As posted in January, most analysts predicted that Chevron and Hess would prevail. Now that the arbitration panel has ruled, Chevron’s acquisition of Hess can be completed.

The position of Exxon and its partner, Chinese govt owned CNOOC, never made much sense given that Chevron was not buying the Stabroek share, they were buying the company that holds that share.

Not much attention has been paid to the importance of Chevron’s acquisition of Hess’s Gulf of America assets. The combined company will be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell). Hess acquired 20 GoA leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

Exxon senior vice president Neil Chapman said he was confident that a three-member arbitration panel would rule in Exxon’s favor and determine it had a right-of-first-refusal to purchase Hess’ stake in a Guyana oil joint venture operated by Exxon.

Hess: “We remain confident that the arbitration will confirm the Stabroek right of first refusal does not apply to the merger.”

The 2024 Gulf of America Safety Compliance Leaders are ranked below according to the number of incidents of non-compliance (INCs) per facility inspection. To be ranked, a company must:

operate at least 2 production platforms

have drilled at least 2 wells during the year

average <1 INC for every 3 facility inspections (0.33 INCs/facility inspection)

average <1 INC for every 10 inspections (0.1 INCs/inspection). Note that each facility inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc). In 2024, there were on average 3.4 inspections for every facility inspection.

District investigation reports are more timely and provide additional insights into safety performance. Impressively, Hess had no incidents warranting a District investigation, and was the only ranked operator with this distinction. I will comment more on the District reports in a future post

Chevron’s 2024 compliance record was among the best in the history of the US OCS oil and gas program. Was it the absolute best? Were it not for the FSI INC at a Unocal (Chevron) facility, one could unequivocally assert that it was. Further evaluation of that INC would be helpful. However, details on specific INCs are not publicly available, so the significance of that violation cannot be evaluated.

operator

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

Chevron

1

0

1

2

117

0.02

311

0.006

BP

2

3

0

5

93

0.05

251

0.02

Anadarko

8

9

1

18

143

0.13

344

0.05

Hess

2

3

0

5

26

0.19

67

0.07

Walter

6

4

1

11

50

0.22

161

0.07

Shell

23

17

5

45

199

0.23

495

0.09

Cantium

24

8

0

32

123

0.26

537

0.06

Murphy

8

9

1

18

70

0.26

191

0.09

Arena

29

28

3

60

189

0.32

803

0.07

Gulf-wide

957

398

109

1464

3133

0.47

10664

0.14

Notes: Numbers are from published BSEE data; INC=incident of non-compliance; W=warning INC; CSI=component shut-in INC; FSI=facility shut-in INC; INCs/fac insp= INCs issued per facility inspection; each facility-inspection may include multiple types of inspections (e.g. production, pipeline, pollution, Coast Guard, site security, etc), in 2024, there were on average 3.4 inspections for every facility inspection

Not meeting the production facilities requirement to be ranked among the top performers, but nonetheless noteworthy, was the compliance record of BOE Exploration & Production (no relation to the BOE blog 😀). See their impressive inspection results below:

W

CSI

FSI

total INCs

facility insp

INCs/ fac insp

insp

INCs/ insp

BOE

1

1

0

2

21

0.1

48

0.04

Transparency on inspections and incidents is important for a program that is dependent on public confidence. For independent observers to better evaluate industry-wide and company-specific safety performance, publication of the following information should be considered:

quarterly updates of the incident tables, as was once common practice

posting of violation summaries for inspections resulting in the issuance of one or more INCs

Chevron is not buying the Stabroek share; they are buying the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership.

As an offshore operator, Exxon has been highly responsible from a safety standpoint. However, the company is not reluctant to stretch the envelope when it comes to contract rights. The most recent example was their acquisition of 163 GoM oil and gas leases for carbon disposal purposes, contrary to the terms of the sale notice and lease contracts.

Interestingly, Exxon’s partner in this dispute is state-owned China National Offshore Oil Corporation. CNOOC acquired their 25% Stabroek share when they purchased Nexen, a Canadian company (sound familiar?). Both the Canadian and US governments had reservations about this acquisition and nearly nixed the deal. Would either government bless that acquisition today?

An International Chamber of Commerce arbitration panel will hear the Stabroek case in May 2025, and the final decision is expected by September 2025.

