While it’s unlikely that the whale strandings are the result of pre-construction activities for offshore wind development, greater transparency on the part of the developer and regulators would be helpful:

What surveys and other offshore activities are being conducted? Where?

What is the timeframe for these activities?

Any sightings of distressed whales?

Other anomalous observations?

Absent regular activity updates, accusations and protests are likely to continue and intensify.

“Mom” (US govt) strongly and openly favors one child (offshore wind) over the other (offshore oil and gas). As a result, beneficial family synergy is not realized, and neither “child” reaches her full potential.

The wind program was intended to complement the oil and gas program, not replace it.

These articles highlight some of the challenges facing offshore wind:

WSJ: Soaring Costs Threaten U.S. Offshore-Wind Buildout

Bloomberg: US Ignored Own Scientists’ Warning in Backing Atlantic Wind Farm

NJ.com: Offshore wind is on N.J.’s horizon but activists worry of impact to whales, economy, the view

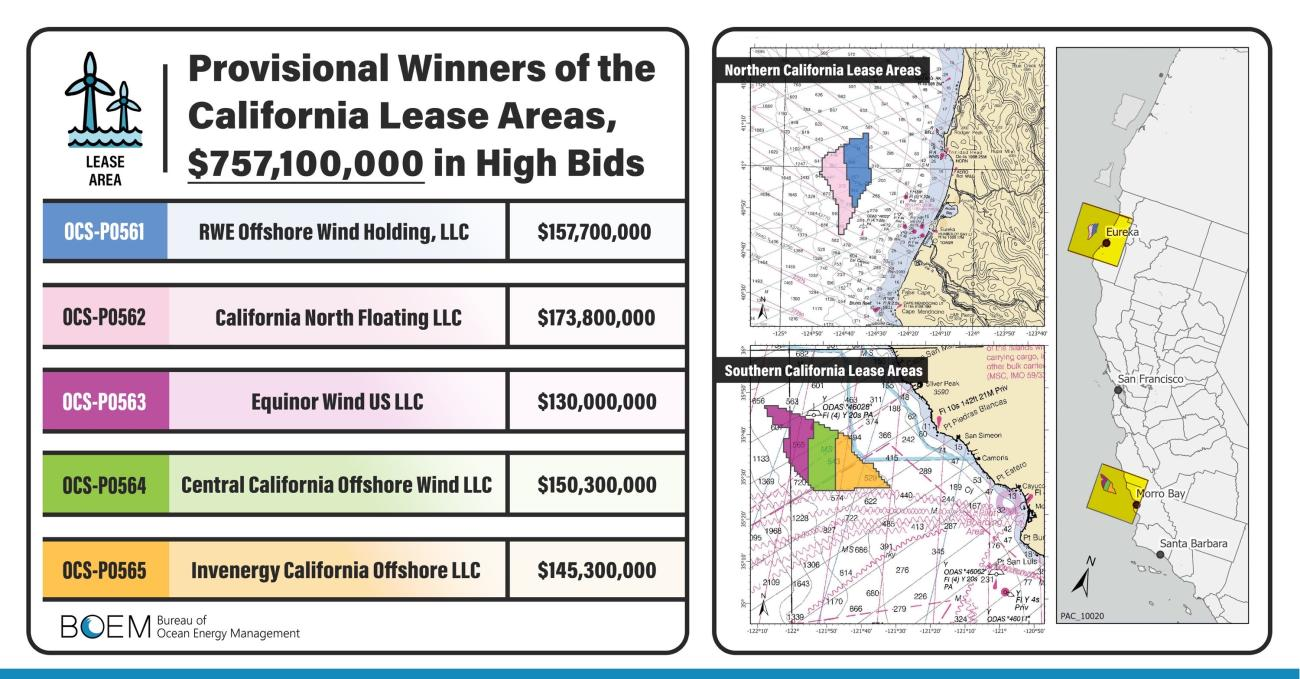

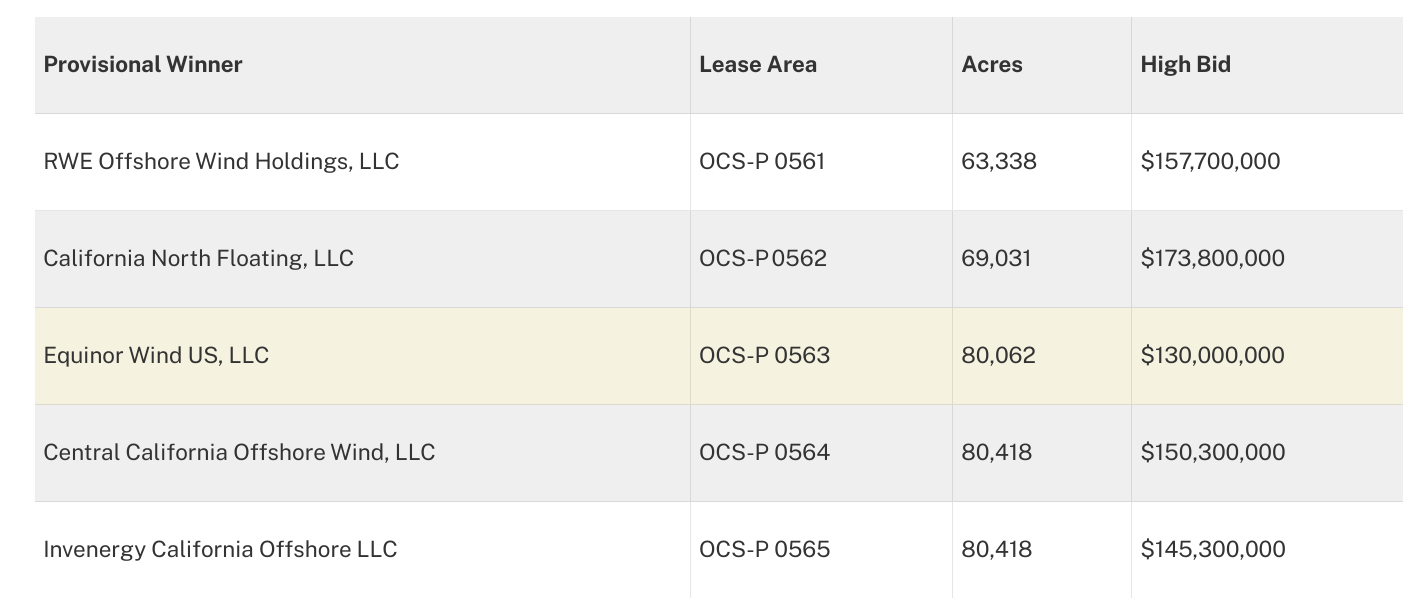

Only Equinor is a familiar name to the offshore oil and gas industry, so here are some blurbs about the other high bidders.

California North Floating, LLC, is a subsidiary of Copenhagen Infrastructure Partners (CIP). Since entering the US offshore market in 2016, CIP has built a leading offshore wind position through its affiliate Vineyard Offshore. This includes Vineyard Wind 1, the country’s first commercial scale offshore wind project which is currently under construction, as well as two lease areas under development totaling approximately 5.0 GW off the coast of Massachusetts and New York.

