“Despite our previously unified stance, some Members of our conference now feel compelled to defend wind and biofuel credits, advocate for carbon capture and hydrogen subsidies, or protect solar and electric vehicle giveaways. Keeping even one of these subsidies opens the door to retaining all eight. How do we retain some of these credits and not operate in hypocrisy?The longstanding Republican position has been to allow the market to determine energy production. If every faction continues to defend their favored subsidies, we risk preserving the entire IRA because no clearly defined principle will dictate what is kept and what is culled.“

OCS Lease Sale 259 was mandated by Congress, and was held on March 29, 2023, two days before the deadline established in the Inflation Reduction Act. Ah, but compliance with environmental law, which is of course subject to interpretation, was still required.

So the formula for eNGOs in such cases is to sue on NEPA grounds in a friendly Federal court. In the case of Sale 259, the plaintiffs asserted that BOEM’s climate change and Rice’s whale analyses were inadequate.

With regard to climate change, the reality is that incremental Gulf of America production will have virtually no effect on petroleum consumption and global GHG emissions. Increased GoA production will actually have a slight positive effect on worldwide GHG emissions given the relatively lower carbon intensity for deepwater Gulf production.

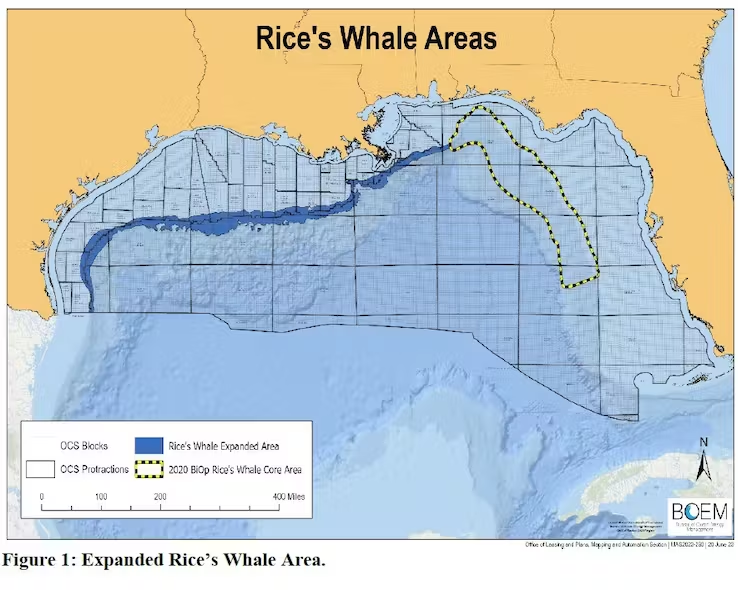

“Based on the limited data available on the use and occurrence of Rice’s whale in the central and northwestern GOMx (one acoustic study (Soldevilla et al. 2022b), one confirmed sighting (NMFS 2018a) and a few unconfirmed sightings (Rosel et al. 2021)), there is insufficient scientific evidence to determine that essential features for Rice’s whale conservation are indeed present in the central and northwestern GOMx. In fact, data on the life-history requirements of Rice’s whale even in the core habitat are still lacking and need further investigation.“

Unsurprisingly, Judge Amit P. Mehta of the US District Court for the District of Columbia, has ruled that BOEM’s environmental assessments on climate change and the Rice’s whale were deficient, and has ordered the parties and intervenors to jointly submit a proposed briefing schedule by April 3, 2025. “The court will also order additional briefing on remedy” (e.g. onerous operating restrictions).

In case you haven’t suffered enough, the judge’s full opinion is attached.

