Good article from our friends at the Petroleum Safety Authority of Norway. When old guys reminisce, people need to listen 😉

“Reagan feared that the world, and especially Europe, would become too dependent on Soviet gas, and saw Troll as an opportunity to create greater independence.”

“Lerøen sees parallels to the current situation, with Russia’s invasion of Ukraine, and the importance Norwegian gas has for the EU, which wants to become independent of Russian gas.”

The CEO of Italian power firm Enel has cast doubt on the continued benefit of using gas to produce electricity, telling CNBC it is“stupid” and that cheaper and better alternatives are now available.

“You can produce electricity better, cheaper, without using gas … Gas is a precious molecule and you should leave it for … applications where that is needed,” he added.

Gas is scarce and expensive in Europe because of bad foreign and energy policy decisions, most notably dependence on Russia and unrealistic expectations regarding renewables. Mr. Starace seems intent on doubling down on the latter. Of course, Enel is a large renewable energy generator and a natural gas purchaser and consumer (not a producer). His comments are thus rather self-serving.

I do agree with Enel on CCS:

Although the company could rely on carbon offsets or carbon capture to hit that target, Bernabei said the technology has failed to take off, despite receiving funding from the EU and national governments. He said there is no reason to expect that situation to change, especially since carbon capture and storage, or CCS, technology is not guaranteed to eliminate 100% of emissions.

“These are very big and complex projects. And at the end, they will not solve the problem,” Bernabei said. “We already tried CCS in the past and it didn’t lead to success. So why do it again?”

Germany has a very strong Green lobby that has now become part of the ruling coalition. Despite an anti-fossil fuel discourse, the Greens have now apparently accepted the necessity of at least one fossil fuel, perhaps not least because Germany has plans to shut down all of its nuclear power plants by the end of this year.

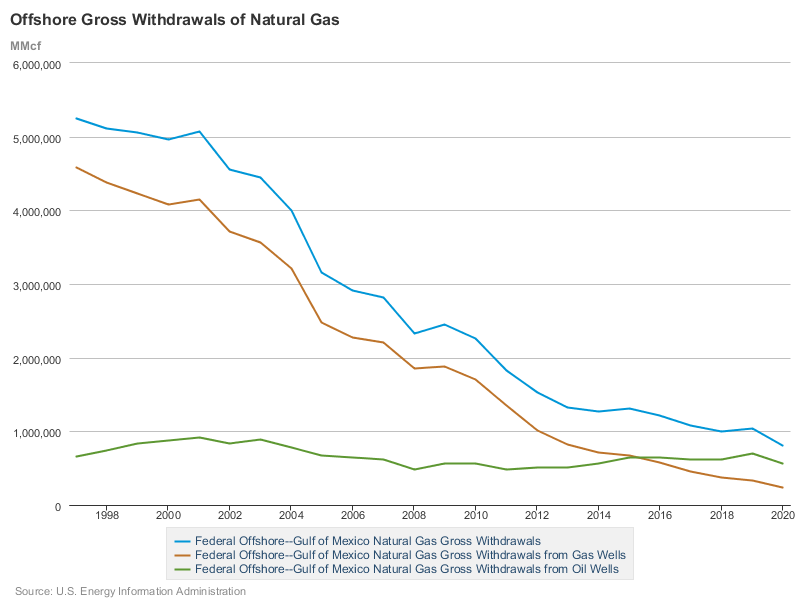

Offshore gas production (see chart below) has declined for the past 20 years and now accounts for only 4% of total US gas production, down from 20% in 2005 and 25% in the 1990s. Associated gas production (oil-well gas) has remained relatively constant owing to the strength in deepwater GoM oil production. 73% of 2020 gas production was from deepwater wells, and was mostly oil-well gas. Associated gas production surpassed nonassociated gas production (gas-well gas) in 2016 and the latter has continued to decline.

The case for natural gas has been well documented (see the EQT letter linked below). Recent natural gas advocacy has emphasized the carbon/GHG advantages given that methane (CH4) is essentially a hydrogen transporter that emits far less CO2 than other fossil fuels when burned. However, natural gas’s other important air quality advantages – low NOx. SO2, and particulate emissions – have greater local significance from a human health standpoint. Those who have ridden a bike behind a natural gas powered bus have no doubt experienced the natural gas advantage firsthand. These buses are literally a breath of fresh air!