Central California Offshore Wind is managed by an East Coast offshore wind energy company, Ocean Winds North America LLC, which formed a joint venture with the Canada Pension Plan Investment Board to win the lease. Ocean Winds has more than 10 years of experience in floating offshore wind, most notably through the development and operation of Windfloat Atlantic (offshore Portugal), the world’s first fully commercially operational floating offshore wind farm

Equinor, a Norwegian company, is a major international oil and gas producer, an important wind energy investor, and a leader in the development of floating wind turbine technology. Equinor operates the Hywind Tampen floating offshore wind farm which will supply power to Norwegian offshore oil and gas fields.

Invenergy and its affiliated companies develop, own, and operate large-scale renewable and other clean energy generation and storage facilities in the Americas, Europe and Asia. Invenergy’s home office is located in Chicago, and it has regional development offices in the United States, Canada, Mexico, Spain, Japan, Poland, and Scotland.

RWE Renewables has experience covering the offshore and onshore wind energy value chain from development to construction and operation. These activities are the responsibility of two functional units, “Unit Renewables Europe & Australia” and “Unit Offshore Wind”, as well as the subsidiary RWE Renewables Americas. RWE Renewables also invests in large-scale solar projects and supports power producers, plant operators and other stakeholders in the development, construction and operation of photovoltaic and solar energy plants as well as in the construction of battery storage systems. The focus is on large-scale industrial projects.

Despite the spectacular 2022 lease sales, not all is rosy for US offshore wind development.

