While a graduate student more than 50 years ago, I wrote a paper entitled “The Use of Natural Gas in Improving Air Quality.” My professor, Dr. Richard Gordon (RIP), a terrific economist who greatly influenced my thinking about energy, liked the paper but thought I was too optimistic about the availability of gas.

The sense at the time was that natural gas was a premium energy source in short supply. I was blissfully ignorant and thought we geologists and petroleum engineers would find and produce the gas. The Shale Boom, for which I can take zero credit, has proven me correct, so I’m taking another victory lap. 😀

Last week, the great Dan Yergin and his team at S&P Global issued a report that explains how economically and environmentally important natural gas has become. Key findings from the report are pasted below:

- Higher US LNG exports lead to lower overall global emissions by displacing the more GHG intensive fuels that would replace them.

- End use combustion is responsible for 57–87% of GHG intensity for coal, oil, gas and LNG, with supply chain methane emissions the key driver of variation between fuels (e.g., domestic vs. international LNG, domestic versus piped natural gas imports, or different crude oil streams).

- Coal emits roughly 70% more greenhouse gases than the US LNG it would replace across all the alternatives analyzed.

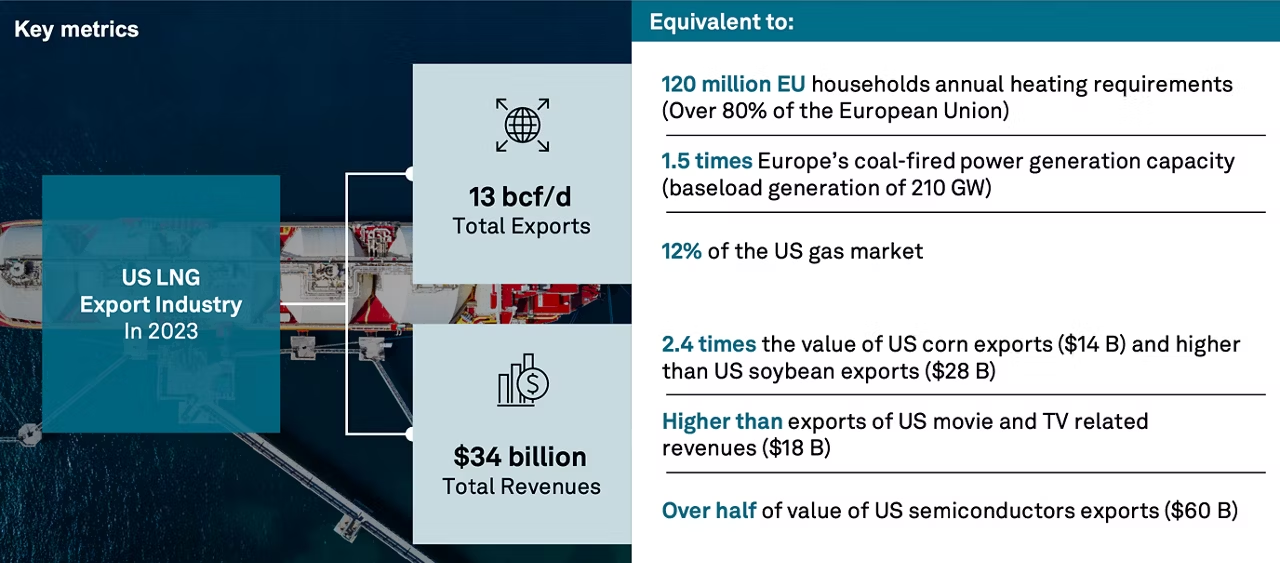

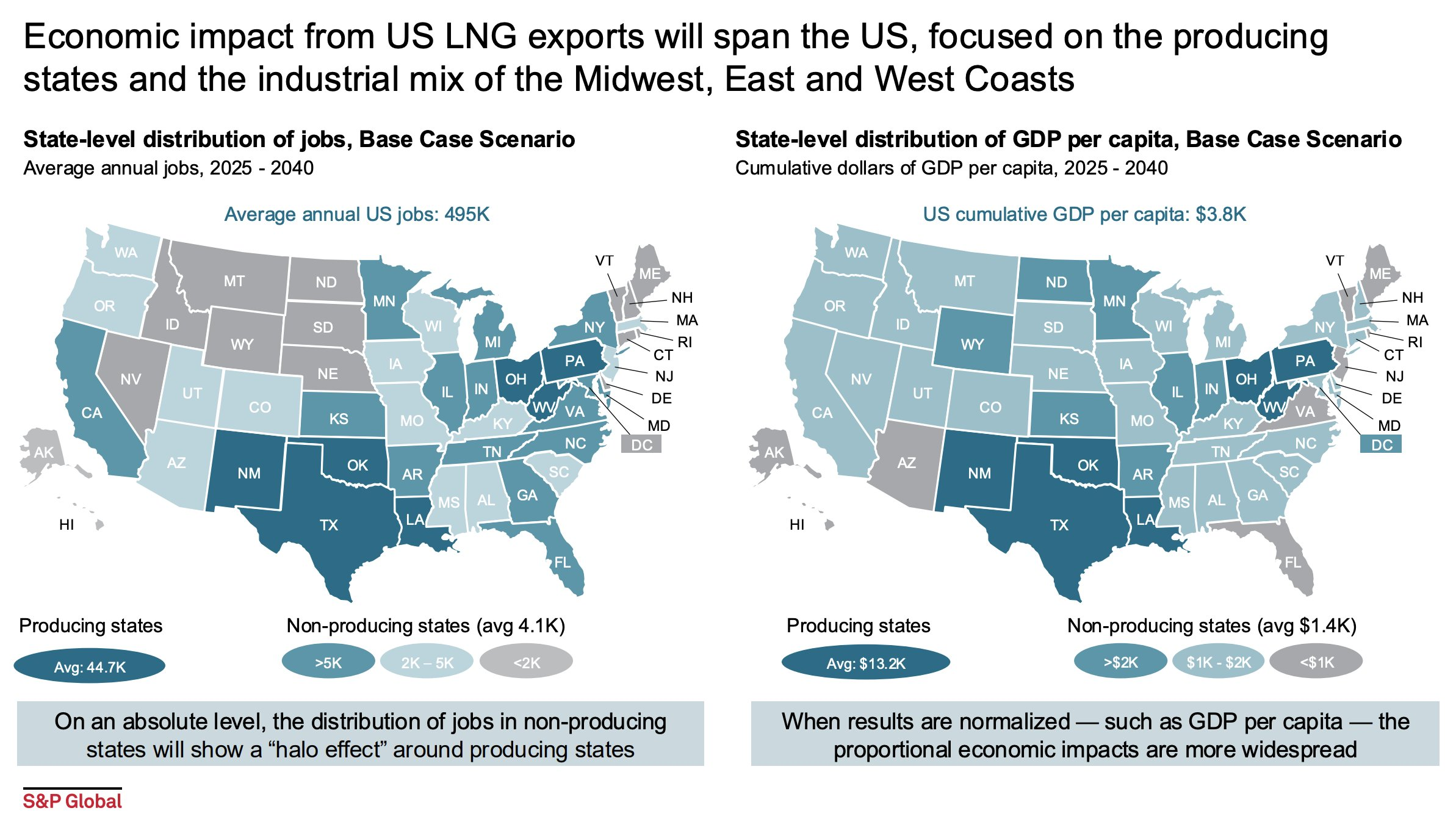

- US LNG’s unprecedented growth is enabled by an extended cross-state value chain, that reaches beyond the core-producing states – about 90% of every dollar spent remains within United States supply chains

