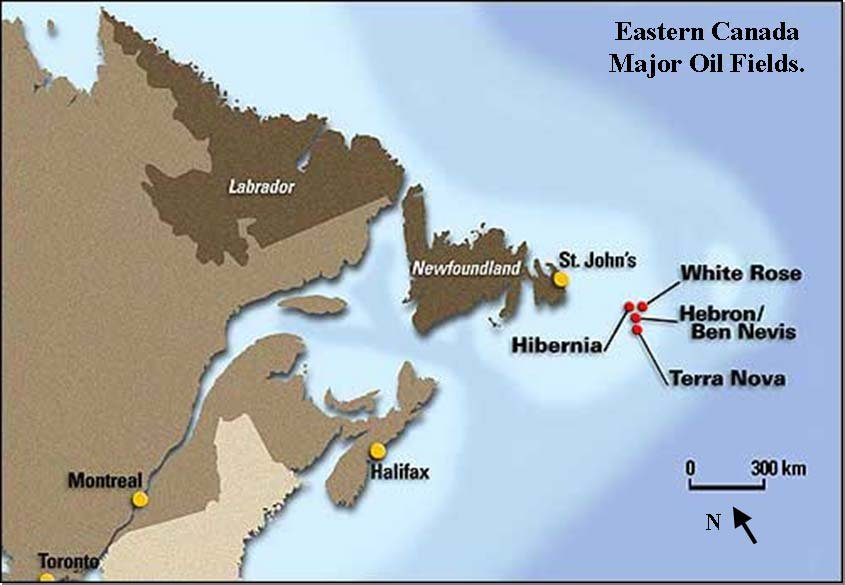

Offshore Newfoundland, a particularly hostile operating environment (“North Sea plus icebergs“), continues to be the only producing area in the North American Atlantic, a distinction that is unlikely to change for at least the next decade.

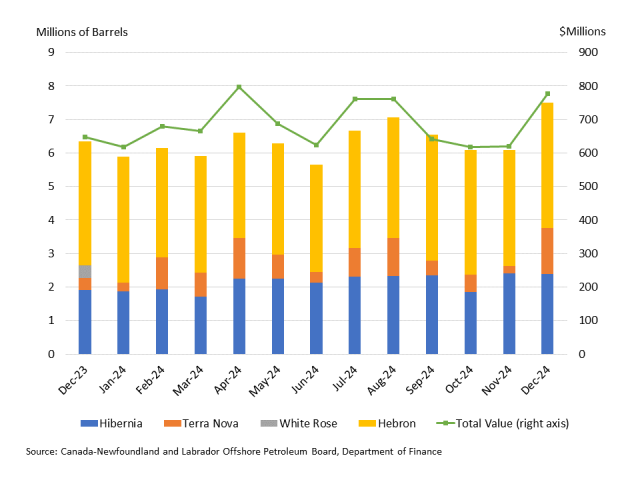

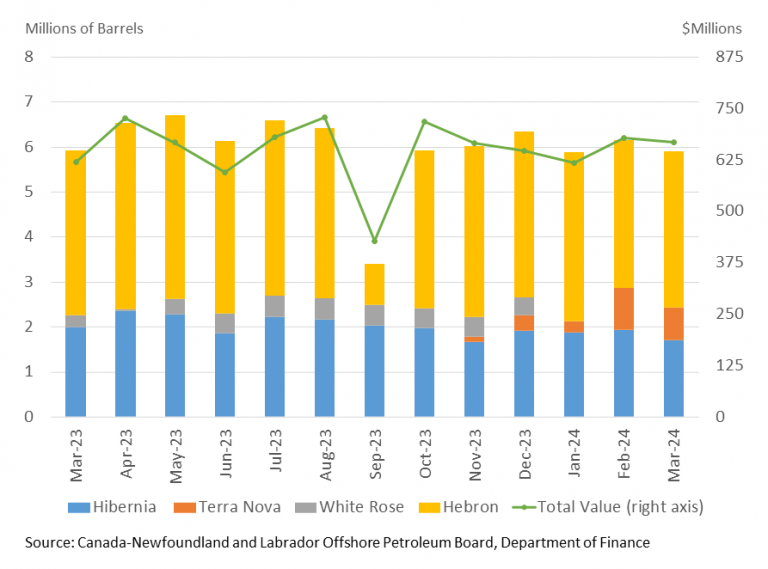

Production is holding firm and there was a nice bounce in December when 7.5 million barrels were produced (242,000 bopd ave.). December’s production was the highest since May 2022 and and was a respectable 57% of the May 2007 peak.

Most impressively, according to CNLOPB data, no fatalities or significant injuries occurred over the past 3 years.