In 2011, then-Interior Secretary Ken Salazar said the Obama administration had set a goal of “10 gigawatts of offshore wind generating capacity by 2020 and 54 gigawatts by 2030.” How has that worked? Well, 11 years after Salazar’s speech, the US has seven turbines operating offshore with a total of capacity of 42 megawatts — or some 9,958 megawatts short of the goal laid out by Salazar.

Gordon Hughes, a professor of economics at the University of Edinburgh, has found that the output of Europe’s offshore wind turbines has been declining by about 4.5% per year. In a report titled “Wind Power Economics: Rhetoric and Reality,” published by the London-based Renewable Energy Foundation in 2020, Hughes concluded that declining output will result in higher operating costs that will start to exceed revenues “after 12 or 15 years.

…addressing climate change through ocean “industrialization” using an “inefficient, expensive and largely untested strategy” was not the right path forward – Kari Martin, Clean Ocean Action

“By undertaking an industrialization project this big, it far outweighs any (climate change) benefit anybody’s ever talked about, or even tried to quantify,” he said. “The harms of this undertaking is, in my view, far worse than any benefits we could realize.” – Michael Dean, Middletown, NJ

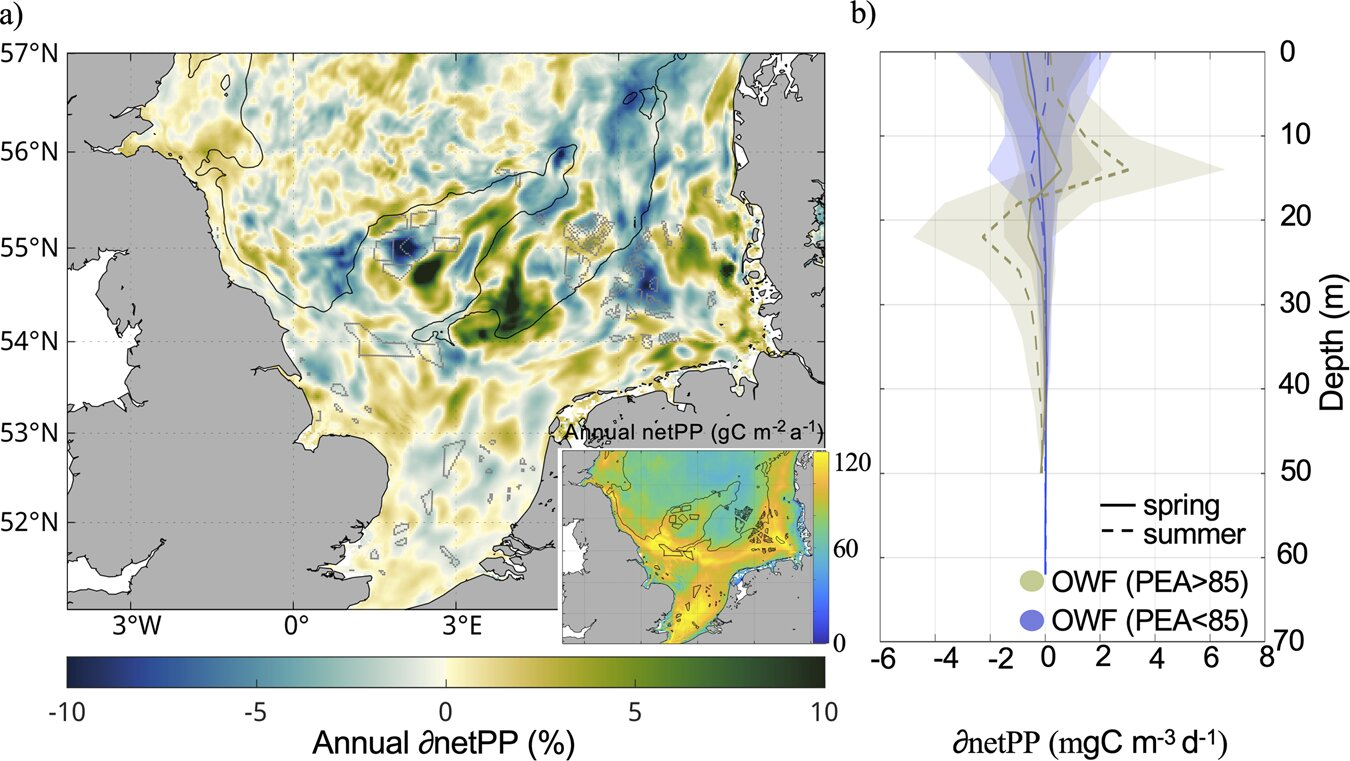

In their latest publication, (scientists at the Helmholtz-Zentrum Hereon) now show that large-scale wind farms can strongly influence marine primary production as well as the oxygen levels in and beyond the wind farm areas. Their results were published in the journal Communications Earth & Environment.

