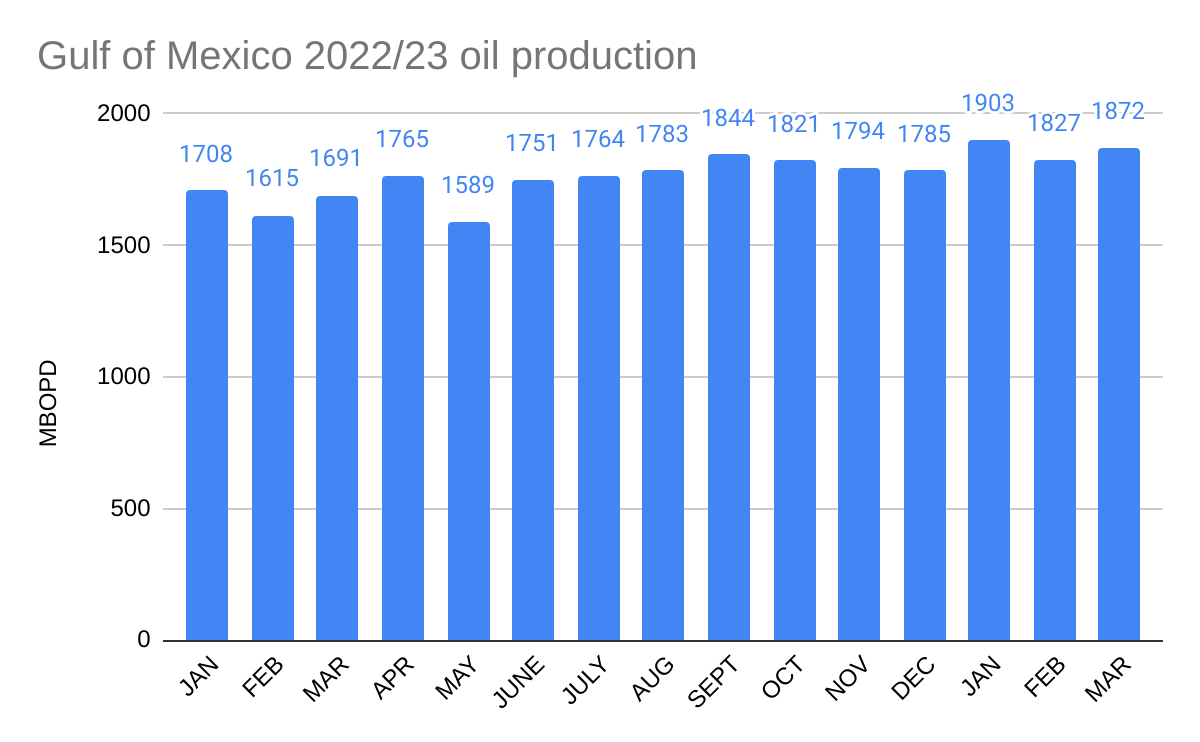

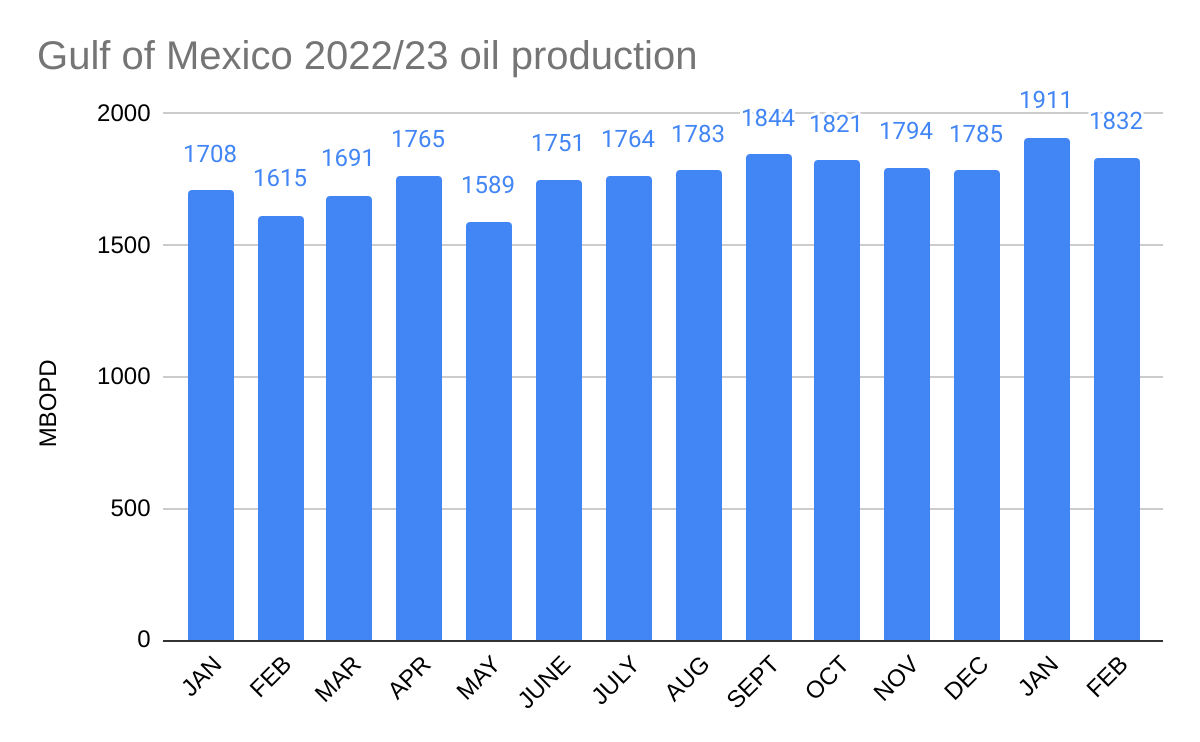

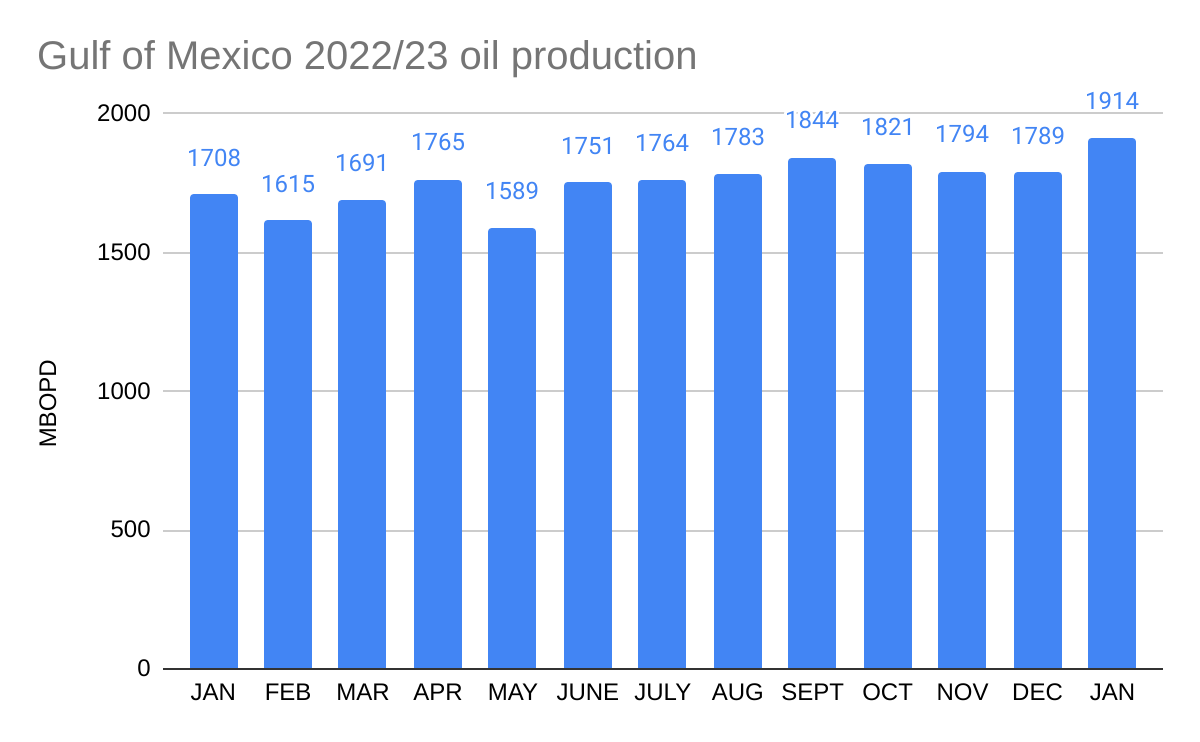

EIA reports October production of 1.959 million bopd. September production was revised down from 2.000 to 1.999 million bopd, a very slight but symbolically significant change. Foul play? 😉

