A post from last March discussed the high and seemingly unfair royalty and rental rates for new leases in the shallow waters of the Gulf of Mexico shelf. A 50% increase in the shelf royalty rate for lease sales 259 and 261 combined with rather punitive rental rates have likely contributed to the sharp decline in bidding for shelf lease blocks (see table below).

This decline in shelf bidding is unfortunate because the smaller companies that operate in the shallow waters of the Gulf are critical to sustaining the production infrastructure. These companies are also significant producers of environmentally favorable nonassociated (gas-well) natural gas.

| lease sale | shelf blocks with bids (excluding CCS bids) | sum of high shelf bids ($million, excluding CCS bids) |

| 257 | 46 | $8.1 |

| 259 | 29 | $4.1 |

| 261 | 13 | $1.7 |

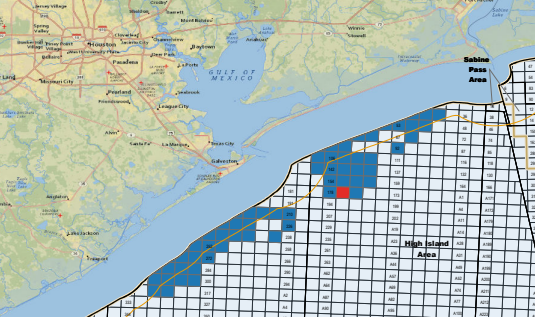

BOEM has completed their evaluation of the Sale 261 shelf bids (see below). Each of these blocks received only a single bid, and every bid was accepted. Ironically, the invalid CCS bids for blocks that have no oil and gas value, were the first to be accepted. This was also the case for Sales 257 and 259.

| Company | Block | high bid ($) per acre ($) | date accepted |

| Byron | SM 60 | 128,750 25.75 | 2/2 |

| Byron | SM 70 | 182,235 33.32 | 2/20 |

| Cantium | GI 35 | 125,000 25.00 | 2/20 |

| Cantium | GI 36 | 125,000 25.00 | 2/20 |

| Cantium | MP 314 | 125,000 25.00 | 3/12 |

| Cantium | SP 63 | 125,000 25.00 | 3/12 |

| Arena | EI 231 | 135,000 27.18 | 2/20 |

| Arena | EI 277 | 135,000 27.18 | 2/20 |

| Arena | EI 281 | 135,000 27.18 | 2/20 |

| Arena | EI 340 | 135,000 27.18 | 2/20 |

| Arena | EI 343 | 135,000 27.18 | 2/20 |

| Arena | WD 119 | 135,000 26.75 | 3/12 |

| Focus | V 152 | 121,152 25.16 | 2/20 |

| Repsol | 36 CCS bids | 187,200 (1) 32.50 | 1/23 |

Suggestions:

- Seek a legislative fix to the Inflation Reduction Act😉 provision that established a 1/6 royalty rate floor for all OCS leases (formerly the royalty rate was 1/8 for leases on the shelf).

- In the interim, administratively lower the royalty for shelf leases to 1/6 (from 18 3/4%).

- Reconsider the rental rate scheme for shelf leases.

- For future oil and gas lease sales, accept all high bids that exceed the specified minimum bid (currently $25/ac for the shelf). The Gulf of Mexico shelf has been extensively explored and developed for 70 years. While prospects remain, they are generally marginal as evidenced by the recent lease sale results. Fair market value is what any company is willing to bid (above the specified minimum).

- Focus on assuring that lease purchasers are technically qualified to minimize safety risks, and that financial assurance for decommissioning (for new and existing leases owned by the high bidder) has been fully addressed.