My mother was a hard-working Quaker farm girl who hung the wash outside until her final days and otherwise conserved energy in a manner that was consistent with her values – thrift, simplicity, and love of fresh air. While there are still many common sense conservationists, professional alarmists have gained control of environmental messaging and dominate fundraising. It may be time for the environmental community to reassess its direction.

Actually, it’s a case of the Ukraine invasion demonstrating the obvious – domestic production is critical to our economy and energy security. Europe and the US have had a wake-up call and responsible leaders now recognize the importance of secure supplies and the need to halt purchases from a tyrant.

The oil industry is doing just fine with $100+ per barrel oil. They will produce oil and gas where the opportunities present themselves: Guyana, Mexico, North Sea, Africa, Brazil, Canada, private lands in supportive US states, and elsewhere. The folly is US policy that unreasonably restricts exploration on Federal lands, including the Outer Continental Shelf. These restrictions penalize the owners of those lands, the people of the United States, not the oil industry and certainly not the Russian tyrant.

BSEE has posted the slides and presentation video announcing their draft Request For Proposals (RFP) to contract for the decommissioning of facilities on five Gulf of Mexico leases. Phase 1 involves the plugging of 15 wells. Per the presentation, this work would be paid for using “orphan well” funds appropriated in the 2021 Infrastucture bill.

Per BSEE’s online borehole file, the wells in question were drilled by Matagorda Island Gas Operations, Anglo-Suisse Offshore Partners, and Bennu Oil and Gas. Matagorda and Bennu declared bankruptcy and are no longer in business. The status of Anglo-Suisse is not entirely clear, but presumably they are no longer financially accountable.

Looking at BOEM online data, these leases had other owners including two US super-majors. However, the wells identified by BSEE were drilled after these and other financially strong companies had assigned their interest. They are thus not legally accountable, which is presumably why these wells were chosen for the RFP.

The unprecedented use of Federal funds for decommissioning reflects poorly on the offshore industry and Federal lease management practices. The financial risks associated with decommissioning have been apparent for more than 30 years (see the July 1991 Forbes article below). Why have these issues not been effectively addressed? Some thoughts:

Operating companies showed little interest in private industry-wide solutions. Rod Pearcy, one of the most respected managers in the history of the Federal offshore program, advocated an industry funded and managed entity to ensure financial assurance and guarantee well and facility decommissioning. This concept never gained traction.

Industry factions disagreed strongly on the regulatory approach that the Federal government should take. Simply put, “majors” wanted to limit future liability for leases they assigned. “Independents” wanted the assigning companies to retain liability such that their financial assurance requirements were minimized. These divisions continue to this day and are the main reason financial assurance regulations are so difficult to update.

Decommissioning costs vary wildly depending on the particular circumstances, making it difficult to establish the amounts of financial assurance to be required. For example, storm damage typically increases well and structure decommissioning costs by a factor of at least 10. Requiring worst case financial assurance amounts would preclude many assignments and the associated increase in oil and gas recovery.

Realistic amounts of bonding and other forms of financial assurance are routinely challenged by lessees and their political representatives.

Poor lease assignment and financial management decisions have significantly increased the risk exposure of predecessor lease owners and taxpayers. The troubling case of Platforms Hogan and Houchin, Santa Barbara Channel, demonstrates the implications of questionable lease assignments and the irresponsible use of decommissioning funds.

Government funded decommissioning will likely be more expensive and will subject the public to unforeseen costs and future liabilities should the operations not go as planned.

The future decommissioning of wind turbines is already a major issue, and measures must be taken to ensure that liability is clearly established and operator funding is assured.

In the past, the regulators, operating companies, and insurers have found ways to ensure that decommissioning costs did not fall on the taxpayer. BSEE continues to be resourceful in that regard. Private solutions should always be the objective. The proposed RFP opens the door to the potential for far greater Federal liabilities down the road, particularly given the uncertainty about predecessor liability in some important cases.

“The absolute earliest a new Lease Sale 257 could occur is July 2, which is after the expiration of the current five year program,” Interior said in a 28 February court filing (opting not to appeal the DC court decision invalidating the lease sale).

So, a new lease sale cannot occur until after the five year program expires and no sale may be held. Brilliant, Joseph Heller would be proud. It’s a good thing oil and gas supplies are plentiful and secure, and that prices are cheap.

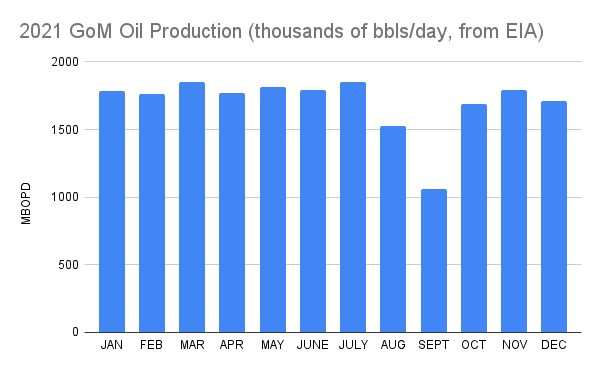

December 2021 oil production averaged 1.713 million bopd, lower than expected and down from 1.794 million bopd in Novermber. Given that the production lost during Hurricane Ida was to have been fully restored, BOE expected production to average greater than 1.8 million bopd.

January data will be helpful but won’t be available until 31 March. GIven the importance of these data and advances in information management, more timely updates should be an objective. We note that Norway released January production data on 22 February.

BP, Equinor, and Shell are exiting Russia, but Exxon’s response seems to be something less. Per Upstream:

US supermajor ExxonMobil is scaling back its operations on its flagship offshore development project in Russia’s Sakhalin Island region in response to the fallout from the crisis in Ukraine, according to the Sakhalin Online news website.

A consortium source cited by the Russian website claimed that foreign managers have been told to leave the project for an initial period of one month.

Exxon accepted the political risks associated with lucrative Russian production, and they now have a massive moral and public relations dilemma. Will they try to wait this crisis out or take more permanent actions?

It would be nice to see Exxon return to the Gulf of Mexico where they haven’t drilled a well since 2019. Currently, Exxon’s primary interest in the Gulf is for carbon sequestration purposes. Perhaps they can focus more on the Gulf’s still promising production potential and less on its potential as a disposal site.