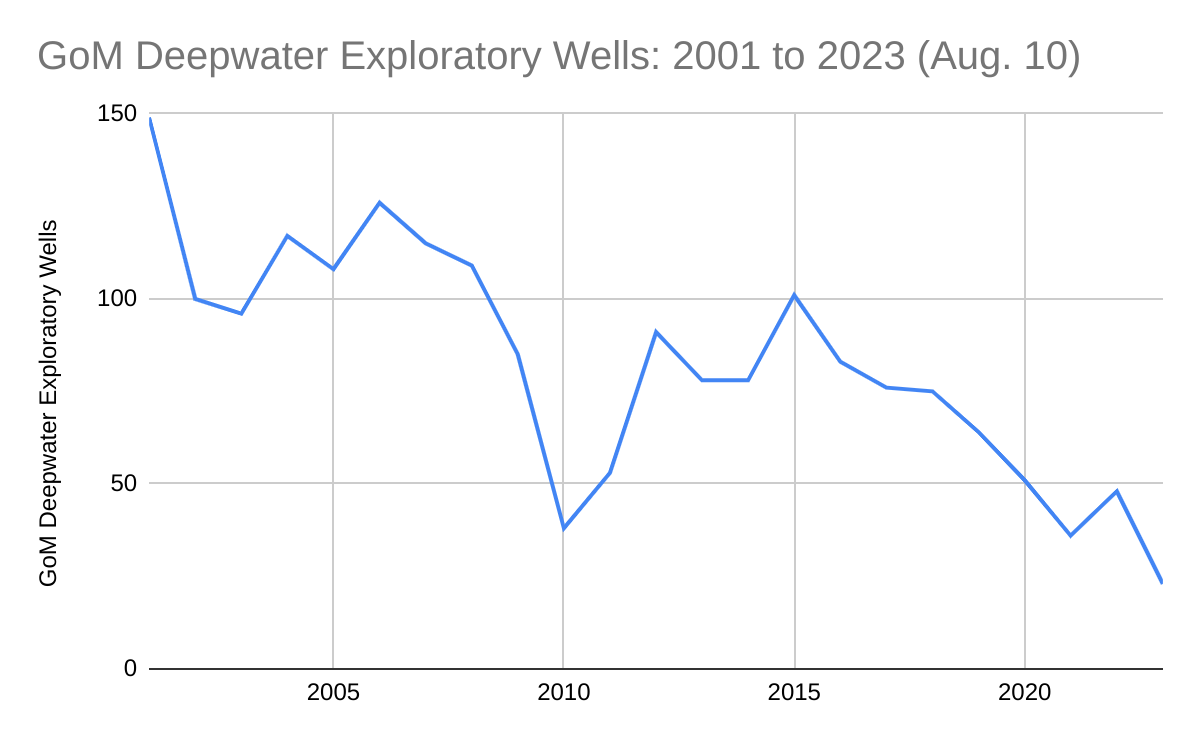

Record low exploratory drilling: 2023 will be the third consecutive year with fewer than 50 deepwater exploratory well starts. The only other year this century with <50 deepwater exploratory well starts was 2010 when there was a post-Macondo drilling moratorium.

