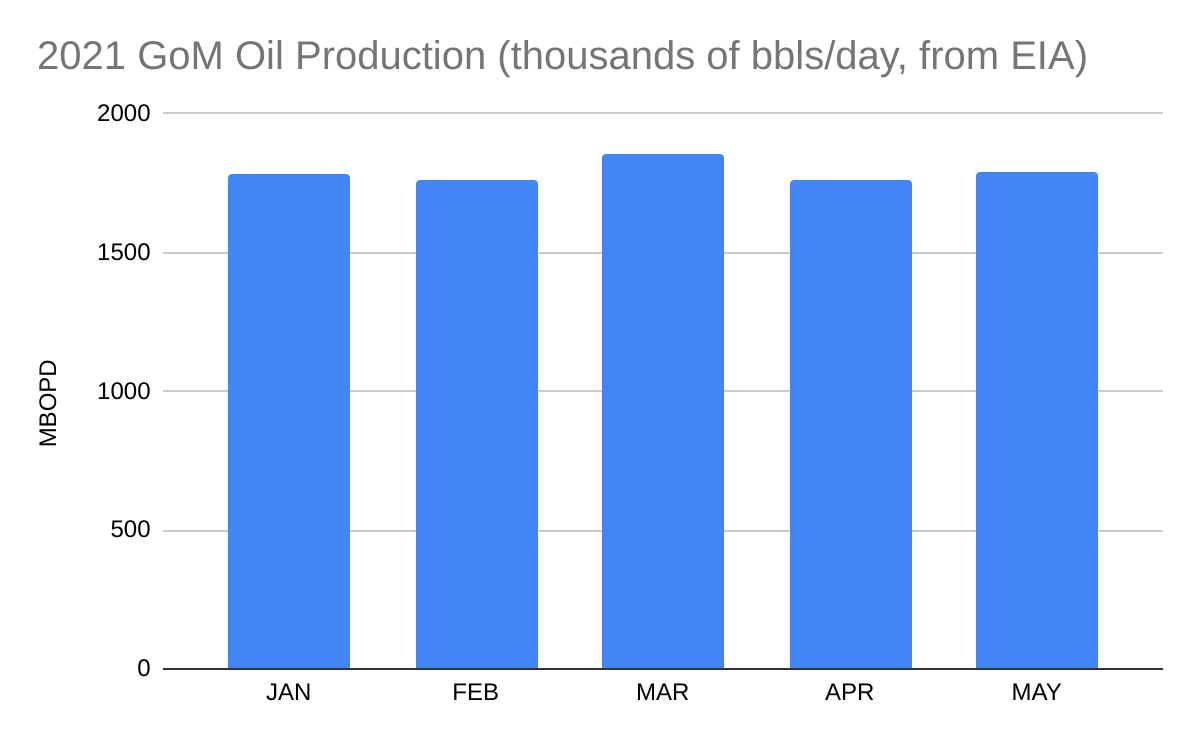

A previous BOE post estimated that current stabilized GoM oil production rates were 1.7 – 1.8 million BOPD. EIA recently announced that May production was 1.791 million BOPD, which is consistent with our estimate. Per the chart below, GoM production was essentially unchanged from the beginning of the year despite a 37% increase in the price of oil (WTI) from 1 January to 31 May. This suggests that stabilized GoM production may have peaked pending first oil from several new projects.

Key production questions:

- Will new production from Mad Dog 2, Vito, PowerNap, Thunder Horse South 2, and the recently sanctioned Whale project offset high depletion rates elsewhere in the deepwater GoM?

- Looking further ahead, is deepwater GoM production sustainable without increased drilling activity? Per BSEE data, only 33 deepwater wells were started in 2021 YTD, just 18 of which are classified as exploratory. Drilling is thus at historic low levels. For reference, there were 477 wells started in 2001, 149 of which were exploratory. This level of activity facilitated a 30% growth in oil production, peaking at 2 million BOPD in 2019.

Regardless of one’s views on the urgency and timing of the “energy transition,” is there any doubt that oil and gas will continue to be important to our economy and security for years to come? If not, should deepwater GoM production, with its relatively low carbon intensity, be a core element of our energy strategy? To better understand the trade-offs, I suggest that BOEM’s Environmental Studies Program conduct a peer reviewed assessment of the carbon intensity of domestic and international supply alternatives. Product transportation considerations should be included in this assessment.

Leave a comment