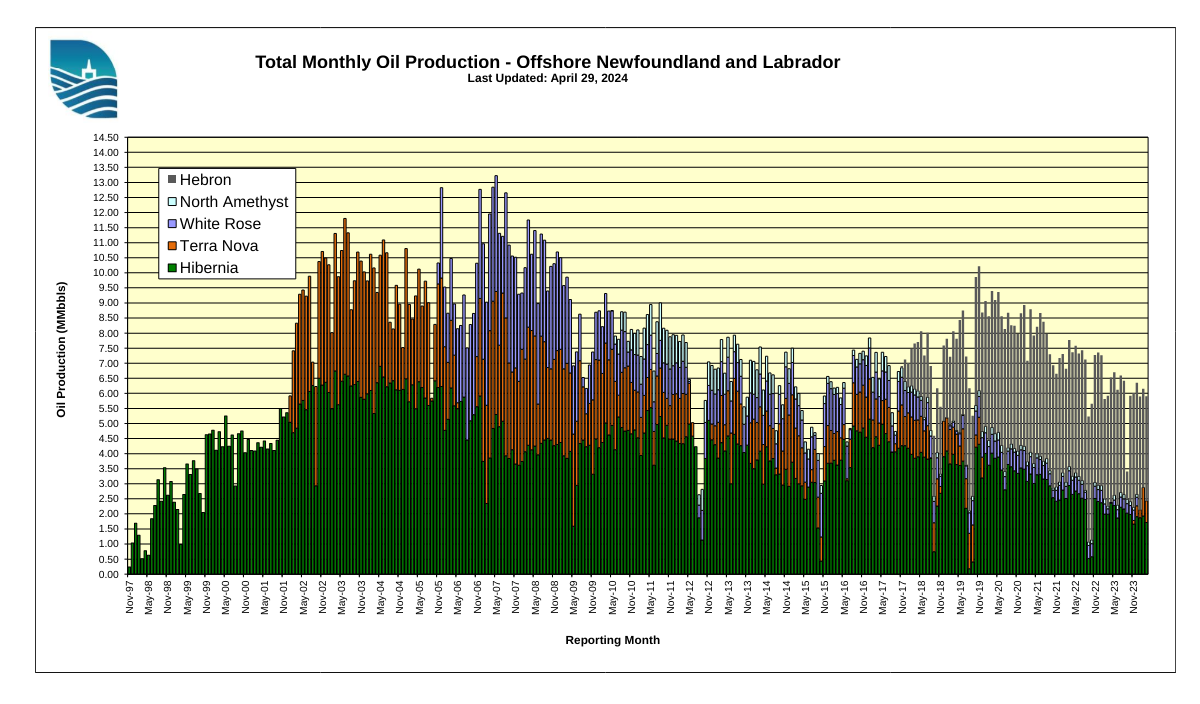

The pioneering Hibernia platform (pictured above), where Newfoundland offshore production began in Nov. 1997, keeps chugging along at 60 to 80,000 bopd. The Hibernia field has produced more than double the original resource estimate of 520 million barrels. Very impressive!

Hebron, the current top producer, continues to produce 100,000+ bopd

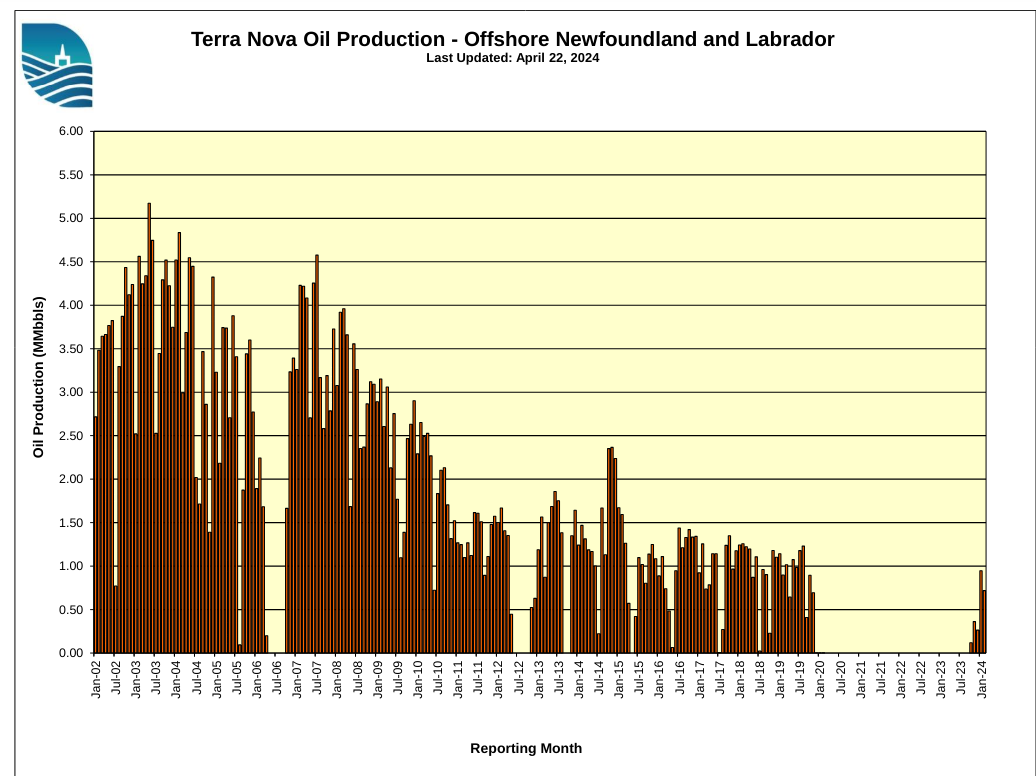

The Terra Nova field contributed ~40,000 bopd in Dec., the highest output since production resumed in late 2023 after extensive downtime to refurbish the FPSO.