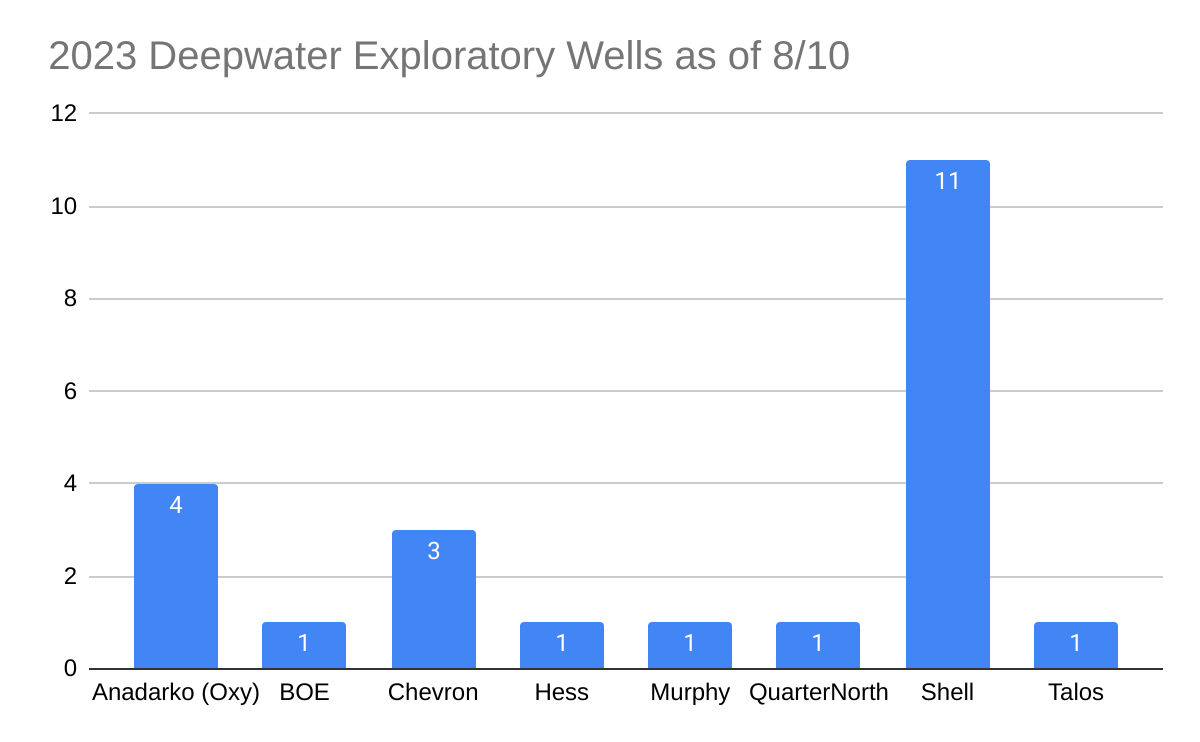

Low participation: Only 8 companies have started deepwater exploratory wells in 2023 YTD. Anadarko, Chevron, and Shell drilled 78% of the wells, with Shell alone accounting for 48%. Compare these numbers with 2001, when 24 companies drilled 149 deepwater exploratory wells.