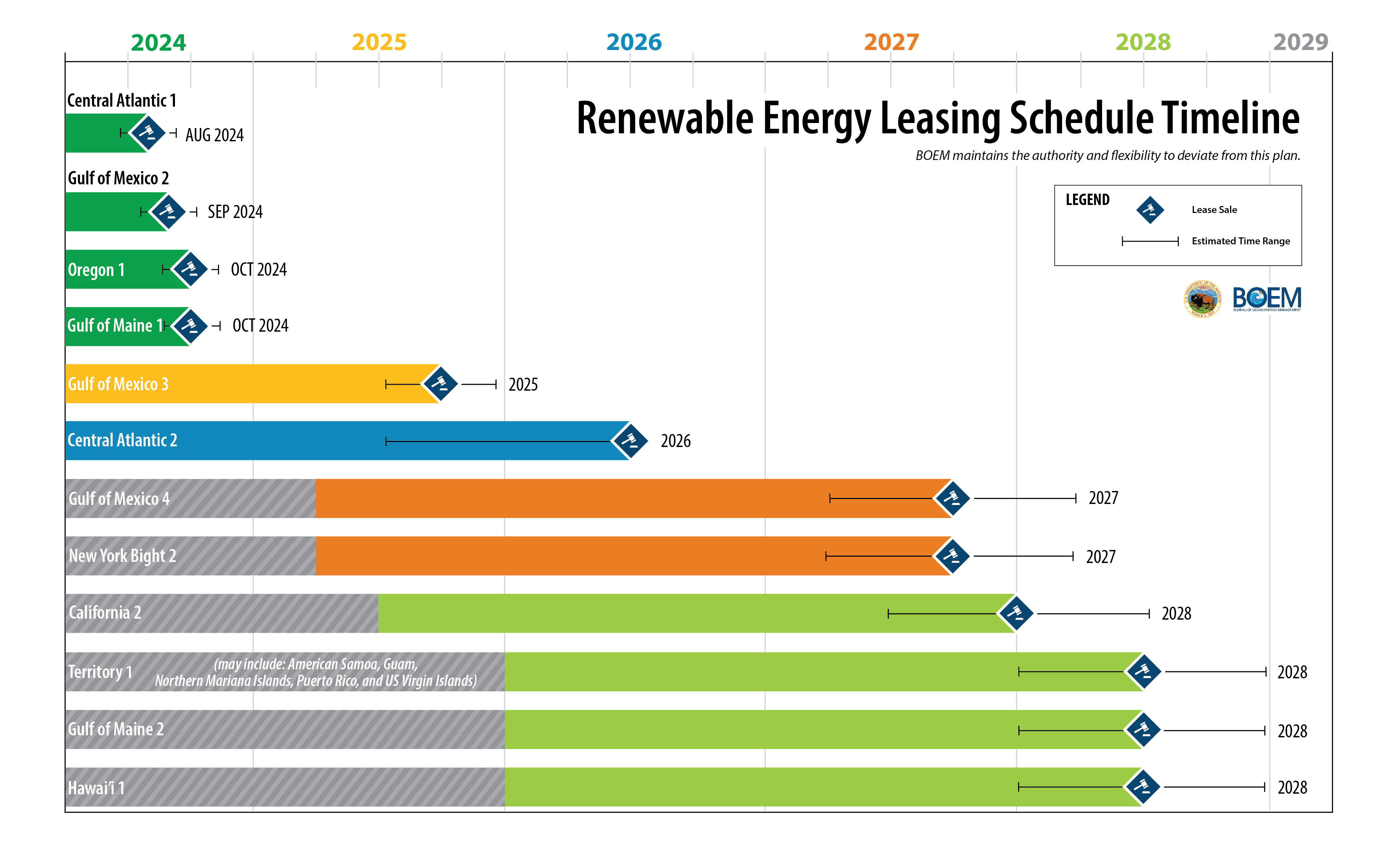

Per a provision in the “Inflation Reduction Act,” no offshore wind leases may be issued after 12/20/2024, the one year anniversary of the last oil and gas lease sale (no. 261).

Although the 4 leases receiving bids at the most recent wind sale (10/29/2024, Gulf of Maine) have presumably been issued, BOEM’s lease table does not reflect that. If those leases have not been issued, it’s too late now.

Assuming that the Gulf of Maine leases have in fact already been issued, the legislative restriction on issuing new leases should not be an issue. A qualifying oil and gas lease sale will likely be held in the Gulf of Mexico in the first half of 2025.

The bigger question is whether the new administration will hold any wind lease sales. Pre-election energy policy comments imply that new wind sales are unlikely.