… For example, Nils Christiansen’s team proved that wake turbulences—air vortices caused by wind turbines—change the flow and stratification of the water beneath them. But the climate just above the sea surface is also being permanently changed, as another team led by Dr. Naveed Akhtar was able to show.

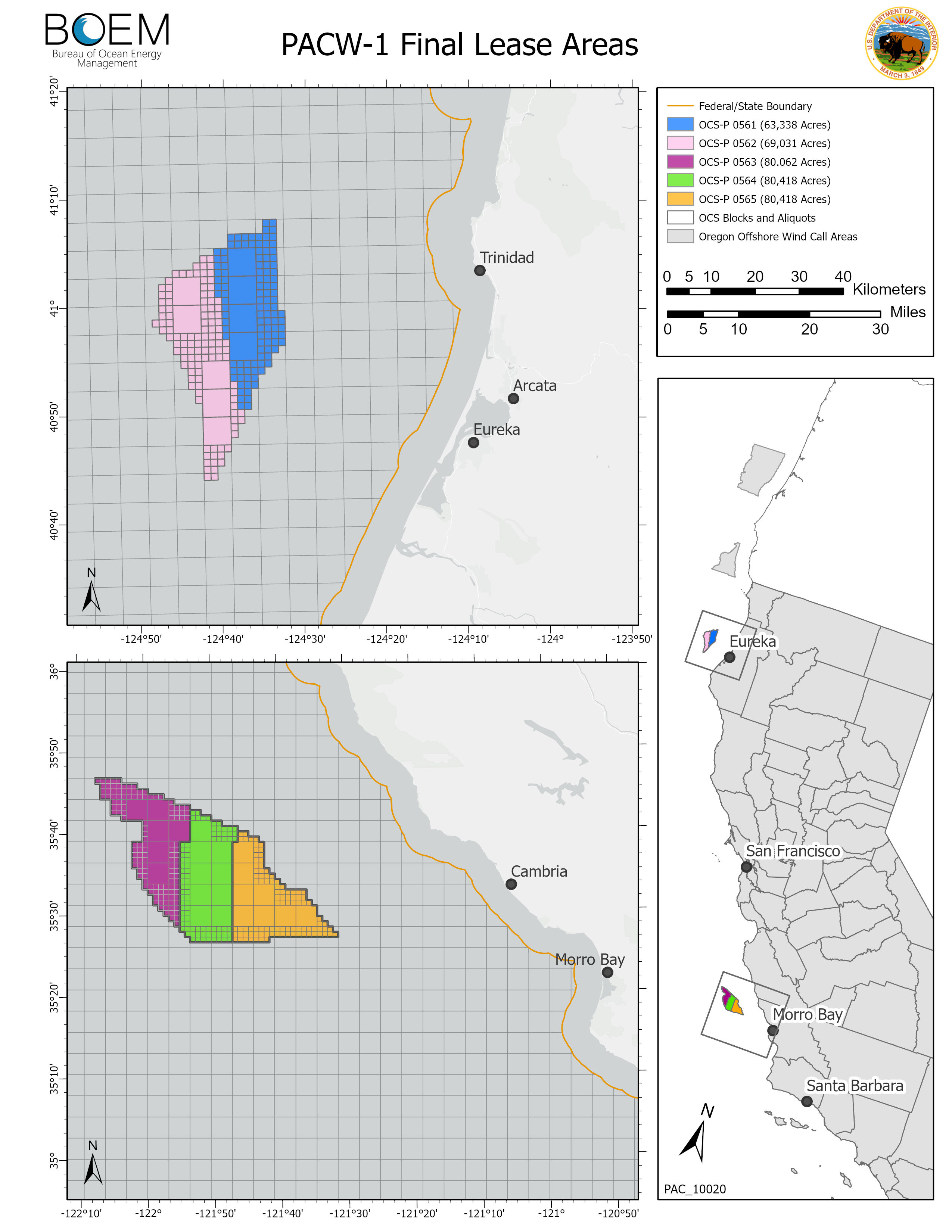

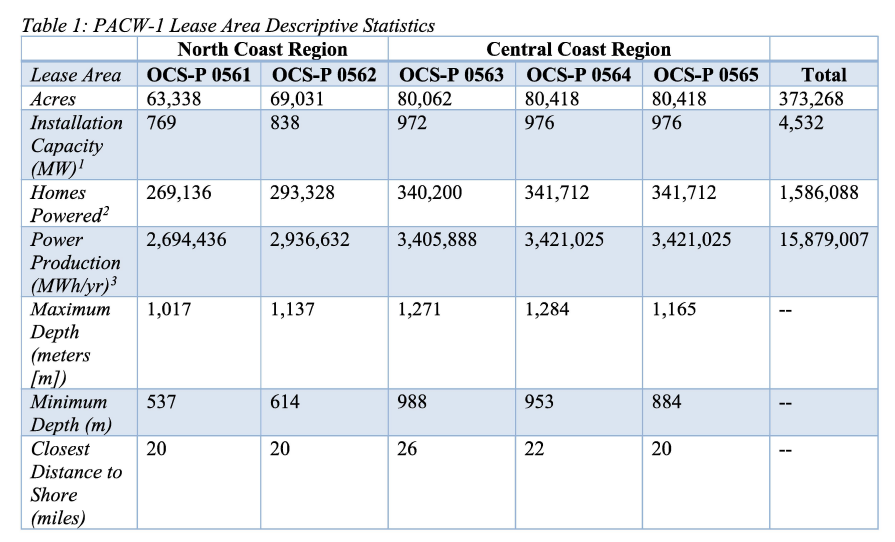

The California wind sale bidding, while lower than the record Atlantic sale in February, was extraordinary given that the 5 leases are relatively distant from shore (20+ miles) and in water depths (537 to 1284 m) that dictate the use of floating turbines. Generous subsidies, credits, and State mandates no doubt contributed to the seemingly inflated bidding, as did an auction system that is designed to maximize bonus payments.

Given the slow progress in US offshore wind development, the setbacks the industry is experiencing, the added challenges associated with commercial deepwater development, the potential cost burden on taxpayers and power customers, and the government’s financial and policy support, a more development-friendly leasing system would seem to be prudent. BOEM took a step in that direction with the with the limited training and supply chain credits provided for in the Sale Notice, but fundamental changes in the auction system may be desirable.

The biggest difference between the wind and the oil and gas programs may be the way the sales are conducted. For oil and gas leases, you submit a single sealed bid. Here is a simplified description of how a wind lease sale is conducted:

At the start of each round, BOEM will state an asking price for each Lease Area. A bid at the full asking price is referred to as a “live bid.”

If the bidder has qualified for a non-monetary credit, it will meet the asking price by submitting a multiple-factor bid—that is, a live bid that consists of a monetary (cash) element and a non-monetary credit.

