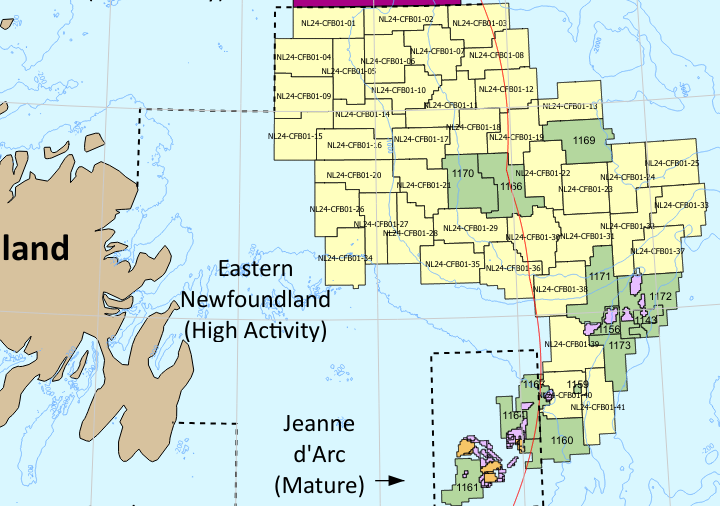

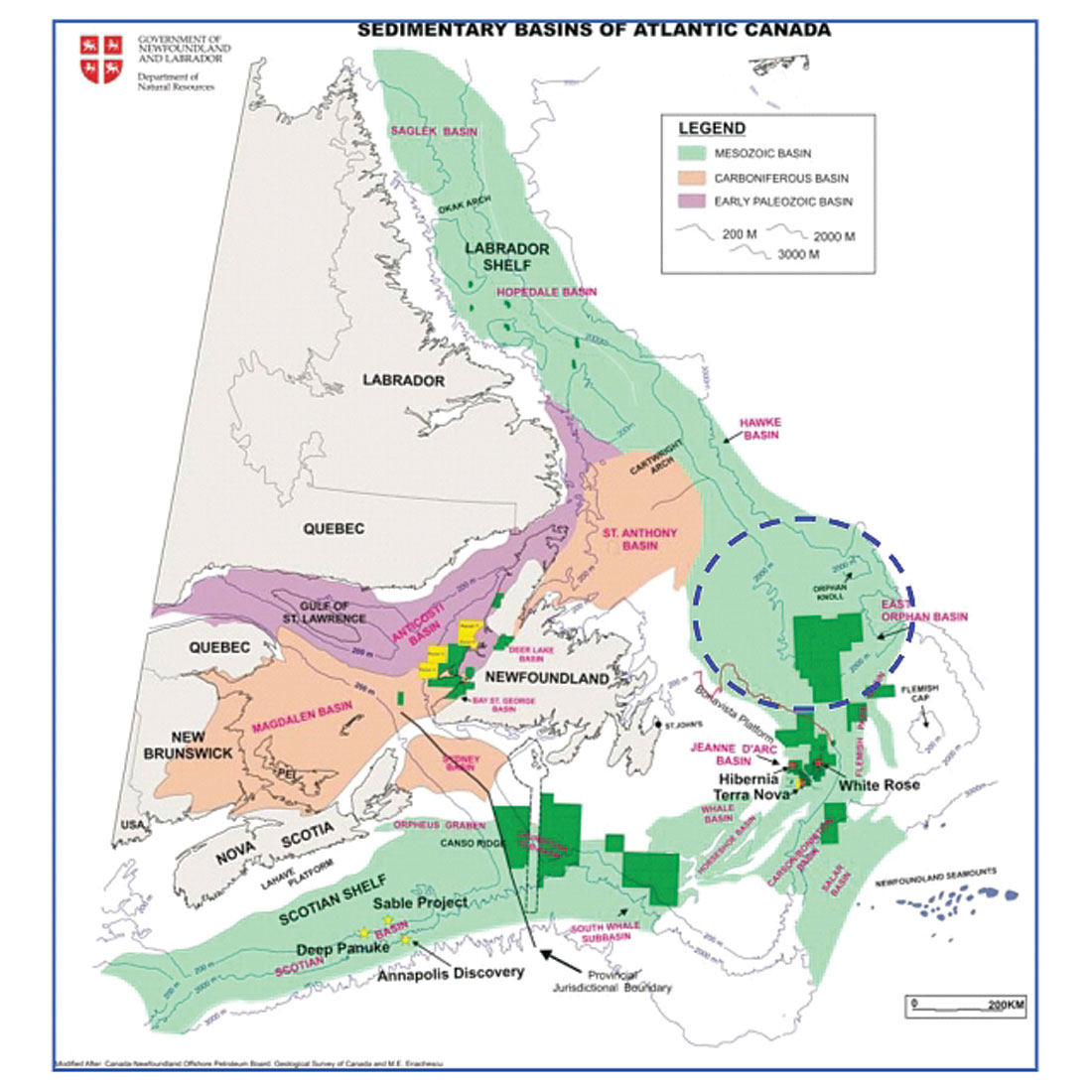

Per rig tracker data, the Stena DrillMAX has been on location at Exxon’s Orphan Basin wellsite since Sunday (19 May). The site is 317 miles (510 km) NE of St. John’s in Block 1169 (~3000 m water depth).

Per this very good resource assessment report for the Govt. of Newfoundland and Labrador, “the Orphan Basin area demonstrates a potentially prolific petroleum system with four main plays (reservoirs and associated seals) sourced by various source rocks (Upper Jurassic, Cretaceous, and Paleogene).“

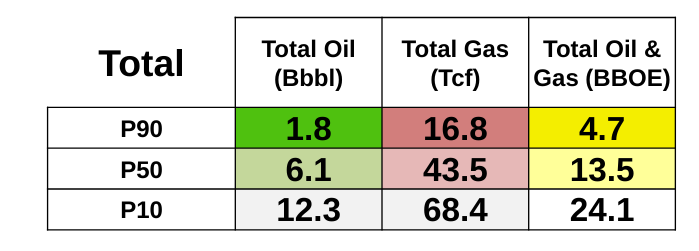

Unrisked resource estimates (theoretical pending confirmation by drilling) at the 90, 50, and 10% probability levels for the Orphan Basin blocks offered for licensing in Nov. 2022:

