttle access, they will destroy it. We all rely on the ocean, how can you do this to your own constituents?

Legislatively dictating well construction, completion, or operational approvals is a redline for me, and I continue to strongly believe the downhole commingling rule should be published as a draft for public review and comment.

The only industry comments are from API and bp America. Both support the direct final rule, and I respect their position. My main quarrel is with the legislative action that put us in this position.

I have had many disagreements with API members over the years, but the dialogue has always been professional. Technical and policy disagreements are healthy for the OCS program, and I will continue to raise potential issues and concerns on this blog.

With regard to bp, I have been impressed by their commitment to the Gulf of America, as summarized in this excerpt from their comments:

The attached comments were submitted to Regulations.gov on 9/8/2025.

Legislatively dictating downhole commingling approvals, as per Section 50102 of the One Big Beautiful Bill, is a reckless precedent from both technical and regulatory policy standpoints.

This type of legislative maneuver compromises the integrity of the OCS oil and gas program and the companies that participate in it. Shaving the maximum royalty rate was one thing; mandating well completion approvals is quite something else. Disappointing. ☹

John Borne was an exceptional engineer and offshore safety leader in our OCS oil and gas program during the US Geological Survey (Conservation Div.) and Minerals Management Service (MMS) eras.

Some thoughts on John’s leadership followed by tributes from distinguished colleagues:

John’s Houma District office was a model for the rest of the OCS program. Houma was the program’s busiest district in terms of operational activity, and the most effective in meeting permitting, inspection, and investigation targets.

The few serious accidents that occurred in the District were carefully investigated and the findings were shared in a timely manner with the goal of preventing their recurrence. If John signed a report, you knew it was complete and accurate.

John was knowledgeable about the complex offshore oil and gas operations he regulated, and was an outstanding teacher and mentor.

John treated all companies the same from the super-majors to the small independents – no biases, no favors, and no ethics issues.

John expected companies to fully comply with the regulations. Any departures had to be clearly in the best interest of safety and the environment.

From Ken Arnold (ex-Shell engr, Paragon Engineering President, NAE): As part of the Shell Training program in 1964 I was assigned to trail John in East Bay for a week. One night I was talking to another trainee on a logging barge tied up to a posted barge rig in SP Blk 24. John was also on the barge. Without warning the barge started pulling away from the rig. The three of us jumped from the barge to the rig but I slipped and fell in the canal. I don’t think I was in the water long enough to get wet, when John and a rig hand fished me out. Unfortunately my glasses fell off and were in the mud. John got a scissors device and retrieved my glasses in a matter of minutes.

I greatly appreciated my week with John. What he took the time to teach me about field work was critical to my subsequent successful career in Shell and in Paragon. He was a gentleman and a first class teacher. I was lucky to have known him.

Jodie Connor (founder and retired President of J. Connor Consulting): John was an excellent representative of the MMS, always fair in his decision-making and approvals. I endearingly called him “By the Book Borne”. He enforced the regulations as they were written, which was fair to all operators. Always kind and willing to explain MMS policies.

Lars Herbst (retired MMS/BSEE Regional Director, Gulf of Mexico): What a legend at MMS! A testament to his leadership are the number of Regional leaders that came out of Houma District. Just to name a few: Mike Saucier, Bryan Domangue, Troy Trosclair, and even Jack Leezy! That work ethic that John instilled has continued even to the next generation of leadership! I was fortunate that John let me act as Drilling Engineer when Saucier went hunting each December. My career at MMS was never the same after that opportunity!

Jack Leezy: (President, Avenger Consulting, retired MMS): John served in the Marine Corp during the Korean war. Upon discharge from the Marine Corp John attend the University of Lafayette and earned a BS degree in Petroleum Engineering. John started his oilfield career when he went to work for Shell Oil in 1960 until 1970 as a Petroleum Engineer.