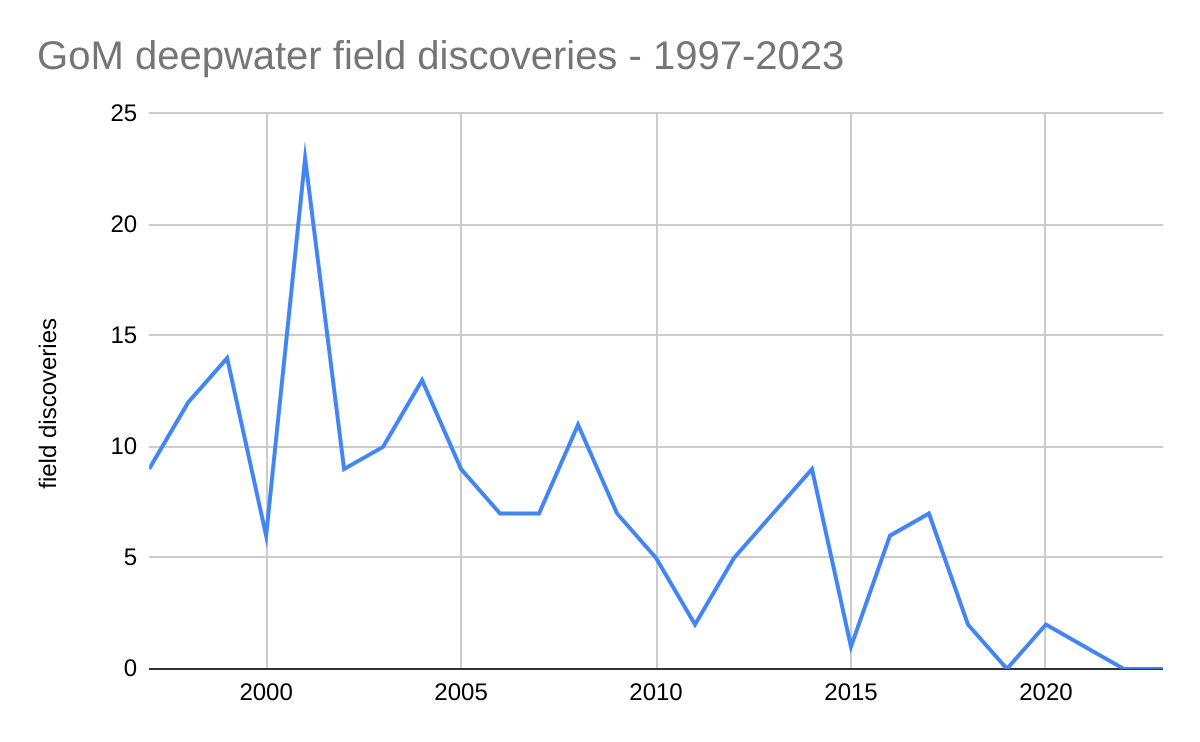

Absence of new field discoveries: Per BOEM’s database, no deepwater fields have been discovered since March 2021 and there were only 3 discoveries in the past 5 years (see chart below)

Leasing and regulatory uncertainty: When will the 5 year leasing plan be finalized and how much will leasing be restricted? What will be the effect of the expanded Rice’s whale area on deepwater operations? To what extent is this expansion justified? What other legal and regulatory threats are on the horizon?

Unrealistic expectations regarding the “energy transition:” In a stunning introductory statement, the Proposed 5 Year Leasing Plan expressed concerns that new leases would produce too much oil and gas for too long. OPEC+ must love the way the US sanctions its own energy production, most notably the oil and gas resources of the OCS. More than 96% of the OCS is off-limits to oil and gas leasing, and the 5 year plan proposed to constrain leasing in the only areas that remain. The favored offshore wind program was intended to be a complement to, not a replacement for, the oil and gas program. Wind energy is limited by intermittency, space preemption, navigation, and wildlife protection concerns.

Some companies have visions of the GoM as a carbon dumping hub: The largest US oil company, which hasn’t drilled a well in the GoM in nearly 4 years and operates just one production platform, seeks praise and profit by sequestering CO2 beneath the Gulf while maximizing oil production elsewhere. How will this sustain economically and strategically important GoM oil and gas production?

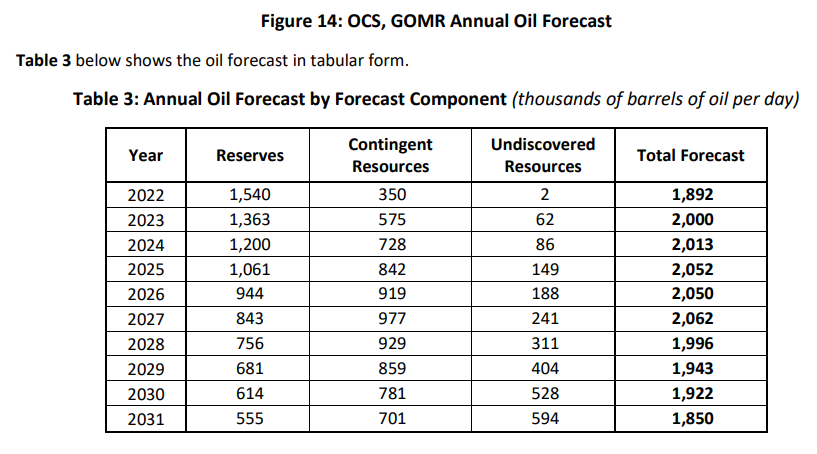

The EIA 2022 figure is spot-on, as it should be given that 10 months of 2022 production data are now in hand. However, BOEM’s 2022 forecast (published in July) missed the mark considerably. (In fairness to BOEM staff, their work was probably completed months before publication pending internal reviews.)