Reuters has published an interesting article on the Exxon/CNOOC vs. Chevron/Hess dispute scheduled for arbitration next year in Paris. According to Reuters (emphasis added):

“Getting the panel to consider the appraised value is central to Exxon’s claim that the deal is an asset acquisition disguised as a merger. Exxon believes the Guyana asset is so valuable that the merger would trigger a change of control and give Exxon and CNOOC a right of first refusal to the asset sale, the people said.“

The Exxon argument implies that Hess’s only major asset is its share of Stabroek, which is hardly the case. Hess’s 30% Stabroek share is without question an important asset with great long-term potential, but Hess is also a major player elsewhere, most notably in the Bakken formation in North Dakota and the Gulf of Mexico. Implying that Hess was a single asset acquisition is thus misleading:

In Q4 of 2023, Hess produced 194,000 boepd in the Bakken formation vs. a Stabroek share of 128,000 bopd.

In 2023, Hess produced 20 million barrels of oil in the GoM and 40 bcf of gas making them the 8th highest oil producer and 7th highest gas producer.

Hess acquired 20 GoM leases in Sale 261, ranking first in total high bids ($88 million) among all participants.

Chevron and Hess GoM assets have significant potential for synergy. The combined company would be the 3rd largest GoM oil producer (behind Shell and bp) and the second largest gas producer (behind only Shell).

This dispute will continue to smolder given the delay in the arbitration hearings until May 2025. As previously mentioned, I believe the Government of Guyana should have intervened. I’m all for companies settling their disputes privately, but this dispute is over Guyanese resources, and the protracted delay could have implications for Guyana.

An International Chamber of Commerce panel has set a May 2025 date for the hearing on the dispute over Chevron’s acquisition of Hess’s share of Guyana’s Stabroek field. This is a massive delay considering the impact of this arbitration case on Chevron’s purchase of Hess.

As noted in a previous post, the Exxon/CNOOC position seems to be a stretch. Chevron did not buy the Stabroek share; they bought the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership. The panel will decide, but given the May 2025 hearing date, we probably won’t know the outcome for a year.

The Guyanese government has not taken a position in this dispute, but in my opinion, there are reasons for them to be concerned. Stabroek is Guyana’s offshore gem, their most important economic asset. The dispute has to affect teamwork and communication.

From safety, environmental, and production standpoints, do you want feuding partners managing such an important national asset? Those are Guyanese resources that the Stabroek partners are licensed to produce. I would have liked to have seen the government tell them to get this resolved in 30 days or we’ll resolve it for them.

As we wait for the International Chamber of Commerce (ICC) arbitration panel to rule on the Exxon-CNOOC-Chevron-Hess Stabroek dispute, key excerpts from Chevron’s SEC filing about their merger with Hess are pasted below. The text highlighted in red is particularly interesting.

If the ICC arbitration panel rules that the right-of-first-refusal (ROFR) provision applies, the Chevron filing says that the merger is off and Hess continues as Stabroek’s 30% owner. If that statement is correct, Exxon and CNOOC cannot obtain the Hess share. Their only benefit from the challenge would be to deny their rival Chevron from participating in the block or to receive payment from Chevron for approving the ownership change.

It’s also noteworthy that Exxon initially showed support for the deal (quote below).

p. 32: With respect to the Stabroek ROFR (as defined in the section entitled “The Merger—Stabroek JOA”), if the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close. Some of these conditions are not in Hess’ or Chevron’s control.

Further, subject to any then ongoing arbitration relating to the Stabroek JOA, either Chevron or Hess may terminate the merger agreement if the merger has not been completed by October 22, 2024, (or April 22, 2025 or October 22, 2025, if the applicable end date is extended pursuant to the merger agreement) or by such later date as the parties may mutually agree.

p. 81: The Stabroek JOA contains a right of first refusal (the “Stabroek ROFR”) provision that, if applicable to a change of control transaction and properly exercised, provides the Stabroek Parties with a right to acquire the participating interest in the Stabroek Block held by the Stabroek Party subject to such transaction (at a value that is based on the portion of the value of the change of control transaction that reasonably should be allocated to such participating interest and is increased to reflect a tax gross-up) only after, and conditioned on, the closing of such transaction. Chevron and Hess believe that the Stabroek ROFR does not apply to the merger due to the structure of the merger and the language of the Stabroek ROFR provisions.

p. 82: On October 24, 2023, shortly after the merger was announced, Exxon issued the following statement, indicating its support for the merger: “Hess has been a valued partner in Guyana since 2014 and we look forward to continuing our successful operations in the Stabroek block with Chevron, pending the deal closing.” However, Exxon and CNOOC subsequently informed Chevron and Hess that they believe the Stabroek ROFR applies to the merger. Hess, Chevron, Exxon and CNOOC subsequently engaged in discussions regarding the applicability of the Stabroek ROFR to the merger.