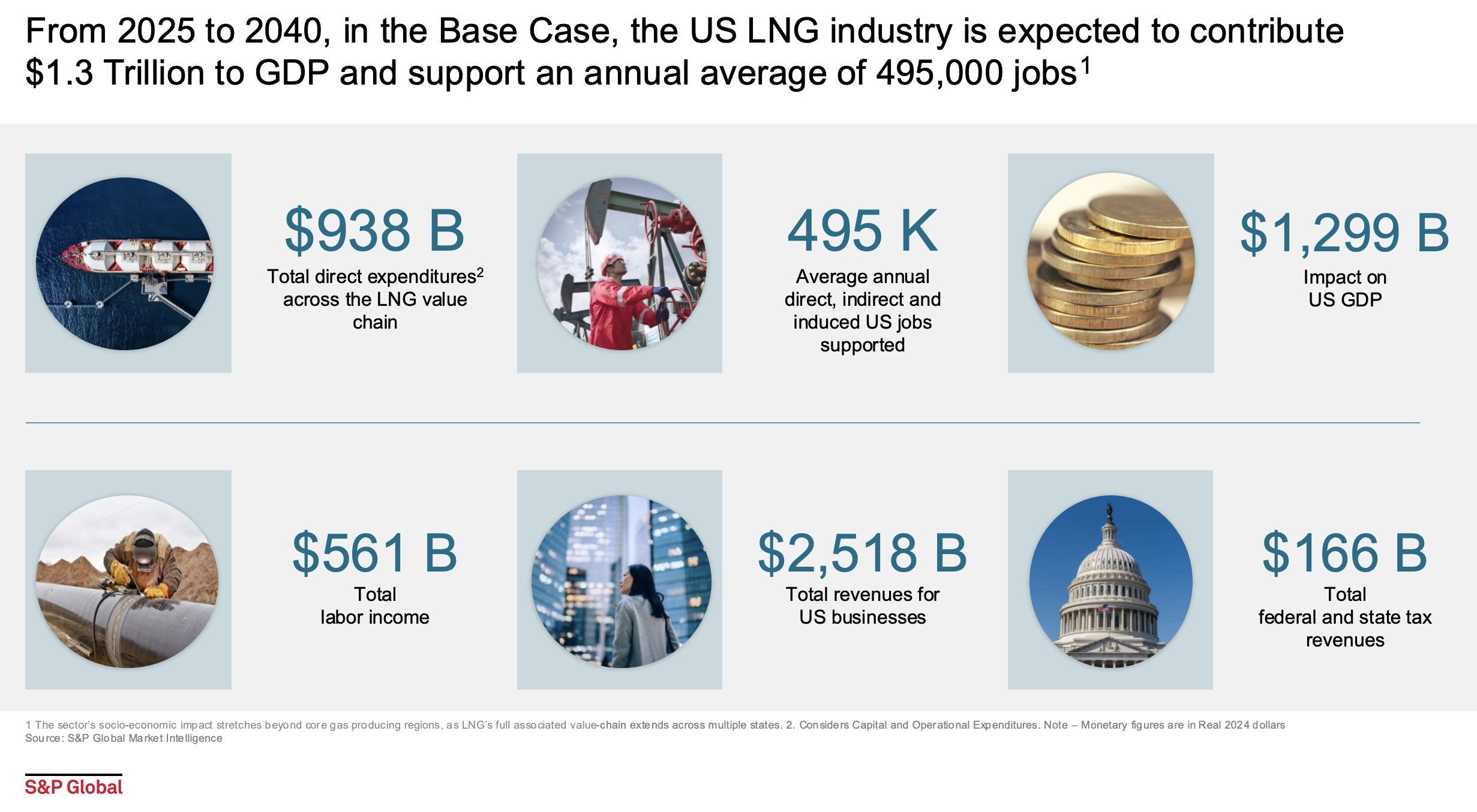

- Of the annual average of 495,000 US jobs supported through 2040, 37% will be in non-producing states. As many jobs will be supported in on-producing states as in Texas

- Over the same period, LNG Exports will contribute $1.3 trillion in GDP, with $383 billion or 30% in non-producing states. On a per capita basis, producing states benefit from a cumulative $13.2K GDP per capita

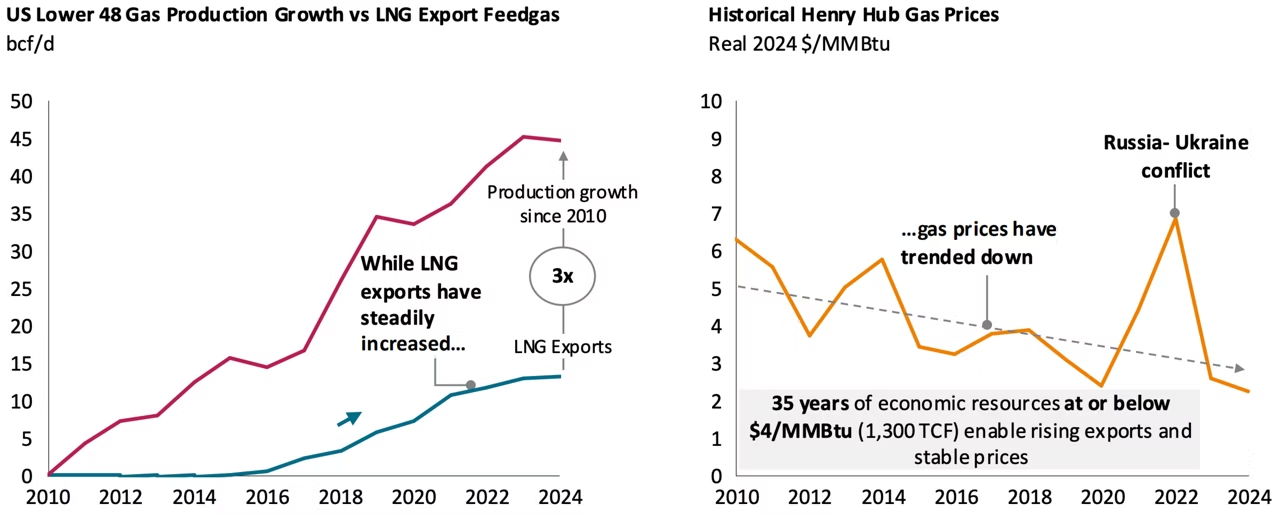

- The US Northeast (NE) has vast amounts of low-cost gas reserves in the Marcellus and Utica formations (New York, Pennsylvania, West Virginia, Ohio), sufficient to meet nationwide demand for ~17 years

- Due to pipeline constraints these reserves are being developed at a suboptimal rate, pushing gas prices at Boston, Chicago and New York City Gates up 160% higher than the national gas market in peak months

- Expanding NE pipeline capacity by 6.1 Bcf/d could reduce HH gas prices by $0.20/MMBtu and significantly lower prices across the region. Cumulative nationwide consumer savings could reach $76 billion through 2040

Should you be interested in learning more, the above findings are well supported by detailed information in the report.