Per a provision in the “Inflation Reduction Act,” no offshore wind leases may be issued after 12/20/2024, the one year anniversary of the last oil and gas lease sale (no. 261).

Although the 4 leases receiving bids at the most recent wind sale (10/29/2024, Gulf of Maine) have presumably been issued, BOEM’s lease table does not reflect that. If those leases have not been issued, it’s too late now.

Assuming that the Gulf of Maine leases have in fact already been issued, the legislative restriction on issuing new leases should not be an issue. A qualifying oil and gas lease sale will likely be held in the Gulf of Mexico in the first half of 2025.

The bigger question is whether the new administration will hold any wind lease sales. Pre-election energy policy comments imply that new wind sales are unlikely.

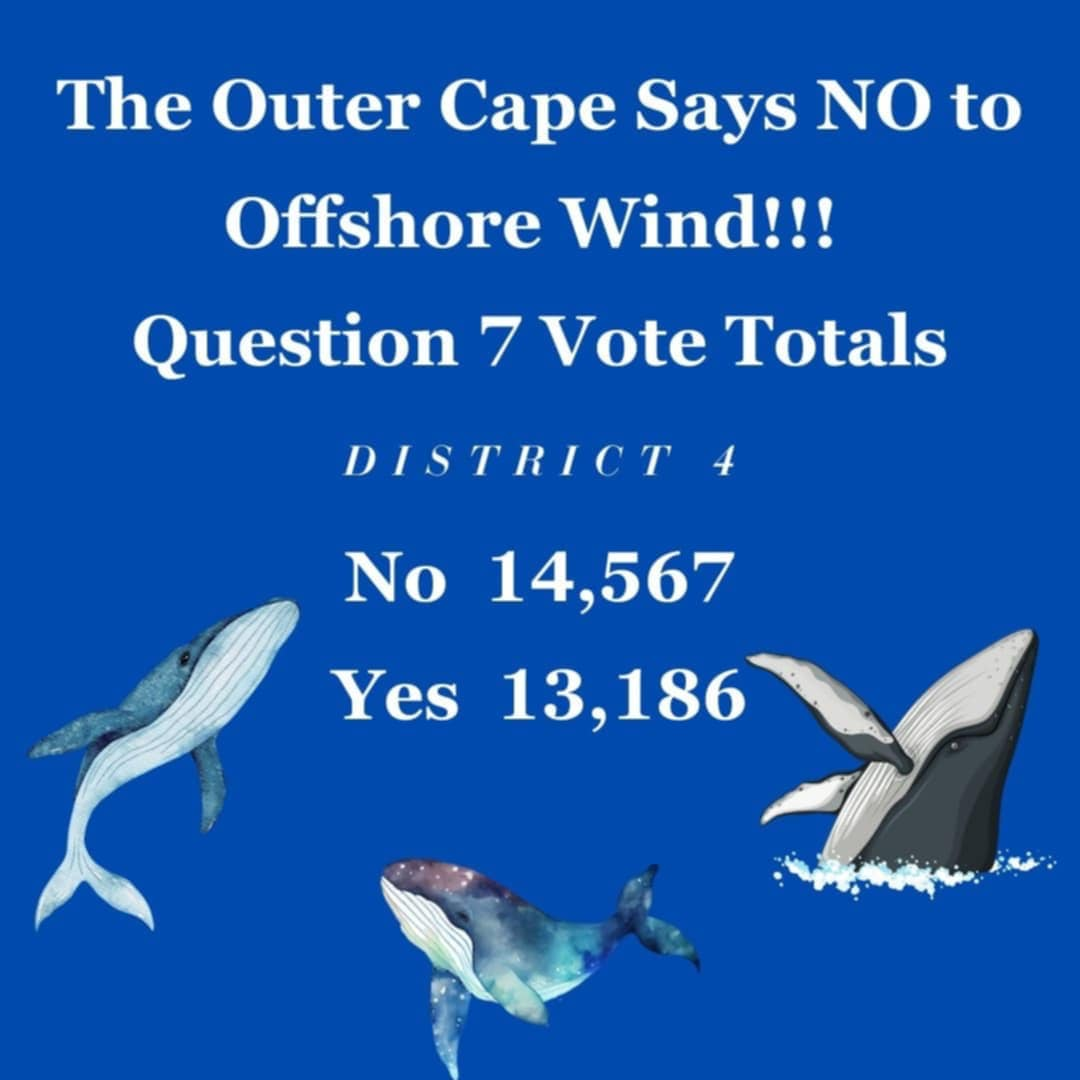

Ballot Question 7: Shall the State Representative from this district be instructed to vote in favor of legislation that would support the development of SouthCoast Wind and Commonwealth Wind and other possible future offshore and onshore wind power developments in Massachusetts?