Other environmental advantages of offshore natural gas, particularly nonassociated gas, receive less attention but are nonetheless significant. Advantages of nonassociated offshore gas include the following:

Fewer wells required than for shale gas

No risk of fresh water contamination

Platforms provide beneficial reef effects

Minimal space preemption and land disturbance relative to onshore gas production and wind/solar operations

Low facility density and navigation risks relative to wind operations;

Lower elevation and fewer view-shed, aesthetic, and aviation issues than for wind

Minimal avian risks relative to on- and offshore wind operations

Minimal spill risk relative to oil and associated gas production

Significantly less flaring than for oil well gas. While the overall % of US offshore gas production that is flared is low (approx. 1.0 -1.5% from 2016-2020 per EIA data), the % of gas-well gas that is flared has historically been less than 0.5%.

Low natural gas prices and competition from nimble and efficient shale operations have constrained offshore gas exploration. Ultradeep (subsurface) drilling has shown promise from a gas resource perspective but has proven to be expensive and operationally challenging. Some independent producers are still acquiring gas prone shelf tracts and that needs to be encouraged. Consideration should be given to incentives such as making nonassociated gas production royalty free. That would certainly seem preferable to subsidizing complex, expensive, and uncertain carbon disposal operations on offshore leases.

In 2019, the United States emitted 970 million metric tons less than in 2005, with 525 million metric tons of that emissions reduction resulting from replacing coal with natural gas in power generation. Said another way: since 2005, in the United States, all emissions reduction efforts combined have had less impact than coal to gas switching alone.

The emissions associated with the production of natural gas are dwarfed by the emissions reduction of switching from the consumption of coal to gas.

Meanwhile, China, which produced only 3% of the world’s natural gas but the majority of the world’s coal, saw its methane emissions increase by an amount roughly equivalent to adding a second Europe to the world.

Shares of McMoRan Exploration jumped more than 12% June 29 after the company announced that additional drillinghas confirmed its geological theories about the high potential of drilling ultra-deep natural gas prospects in the shallow waters of the Gulf of Mexico.

Hype, reality, or something in-between? One has to weigh the resource promise against the operational challenges, high costs, and gas market uncertainties.

A global shift away from nuclear power in response to the atomic plant crisis unfolding in Japan will likely spur a scramble for Australian energy, catapulting the country ahead of Qatar as the world’s biggest supplier of liquefied natural gas in the near future.

“The Honda Civic GX (the only NGV available to U.S. consumers and repeat winner of the ACEEE Green List) has been so successful Honda predicts it will double GX sales in the U.S. this year after doubling them in 2009. Utah, Oklahoma and California have been very successful in building out natural gas infrastructure and deploying NGVs that are refueling with natural gas.”SeekingAlpha.com

Supply does not appear to be an issue in light of the numerous domestic options including shale gas, Alaskan gas, coalbed methane, and conventional onshore and offshore gas. Given the proximity of enormous shale gas resources to major markets, shale gas is the featured attraction. However, this is an offshore blog, and from a strictly environmental perspective, offshore gas is the preferred option. Why?

No freshwater contamination issues

Small environmental footprint – limited facilities needs and minimal space preemption

No production in or near residential areas

Potential production near major natural gas markets. For example, there is a natural gas discovery in the Atlantic approximately 100 miles southeast of the New York City area. (Before my geologist friends get upset, I will point out that the productive reservoirs are highly complex and further exploration is necessary to determine whether this field – the former Hudson Canyon Unit – and other Atlantic prospects are commercially viable.)

Potential for combining offshore gas and wind projects into offshore energy units that can ensure consistent power supply. (See slide below from a presentation by George Hagerman, Virginia Tech Advanced Research Institute)

Rash statement? Hyperbole? Possibly, but shale gas is a game-changer for the northeastern US. How effectively will the resource be exploited? Will the true potential be realized? Stay tuned.

This New York Times article and video discuss the dispute on the island of Vinalhaven, Maine, about the noise associated with the island’s three wind turbines.

Comments:

-Locating wind projects offshore minimizes noise and visual issues, but increases costs and operational complexity. There are always trade-offs.

-When all environmental impacts are considered, offshore natural gas is tough to beat: minimal visual impacts, none of the freshwater issues that are complicating shale gas development, few land use issues, little or no spill risk (depending how dry the gas is). The trade-off is CO2 emissions. While combustion of natural gas emits 30% and 45% less CO2 than oil and coal respectively, the CO2 emissions are still significant.

![[OZLNG]](https://i0.wp.com/si.wsj.net/public/resources/images/AM-AM993_OZLNG_NS_20110316055703.jpg)