To participate in the next round of the auction, a bidder is required to have submitted a live bid for one of the Lease Areas (or have a carried-forward bid) in each previous round.

As long as there are two or more live bids (including carried-forward bids) for at least one of the Lease Areas, the auction moves to the next round

If there was only one live bid (including carried-forward bids) or no live bids for a Lease Area in the previous round, the asking price would not be increased.

A live bid would automatically be carried forward if it was uncontested in the previous round, and the bidder who placed the uncontested bid would not be permitted to place any other bid in the current round of the auction.

Conversely, if a live bid was contested in the previous round, the bidder who placed the contested bid would be free to bid on any Lease Area in the auction in the next round, at the new asking price.

If a bidder decides to stop bidding before the final round of the auction, there are circumstances in which the bidder could nonetheless win a lease.

Between rounds, BOEM will disclose to all bidders that submitted bids: (1) the number of live bids (including carried-forward bids) for each Lease Area in the previous round of the auction.

In any round after the first round, a bidder may submit an “exit bid” only for the same Lease Area as the bidder’s contested live bid in the previous round. An exit bid is a bid that is greater than the previous round’s asking price, but less than the current round’s asking price.

The auction ends (finally) when a round occurs in which each of the Lease Areas in the auction receives one or zero live bids (including carried-forward bids), regardless of the number of exit bids on any Lease Area.

Perfectly clear? You can read the full description in the Sale Notice.

Is this the best way to award offshore wind leases?