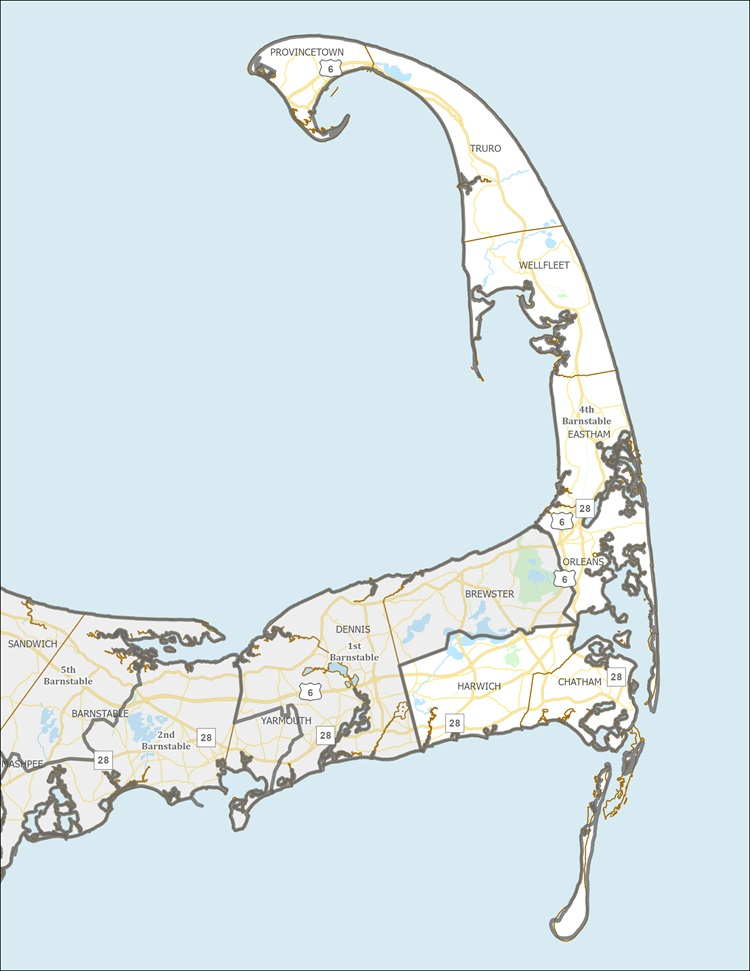

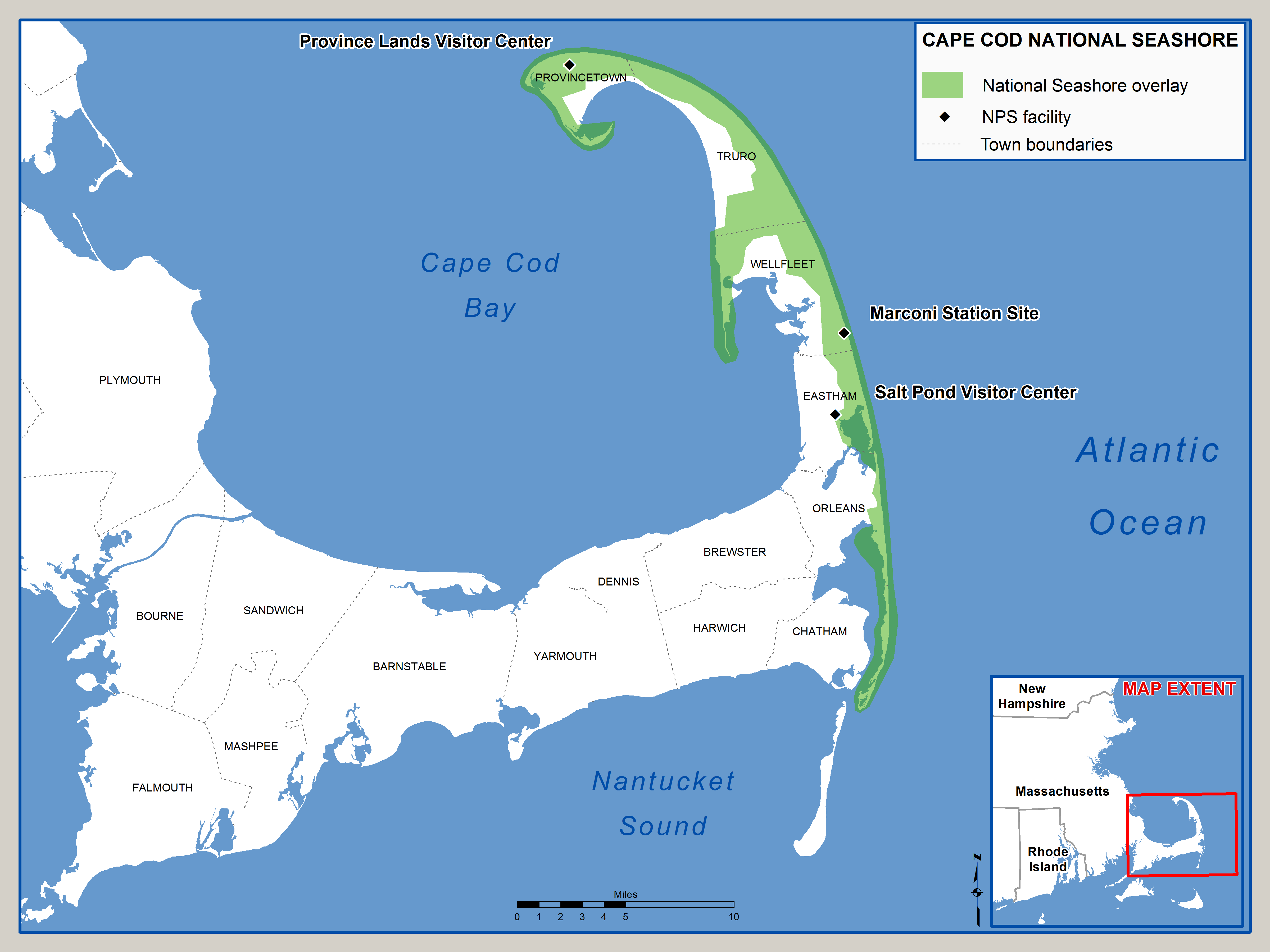

This nonbinding initiative, which was reportedly the work of an individual wind advocate, was a surprise addition to the ballot for residents of the 4th Barnstable District of the Massachusetts House. That district includes the Outer Cape towns of Chatham, Eastham, Harwich, Orleans, Provincetown, Truro, and Wellfleet (see map above).

While nonbinding, the ballot initiative was intended to demonstrate support among Outer Cape residents for offshore wind development. However, perhaps unexpectedly, the initiative failed with 52.4% voting against (graphic below). It’s noteworthy that 82% of South Shore (Massachusetts) voters supported offshore wind development when a similar initiative was on the ballot in 2008. That’s a massive decline in support albeit in a different coastal area of the state.