John joined U.S.G.S. In 1970 as a Petroleum Engineer in the Lafayette District. John accepted a promotion in 1972 in the Regional office and was selected as the first District Supervisor in the newly formed Houma District office in October1974. John remained as the District Supervisor until his retirement in 1995. John was instrumental in developing Bureau policies of which some are still in place as of today. John served on countless MMS and industry committees alike during his career. John was looked upon as professional and highly respected by MMS and industry alike. He performed is duties in such a way that even if you may not have liked his decision, you respected it. John’s demeanor never changed as he never lost his composure and worked evenly though all the trials and tribulations during his career at MMS. John even won MMS’s Engineer of the Year award. I owe a lot to John in helping me form my career at MMS as I tried to handle my supervisory duties in the same manner in which John did.

RIP John. You were a superstar! As an engineer, regulator, leader, teacher, and colleague, no one did it better!

The latest Baker Hughes Rig Count Report shows only 10 rigs actively drilling in the Gulf. All are at deepwater locations – 7 in the Mississippi Canyon area, 2 in Green Canyon, and 1 in Alaminos Canyon. Per the BSEE borehole file, Shell accounts for most of the current MS Canyon wells and the Alaminous Canyon well. Beacon is also drilling in the MS Canyon, and the Green Canyon well appears to be a Chevron operation.

Only Anadarko/Oxy, Beacon/BOE, BP, Chevron/Hess, Shell, and Talos have spudded deepwater exploratory wells in 2025 YTD. Arena and Cantium are the only shelf drillers – all development wells.

Technological advances and extensions of past discoveries have sustained Gulf production, but declines are certain over the longer term if drilling activity doesn’t increase. Oil price uncertainty is an issue, but that’s always the case. Semiannual lease sales are now legislatively required and the terms will be attractive, so those issues are off the table. Let’s see what the bidding looks like at the upcoming sale.