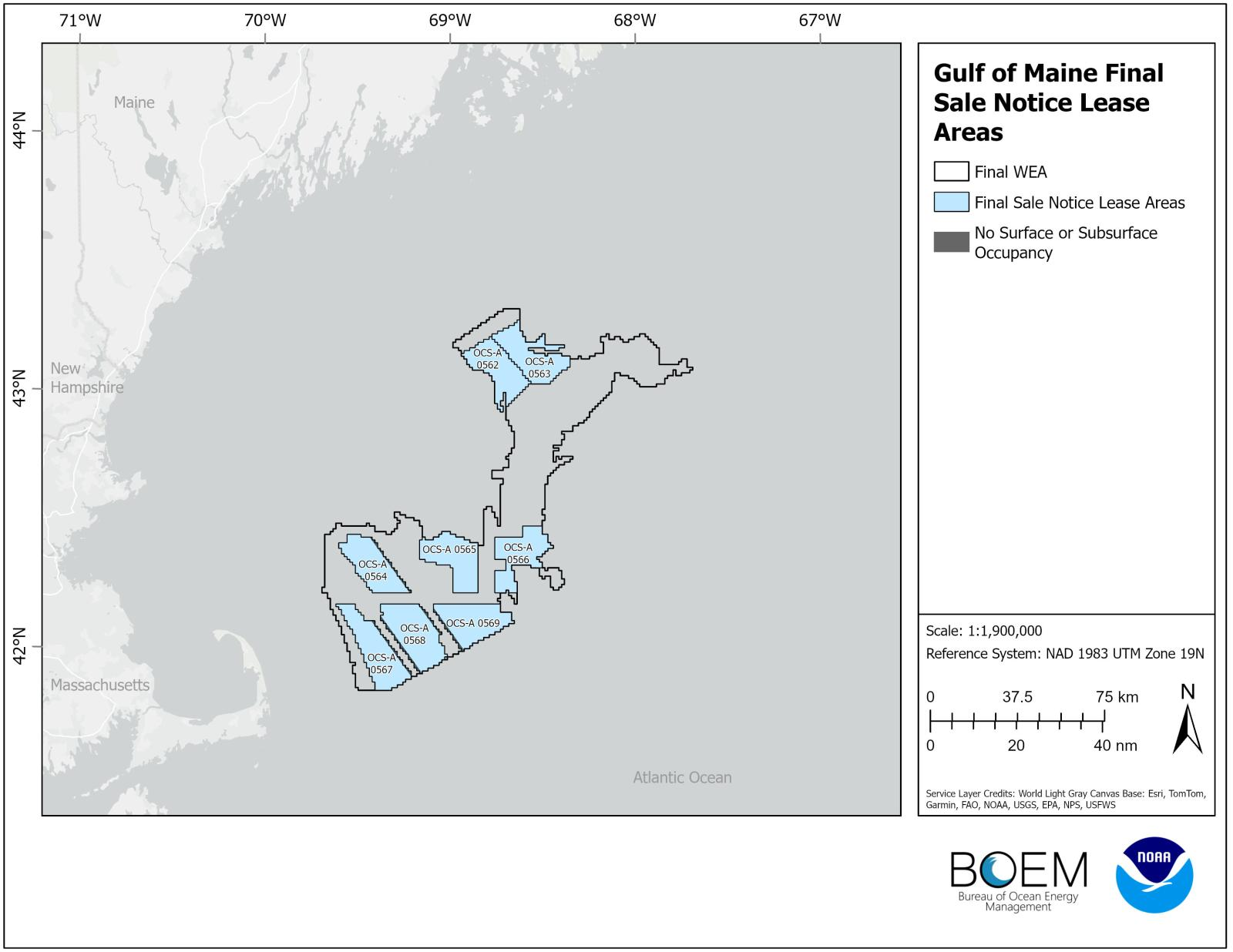

Gulf of Maine Final Lease Areas, Acres, and Assigned Region

Lease Area ID

Total Acres

Developable Acres

OCS-A 0562

97,854

97,854

OCS-A 0563

105,682

105,682

OCS-A 0564

98,565

93,756

OCS-A 0565

103,191

103,191

OCS-A 0566

96,075

96,075

OCS-A 0567

117,780

113,208

OCS-A 0568

124,897

116,363

OCS-A 0569

106,038

101,757

Total

850,082

827,886

Average

106,260

103,486

Note that the ave. lease size is 18.4 times larger than a typical Gulf of Mexico oil and gas lease

Today’s Gulf of Maine sale will likely be the last wind lease sale for at least a year.

Per a provision in the “Inflation Reduction Act,” no offshore wind leases may be issued after 12/20/2024, the one year anniversary of the last oil and gas lease sale (no. 261).

The date of the next oil and gas lease sale is anyone’s guess. Next week’s elections are, of course, the elephant in the room. However, there is also an enormous ruling by a Federal judge in Maryland that would halt the issuance of Gulf of Mexico oil and gas leases and the approval of operating plans effective Dec. 20, 2024. Ironically (or perhaps not?), this is the same date after which no wind leases may be issued absent an oil and gas lease sale.

Chevron and industry trade associations have appealed Judge Boardman’s ruling. (Given the enormous implications of that ruling on current and future Gulf of Mexico production, I’m curious as to why Chevron is the only major producer that is a party in this appeal. Chevron was also the only producer that was a party in the litigation overturning the restrictive Sale 261 lease sale provisions. I’m assuming there is some legal or tactical reason for the absence of participation by Shell, bp, and Oxy?)

