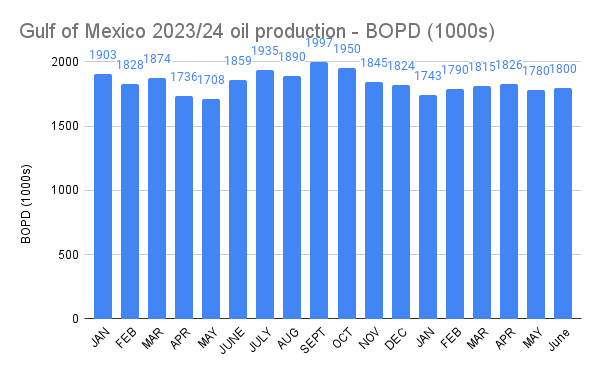

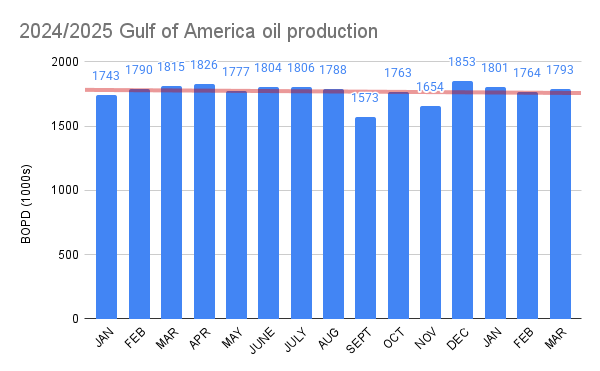

March Gulf of America oil production was nearly identical to the 2024/2025 average, and the trend line (red) is remarkably flat. However, production remains below the volumes forecasted by EIA and well below those forecasted by BOEM.

It appears that new deepwater production is replacing Gulf-wide production declines, but is not yet sufficient to increase total production. We will see if that changes as the year progresses.

- March 2025 Gulf of America production: 1.793 million bopd

- 2024/2025 average production: 1.77 million bopd

- 2024/2025 average omitting Sept. 2024 (tropical storms): 1.784 million bopd

- EIA forecast for 2025 (published 9/16/2024): 1.9 million bopd

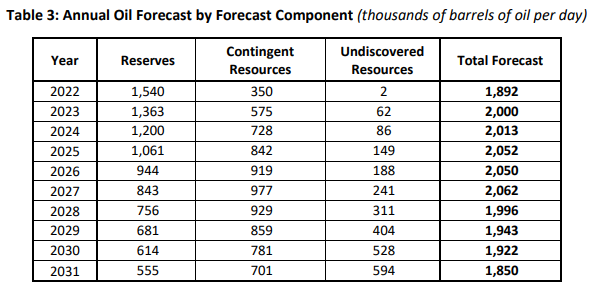

- BOEM forecast for 2025 (published in 2022, table below): 2.052 million bopd