While checking for updates on the important Orphan Basin well, I looked at Newfoundland production data and found it surprisingly encouraging:

The pioneering Hibernia field has produced more than double the original resource estimate of 520 million barrels, and is still chugging along at about 60,000 bopd.

Hebron, the current top producer, is holding strong at 100,000+ bopd.

White Rose, which was in danger of being abandoned, is poised for a renaissance with the installation of the West White Rose concrete gravity structure.

Terra Nova is once again producing at near 2019 levels after a four year hiatus. The Terra Nova story has many important technical, management, regulatory, safety, and logistical elements, and presents good case study opportunities for Newfoundland academics (Memorial University?).

With prospects for production at Bay du Nord brightening and interesting targets like the Orphan basin being explored, pessimistic forecasts for Newfoundland’s resilient offshore sector may be a bit premature.

The latest World Bank data tell us that significant gas flaring issues persist. Worldwide, 138,549 million m3 of gas were flared in 2022. This equates to a massive 4 tcf, the equivalent of the reserves in a major gas field and more than 5 times the total gas production in the Gulf of Mexico in 2022.

The top ten “flarers” are listed below. Each of these fields flared from 19 to 42 bcf. For comparison, the top ten GoM gas producers in 2022 produced 10 to 57 bcf, so single fields are flaring more than GoM companies are producing in total. Assuming for discussion purposes a gas-oil ratio of 1000 cu ft/bbl, all of the gas associated with 19 million to 42 million barrels of oil production was wasted from each field.

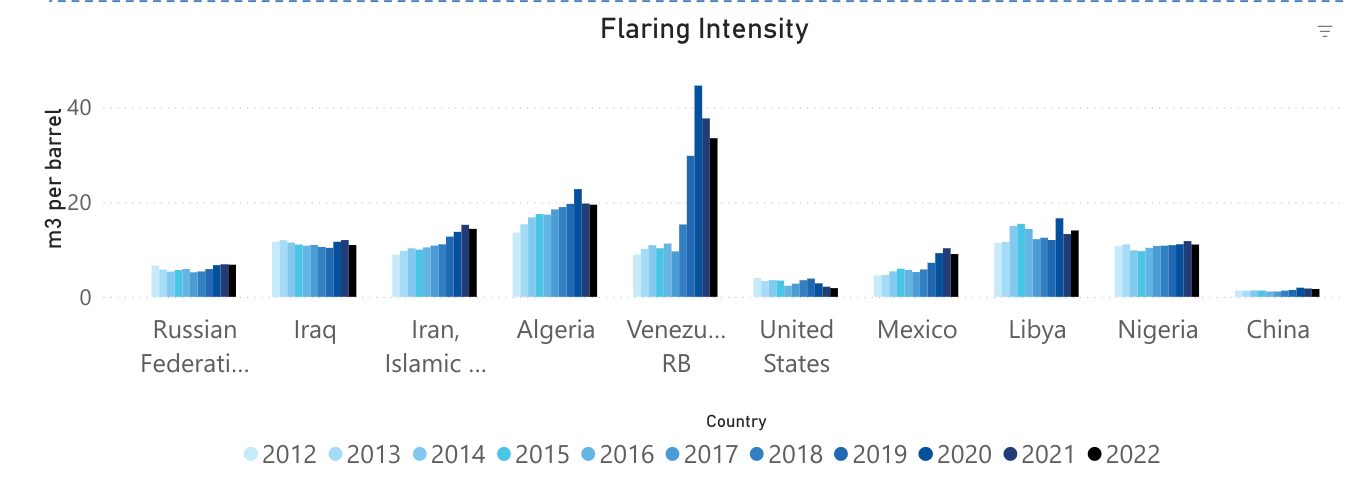

Posted below are the World Bank’s flaring intensity data (m3 of gas flared per bbl of oil produced) for the 10 countries with the highest flaring volumes. Venezuela’s flaring intensity rose to 44.6 m3/bbl in 2020, before declining moderately the following 2 years. 44.6 m3/bbl equates to 1575 cu ft/bbl. This gas flaring to oil production ratio implies that a very high percentage of Venezuela’s associated gas production was flared.

Here in North America, we have flaring issues of our own. Mexico’s Cactus Field is a top ten flarer (first table above) with 534.5 million m3 flared in 2022. The World Bank also lists 6 Permian Basin fields with >50 million m3 of gas flared in 2022.

Zeroing in on the US/Canada offshore sectors, fields with >1 million m3 of gas flared (2022) are listed below. Four of the top 7 are offshore Alaska and Newfoundland where the gas cannot currently be marketed and reinjection, field use, and flaring are the only options. Can production from these fields be better managed to reduce flaring volumes?