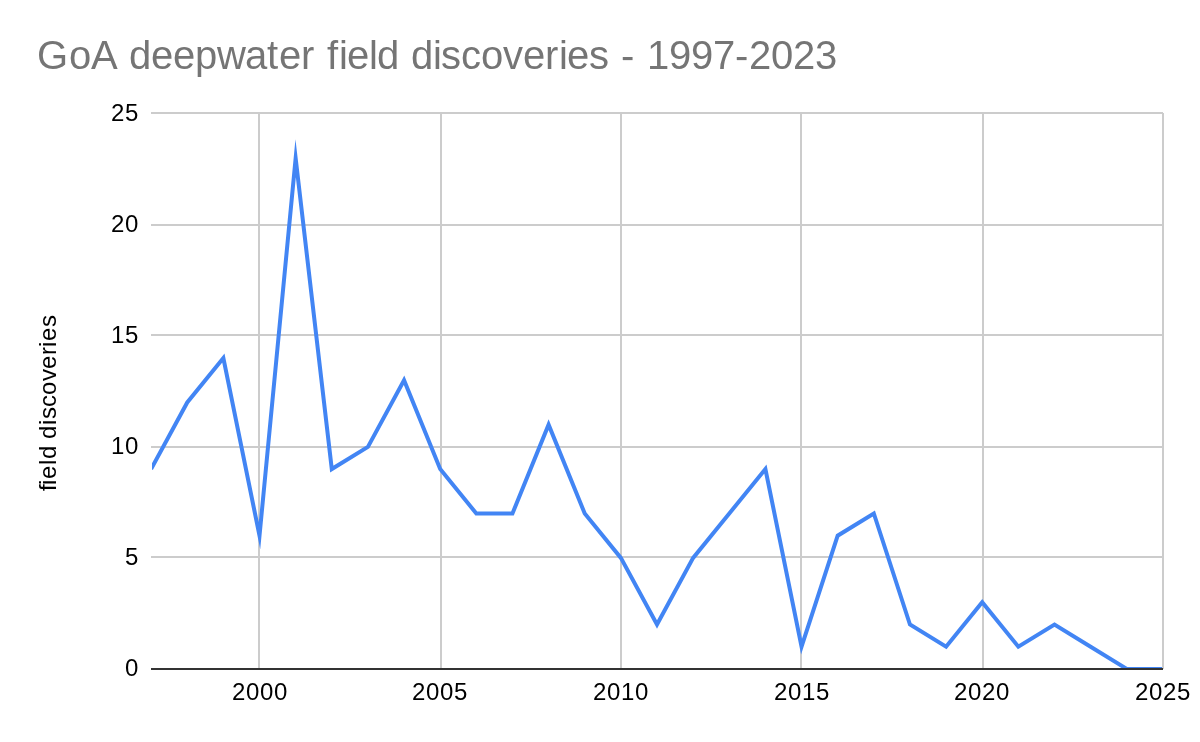

The decline in deepwater discoveries (BOEM data below) is particularly discouraging. Per BOEM, the last deepwater field discovery was in March 2023.

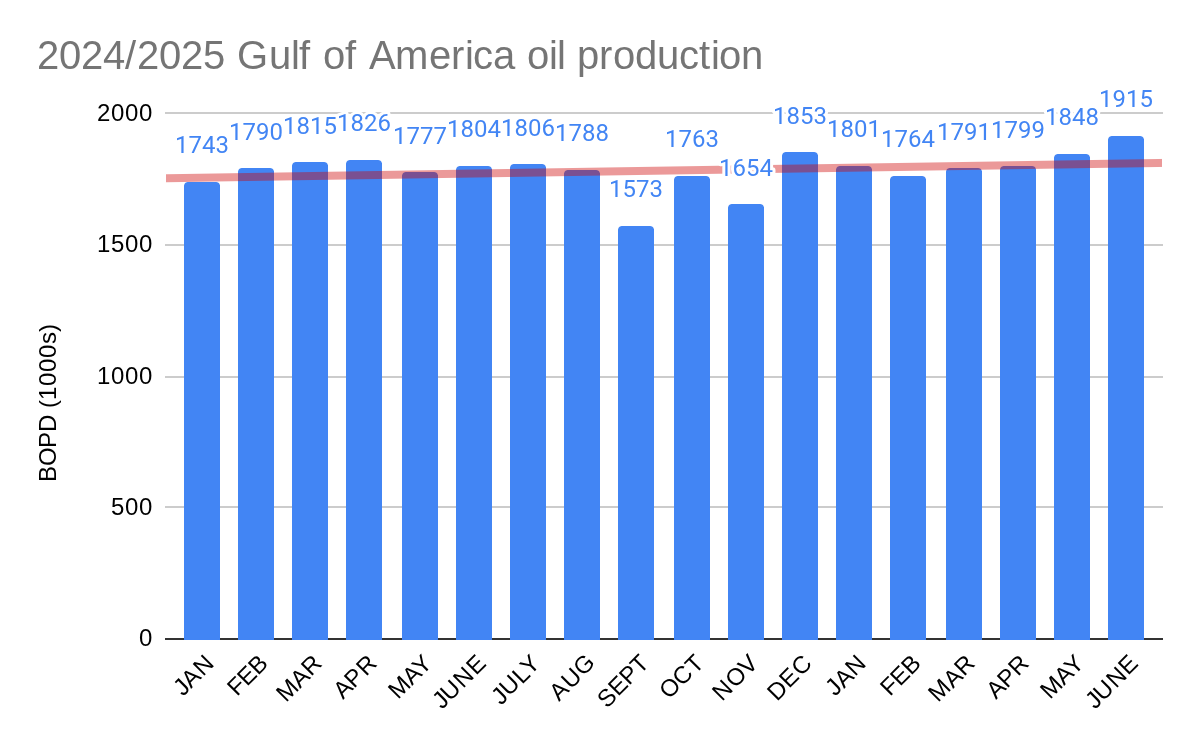

The average oil production rate for the Gulf OCS was 1.915 million bopd in June, the highest rate since Oct. 2023 and thus the highest in the history of the Gulf of America 😉.