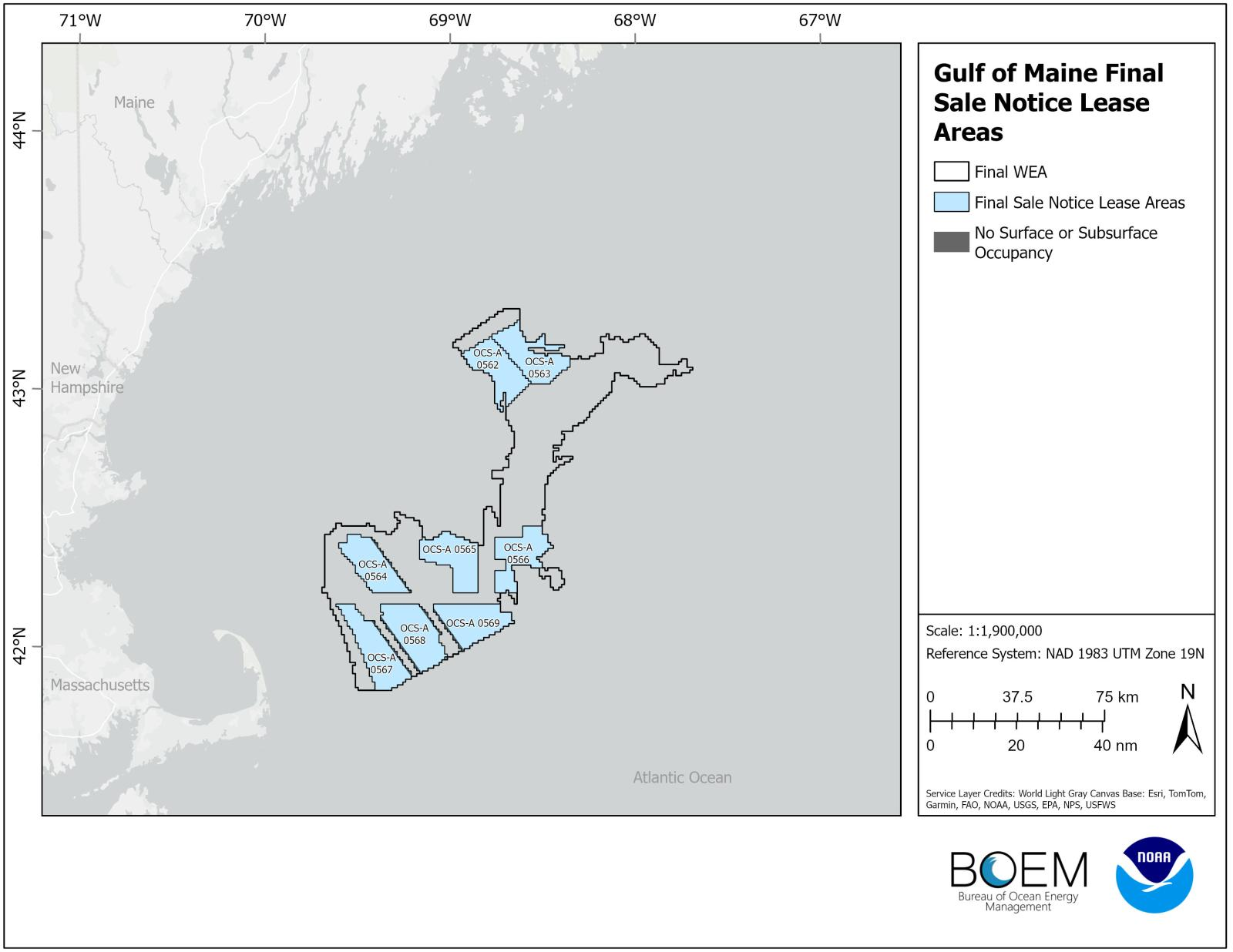

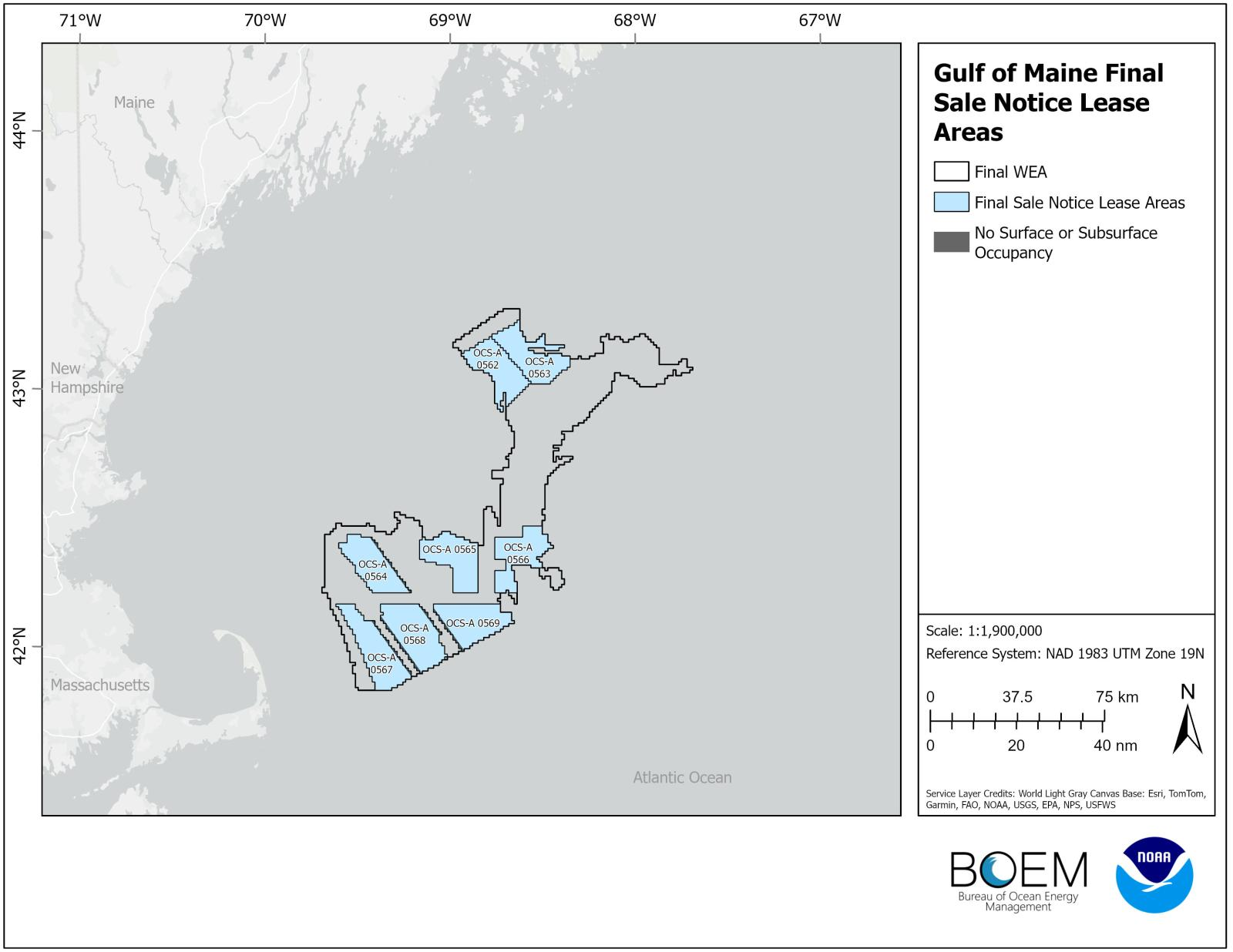

The opinion of Outer Cape residents is important because their towns are the closest to 3 of the 4 leases (0564, 0567, and 0568 in the graphic below) receiving bids at the Gulf of Maine sale. Those leases are directly offshore from the Cape Cod National Seashore.

The table below illustrates the dramatic decline in bidding for Atlantic wind leases over the past 2 years. (The California sale is also included in the table.)

offshore area

sale date

leases sold

acres leased

bonus bids ($ millions)

$/acre

NY/NJ

2/2022

6

488,000

4,370

8955

California

12/2022

5

373,268

757.1

2028

Central Atl.

8/2024

2

277,948

92.65

333

Gulf of Maine

10/2024

4

439,096

21.9

50

Accepting that bidding at the 2/2022 sale, which averaged nearly $9000/acre, was irrationally exuberant, bidding at this week’s sale was still incredibly weak. Even the bids at the Central Atlantic sale, just 2 months ago, averaged $333/acre, 6.7 times higher than the Gulf of Maine bids.