Finally, given the legislation linking future wind sales with oil and gas sales, are the Sierra Club et al, the plaintiffs in this case, comfortable with Judge Boardman’s decision? Perhaps they are okay with the judge’s ruling given the absence of any planned Atlantic wind leasing until 2026?

In response to a lawsuit filed by the Sierra Club et al, a Federal judge in Maryland vacated a 2020 biological opinion by the National Marine Fisheries Service (part of NOAA) that addressed risks to endangered species, most notably Rice’s whale, from oil and gas operations in the Gulf of Mexico. The decision by Federal Judge Deborah Boardman, who was appointed to her position in 2021, is attached.

Judge Boardman’s ruling is effective on Dec. 20, 2024. After that date, no new GoM leases may be issued and no new operating plans may be approved pending a new biological opinion. Existing GoM operations could also be affected. In other words, the ruling could have unprecedented effects on the OCS oil and gas program. (If you wonder how a Maryland judge can issue a ruling that could have major consequences for Louisiana and Texas, it is presumably because NOAA’s headquarters office is in Silver Spring, MD.)

The biological opinion process will likely be lengthy given the political considerations in an election year and the prospects for related litigation.

The judge’s ruling could also affect wind leasing in a manner that was perhaps unforeseen. Offshore wind leasing, which the plaintiffs strongly support despite the risks to the critically endangered North Atlantic Right Whale, could be delayed. Per a provision in the “Inflation Reduction Act,” no offshore wind leases may be issued after 12/20/2024, the one year anniversary of the last oil and gas lease sale (no. 261). Ironically, this is the same date as the effective date of the judge’s ruling.

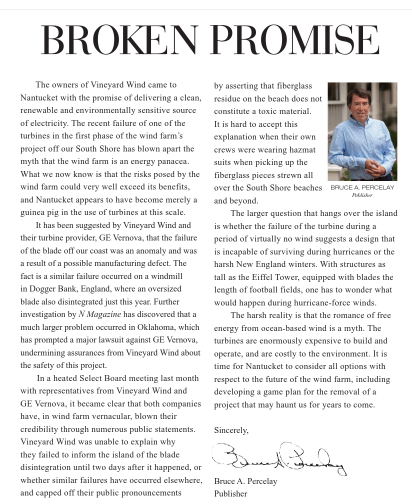

The judge’s decision will likely further delay the next oil and gas lease sale (no. 262) well into 2025 or later, and extend the pause in issuing wind leases that begins on 12/20/2024. Perhaps with that in mind, BOEM has been forging ahead with wind auctions despite the troubling Vineyard Wind blade failure, economic challenges for the wind industry, and growing opposition from coastal residents. An editorial by the publisher of Nantucket Magazine expresses concerns that should not be overlooked in the rush to auction wind leases.

(More on a new biological opinion related to the Right Whale in a future post.)

(2) the Secretary may not issue a lease for offshore wind development under section 8(p)(1)(C) of the Outer Continental Shelf Lands Act (43 U.S.C.1337(p)(1)(C)) unless— (A) an offshore lease sale has been held during the 1-year period ending on the date of the issuance of the lease for offshore wind development; and (B) the sum total of acres offered for lease in offshore lease sales during the 1-year period ending on the date of the issuance of the lease for offshore wind development is not less than 60,000,000 acres.

Lease Sale 261 was held on 12/20/23. Absent legislative action, no wind leases may be issued after 12/20/24 unless another oil and gas lease sale is held prior to that date. Given that the minimalist 5 year oil and gas leasing plan, which is being challenged, does not propose a sale until 2025, wind lease issuance will likely be suspended at the end of the year. (Note: I wonder if the legislative restriction also applies to lease assignments from existing owners to new owners? Probably not, but that would be very significant given the current state of the offshore wind industry.)

Perhaps the wind program should be required to develop 5 year leasing plans, as is the case for the oil and gas program. This might facilitate a more holistic approach to wind energy development and ease concerns about cumulative impacts.

The current leasing policy as articulated in both the draft and final proposed program is to phase out oil and gas production:

The long-term nature of OCS oil and gas development, such that production on a lease may not begin for a decade or more after lease issuance and can continue for decades, makes consideration of net-zero pathways relevant to the Secretary’s determinations on how the National OCS Program best meets the Nation’s energy needs.