If the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close, and, pursuant to the terms of the Stabroek JOA, the Exxon affiliate and the CNOOC affiliate would cease to have rights under the Stabroek ROFR with respect to the merger. In that event, Hess would remain an independent public company and would continue to own its participating interest in the Stabroek Block. Based on the express terms of the Stabroek JOA, Chevron and Hess do not believe there is any material likelihood that the circumstances described in this paragraph will occur.

p. 118: In addition, with respect to the Stabroek ROFR, if the arbitration does not result in a confirmation that the Stabroek ROFR does not apply to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close.

Canadian and US approvals were granted and CNOOC acquired Nexen (Canada) in 2013.

Nexen’s Guyana interest was not mentioned in the press announcement, and appears to have been a rather minor consideration in the acquisition.

So, an apparent afterthought in CNOOC’s takeover of Nexen has (1) proven to be extremely profitable, (2) given the company and the Chinese government leverage in the Exxon-Chevron supermajor dispute, and (3) opened the door for CNOOC to increase their interest in the massive Stabroek field.

Are Exxon and Chinese partner (CNOOC) attempting to use Chevron’s acquisition of Hess to improve their already lucrative position in Guyana’s prolific Stabroek block?

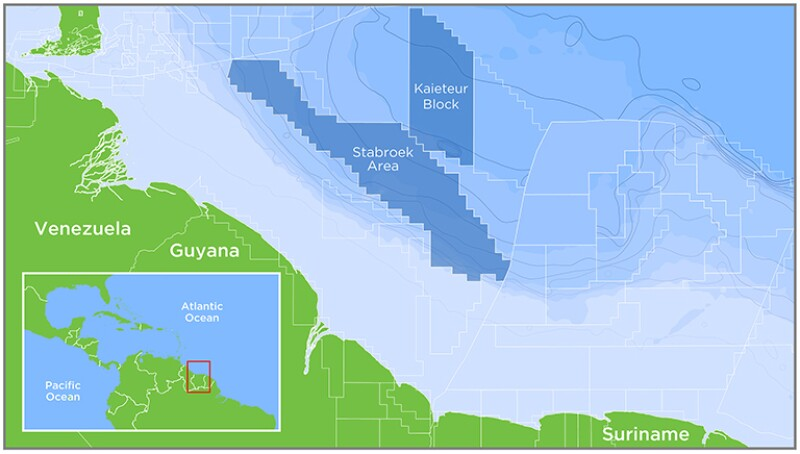

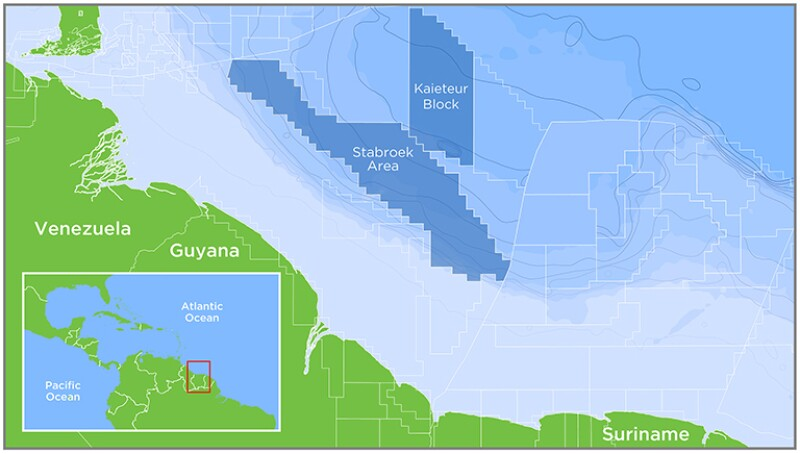

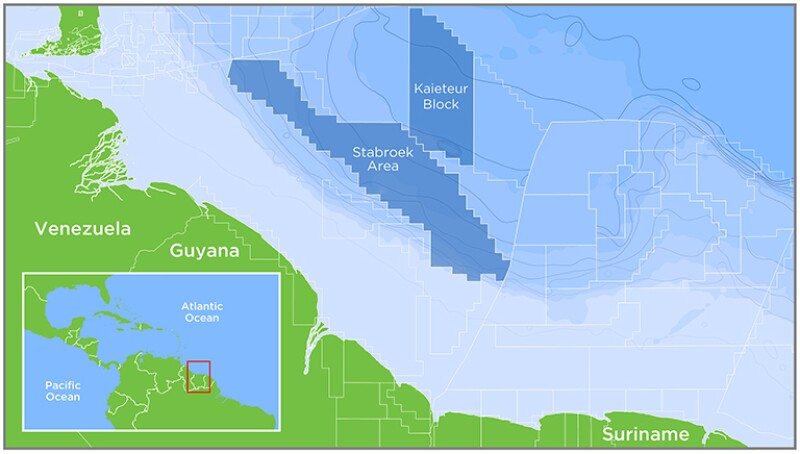

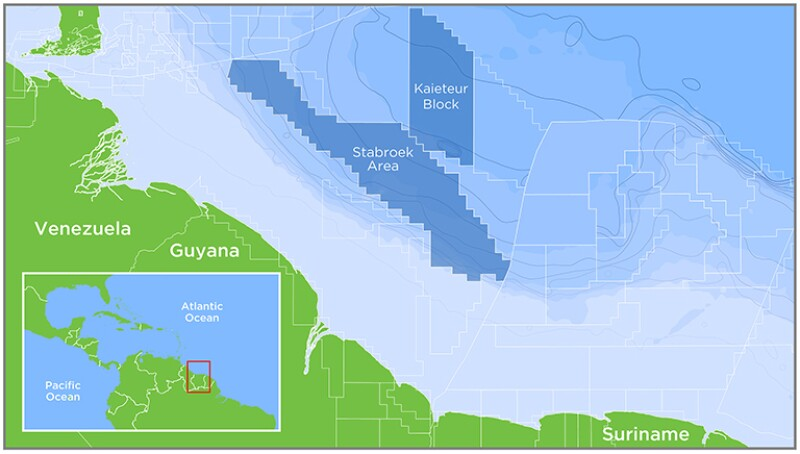

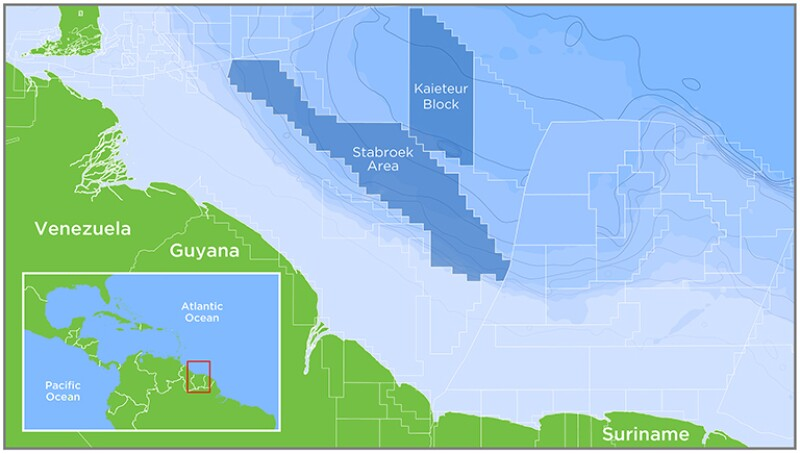

The Stabroek operating agreement outlines terms for Hess, Exxon, and CNOOC to explore and develop the block.

This Stabroek agreement includes a right of first refusal (ROFR) provision which allows the parties to buy out the stake of one of them in the event of a ‘change of control’ transaction.

Chevron and Hess argue that the merger’s structure does not trigger the ROFR clause.

Exxon and CNOOC argue that the clause applies. This could force Hess to offer its stake in the Stabroek block to its partners first.

The Exxon/CNOOC position seems to be a stretch. Chevron did not buy the Stabroek share; they bought the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership.

As an offshore operator, Exxon has been highly responsible from a safety standpoint. However, the company has a shown tendency to stretch the envelope when it comes to contract rights. The most recent example was their acquisition of 163 GoM oil and gas leases for carbon disposal purposes, contrary to the terms of the sale notice and lease contracts.