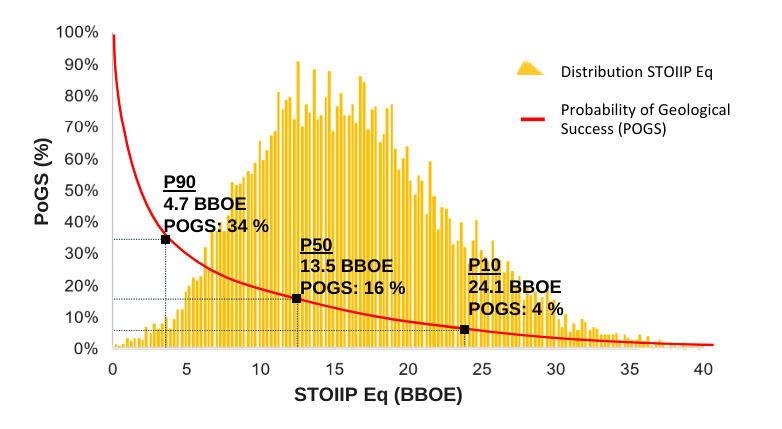

Taking into account the risks of the geologic model not accurately reflecting the reservoir, seal, charging, and trap components of the petroleum system, the probability of finding 13.5 billion drops to 16% (see plot below). This is still a high probability for a massive wildcat discovery.

This is why you move a state-of-the-art drillship thousands of miles to drill a single exploratory well at a remote location in the North Atlantic. The most likely outcome is negative or inconclusive findings, but the potential for such a major discovery justifies the investment.

The PGOS curve quantifies the probability of success in finding the identified volume of resources in the new Orphan Basin blocks (e.g. there is a 34% chance of finding 4.7 billion BOE and a 16% chance of finding 13.5 billion BOE).