Basing leasing decisions on highly uncertain “net-zero pathways” would seem to be a considerable stretch of the Secretary’s authority under the OCS Lands Act. A strategic shutdown of the offshore oil and gas program, which would dramatically increase energy supply and security risks going forward, should be authorized by Congress. Even the threat of such a shutdown could have major economic implications.

Senator Manchin and the Alaska delegation criticized the DOI decision memo for Sale 258. The memo implied that the highest allowable royalty rate was chosen to minimize bidder interest and limit future production. Unfortunately, the “Inflation Reduction Act,” which mandated these lease sales, was not particularly helpful in creating interest in the less attractive OCS tracts like those in the Cook Inlet and the shallower waters of the Gulf of Mexico.

Sec. 50261 of the IRA raised the minimum allowable royalty rate from 12 1/2% to 16 2/3%, while capping the maximum rate at 18 3/4%. This provision favors deepwater operators, typically majors and large independents, whose royalty rates were capped at 18 3/4%, the same rate as for previous OCS sales.

Conversely, the IRA royalty provisions penalize the smaller companies and gleaners who are critical to sustaining shallow water (shelf) operations, including environmentally favorable nonassociated (gas-well) natural gas production, by raising the minimum royalty rate to 16 2/3%. DOI exacerbated IRA’s impact by electing to charge the highest allowable royalty rate for Cook Inlet and GoM shelf leases. The net result was a 50% royalty rate increase from prior sales (12.5 to 18.75%).

The table below illustrates the royalty rate implications of the IRA language and the DOI decisions.

Area

Sale

Date

% royalty: <200m water depth

% royalty: >200m water depth

Cook Inlet

244

6/21/2017

12.5

12.5

GoM

256

11/18/2020

12.5

18.75

GoM

257

11/17/2021

12.5

18.75

Cook Inlet

258

12/30/2022

18.75

18.75

GoM

259

3/29/2023

18.75

18.75

Notes:

The base primary term for GoM shelf leases is only 5 years vs. 10 years for leases in .>800 m of water.

In lease year 8 and beyond the rental rates are nearly double for shelf leases vs. deepwater leases ($40/ac vs. $22/ac).

While deepwater development typically requires more time, the higher rental penalty for delayed shelf production (which must be approved by BSEE) is not warranted. $40/acre or $240,000 per year (plus inspection and permitting fees) is a high cost for a marginal shelf lease.

Cook Inlet Sale 244 drew 14 high bids totaling more than $3 million. Sale 258 drew only 1 bid of $64,000. While many factors influence lease sale participation, the 50% increase in royalty rate certainly made the Cook Inlet leases less attractive.

Other than the increased royalty rate, the terms for both Cook Inlet sales were essentially the same. The primary lease term was 10 years and the minimum bonus bid was $25/hectare for both sales. The rental rate was increased by only $3/hectare ($13 to $16).

As a result of a provision in the Inflation Reduction Act, leases may be sold but not awarded. See the paragraph below that was inserted at the end of the sale notice. No wind leases may be issued until Sale 259 oil and gas leases are issued (presumably late next spring).

XV. Compliance With the Inflation Reduction Act (Pub. L. 117-169 (Aug. 16, 2022)(Hereinafter, the “IRA”):

Section 50265(b)(2) of the IRA provides that “[d]uring the 10-year period beginning on the date of enactment of this Act . . . the Secretary may not issue a lease for offshore wind development under section 8(p)(1)(C) of the Outer Continental Shelf Lands Act (43 U.S.C. 1337(p)(1)(C)) unless— (A) an offshore lease sale has been held during the 1-year period ending on the date of the issuance of the lease for offshore wind development; and (B) the sum total of acres offered for lease in offshore lease sales during the 1-year period ending on the date of the issuance of the lease for offshore wind development is not less than 60,000,000 acres.” Section 50264(d) of the IRA provides that “. . . not later than March 31, 2023, the Secretary shall conduct Lease Sale 259[.]” Conducting Lease Sale 259 is needed for BOEM to satisfy the requirements in section 50265(b)(2) of the IRA and issue the leases resulting from this lease sale. Notwithstanding the foregoing, nothing in the IRA prevents BOEM from holding this auction.

Per legislation signed by the President on Aug. 16, 2022:

(b) LEASE SALE 257 REINSTATEMENT.— (1) ACCEPTANCE OF BIDS.—Not later 30 days after the date of enactment of this Act, the Secretary shall, without modification or delay— (A) accept the highest valid bid for each tract or bidding unit of Lease Sale 257 for which a valid bid was received on November 17, 2021; and (B) provide the appropriate lease form to the winning bidder to execute and return.