Deepwater (>1000′) activity continues to dominate, accounting for 61% of the well starts.

Not a single company drilled both shelf and deepwater wells.

While shelf facilities currently account for only about 7% of GoM oil production, 1122 of the 1179 remaining platforms are on the shelf and they account for 24% of GoM gas production, most of which is environmentally favorable nonassociated gas.

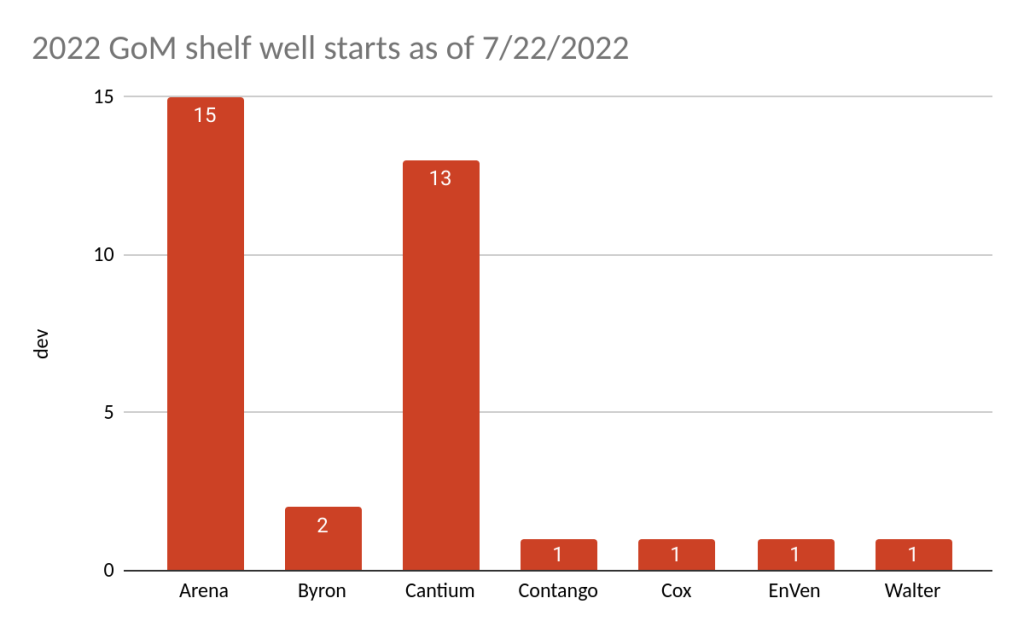

Two companies, Arena and Cantium, accounted for 75% of the shelf well starts. Excluding the CCS bids, Arena and Cantium were the most active shelf bidders in Sale 279. Arena bid alone on 7 blocks. Cantium was the high bidder on 5 blocks. (Focus Exploration was high bidder on 4 shelf blocks and was “outbid” by Exxon for High Island 177.)

One company, Shell, accounted for 39% of the deepwater well starts

One of BP’s exploratory wells (drilled subsequent to Sale 257) was in Green Canyon 821, immediately south of GC 777, the block that BP/Talos bid $1.8 million for in Sale 257. That bid was rejected by BOEM. In sale 259, BP was the sole bidder for GC 777, and their bid was only $583,000, less than 1/3 of their Sale 257 bid. Perhaps the GC 821 exploratory well reduced the value of GC 777? Will this lower bid now be accepted?

DW expl

DW dev

shelf expl

shelf dev

Anadarko

5

1

Arena

22

BOE

1

4

BP

2

3

Byron

2

Cantium

20

Chevron

3

Contango

2

Cox

2

Eni

2

5

EnVen

5

Greyhound

2

Hess

2

Kosmos

1

LLOG

3

1

Murphy

4

QuarterNorth

2

Shell

25

9

Talos

2

8

Walter

1

Woodside

3

1

Gulf of Mexico well starts during 2022 and the first quarter of 2023

Offshore gas has important environmental advantages, particularly nonassociated gas-well gas (GWG). While the GoM production chart (below) is not pretty, there are signs that gas production may have bottomed and is slowly rising. This is largely due to growth in oil-well gas (OWG) associated with deepwater oil production.

A successful offshore program requires a mix of strategies, and it is encouraging that companies are still pursuing natural gas on the GoM shelf. The second chart (below), based on BOEM data, shows 2022 YTD (probably through Oct.) GWG production for the 11 companies that (1) produced more GWG than OWG and (2) produced more than 1 BCF of GWG.

Interestingly, 100% of the gas produced by Contango, Samchully, and Helis in 2022 was from gas wells. Contrast this with bp, the third largest GoM gas producer. None of bp’s gas production was from gas wells.

Without much hype, shelf operators continue to find and extract oil and gas from beneath the shallow waters of the GoM. The 1700 shelf platforms that remain provide energy for our economy and important hardbottom substrate for marine life. Keep it going! Only 25 more years until the 100th anniversary! 😀