Safety first: As a descendant of troubled Fieldwood Energy, which had a very poor safety and compliance record, QuarterNorth Energy (QNE) had much to prove. That said, QNE has had a good compliance record in its brief 2 year history. During 76 facility inspections in 2022 and 2023, QNE was cited for only 15 Incidents of noncompliance, all but 2 of which were warnings. This is on par with the companies that had the best compliance records during that period.

BSEE’s incident statistics are hopelessly out-of-date, with the latest data being for 2021, so we have limited information on QNE safety incidents. However, BSEE’s District Investigation Reports, which document the more significant incidents, are relatively current and no QNE incidents were investigated in 2022 and 2023.

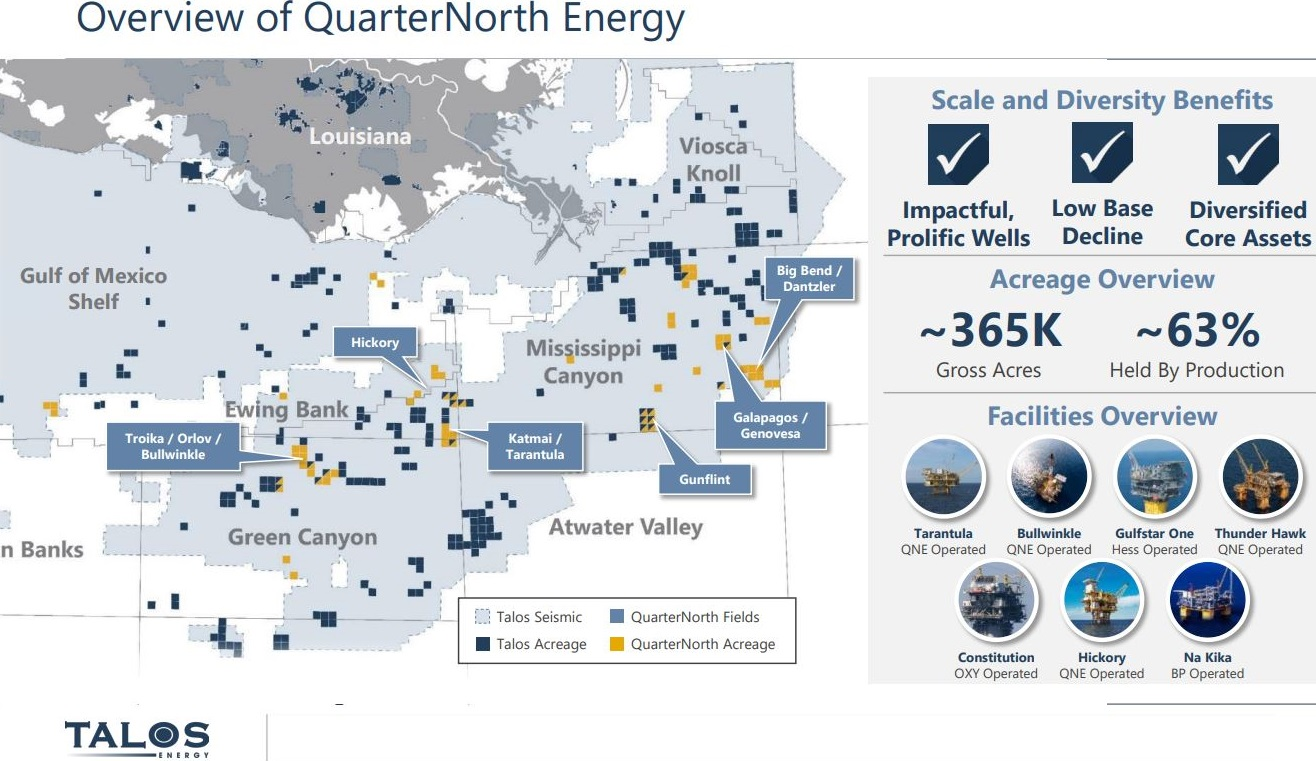

Platforms: Consistent with the general sense that QNE inherited the best of Fieldwood’s facilities, the company’s 15 platforms include Bullwinkle, the Thunder Hawk floating production unit in 6050′ of water, and prominent shelf platforms Tarantula and Hickory.

The acquisition reunites 2 iconic Shell platforms under the same ownership. QNE’s Bullwinkle, installed in 1988 in 1353′ of water, is the world’s tallest (non-compliant) steel tower platform. Talos’s Cognac, installed in 1978 in 1023′ of water, is the first platform in >1000′ of water.

Production and reserves: Per Talos, QNE adds 30,000 boe/d of production and 69 million boe of reserves.

Drilling: Per BSEE records, QNE was the operator for 2 deepwater exploration wells, both of which are classified as completed.

Active leases: The QNE acquisition will add 51 leases to the Talos’s 143 lease inventory.

Recent lease sale activity:

| Sale | QNE | Talos |

| 257 | 2/1 | 10/10 |

| 259 | 6/4 | 5/4 |

| 261 | 6/4 | 14/13 |

Sales price and decommissioning: QNE was already on the market for “more than $2 billion,” shortly after the company was formed. Talos is paying $1.29 billion consisting of 24.8 million shares of Talos’s common stock and approximately $965 million in cash. A case study of the complex Fieldwood bankruptcy and the outcomes for the various parties would be most interesting. Also of interest would be a study of the decommissioning obligations of the former companies and the extent to which the sale proceeds are being applied.