As a result of a provision in the Inflation Reduction Act, leases may be sold but not awarded. See the paragraph below that was inserted at the end of the sale notice. No wind leases may be issued until Sale 259 oil and gas leases are issued (presumably late next spring).

XV. Compliance With the Inflation Reduction Act (Pub. L. 117-169 (Aug. 16, 2022)(Hereinafter, the “IRA”):

Section 50265(b)(2) of the IRA provides that “[d]uring the 10-year period beginning on the date of enactment of this Act . . . the Secretary may not issue a lease for offshore wind development under section 8(p)(1)(C) of the Outer Continental Shelf Lands Act (43 U.S.C. 1337(p)(1)(C)) unless— (A) an offshore lease sale has been held during the 1-year period ending on the date of the issuance of the lease for offshore wind development; and (B) the sum total of acres offered for lease in offshore lease sales during the 1-year period ending on the date of the issuance of the lease for offshore wind development is not less than 60,000,000 acres.” Section 50264(d) of the IRA provides that “. . . not later than March 31, 2023, the Secretary shall conduct Lease Sale 259[.]” Conducting Lease Sale 259 is needed for BOEM to satisfy the requirements in section 50265(b)(2) of the IRA and issue the leases resulting from this lease sale. Notwithstanding the foregoing, nothing in the IRA prevents BOEM from holding this auction.