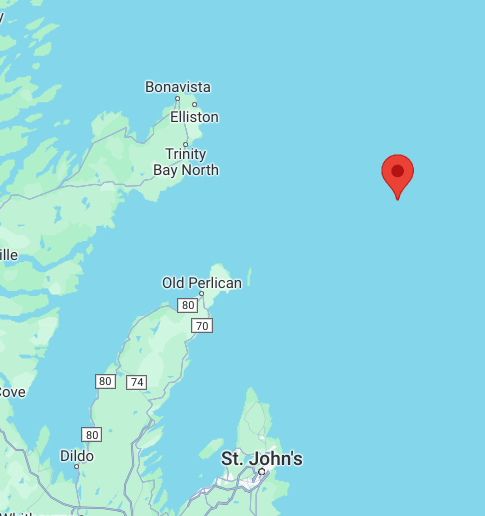

The DrillMAX has exited Bulls Bay and is en route to the Orphan Basin, where Exxon will drill a high potential exploratory well. As of this morning at ~1000 GMT, the drillship was headed north at 7.7 kts (see map).

“Exxon Mobil has led a persistent and apparently successful lobbying campaign behind the scenes to push the US federal government to adopt rules that would allow the conversion of existing oil and gas leases in the Gulf of Mexico into offshore carbon capture and storage (CCS) acreage, according to documents seen by Energy Intelligence and numerous interviews with industry players.”Energy Intelligence

The Energy Intelligence article documents the ongoing carbon disposal lobbying by Exxon and others. Those meetings are okay prior to publishing a Notice of Proposed Rulemaking (NPRM) for public comment. However, the article implies that the next step is a final rule: “Whether or not Exxon succeeds will become fully clear when the US issues final rules guiding CCS leasing, expected sometime this year.”

A final rule this year is unlikely, because an NPRM has to be published first for public comment. The only exception would be if BOEM was able to establish “good cause” criteria for a direct final or interim final rule in accordance with the Administrative Procedures Act. Such an attempt at corner cutting seems unlikely, especially in an election year when all regulatory actions are subject to additional scrutiny.

Exxon must have thought they had a clear path forward after 11th hour additions to the “Infrastructure Bill” authorized carbon disposal on the OCS, exempted such disposal from the Ocean Dumping Act, and provided $billions for CCS projects. Keep in mind that the Infrastructure Bill was signed just two days before OCS Oil and Gas Lease Sale 257, at which Exxon acquired 94 leases for carbon disposal purposes.

What the Infrastructure Bill did not provide is authority to acquire carbon disposal leases at an oil and gas lease sale. Now the lobbyists are apparently scrambling to overcome that obstacle administratively.

A single company or small group of companies should not be dictating the path forward for the Gulf of Mexico. Super-major Exxon is a relative minnow in the Gulf of Mexico OCS. They have not drilled an exploratory well since 2018, not drilled a development well since 2019, operate only one platform (Hoover, installed in 2000), ranked 11th in 2023 oil production, and ranked 29th in 2023 gas production.

Lastly, and most importantly, public comment on the myriad of technical, financial, and policy issues associated with GoM carbon disposal is imperative. That input is essential before final regulations are promulgated.