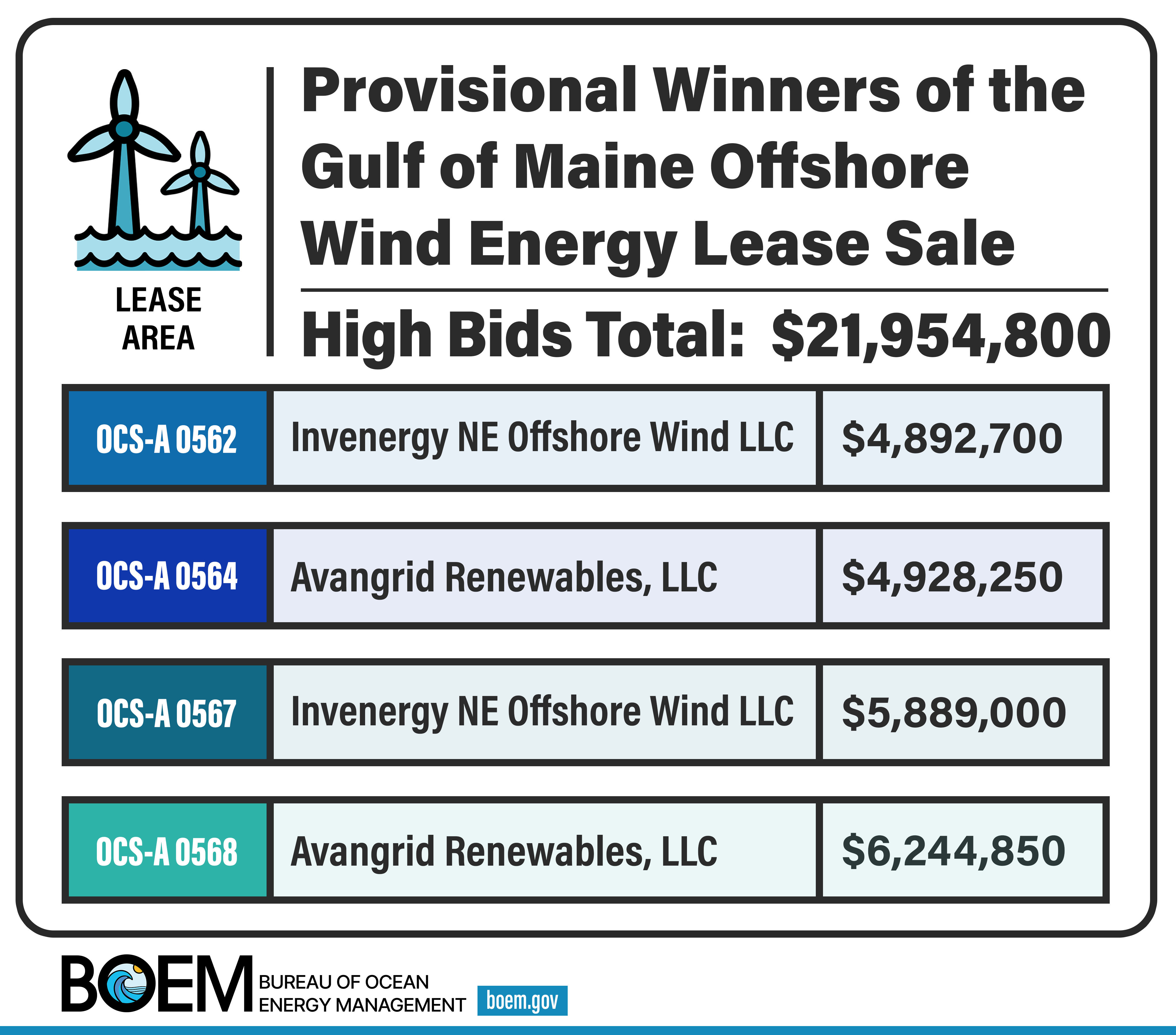

Do the Gulf of Maine bids pass BOEM’s fair market value tests? Apparently so; the sale notice established $50/acre as the minimum bid, and that is where the bidding started and ended. Invenergy and Avangrid had no competition and presumably got the tracts they wanted at the lowest possible price. We’ll see how this works out for the companies and power consumers.

Gulf of Maine Final Lease Areas, Acres, and Assigned Region

Lease Area ID

Total Acres

Developable Acres

OCS-A 0562

97,854

97,854

OCS-A 0563

105,682

105,682

OCS-A 0564

98,565

93,756

OCS-A 0565

103,191

103,191

OCS-A 0566

96,075

96,075

OCS-A 0567

117,780

113,208

OCS-A 0568

124,897

116,363

OCS-A 0569

106,038

101,757

Total

850,082

827,886

Average

106,260

103,486

Note that the ave. lease size is 18.4 times larger than a typical Gulf of Mexico oil and gas lease

Today’s Gulf of Maine sale will likely be the last wind lease sale for at least a year.

Per a provision in the “Inflation Reduction Act,” no offshore wind leases may be issued after 12/20/2024, the one year anniversary of the last oil and gas lease sale (no. 261).

The date of the next oil and gas lease sale is anyone’s guess. Next week’s elections are, of course, the elephant in the room. However, there is also an enormous ruling by a Federal judge in Maryland that would halt the issuance of Gulf of Mexico oil and gas leases and the approval of operating plans effective Dec. 20, 2024. Ironically (or perhaps not?), this is the same date after which no wind leases may be issued absent an oil and gas lease sale.

Chevron and industry trade associations have appealed Judge Boardman’s ruling. (Given the enormous implications of that ruling on current and future Gulf of Mexico production, I’m curious as to why Chevron is the only major producer that is a party in this appeal. Chevron was also the only producer that was a party in the litigation overturning the restrictive Sale 261 lease sale provisions. I’m assuming there is some legal or tactical reason for the absence of participation by Shell, bp, and Oxy?)

Finally, given the legislation linking future wind sales with oil and gas sales, are the Sierra Club et al, the plaintiffs in this case, comfortable with Judge Boardman’s decision? Perhaps they are okay with the judge’s ruling given the absence of any planned Atlantic wind leasing until 2026?

The New England Fishermen’s Stewardship Association (NEFSA) is sending the attached letter to Maine Gov. Janet Mills along with a petition with over 2,500 signatures urging her to halt the development of offshore wind farms in the Gulf of Maine.

A Gulf of Maine wind lease sale is scheduled for Oct. 29.