Of greater concern, given the policy implications, is the rosy BOEM forecast for the out-years. Despite historically low levels of leasing and exploratory drilling, BOEM forecasts oil production to exceed 2 million BOPD through 2027 and to remain well above the current (2022) level through 2031 (second table below).

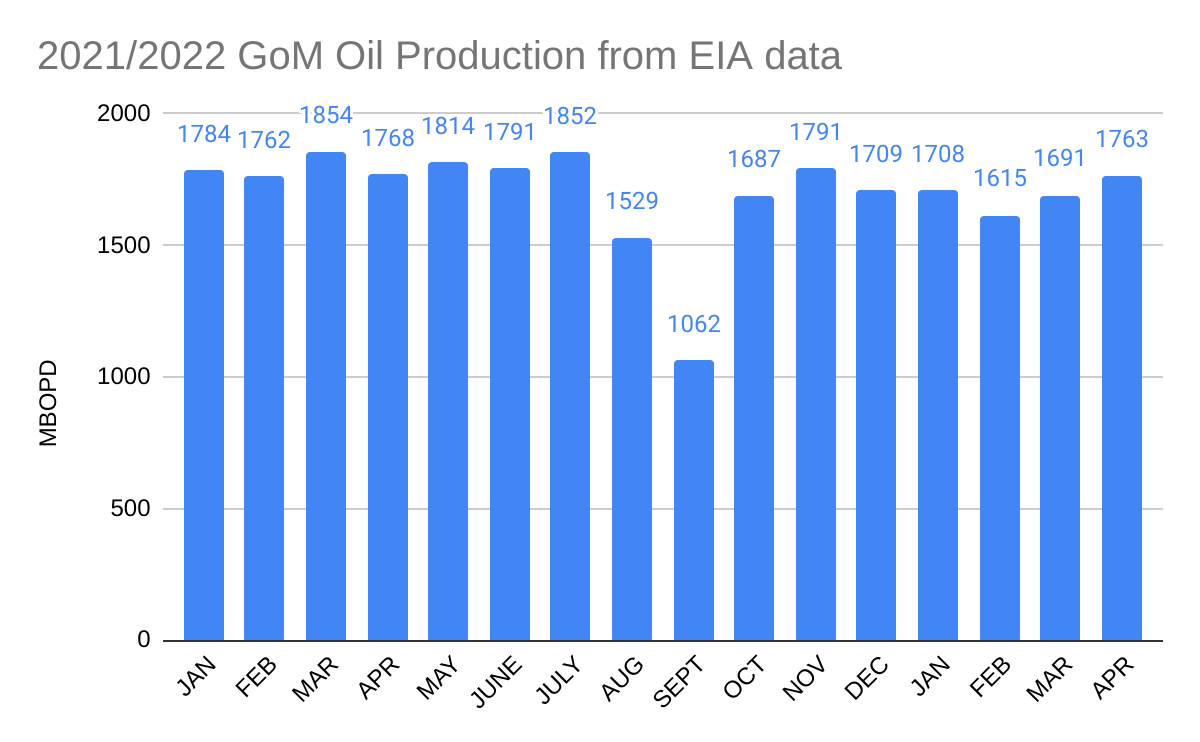

Assuming no significant tropical storm shutdowns this month, we should get a good read on the impact of the pipeline outage when the EIA production data for August are posted.

“BOEM’s short-term (20-year) production forecast for existing leases shows steady growth from 2022 through 2024 and declining thereafter (see Section 5.2.1). The long-term nature of OCS oil and gas development, such that production on a lease can continue for decades makes consideration of future climate pathways relevant to the Secretary’s determinations with respect to how the OCS leasing program best meets the Nation’s energy needs.“

Basing leasing decisions on “future climate pathways” would seem to be a considerable stretch of the Secretary’s authority under the OCS Lands Act and may be inconsistent with the recent SCOTUS decision in West Virginia vs. EPA. A strategic shutdown of the offshore oil and gas program would dramatically increase energy supply and security risks going forward, and should be authorized by Congress.