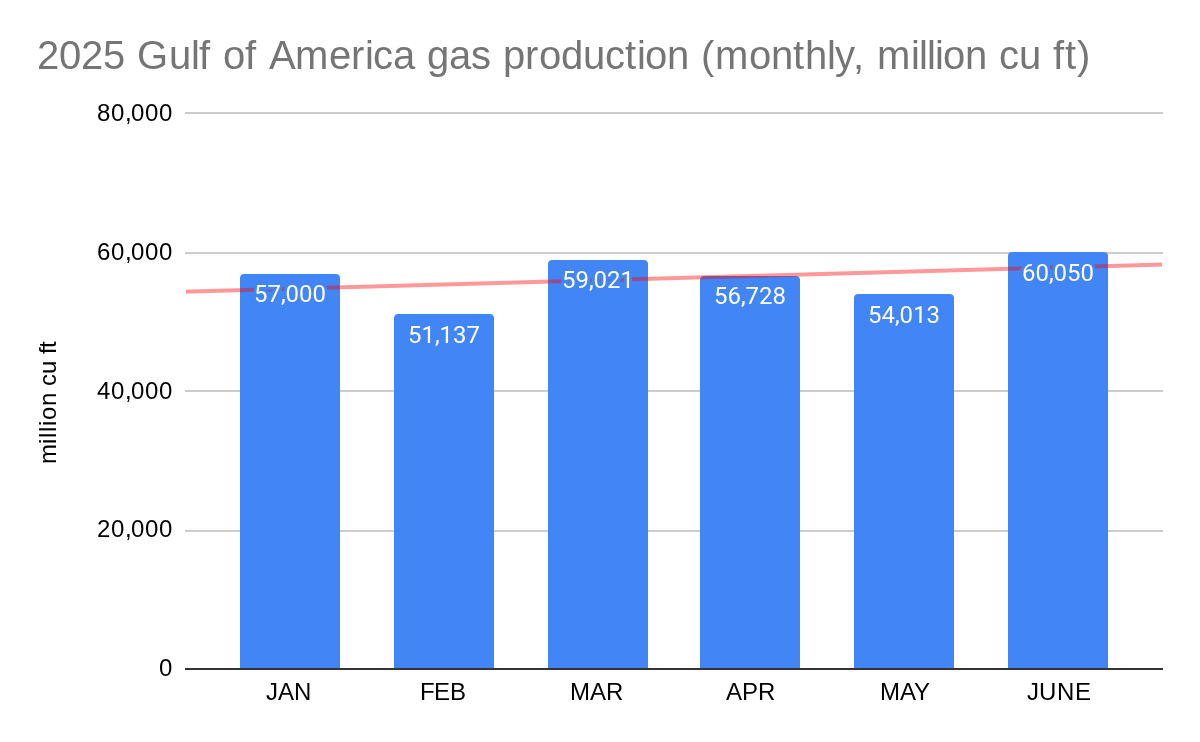

Natural gas production, which is now primarily from oil wells (i.e. associated gas) and is thus more closely linked to oil production rates, increased by >10% in June to over 60 bcf. As was the case for oil, gas production was the highest since Oct. 2023.

It is now peak hurricane season, so the eyes of production forecasters are focused on the tropics. Few need to be reminded about what happened 20 years ago when Hurricanes Katrina and Rita roared through the Gulf, preceded by Hurricane Ivan “The Terrible” one year earlier. Those 3 hurricanes triggered major improvements in hurricane preparedness, particularly with regard to stationkeeping capabilities.

The “One Big Beautiful Bill Act of 2025” (OBBB), Public Law 119-21, which was signed into law on July 4, 2025, includes a significant offshore production directive (section 50102) that has received little public attention:

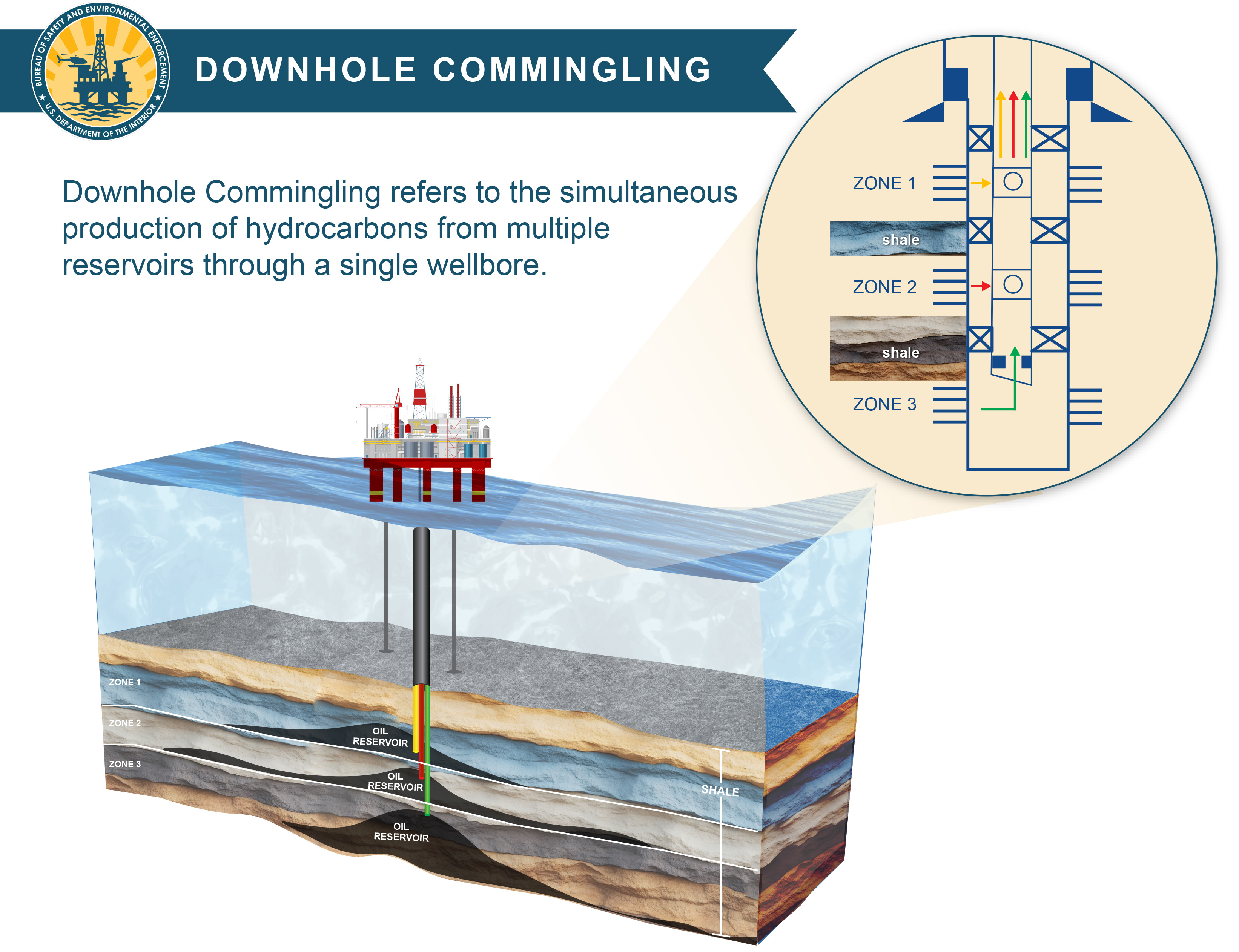

“The Secretary of the Interior shall approve a request of an operator to commingle oil or gas production from multiple reservoirs within a single wellbore completed on the outer Continental Shelf in the Gulf of America Region unless the Secretary of the Interior determines that conclusive evidence establishes that the commingling—(1) could not be conducted by the operator in a safe manner; or (2) would result in an ultimate recovery from the applicable reservoirs to be reduced in comparison to the expected recovery of those reservoirs if they had not been commingled.”

This is, to the best of my knowledge, the first time in the history of the OCS oil and gas program that Congress has directed the safety regulator to approve well completion practices that could increase safety, environmental, and resource conservation risks.