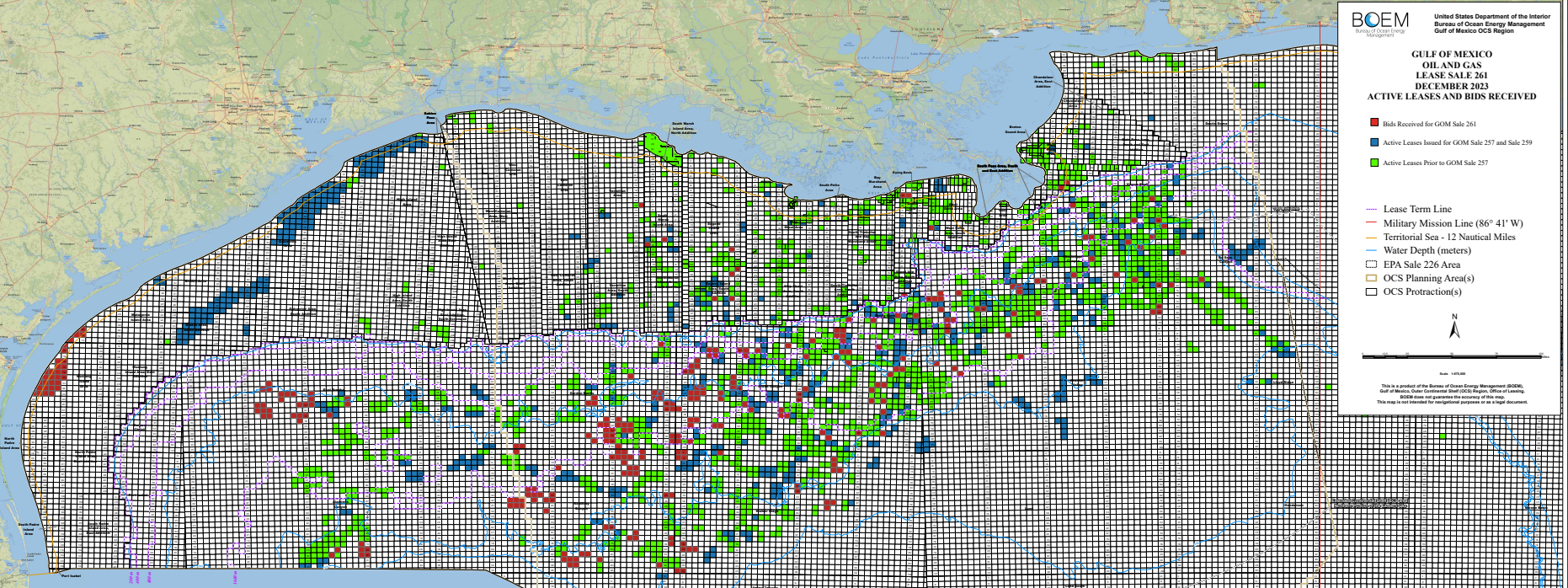

At Sale 261, Repsol was the sole bidder for 36 nearshore Texas tracts in the Mustang Island and Matagorda Island areas (red blocks at the western end of the map above). Exxon acquired 163 nearshore Texas tracts (blue in map above) at Sales 257 and 259.

The DrillMAX is en route from Guyana to drill the Persephone wildcat well 500 km NE of Newfoundland in the highly prospective Orphan basin (3000 m water depth). This looks like the farthest from shore any well has been drilled in the Atlantic. The late spring date is prudent.This is definitely a well to watch because of the resource potential and difficult operating conditions.

As we wait for the International Chamber of Commerce (ICC) arbitration panel to rule on the Exxon-CNOOC-Chevron-Hess Stabroek dispute, key excerpts from Chevron’s SEC filing about their merger with Hess are pasted below. The text highlighted in red is particularly interesting.

If the ICC arbitration panel rules that the right-of-first-refusal (ROFR) provision applies, the Chevron filing says that the merger is off and Hess continues as Stabroek’s 30% owner. If that statement is correct, Exxon and CNOOC cannot obtain the Hess share. Their only benefit from the challenge would be to deny their rival Chevron from participating in the block or to receive payment from Chevron for approving the ownership change.

It’s also noteworthy that Exxon initially showed support for the deal (quote below).

p. 32: With respect to the Stabroek ROFR (as defined in the section entitled “The Merger—Stabroek JOA”), if the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close. Some of these conditions are not in Hess’ or Chevron’s control.

Further, subject to any then ongoing arbitration relating to the Stabroek JOA, either Chevron or Hess may terminate the merger agreement if the merger has not been completed by October 22, 2024, (or April 22, 2025 or October 22, 2025, if the applicable end date is extended pursuant to the merger agreement) or by such later date as the parties may mutually agree.

p. 81: The Stabroek JOA contains a right of first refusal (the “Stabroek ROFR”) provision that, if applicable to a change of control transaction and properly exercised, provides the Stabroek Parties with a right to acquire the participating interest in the Stabroek Block held by the Stabroek Party subject to such transaction (at a value that is based on the portion of the value of the change of control transaction that reasonably should be allocated to such participating interest and is increased to reflect a tax gross-up) only after, and conditioned on, the closing of such transaction. Chevron and Hess believe that the Stabroek ROFR does not apply to the merger due to the structure of the merger and the language of the Stabroek ROFR provisions.

p. 82: On October 24, 2023, shortly after the merger was announced, Exxon issued the following statement, indicating its support for the merger: “Hess has been a valued partner in Guyana since 2014 and we look forward to continuing our successful operations in the Stabroek block with Chevron, pending the deal closing.” However, Exxon and CNOOC subsequently informed Chevron and Hess that they believe the Stabroek ROFR applies to the merger. Hess, Chevron, Exxon and CNOOC subsequently engaged in discussions regarding the applicability of the Stabroek ROFR to the merger.