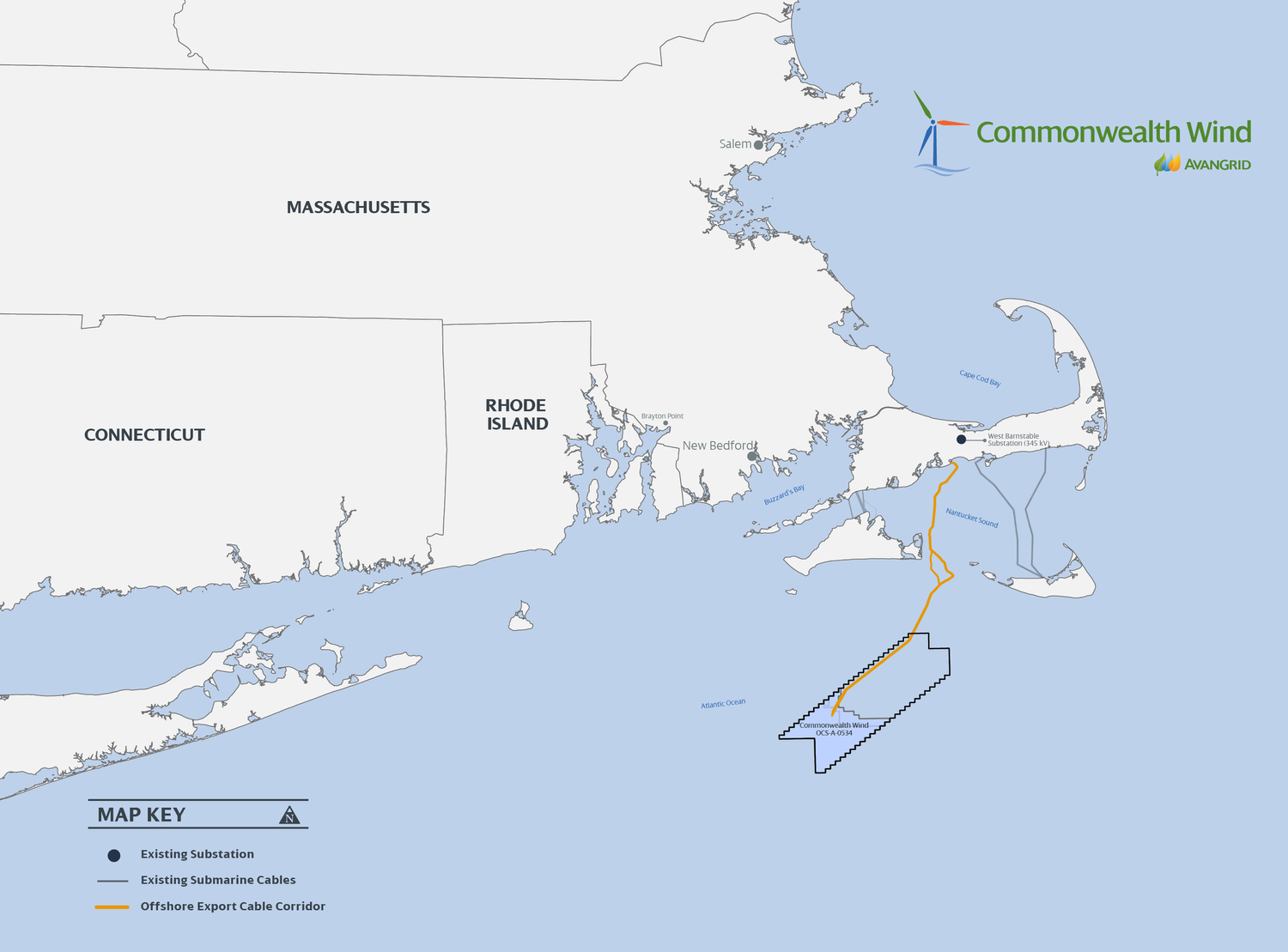

In particular, this suspension would allow the parties to examine the effect of unprecedented commodity price increases, interest rate hikes, and supply shortages on the overall viability of Commonwealth Wind’s offshore wind generation project that is the subject of the PPAs (the “Project”), including whether it remains economic and whether it can be financed under the current terms of the PPAs. A one-month suspension would also enable the parties to consider potential approaches to restore the Project’s viability – including cost saving measures, tax incentives under the newly enacted Inflation Reduction Act, an increase in the PPA prices, and improvements to Project efficiencies – and to determine whether additional time, beyond the period requested in this Motion, is needed to resolve the appropriate path forward or provide a complete record.

At a minimum, the expected commercial operation date, already more than 5 years into the future (2028), would seem to be threatened.

GUILDFORD, UK — Alpha Petroleum Resources, Energean UK and Orsted Hornsea Project Four will consider repurposing the Wenlock gas platform in the UK southern North Sea, which is nearing the end of its productive life.

One possibility is to reuse the facility as an artificial nesting site to offset the impact on certain bird species of offshore wind developments in the area.

Black-legged kittiwakes have set up nests on various North Sea platforms, according to Orsted’s recent surveys. Repurposing an existing platform as an artificial nesting structure is seen as an alternative to building a new artificial nesting structure to support the local development of the Hornsea Four offshore wind farm.

The energy sections begin on page 232 and continue until the end (page 725!). Some highlights from an offshore energy perspective (more important items in bold):

p. 429 – Tax credit eligibility for offshore wind energy components including blades, nacelles, foundations, and towers.

p. 447 – Credits for CCS equipment

p. 460 – For offshore wind facilities, this section specifies the % of the total costs that must be expended in the US for the facility to qualify as being manufactured in the US. That % rises gradually to 55% after 12/31/2027.

p. 518 – Eligibility of CCS for credits

p. 615 – $100 million for offshore wind electricity transmission planning, modelling, and analysis. (Seems like a lot for planning and analysis.)

p. 621 – $10 million for oversight by DOE Inspector General. (Those folks will have their hands full!)

p. 628 – Authorizes wind leasing in the EGOM and South Atlantic areas withdrawn from all leasing at the end of the Trump administration.

p. 631 – Authorizes offshore wind leasing adjacent to US territories. (Should be interesting!)

p. 632 – Codifies increase in offshore royalty rates: range of 16 2/3% – 18 3/4% for 10 years; not less than 16 2/3 % thereafter

p. 640 – The provision requiring that royalty be paid on flared/vented gas could be problematic. The exceptions are not consistent with those currently in the regulations, and would be difficult for BSEE/ONRR to manage. The proposed legislation (exception 1) exempts “gas vented or flared for not longer than 48 hours in an emergency situation that poses a danger to human health, safety, or the environment.” However, current BSEE regulations allow limited (48 hours cumulative) flaring for certain operations (e.g. during the unloading or cleaning of a well, drill-stem testing, production testing, and other well-evaluation testing). This flaring is essential but not normally an emergency situation. Requiring royalty payments for such essential, but not emergency, flaring would be unreasonable and inconsistent with the intent of this provision (minimize unnecessary flaring and venting).

p. 641 – Per our previous post, this section reinstates Lease Sale 257 (GoM) and requires that the scheduled 2022 lease sales 258 (GoM) and 259 (Cook Inlet) be held by 12/31/2022. Lease Sale 261 (GoM) must be held by 9/30/2023. Saddle up!