Rather than calling for the operator to demonstrate that a downhole commingling plan is safe and optimizes resource recovery, the plan must be approved unless BSEE proves conclusively that the operation could not be conducted safely or that resource recovery would be reduced. This is the antithesis of the operator responsibility doctrine, a fundamental principle of the OCS regulatory program, and safety management principles that call for the operator to demonstrate that safety, environmental, and resource conservation risks have been effectively addressed.

Only 40 days after the OBBB was signed, BSEE published a direct final rule implementing the downhole commingling directive. This is warp speed for promulgating a Federal regulation! In keeping with the rush to finalize the rule, the preamble asserts that “notice and comment are unnecessary because this rule is noncontroversial; of a minor, technical nature; and is unlikely to receive any significant adverse comments.”

I intend to submit comments prior to the Sept. 12 deadline. These comments will assert that the rule does not qualify for an exemption from the Administrative Procedures Act’s public review and comment requirement. I will also recommend that BSEE consider hosting a public forum during the comment period to present their research on downhole commingling and discuss the risk mitigations.

Below are some of the issues/questions that should be considered during the public comment period:

BSEE’s own fact sheet acknowledges the well-known pressure differential, crossflow, and fluid compatibility risks associated with downhole commingling. The public should have the opportunity to provide input on the extent to which “intelligent completions” and other production technology are effective in mitigating these risks.

The industry-funded Univ. of Texas (UT) study, which led to a relaxation of downhole commingling restrictions, was specific to the “unique Paleogene Gulf of Mexico fields.” Does BSEE have evidence that supports the applicability of the study to other fields?

The authors of the UT study acknowledged that their findings were based on a “simple but reasonable geological base case model.” They also acknowledged the need for “a more comprehensive study using advanced geological models to explore additional geological features.” What are BSEE’s plans for additional research?

Should an independent assessment of Gulf of America downhole commingling safety and resource recovery risks be conducted before finalizing a rule that essentially mandates approval of all applications?

BSEE’s April 2025 policy change raised the allowable pressure differential for commingling production in Paleogene (Wilcox) reservoirs from 200 psi to 1500 psi. Unlike the policy update, the new rule includes no boundaries whatsoever.

What criteria will BSEE use in determining that there is “conclusive evidence” that a commingling request would be unsafe or would reduce ultimate resource recovery? Will BSEE disapprove any requests outside the parameters in the current policy guidance or subsequent updates?

There are many more issues that remain to be discussed, which is why the downhole commingling rule should be published in draft form, with a comment period of at least 90 days.

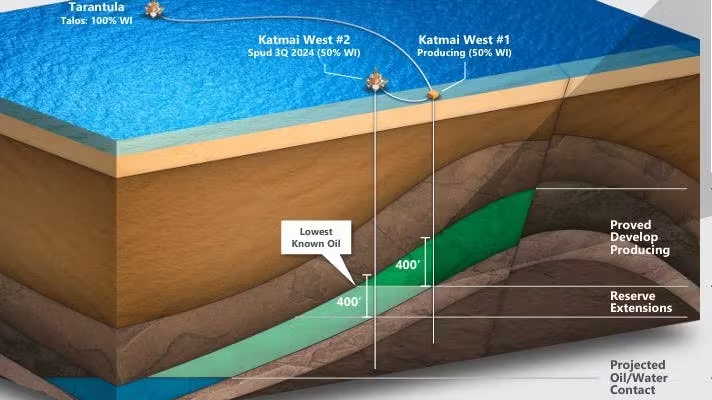

Talos announced successful drilling results at the Daenerys prospect (Katmai West #2) in the Gulf of America (Walker Ridge blocks 106, 107, 150, and 151).

Daenerys is a good example of the evolution of deepwater project ownership, which was once exclusively the domain of major international oil companies. Over the past 20 years, participation by independents increased gradually, followed by smaller independents and informed investment companies.

Impressively, the Daenerys partnership (table below) includes a tribe that has the same % ownership as a super-major, and a highly efficient investment company owned by a single person.

Talos (operator)

large US independent

27.0% share

Shell

international supermajor

22.5%

Red Willow

private company owned by the Southern Ute Tribe

22.5%

Houston Energy

private independent focused on deepwater energy resources