If the arbitration does not result in a confirmation that the Stabroek ROFR is inapplicable to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close, and, pursuant to the terms of the Stabroek JOA, the Exxon affiliate and the CNOOC affiliate would cease to have rights under the Stabroek ROFR with respect to the merger. In that event, Hess would remain an independent public company and would continue to own its participating interest in the Stabroek Block. Based on the express terms of the Stabroek JOA, Chevron and Hess do not believe there is any material likelihood that the circumstances described in this paragraph will occur.

p. 118: In addition, with respect to the Stabroek ROFR, if the arbitration does not result in a confirmation that the Stabroek ROFR does not apply to the merger, and if Chevron, Hess, Exxon and/or CNOOC do not otherwise agree upon an acceptable resolution, then there would be a failure of a closing condition under the merger agreement, in which case the merger would not close.

Canadian and US approvals were granted and CNOOC acquired Nexen (Canada) in 2013.

Nexen’s Guyana interest was not mentioned in the press announcement, and appears to have been a rather minor consideration in the acquisition.

So, an apparent afterthought in CNOOC’s takeover of Nexen has (1) proven to be extremely profitable, (2) given the company and the Chinese government leverage in the Exxon-Chevron supermajor dispute, and (3) opened the door for CNOOC to increase their interest in the massive Stabroek field.

Chevron continues to operate in Venezuela and is a beneficiary of the easing of US sanctions that facilitated the resumption of oil exports. Is the government of Guyana okay with Stabroek partners helping to support the regime that claims much of their offshore oil?

On the other hand, what about Exxon’s Stabroek partner, state-owned China National Offshore Oil Corp.? CNOOC has a 25% share of the Stabroek block (vs. 45% for Exxon and 30% for Hess) as a result of their takeover of (Canadian) Nexen in 2013. The CNOOC acquisition of Nexen was similar to Chevron’s acquisition of Hess. Was Exxon okay with that change in ownership?

CNOOC hasn’t released any public statements on the Stabroek dispute, but appears to be aligned with Exxon. Presumably, CNOOC also wants a larger share of the Stabroek pie. Is the Government of Guyana okay with an ally of Venezuela increasing their influence and having access to geologic, reservoir, and operational data for the Stabroek block? CNOOC is also partnered with Exxon on the block they acquired at the most recent licensing round.

Given the national security implications, is the Government of Guyana okay with leaving the resolution of this dispute to an ICC tribunal in Paris?

Are Exxon and Chinese partner (CNOOC) attempting to use Chevron’s acquisition of Hess to improve their already lucrative position in Guyana’s prolific Stabroek block?

The Stabroek operating agreement outlines terms for Hess, Exxon, and CNOOC to explore and develop the block.

This Stabroek agreement includes a right of first refusal (ROFR) provision which allows the parties to buy out the stake of one of them in the event of a ‘change of control’ transaction.

Chevron and Hess argue that the merger’s structure does not trigger the ROFR clause.

Exxon and CNOOC argue that the clause applies. This could force Hess to offer its stake in the Stabroek block to its partners first.

The Exxon/CNOOC position seems to be a stretch. Chevron did not buy the Stabroek share; they bought the company that holds that share. Hess is to be part of Chevron and there would be no change of control from the standpoint of the partnership.

As an offshore operator, Exxon has been highly responsible from a safety standpoint. However, the company has a shown tendency to stretch the envelope when it comes to contract rights. The most recent example was their acquisition of 163 GoM oil and gas leases for carbon disposal purposes, contrary to the terms of the sale notice and lease contracts.