An International Chamber of Commerce panel has set a May 2025 date for the hearing on the dispute over Chevron’s acquisition of Hess’s share of Guyana’s Stabroek field. This is a massive delay considering the impact of this arbitration case on Chevron’s purchase of Hess.

As noted in a previous post, the Exxon/CNOOC position seems to be a stretch. Chevron did not buy the Stabroek share; they bought the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership. The panel will decide, but given the May 2025 hearing date, we probably won’t know the outcome for a year.

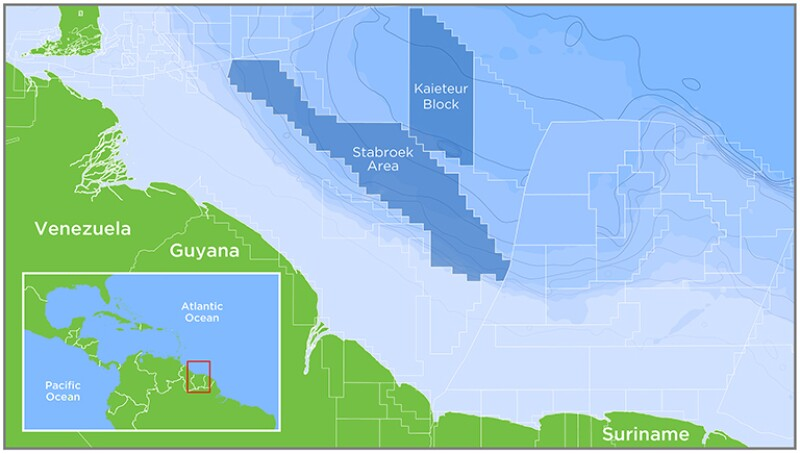

The Guyanese government has not taken a position in this dispute, but in my opinion, there are reasons for them to be concerned. Stabroek is Guyana’s offshore gem, their most important economic asset. The dispute has to affect teamwork and communication.

From safety, environmental, and production standpoints, do you want feuding partners managing such an important national asset? Those are Guyanese resources that the Stabroek partners are licensed to produce. I would have liked to have seen the government tell them to get this resolved in 30 days or we’ll resolve it for them.

As we wait for the International Chamber of Commerce (ICC) arbitration panel to rule on the Exxon-CNOOC-Chevron-Hess Stabroek dispute, key excerpts from Chevron’s SEC filing about their merger with Hess are pasted below. The text highlighted in red is particularly interesting.

If the ICC arbitration panel rules that the right-of-first-refusal (ROFR) provision applies, the Chevron filing says that the merger is off and Hess continues as Stabroek’s 30% owner. If that statement is correct, Exxon and CNOOC cannot obtain the Hess share. Their only benefit from the challenge would be to deny their rival Chevron from participating in the block or to receive payment from Chevron for approving the ownership change.

It’s also noteworthy that Exxon initially showed support for the deal (quote below).

p. 32: With respect to the Stabroek ROFR (as defined in the section entitled “The Merger—Stabroek JOA”), if the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close. Some of these conditions are not in Hess’ or Chevron’s control.

Further, subject to any then ongoing arbitration relating to the Stabroek JOA, either Chevron or Hess may terminate the merger agreement if the merger has not been completed by October 22, 2024, (or April 22, 2025 or October 22, 2025, if the applicable end date is extended pursuant to the merger agreement) or by such later date as the parties may mutually agree.

p. 81: The Stabroek JOA contains a right of first refusal (the “Stabroek ROFR”) provision that, if applicable to a change of control transaction and properly exercised, provides the Stabroek Parties with a right to acquire the participating interest in the Stabroek Block held by the Stabroek Party subject to such transaction (at a value that is based on the portion of the value of the change of control transaction that reasonably should be allocated to such participating interest and is increased to reflect a tax gross-up) only after, and conditioned on, the closing of such transaction. Chevron and Hess believe that the Stabroek ROFR does not apply to the merger due to the structure of the merger and the language of the Stabroek ROFR provisions.

p. 82: On October 24, 2023, shortly after the merger was announced, Exxon issued the following statement, indicating its support for the merger: “Hess has been a valued partner in Guyana since 2014 and we look forward to continuing our successful operations in the Stabroek block with Chevron, pending the deal closing.” However, Exxon and CNOOC subsequently informed Chevron and Hess that they believe the Stabroek ROFR applies to the merger. Hess, Chevron, Exxon and CNOOC subsequently engaged in discussions regarding the applicability of the Stabroek ROFR to the merger.

If the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close, and, pursuant to the terms of the Stabroek JOA, the Exxon affiliate and the CNOOC affiliate would cease to have rights under the Stabroek ROFR with respect to the merger. In that event, Hess would remain an independent public company and would continue to own its participating interest in the Stabroek Block. Based on the express terms of the Stabroek JOA, Chevron and Hess do not believe there is any material likelihood that the circumstances described in this paragraph will occur.

p. 118: In addition, with respect to the Stabroek ROFR, if the arbitration does not result in a confirmation that the Stabroek ROFR does not apply to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close.

Canadian and US approvals were granted and CNOOC acquired Nexen (Canada) in 2013.

Nexen’s Guyana interest was not mentioned in the press announcement, and appears to have been a rather minor consideration in the acquisition.

So, an apparent afterthought in CNOOC’s takeover of Nexen has (1) proven to be extremely profitable, (2) given the company and the Chinese government leverage in the Exxon-Chevron supermajor dispute, and (3) opened the door for CNOOC to increase their interest in the massive Stabroek field.

Are Exxon and Chinese partner (CNOOC) attempting to use Chevron’s acquisition of Hess to improve their already lucrative position in Guyana’s prolific Stabroek block?

The Stabroek operating agreement outlines terms for Hess, Exxon, and CNOOC to explore and develop the block.

This Stabroek agreement includes a right of first refusal (ROFR) provision which allows the parties to buy out the stake of one of them in the event of a ‘change of control’ transaction.

Chevron and Hess argue that the merger’s structure does not trigger the ROFR clause.

Exxon and CNOOC argue that the clause applies. This could force Hess to offer its stake in the Stabroek block to its partners first.

The Exxon/CNOOC position seems to be a stretch. Chevron did not buy the Stabroek share; they bought the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership.

As an offshore operator, Exxon has been highly responsible from a safety standpoint. However, the company has a shown tendency to stretch the envelope when it comes to contract rights. The most recent example was their acquisition of 163 GoM oil and gas leases for carbon disposal purposes, contrary to the terms of the sale notice and lease contracts.

Of course, the 3 Stabroek Block partners who are responsible for this production – Exxon (45%), Hess (30%), and CNOOC (25%) – are also doing quite well. If you are wondering about this curious mix of companies – a US supermajor, a large US independent, and a state-owned Chinese mega-company – this OilNow post explains what happened.

Initially, Exxon and Shell were 50/50 partners in the Stabroek Block. Shell thought the chances for success were slim and opted out a year before the world class Liza discovery (ouch!). After Shell departed, Exxon sent “at least 35 letters” to prospective partners and only Hess and CNOOC responded favorably (actually, it was Nexen, not CNOOC that responded). The Liza discovery followed and the rest is history.

Will exploration offshore Jamaica and Barbados also prove successful? Stay tuned.